Fed governors may dissent against Powell amid Trump pressure - WSJ’s Timiraos

Introduction & Market Context

Enghouse Systems Ltd (TSX:ENGH) presented its Q2 FY2025 corporate results on June 6, 2025, revealing a mixed performance characterized by stable revenue but declining profitability. Following the presentation, Enghouse shares dropped 9.85%, closing at $23.71, significantly below the company’s 52-week high of $34.42.

The Canada-headquartered software company, which operates in over 25 countries with approximately 1,900 employees, continues to pursue its dual growth strategy of organic expansion and strategic acquisitions, despite facing headwinds in its Interactive Management Group segment.

Quarterly Performance Highlights

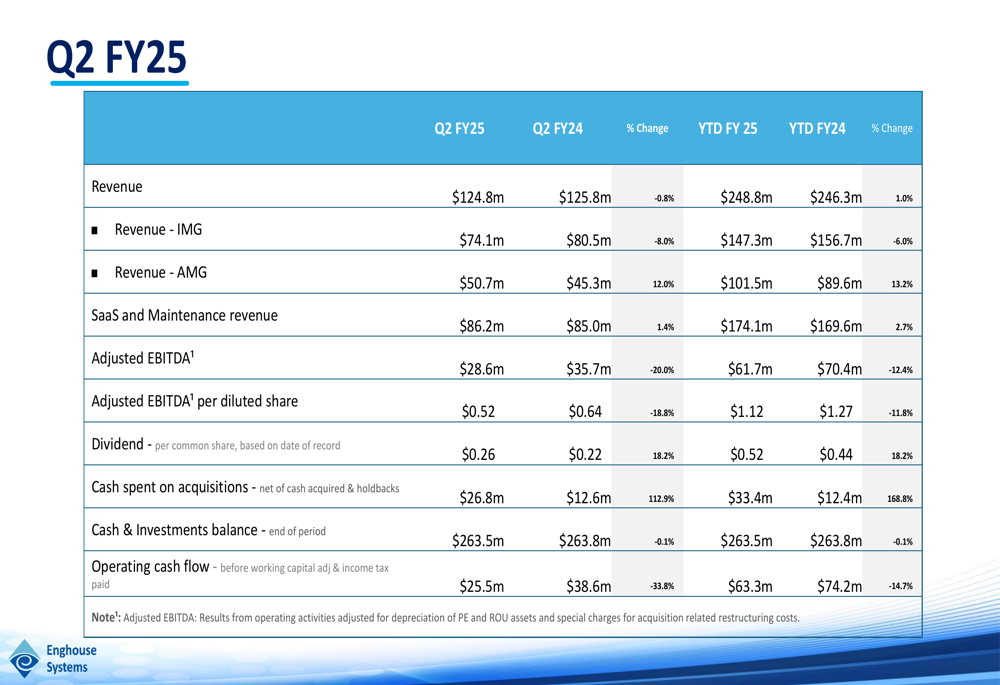

Enghouse reported Q2 FY2025 revenue of $124.8 million, representing a slight decrease of 0.8% compared to the same period last year. The company’s performance revealed a stark contrast between its two business segments, with the Asset Management Group (AMG) growing 12.0% year-over-year to $50.7 million, while the Interactive Management Group (IMG) declined 8.0% to $74.1 million.

As shown in the following comprehensive quarterly results table:

The company’s recurring revenue streams showed resilience, with SaaS and Maintenance revenue increasing 1.4% to $86.2 million, now representing approximately 69% of total revenue. However, profitability metrics declined significantly, with Adjusted EBITDA falling 20.0% to $28.6 million and Adjusted EBITDA per diluted share decreasing 18.8% to $0.52.

The quarterly results missed analyst expectations, with actual EPS of $0.24 falling short of the forecasted $0.3757, and revenue below the anticipated $129.64 million. Operating cash flow also declined substantially, down 33.8% to $25.5 million compared to the same quarter last year.

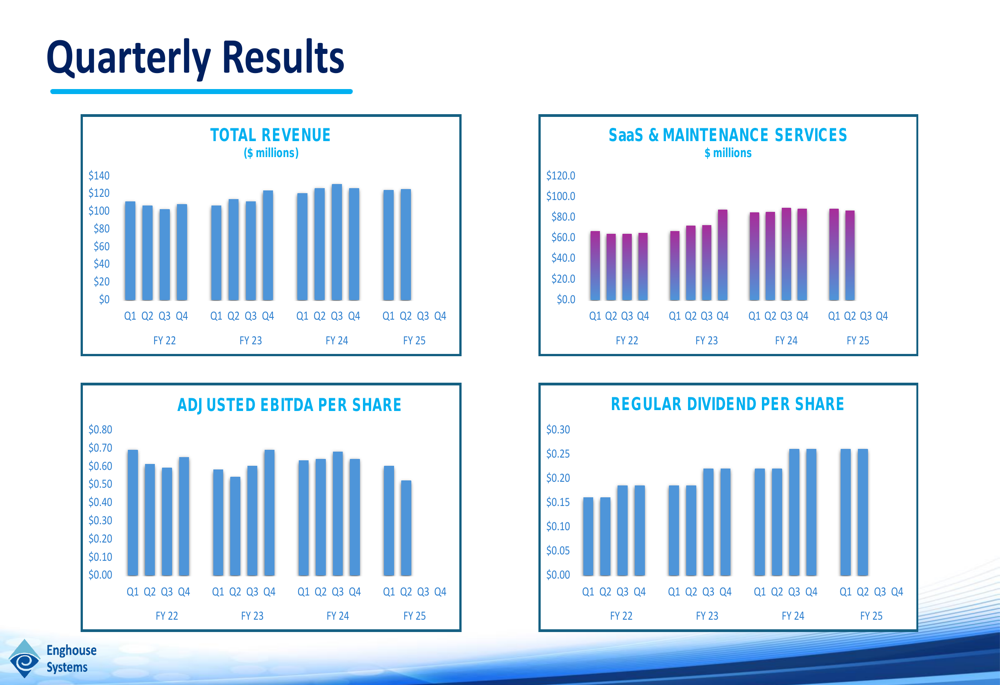

Looking at the longer-term quarterly trends, Enghouse has shown relatively consistent revenue but fluctuating profitability:

Strategic Initiatives

Despite profitability challenges, Enghouse continues to aggressively pursue its acquisition strategy, more than doubling its spending on acquisitions in Q2 FY2025 to $26.8 million, compared to $12.6 million in the same period last year.

The company’s acquisition approach targets businesses in the $5-$50 million revenue range, preferably with strong recurring revenue, geographic or product expansion potential, and high barriers to entry. Enghouse aims for a cash-on-cash payback within 5-7 years on these investments.

As illustrated in the recent acquisitions slide, the company has maintained an active M&A strategy across multiple geographies:

During the earnings call, CEO Steven Sadler addressed challenges in monetizing AI benefits, noting, "AI continues to be promoted in discussions, but there’s great difficulty in monetizing its benefits." This sentiment reflects broader industry challenges in translating technological advancements into revenue growth.

Detailed Financial Analysis

Enghouse maintains a strong financial position with $263.5 million in cash and investments and no external debt, providing flexibility for future acquisitions and shareholder returns. The company increased its quarterly dividend by 18.2% year-over-year to $0.26 per share, continuing its 19-year track record of dividend growth.

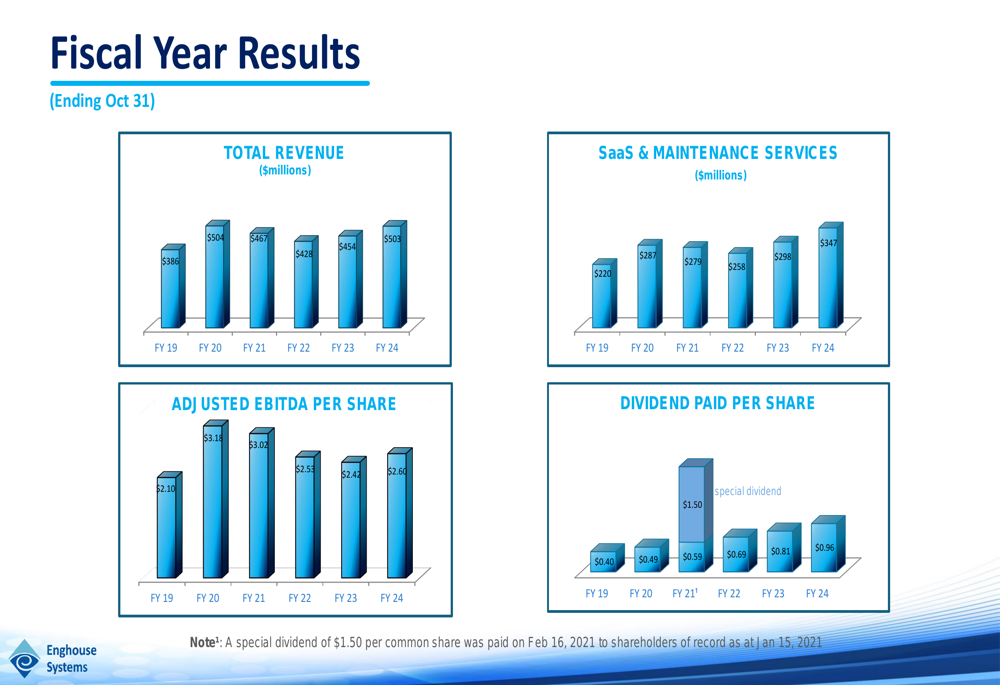

The multi-year financial trends show steady revenue growth but recent pressure on profitability metrics:

The divergence between segments is particularly noteworthy. The Asset Management Group, which includes Networks and Transportation & Public Safety solutions, is showing strong momentum with 12.0% growth. This segment provides critical infrastructure software for telecom operators, transit companies, and public safety organizations.

Meanwhile, the Interactive Management Group, which offers contact center, video interaction, and customer experience solutions, is facing more significant challenges with an 8.0% revenue decline:

Forward-Looking Statements

CFO Rob Bevitt emphasized the company’s strategic positioning during the earnings call, stating, "We believe that periods of uncertainty often create opportunities for well-capitalized disciplined companies like Enghouse to strengthen their market position."

The company faces several challenges moving forward, including slow enterprise decision-making, geopolitical instability, foreign exchange volatility, and the ongoing transition from 4G to 5G technology. Competitors struggling with profitability could also impact market dynamics.

Despite these challenges, Enghouse remains committed to its acquisition strategy and continues to explore opportunities in AI and SaaS. The company’s strong cash position and debt-free balance sheet provide a solid foundation for navigating market uncertainties while continuing to return value to shareholders through growing dividends.

Investors will be watching closely to see if Enghouse can reverse the profitability decline while maintaining its dividend growth trajectory in the coming quarters. The divergence between segment performances suggests potential strategic decisions may be needed to address underperforming areas while capitalizing on strengths in the growing Asset Management Group.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.