Asia FX muted despite Fed cut bets; Japanese yen slides after PM Ishiba resigns

Introduction & Market Context

Enghouse Systems Ltd (TSX:ENGH) released its Q3 FY25 corporate presentation on September 5, 2025, revealing a 3.8% year-over-year revenue decline amid challenging market conditions. The Canadian software company’s stock fell 10.03% following the presentation, reflecting investor concerns about the company’s performance trajectory.

The presentation comes after Enghouse missed both revenue and earnings expectations in its previous quarter. According to the company’s current financial position, Enghouse maintains a strong cash position of $271.6 million, up 5.0% from the same period last year, providing stability despite operational headwinds.

Quarterly Performance Highlights

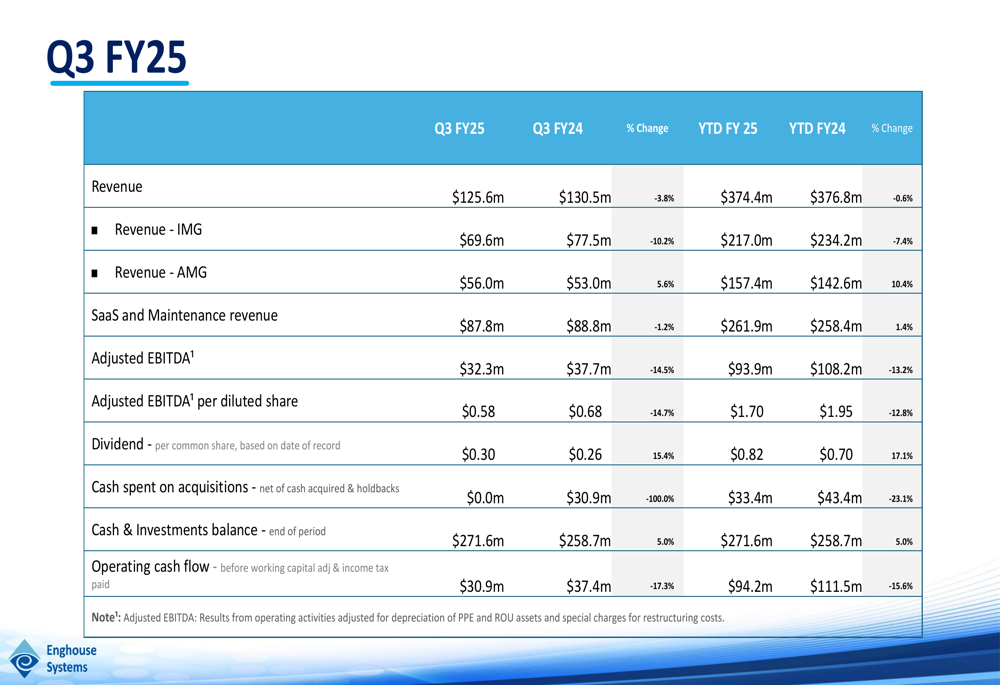

Enghouse reported Q3 FY25 revenue of $125.6 million, down 3.8% compared to $130.5 million in Q3 FY24. Year-to-date revenue reached $374.4 million, representing a slight 0.6% decline from the prior year period. More concerning was the 14.5% drop in adjusted EBITDA to $32.3 million and a 14.7% decrease in adjusted EBITDA per diluted share to $0.58.

As shown in the following detailed quarterly results table:

Despite the overall revenue decline, Enghouse maintained relative stability in its recurring revenue streams, with SaaS and maintenance revenue reaching $87.8 million, down just 1.2% year-over-year. This represents approximately 70% of total revenue, highlighting the company’s focus on building stable, long-term revenue sources.

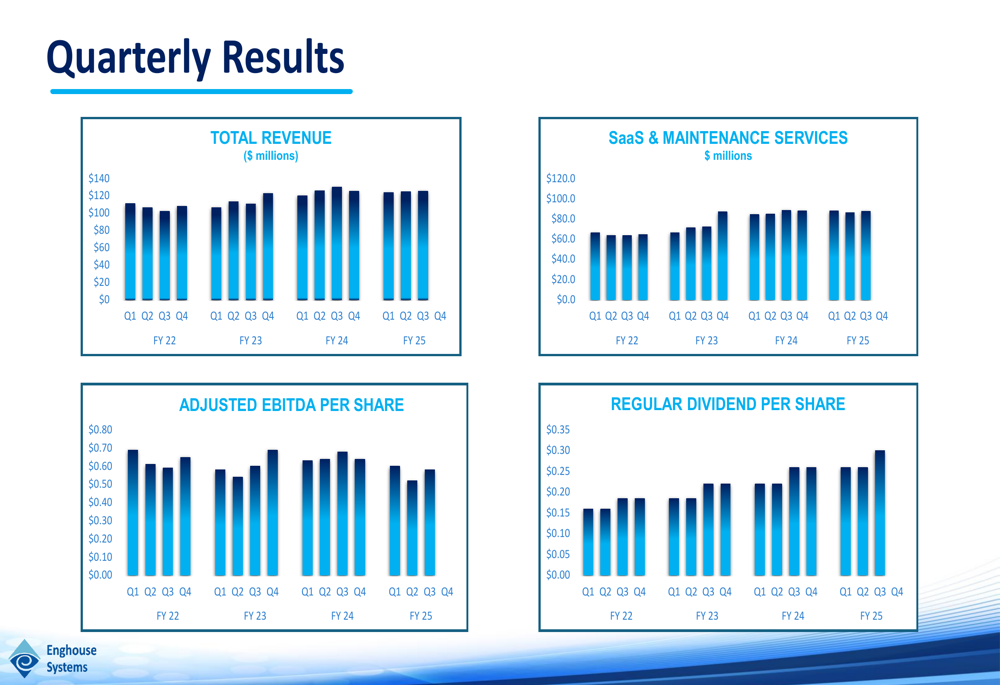

The company’s quarterly dividend increased by 15.4% to $0.30 per share, continuing Enghouse’s commitment to returning value to shareholders despite operational challenges. This is visualized in the quarterly trends chart:

Segment Performance Analysis

A notable divergence emerged between Enghouse’s two main business segments. The Interactive Management Group (IMG) saw a significant 10.2% revenue decline to $69.6 million in Q3 FY25, while the Asset Management Group (AMG) delivered 5.6% growth, reaching $56.0 million.

The IMG segment focuses on customer interaction solutions including video collaboration, contact centers, and specialty products for marketing communications and telecom expense management. Its comprehensive portfolio includes:

Meanwhile, the AMG segment, which includes the Networks Group and Transportation & Public Safety Group, continued to show strength. This segment provides technology solutions to communications, media, utilities, and defense organizations, as well as software for transit, supply chain, and public safety applications.

The Transportation & Public Safety portfolio has been a particular bright spot within AMG:

Acquisition Strategy & Recent Deals

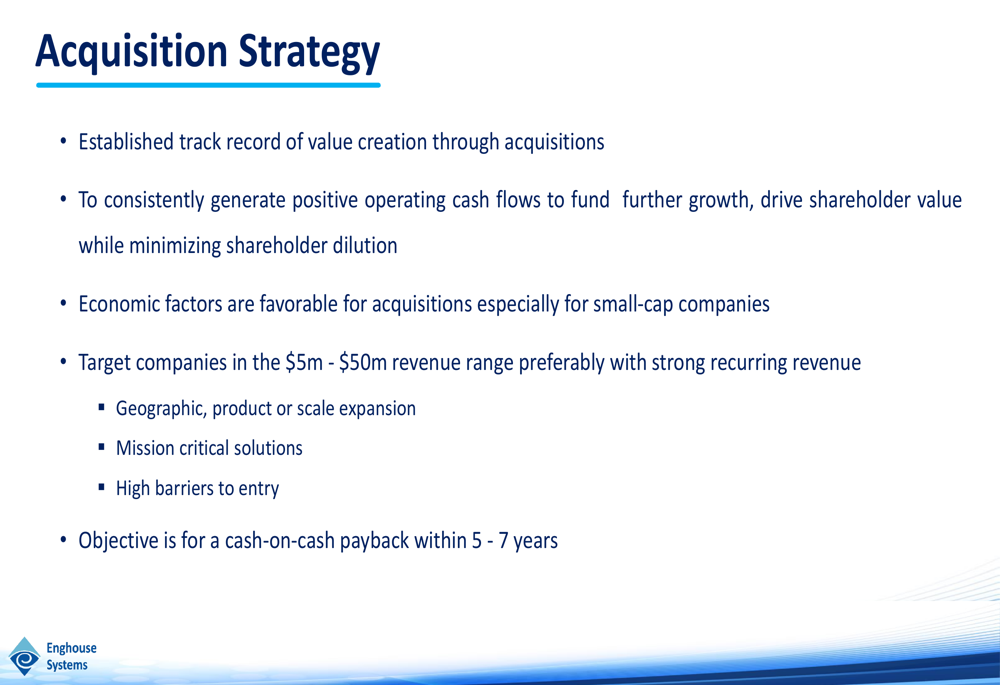

Enghouse continues to emphasize its dual growth strategy combining organic expansion with strategic acquisitions. The company targets businesses in the $5-$50 million revenue range with strong recurring revenue profiles, aiming for a cash-on-cash payback within 5-7 years.

The company’s acquisition approach is outlined as follows:

Recent acquisitions have expanded Enghouse’s global footprint and diversified its product portfolio. Over the past two years, the company has completed seven acquisitions across multiple countries, including Lifesize and Mediasite in the USA, AccuLab in England, and Margento in Slovenia.

In Q3 FY25, Enghouse did not complete any new acquisitions, compared to $30.9 million spent in the same quarter last year. Year-to-date, acquisition spending reached $33.4 million, down 23.1% from the prior year period.

Forward-Looking Statements

Despite current headwinds, Enghouse maintains a strong financial foundation with $271.6 million in cash and investments and no external debt. This positions the company to continue its acquisition strategy even in a challenging economic environment.

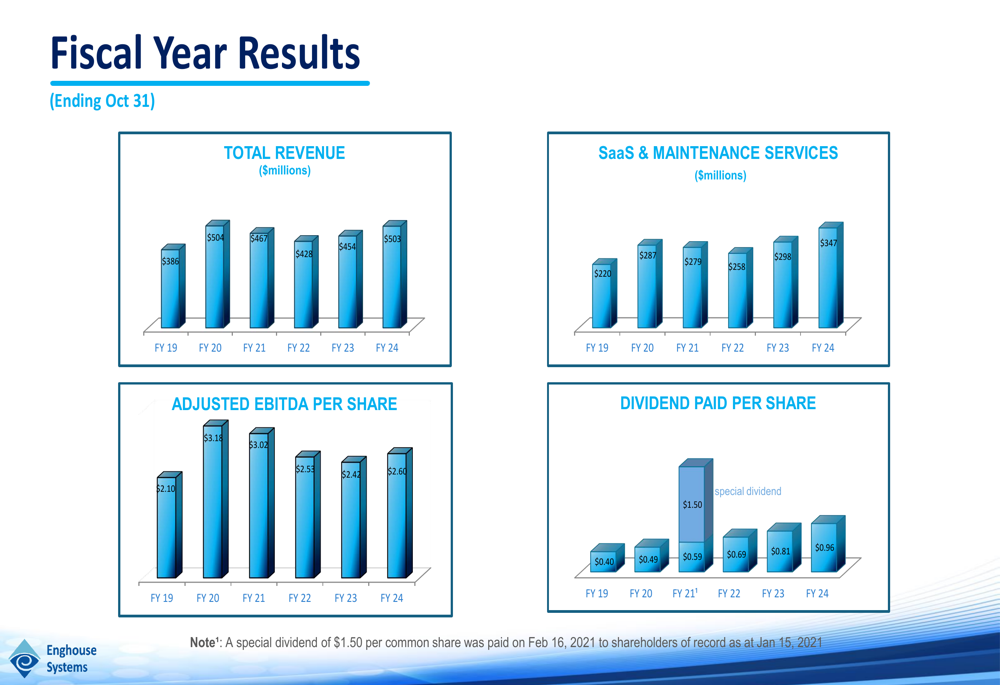

The company’s long-term performance shows steady revenue growth from $386 million in FY19 to $504 million in FY24, with recurring revenue from SaaS and maintenance services increasing from $220 million to $347 million over the same period.

However, the recent quarterly performance raises questions about Enghouse’s near-term growth trajectory. The significant decline in the IMG segment, which historically has been a strong performer, will require management attention to reverse the trend.

With the stock price dropping 10.03% following the presentation, investors appear concerned about the company’s ability to return to growth. Management will need to demonstrate that its acquisition strategy can effectively counter organic growth challenges while improving operational efficiency to address the concerning decline in adjusted EBITDA.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.