How are energy investors positioned?

Introduction & Market Context

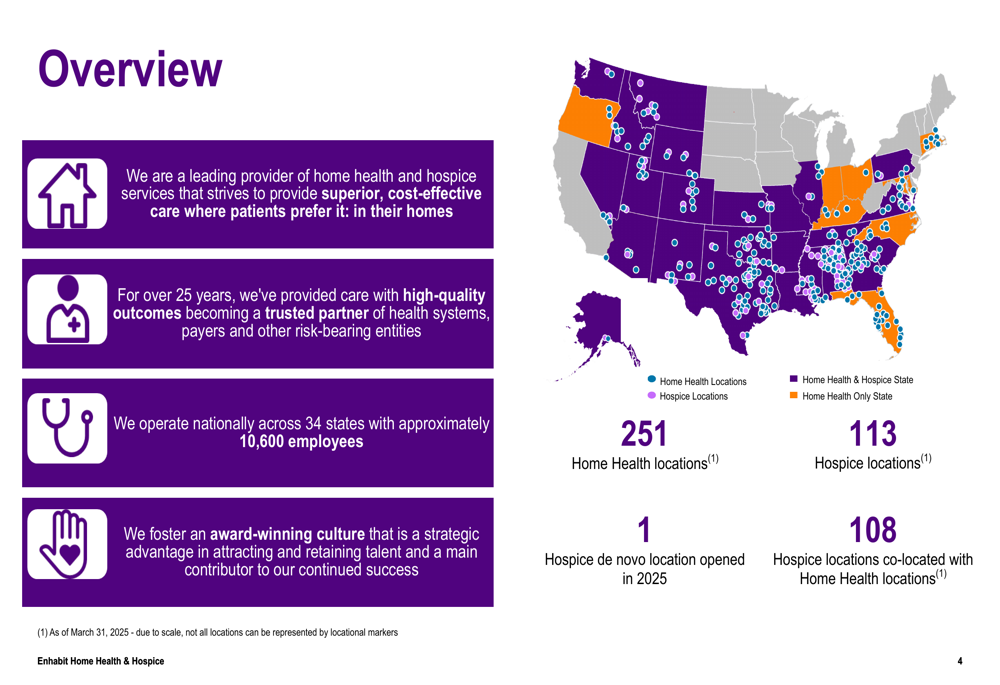

Enhabit Inc. (NYSE:EHAB), a leading provider of home health and hospice services, presented its first quarter 2025 earnings results on May 8, 2025. The company, which operates in 34 states with 251 home health and 113 hospice locations, showed mixed segment performance while making progress on key financial metrics.

The presentation comes after a challenging Q4 2024, when the company missed earnings expectations, resulting in a significant stock drop. However, the company’s shares have shown some recovery, closing at $8.20 on May 7, 2025, up 1.99% ahead of the earnings call.

As shown in the following overview of Enhabit’s national footprint and operations:

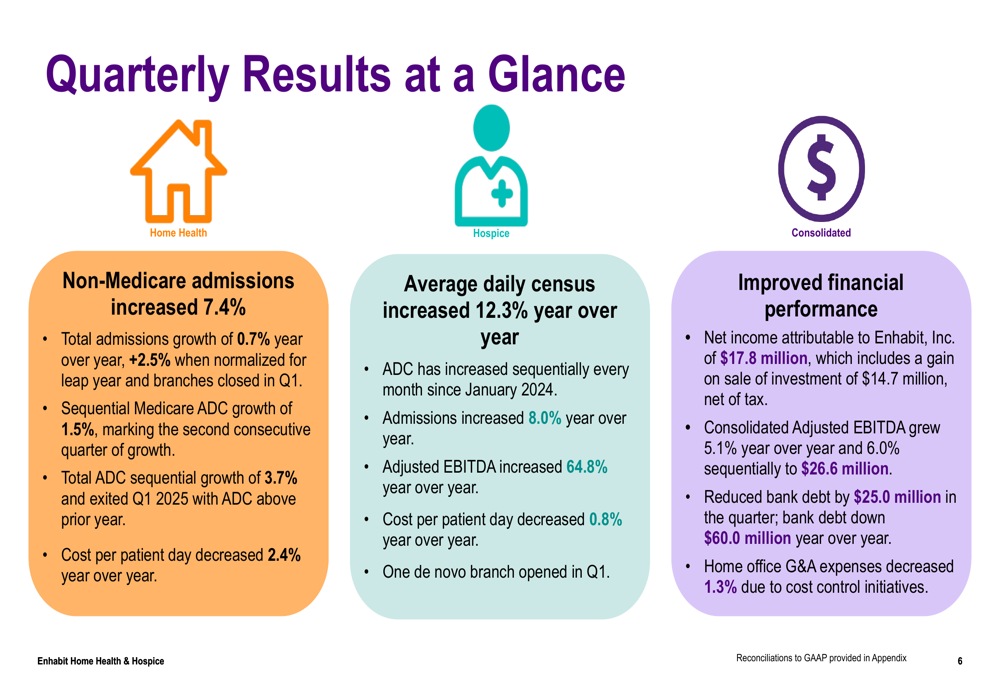

Quarterly Performance Highlights

Enhabit reported Q1 2025 net income attributable to the company of $17.8 million, which included a $14.7 million gain on sale of investment (net of tax). Consolidated Adjusted EBITDA grew 5.1% year-over-year to $26.6 million, representing a 6.0% sequential improvement from Q4 2024.

Total (EPA:TTEF) net service revenue was $259.9 million, down 1.0% compared to Q1 2024, but the company improved its gross margin to 49.9% from 48.9% in the prior year period. Adjusted EBITDA margin expanded to 10.2% from 9.6% year-over-year.

The following slide summarizes the key quarterly results:

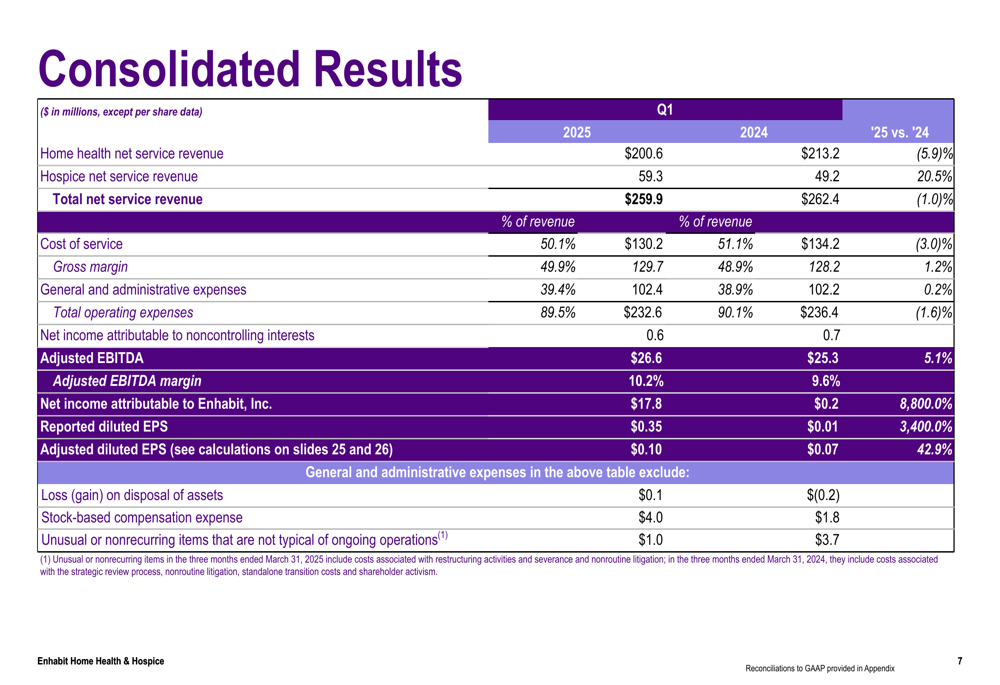

A more detailed breakdown of the consolidated financial results shows the contrast between segment performances:

Segment Analysis: Home Health vs. Hospice

Enhabit’s two business segments showed divergent performance in Q1 2025. The home health segment, which accounts for approximately 77% of total revenue, faced challenges with revenue declining 5.9% year-over-year to $200.6 million. However, the company noted sequential improvement with Medicare average daily census (ADC) growing 1.5% and total ADC increasing 3.7% from Q4 2024.

The home health segment’s Adjusted EBITDA was $38.3 million in Q1 2025, down from $43.2 million in Q1 2024, but up 7.9% sequentially from $35.5 million in Q4 2024. Cost per patient day decreased 2.4% year-over-year to $27.9, helping to maintain the segment’s gross margin at 48.5%.

In contrast, the hospice segment showed robust growth with revenue increasing 20.5% year-over-year to $59.3 million. Average daily census grew 12.3% compared to Q1 2024, and admissions increased 8.0%. The segment’s Adjusted EBITDA surged 64.8% year-over-year to $15.0 million, with margin expanding to 25.3% from 18.5% in Q1 2024.

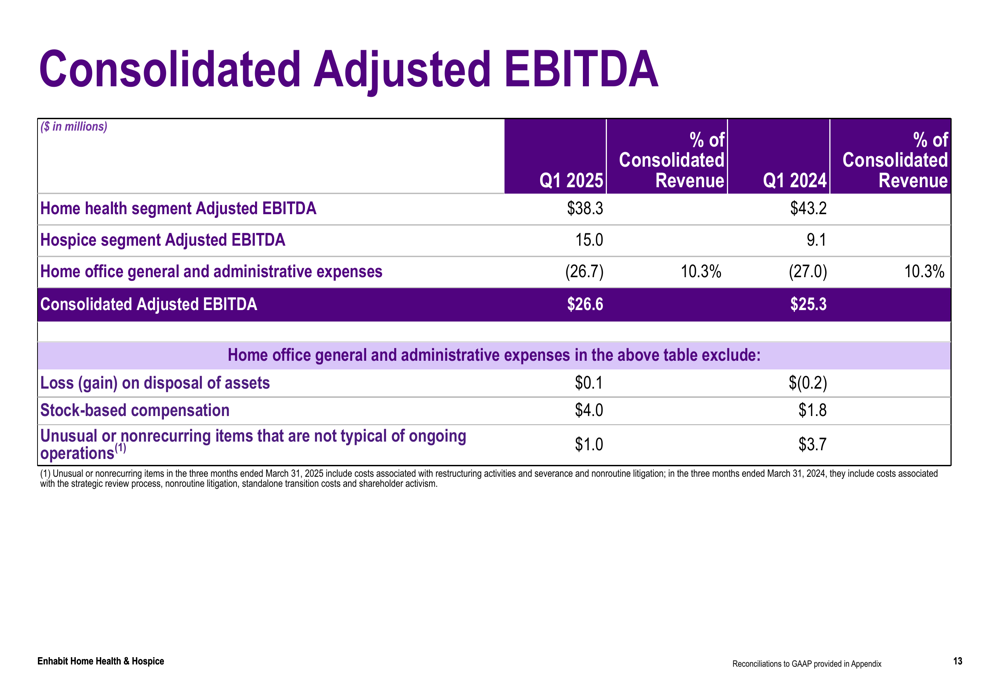

The consolidated Adjusted EBITDA breakdown illustrates how the strong hospice performance helped offset challenges in the home health segment:

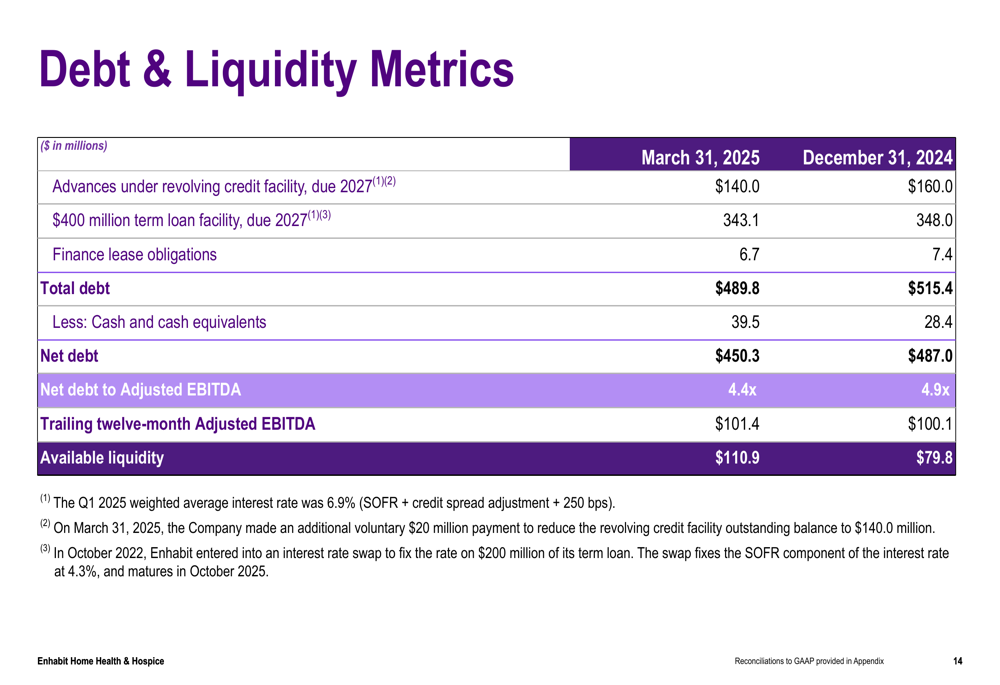

Debt Reduction and Financial Position

A key focus for Enhabit has been strengthening its balance sheet. The company reduced bank debt by $25.0 million during Q1 2025, bringing its leverage ratio below 4.5x for the fifth consecutive quarter of improvement. This achievement came one quarter earlier than required by its credit agreement, which will result in improved pricing and fewer restrictions.

As of March 31, 2025, Enhabit reported:

- Total debt of $489.8 million, down from $515.4 million at the end of 2024

- Cash and cash equivalents of $39.5 million, up from $28.4 million

- Net debt to Adjusted EBITDA ratio of 4.4x, improved from 4.9x

- Available liquidity of $110.9 million, up from $79.8 million

The following slide details the company’s debt and liquidity position:

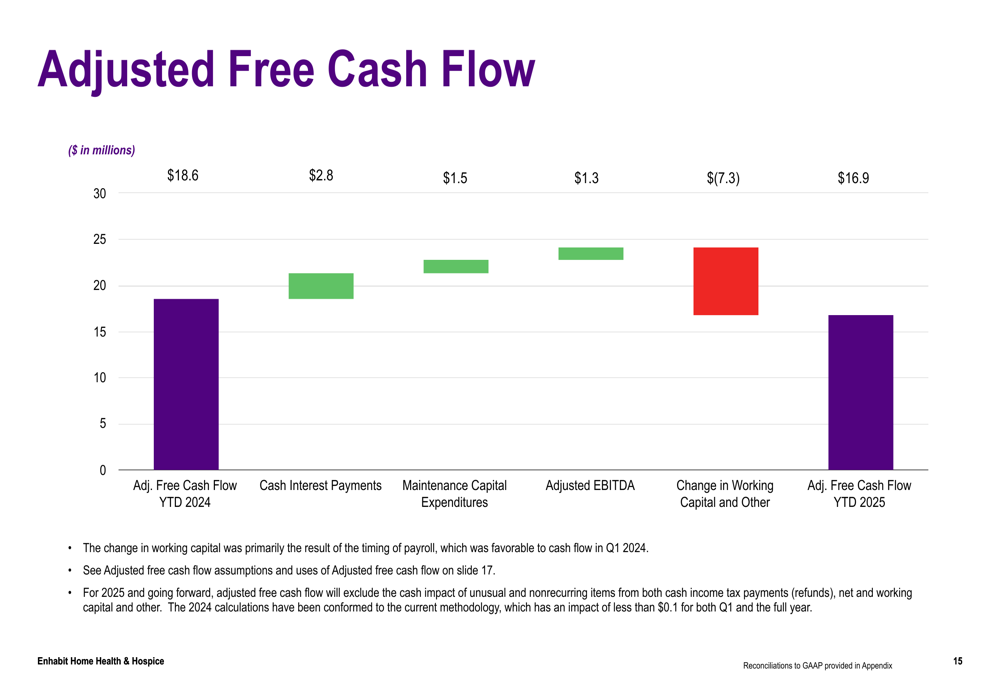

Adjusted free cash flow for Q1 2025 was $16.9 million, compared to $18.6 million in Q1 2024. The slight decrease was primarily due to changes in working capital, partially offset by improved Adjusted EBITDA and lower maintenance capital expenditures.

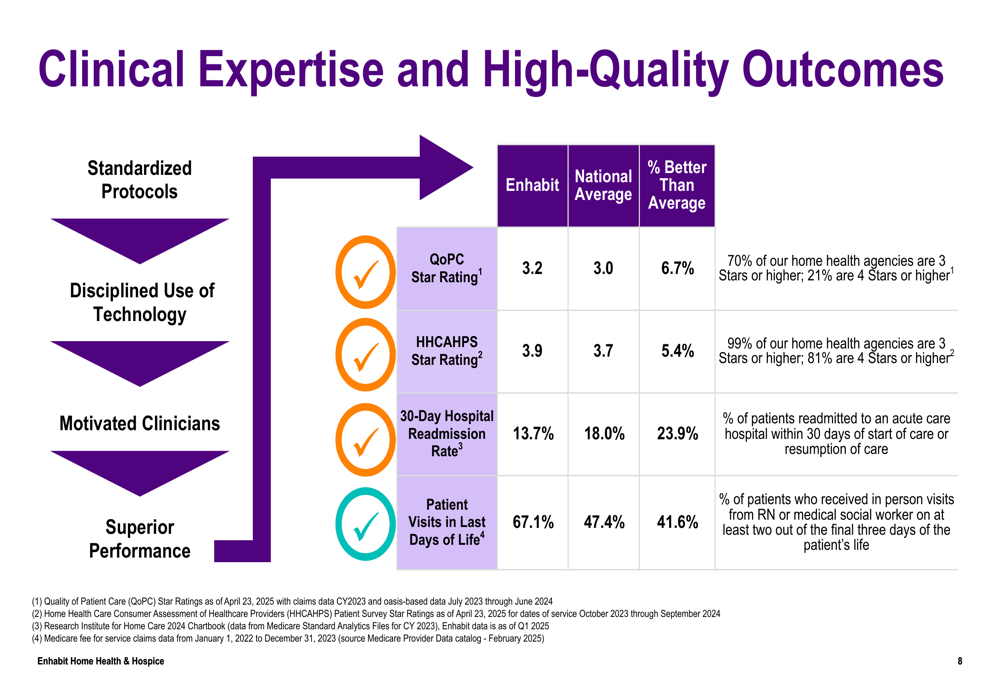

Quality Metrics and Competitive Positioning

Enhabit emphasized its clinical expertise and quality outcomes as competitive advantages in the marketplace. The company outperformed national averages across several key quality metrics, which can influence referrals and payer relationships.

Notable quality metrics included:

- Quality of Patient Care (QoPC) Star Rating of 3.2, compared to the national average of 3.0

- HHCAHPS Star Rating of 3.9, compared to the national average of 3.7

- 30-Day Hospital Readmission Rate of 13.7%, significantly better than the national average of 18.0%

- Patient Visits in Last Days of Life at 67.1%, substantially higher than the national average of 47.4%

The following slide illustrates these quality metrics:

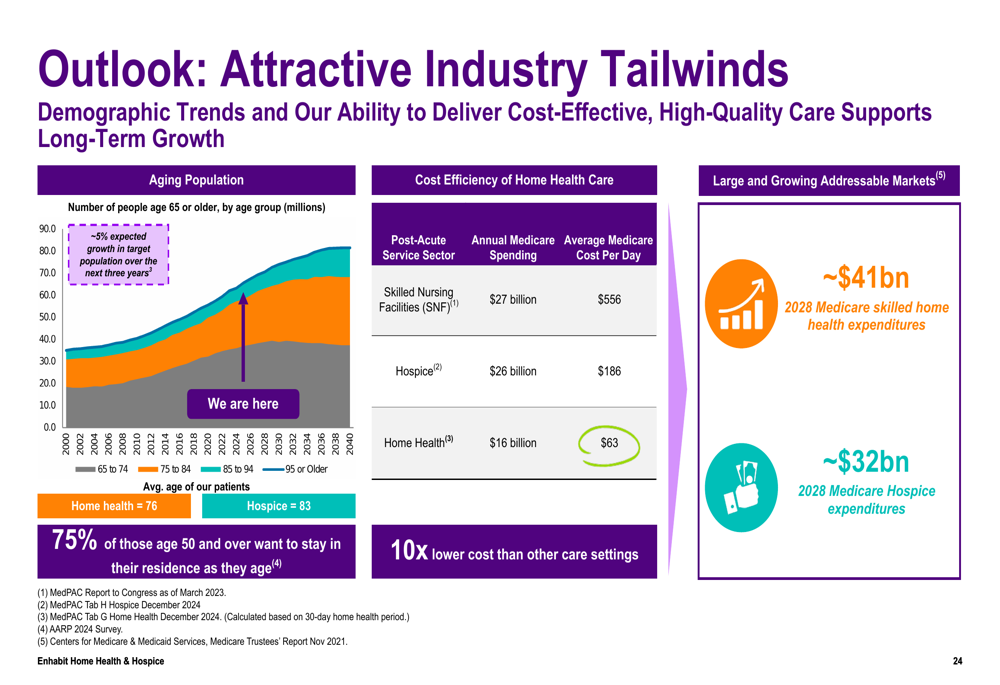

The company also highlighted attractive industry tailwinds that support its long-term growth strategy, including an aging population and the cost efficiency of home health care compared to other settings:

Forward-Looking Statements and Guidance

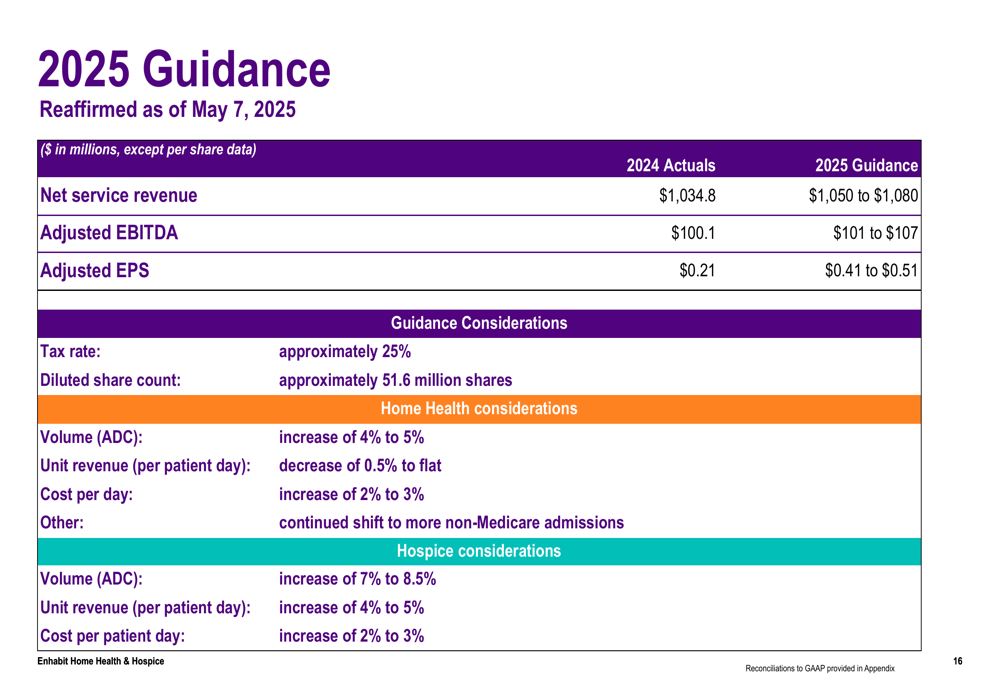

Enhabit reaffirmed its 2025 guidance, projecting:

- Net service revenue of $1,050 to $1,080 million, compared to $1,034.8 million in 2024

- Adjusted EBITDA of $101 to $107 million, compared to $100.1 million in 2024

- Adjusted EPS of $0.41 to $0.51, compared to $0.21 in 2024

The guidance assumes continued growth in hospice average daily census and sequential improvement in home health census. The company also expects to benefit from its ongoing cost control initiatives, with home office G&A expenses decreasing 1.3% in Q1 2025.

The following slide details the company’s 2025 guidance:

For 2025, Enhabit outlined its priorities across four key areas: Growth, Financial Health, Quality, and People. The company plans to focus on home health census growth, payer mix optimization, hospice average daily census expansion, and de novo location development. Financial priorities include continued de-leveraging, G&A expense management, and cost control across both segments.

While Enhabit faces ongoing challenges in its home health segment, particularly with Medicare volume, the company’s strong hospice performance, improved financial position, and quality metrics position it to potentially benefit from favorable industry trends in the aging-in-place healthcare market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.