Stock market today: S&P 500 extends monthly win streak despite Nvidia-led stumble

Introduction & Market Context

Encore Capital Group (NASDAQ:ECPG) delivered exceptional second-quarter results for 2025, showcasing record-breaking performance across multiple metrics. The debt purchasing specialist capitalized on favorable market conditions in the United States, where high credit card charge-off rates combined with strong lending activity created robust portfolio supply.

The company’s presentation, delivered on August 6, 2025, highlighted how Encore has leveraged these conditions to drive significant growth in collections, portfolio purchases, and ultimately, shareholder returns.

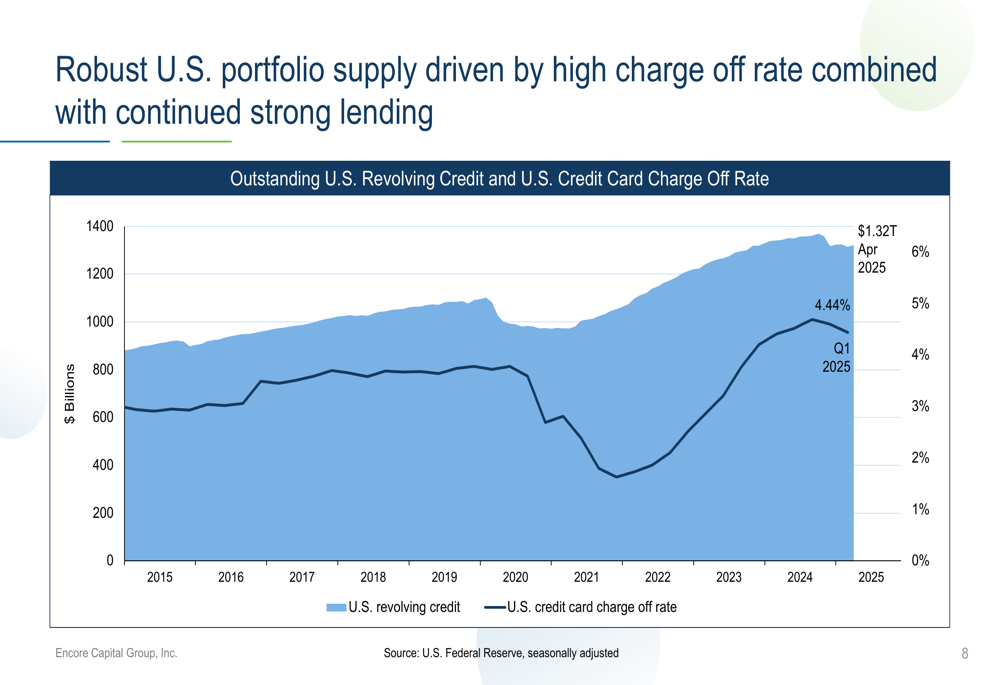

U.S. credit markets continue to provide fertile ground for Encore’s business model, with revolving credit reaching $1.32 trillion as of April 2025 and credit card charge-off rates hitting 4.44%.

As shown in the following chart of U.S. portfolio supply drivers:

Quarterly Performance Highlights

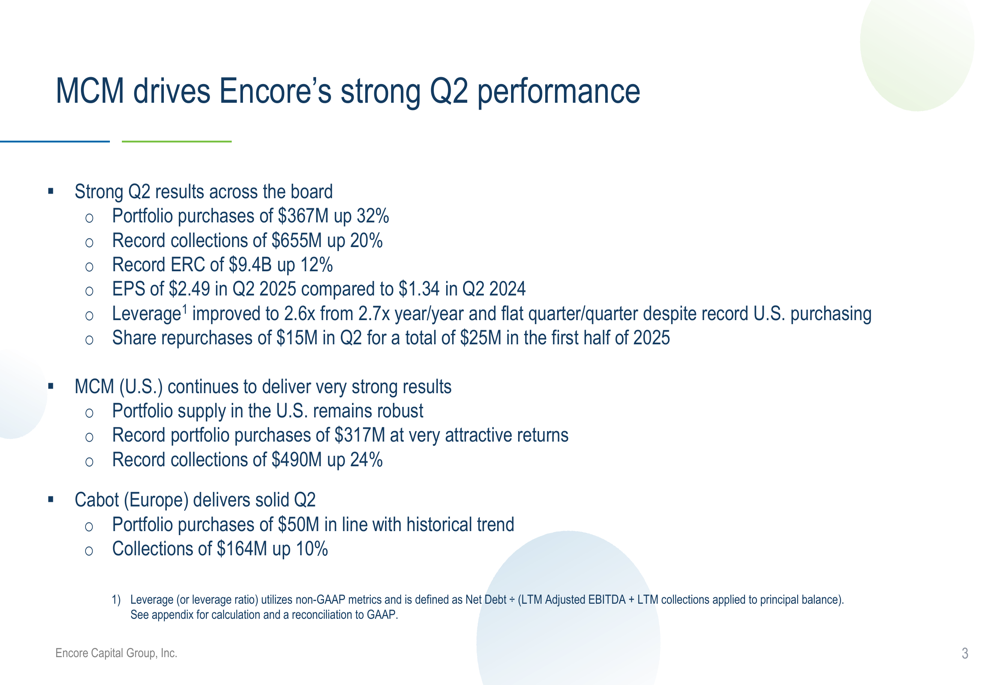

Encore Capital reported earnings per share of $2.49 for Q2 2025, representing an impressive 86% increase from $1.34 in the same quarter last year. This significantly exceeded analyst expectations of $1.39 per share, according to the earnings report.

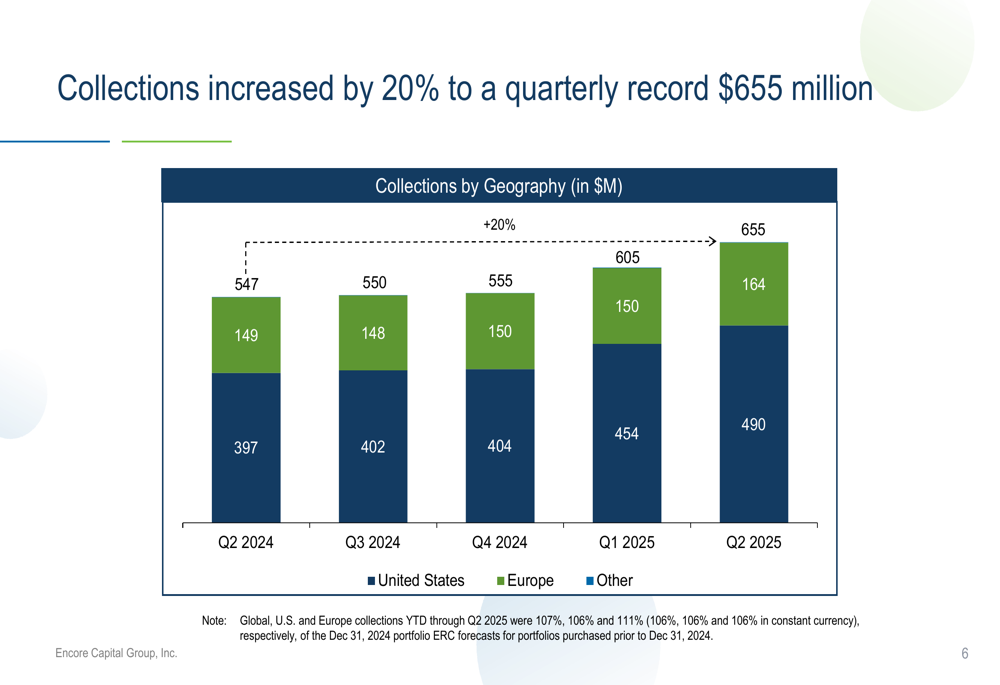

The company achieved record quarterly collections of $655 million, up 20% year-over-year, while portfolio purchases increased by 32% to $367 million. Estimated Remaining Collections (ERC) reached a record $9.4 billion, representing 12% growth compared to Q2 2024.

The following slide illustrates Encore’s strong quarterly performance:

Collections growth has been consistent over the past five quarters, with particularly strong momentum in the most recent period, as shown in this chart:

Portfolio purchasing activity has also accelerated, especially in the U.S. market, which accounted for 86% of total purchases in Q2 2025:

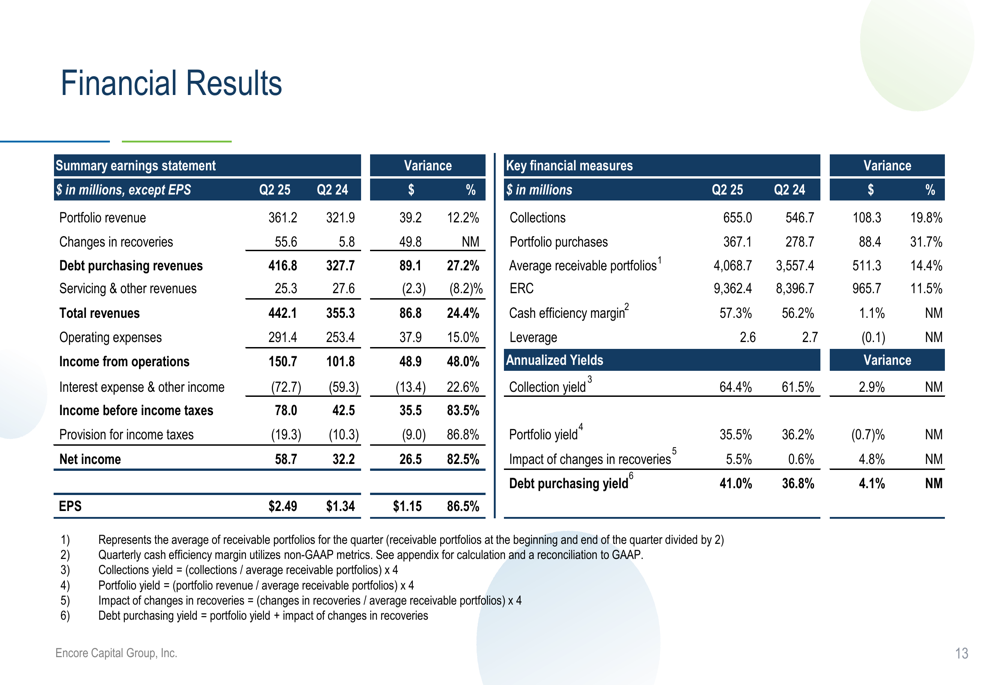

The company’s financial results summary provides a comprehensive view of its performance metrics:

Segment Analysis

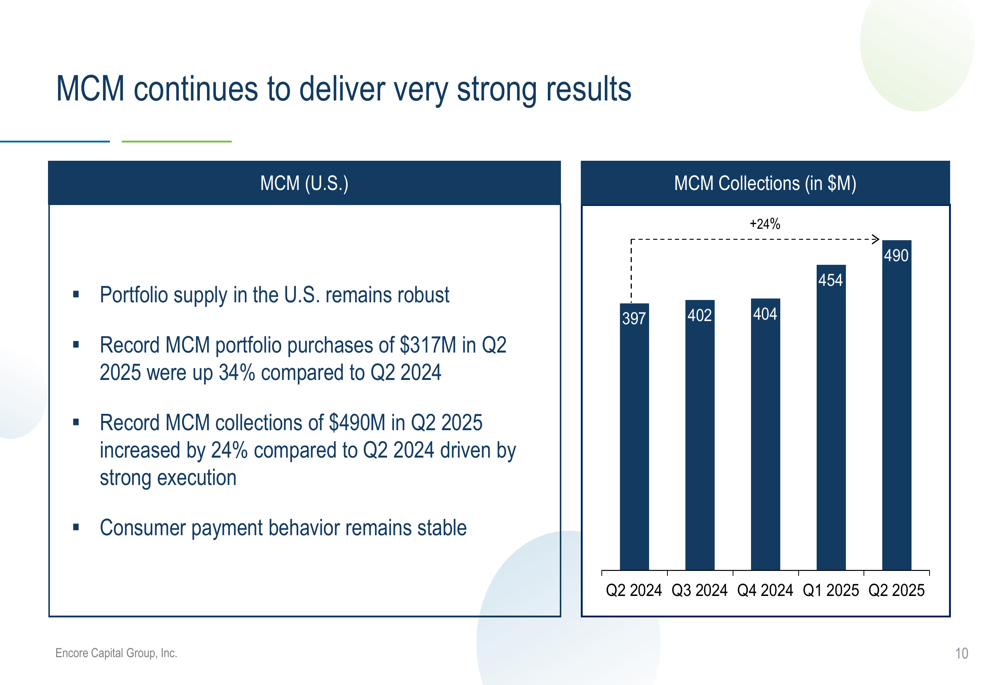

Encore’s U.S. business, operated through Midland Credit Management (MCM), was the primary driver of growth. MCM achieved record portfolio purchases of $317 million in Q2, up 34% year-over-year, and record collections of $490 million, representing a 24% increase from Q2 2024.

The U.S. segment benefited from robust portfolio supply driven by elevated charge-off rates and continued strong lending activity. Consumer payment behavior remained stable despite the challenging economic environment.

As illustrated in the MCM performance chart:

Meanwhile, Encore’s European operations through Cabot (NYSE:CBT) showed more modest growth. Cabot’s collections increased by 10% year-over-year to $164 million, while portfolio purchases remained steady at $50 million, in line with historical trends.

The European segment, particularly the UK market, continues to face challenges including subdued consumer lending, low delinquencies, and robust competition.

Financial Position and Capital Allocation

Encore Capital has maintained a strong financial position while pursuing growth opportunities. The company’s leverage ratio improved to 2.6x from 2.7x year-over-year, despite record U.S. portfolio purchasing activity.

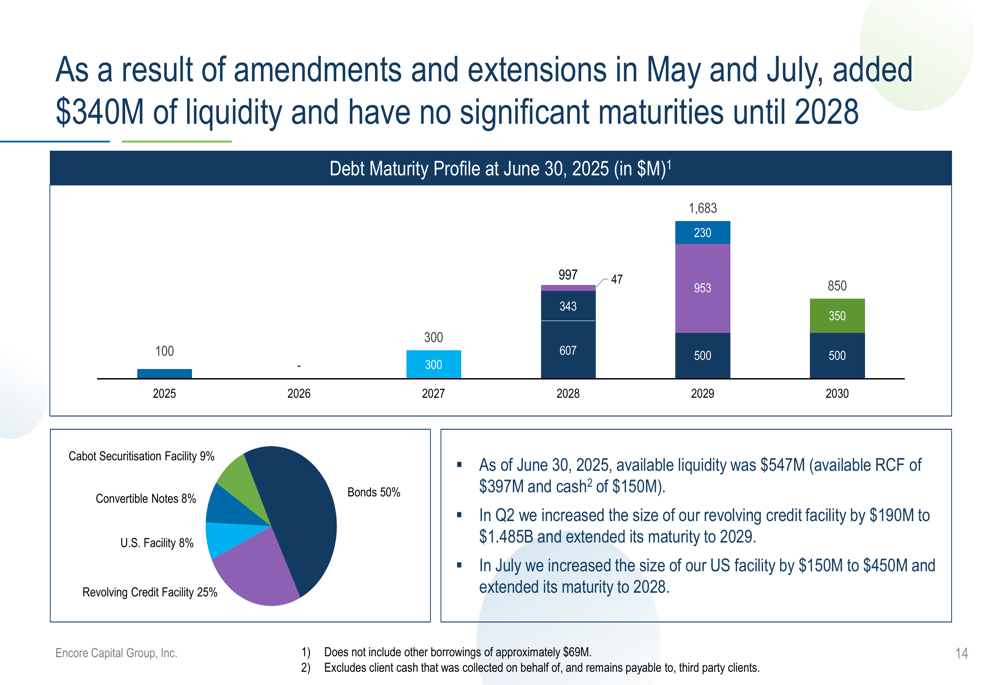

During Q2 2025, Encore repurchased $15 million worth of shares, bringing the total for the first half of 2025 to $25 million. The company also enhanced its liquidity position by adding $340 million of liquidity with no significant debt maturities until 2028.

The debt maturity profile as of June 30, 2025, shows a well-structured financing approach:

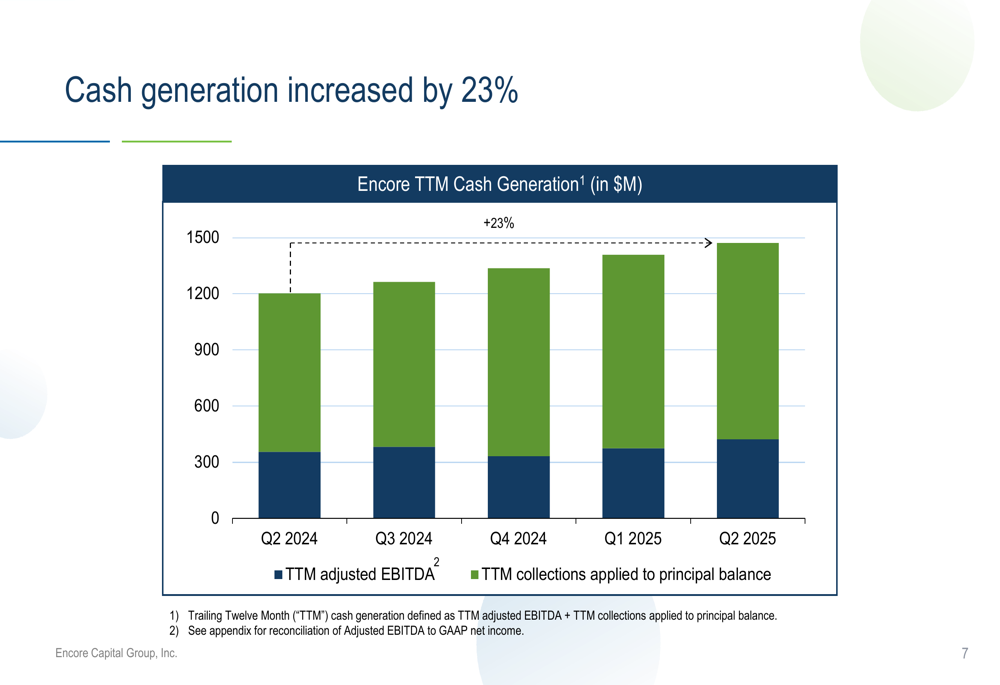

Cash generation has shown consistent growth over the trailing twelve months, increasing by 23% year-over-year:

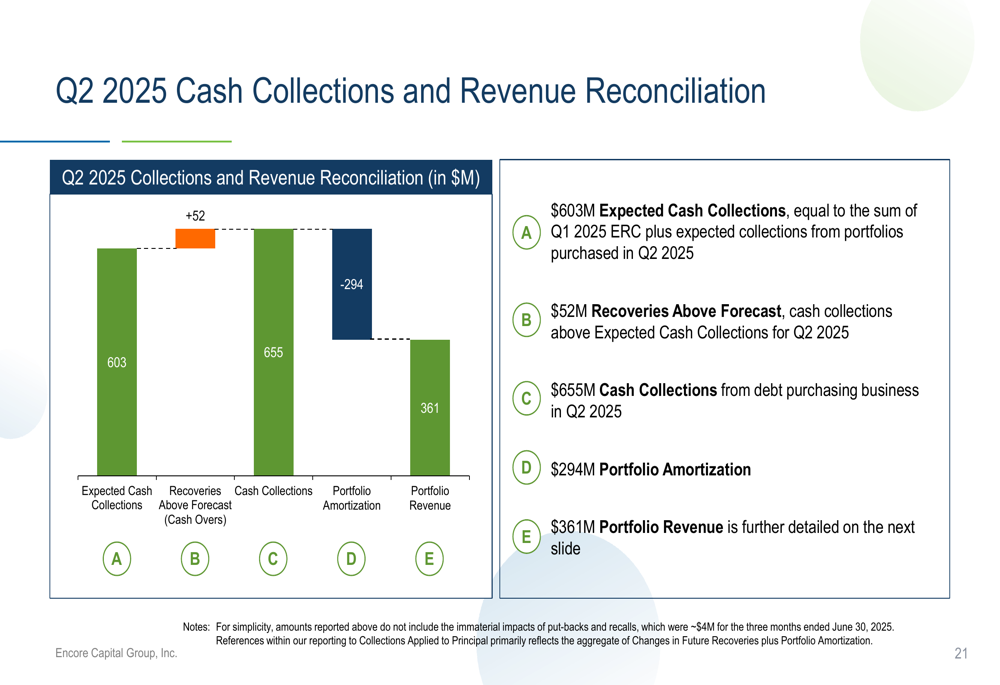

The company’s cash collections and revenue reconciliation provides insight into how collections translate into revenue:

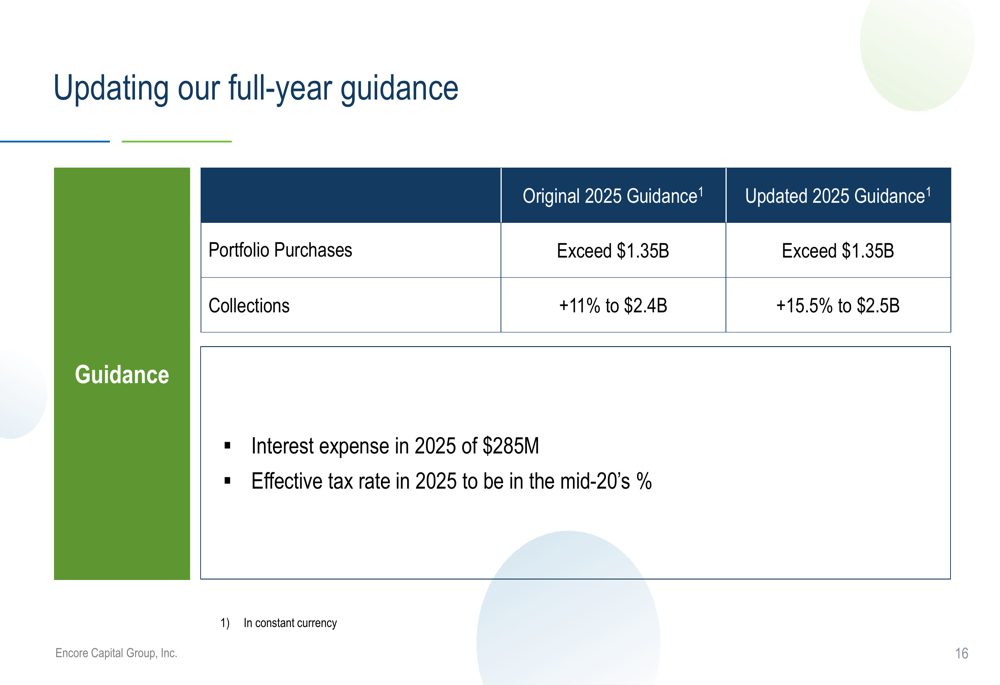

Updated Guidance and Outlook

Based on the strong first-half performance, Encore Capital has raised its full-year guidance for 2025. The company now expects portfolio purchases to exceed $1.35 billion and collections to grow by 15.5% to $2.5 billion.

Interest expense for 2025 is projected to be $285 million, while the effective tax rate is expected to be in the mid-20’s percentage range.

The updated guidance reflects management’s confidence in continued strong performance, particularly in the U.S. market:

Ashish Masih, CEO of Encore Capital, emphasized the company’s strategic focus during the earnings call: "Our mission is to create pathways to economic freedom for the consumers we serve." He added, "We feel really good about our position, how the year is going, and expect this momentum to continue," underscoring the company’s positive outlook.

Following the earnings announcement, Encore Capital’s stock price increased by 2.16% in aftermarket trading, reaching $37.43. While this represents a positive market reaction, the stock remains well below its 52-week high of $51.77, suggesting potential upside if the company continues to deliver strong results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.