Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Energy Transfer LP (NYSE:ET) reported its second quarter 2025 results on August 6, highlighting volume growth across all segments while revealing a sequential decline in adjusted EBITDA. The midstream energy giant’s stock rose 2.37% in after-hours trading to $18.15, building on a 0.71% gain during regular trading hours, as investors responded positively to the company’s continued expansion plans and stable distribution growth.

The company’s presentation emphasized its nationwide footprint and diversified revenue streams, with a particular focus on accelerating investments in natural gas infrastructure to capitalize on growing demand from power generation and data centers.

Quarterly Performance Highlights

Energy Transfer reported Q2 2025 adjusted EBITDA of $3.87 billion, representing a sequential decline from the $4.1 billion reported in Q1 2025. Distributable cash flow attributable to partners reached $1.96 billion for the quarter. The company announced an increase to its quarterly cash distribution to $0.33 per unit, up more than 3% compared to Q2 2024, continuing its track record of distribution growth.

Operational performance showed strength across all segments, with interstate natural gas transportation volumes increasing 11%, midstream gathered volumes up 10%, and crude oil transportation rising 9%. Intrastate natural gas transportation, NGL transportation, and NGL fractionated volumes also showed positive growth at 8%, 4%, and 5% respectively.

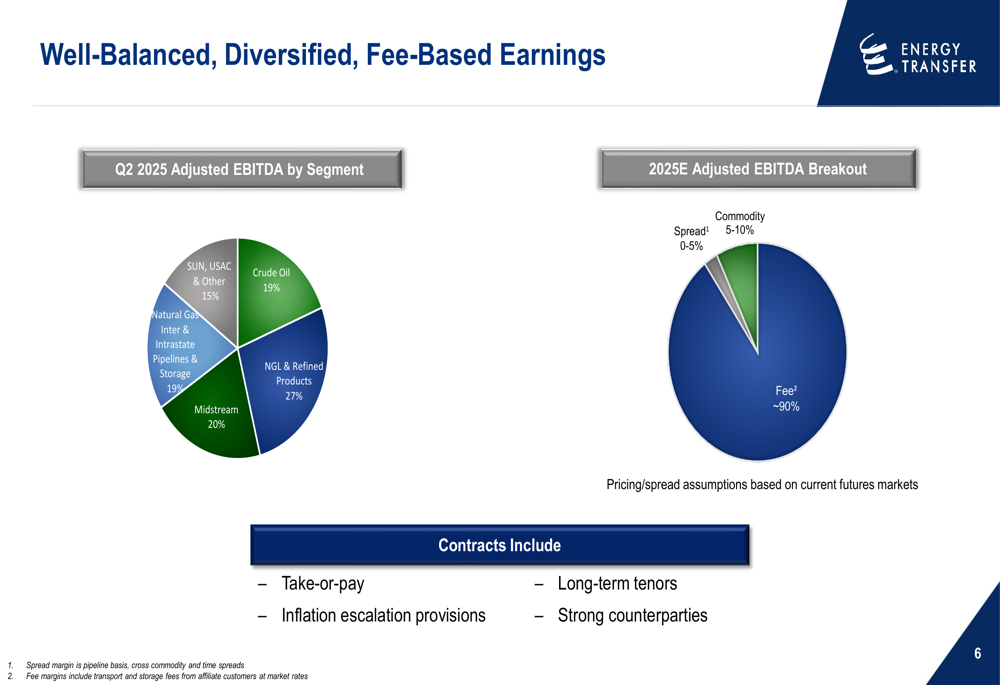

As shown in the following chart of Energy Transfer’s diversified earnings by segment:

The company’s earnings remain well-balanced across multiple business lines, with NGL & Refined Products representing the largest segment at 27% of Q2 2025 adjusted EBITDA. Importantly, approximately 90% of the company’s 2025 expected adjusted EBITDA is fee-based, providing stability and predictability to cash flows despite commodity price fluctuations.

Strategic Initiatives

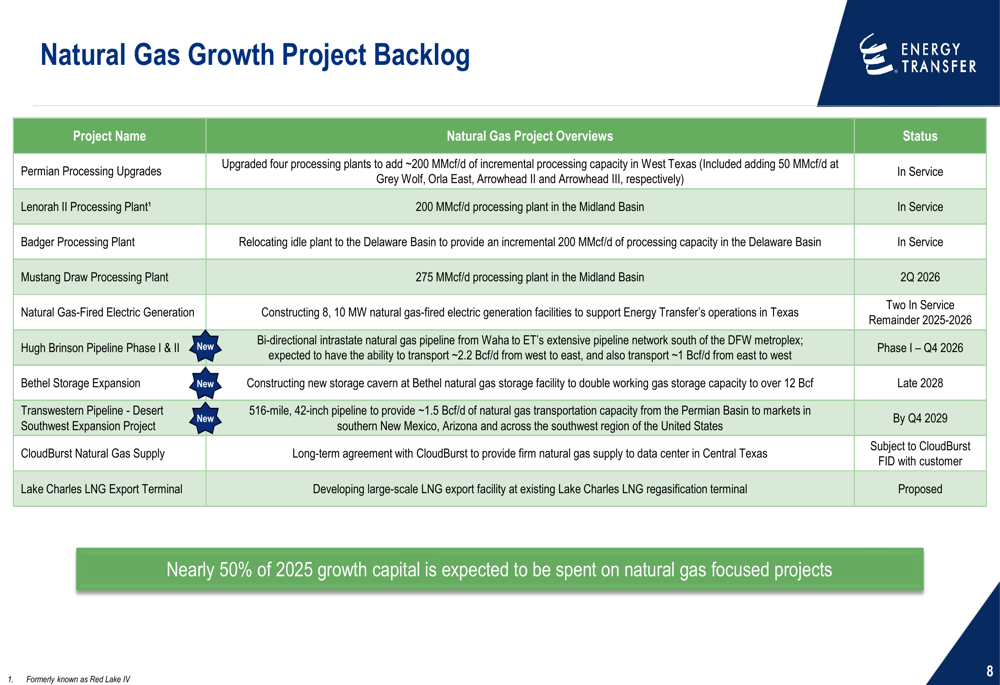

Energy Transfer continues to execute an aggressive growth strategy, maintaining its 2025 growth capital guidance of approximately $5 billion. The allocation of this capital demonstrates the company’s strategic shift toward natural gas infrastructure, with nearly 50% of 2025 growth capital expected to be spent on natural gas-focused projects.

The following breakdown illustrates Energy Transfer’s disciplined approach to capital allocation across its business segments:

A significant portion of the company’s growth capital is directed toward major pipeline expansion projects. The Desert Southwest - Transwestern Pipeline Expansion Project represents one of the largest investments, featuring a 516-mile, 42-inch pipeline from the Permian Basin to Phoenix, Arizona with an expected capacity of approximately 1.5 Bcf/d. This project has an estimated cost of $5.3 billion and is expected to be in service by Q4 2029.

The company’s extensive natural gas project backlog is detailed below:

Another major initiative is the Hugh Brinson Pipeline Project, which includes two phases. Phase I consists of 400 miles of 42-inch pipeline from Waha and the Midland Basin to Maypearl, Texas, with approximately 1.5 Bcf/d capacity, expected to be in service in Q4 2026. Phase II will add compression, making the pipeline bi-directional with the ability to transport approximately 2.2 Bcf/d from west to east and approximately 1 Bcf/d from east to west. The total capital for both phases is expected to be approximately $2.7 billion.

Competitive Industry Position

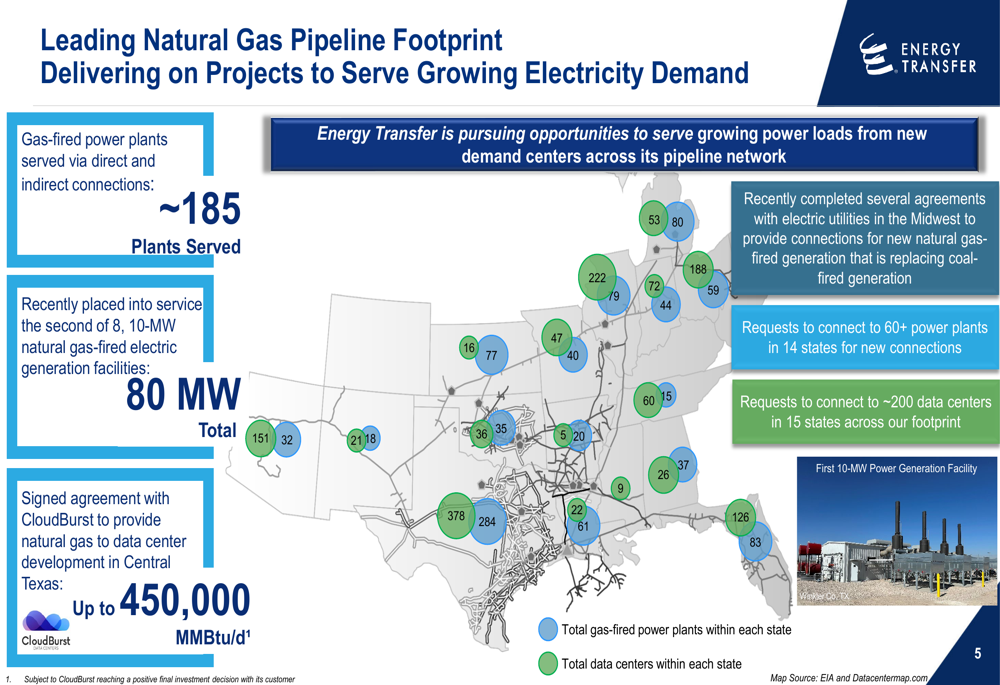

Energy Transfer’s nationwide asset footprint positions the company as one of the most diversified midstream operators in the United States. The company’s natural gas pipeline network serves approximately 185 gas-fired power plants, with connection requests from more than 60 additional plants. The growing data center market represents a significant opportunity, with Energy Transfer noting potential demand of up to 450,000 MMBtu/d from CloudBurst Data Centers alone.

The following map illustrates the company’s extensive natural gas pipeline network and its strategic positioning to serve electricity demand:

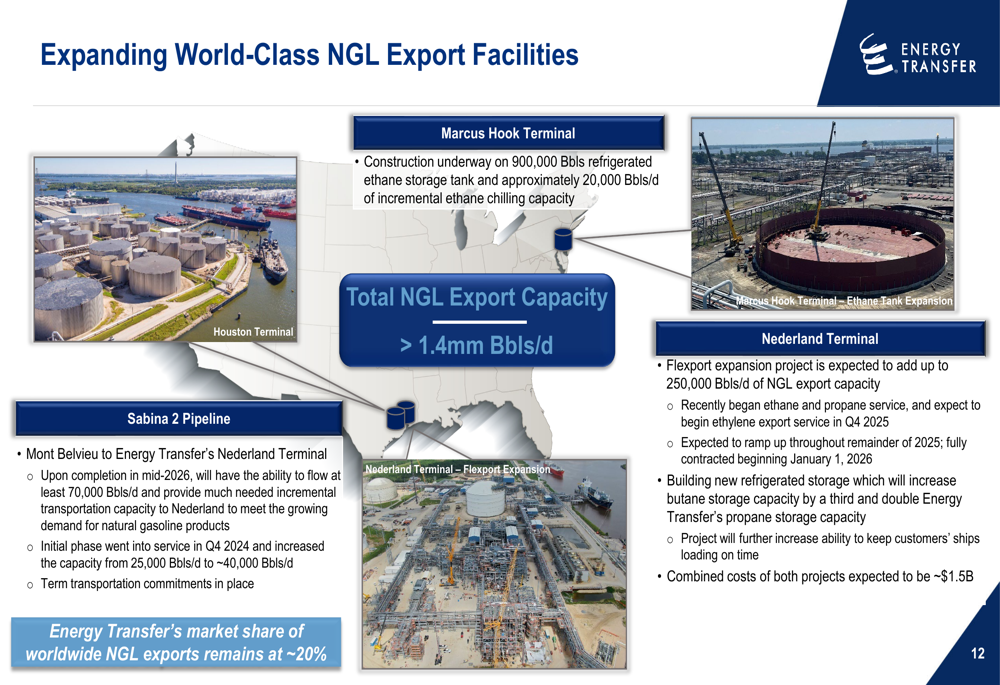

In the NGL export market, Energy Transfer maintains approximately 20% global market share. The company continues to expand its export capabilities through projects at both its Marcus Hook and Nederland terminals, with a combined investment of approximately $1.5 billion. These expansions include a 900,000 barrel refrigerated ethane storage tank at Marcus Hook and the Flexport expansion at Nederland, which is expected to add up to 250,000 barrels per day of NGL export capacity.

Forward-Looking Statements

Energy Transfer’s presentation highlighted several key developments that will drive future growth. The company recently reached final investment decision (FID) on Phase II of the Hugh Brinson Pipeline project and on the construction of a new storage cavern at the Bethel natural gas storage facility, which will double the natural gas working storage capacity at the facility to over 12 Bcf.

The Lake Charles LNG project continues to advance, with Energy Transfer signing a Heads of Agreement (HOA) with MidOcean Energy for the joint development of the project. This represents a significant step forward for what could become a major LNG export facility.

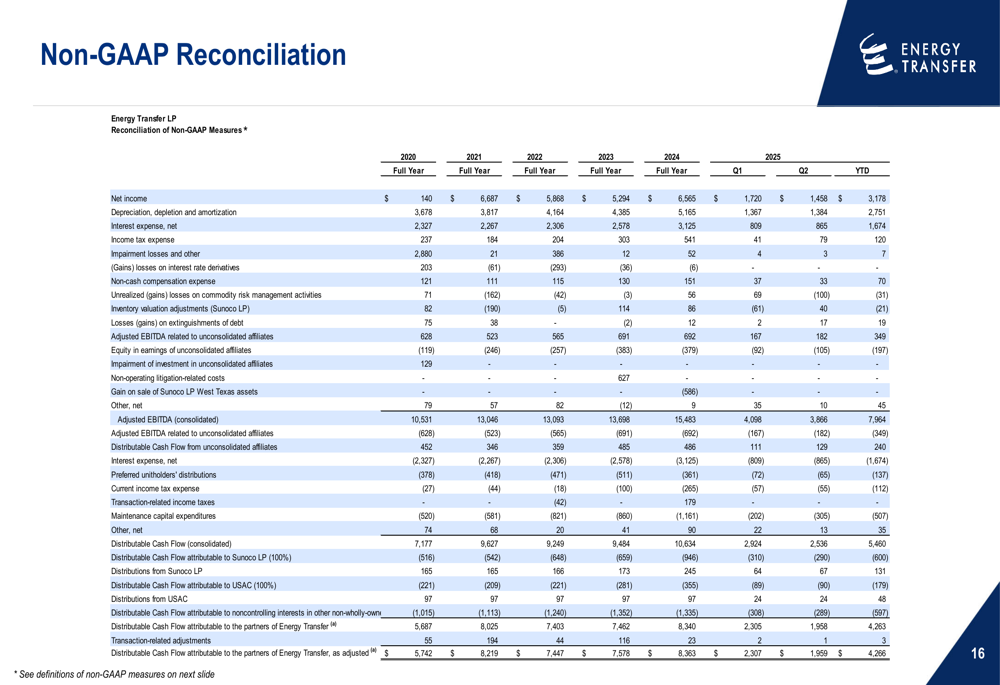

The company’s historical financial performance shows consistent growth in adjusted EBITDA over the past several years:

Energy Transfer is also advancing sustainability initiatives, including the construction of eight 10-MW natural gas-fired electric generation facilities with a total capacity of 80 MW. The company sources 20% of its power from solar and wind, and expects 790,000 tons of emissions reduction from its Dual Drive technology.

While the presentation maintains an optimistic outlook, investors should note that the Q1 2025 earnings report highlighted potential risks including gas supply slowdown in certain production basins, fluctuations in international demand for NGLs, and market softening that could defer planned projects. The sequential decline in adjusted EBITDA from Q1 to Q2 2025 also warrants monitoring in future quarters.

As Energy Transfer continues its strategic pivot toward natural gas infrastructure, the company appears well-positioned to capitalize on growing demand from power generation and data centers, while maintaining its diversified business model and stable distribution growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.