Fubotv earnings beat by $0.10, revenue topped estimates

Executive Summary

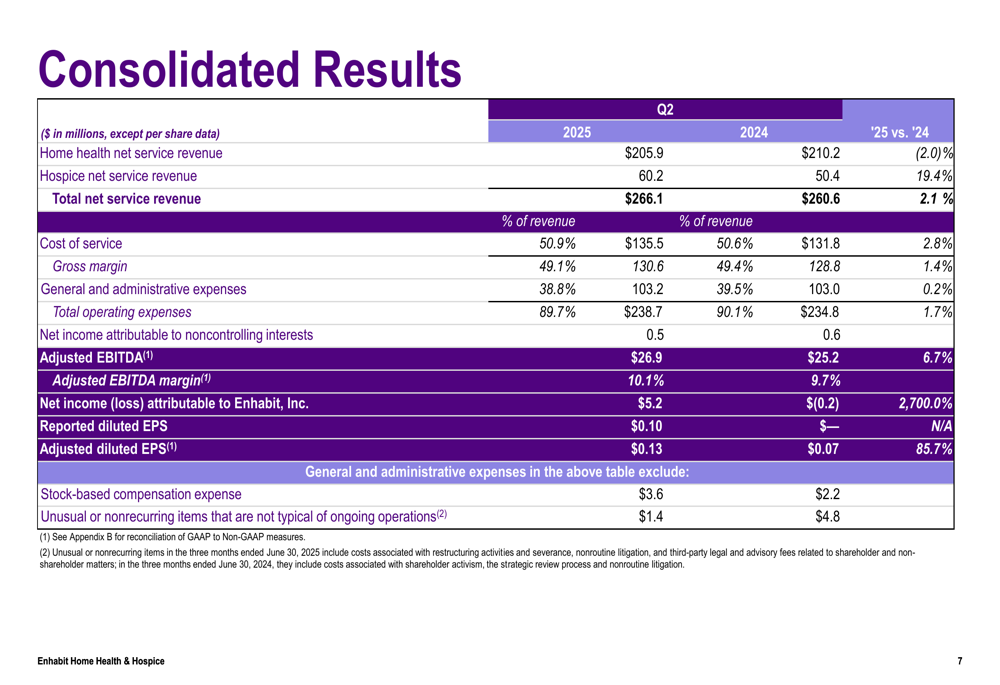

Enhabit Home Health & Hospice (NYSE:EHAB) reported its second quarter 2025 results on August 6, showing overall revenue growth of 2.1% year-over-year to $266.1 million, driven by strong performance in its Hospice segment that offset challenges in Home Health. The company reported net income of $5.2 million, a significant improvement from a $0.2 million loss in the same period last year, while adjusted EBITDA increased 6.7% to $26.9 million.

The company’s strategic priorities appear to be yielding results, with sequential growth in both segments and continued debt reduction. Enhabit also updated its full-year 2025 guidance, maintaining a positive outlook despite mixed segment performance.

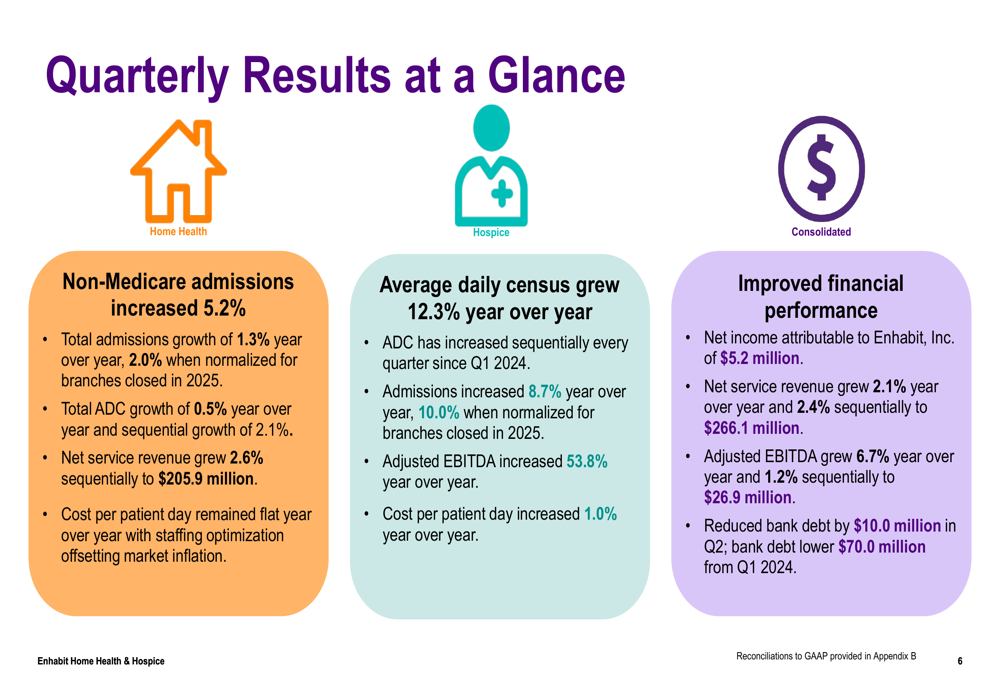

As shown in the following overview of quarterly results, Enhabit’s performance demonstrated improvement across multiple metrics:

Segment Performance Highlights

Enhabit’s performance showed a clear divergence between its two main business segments. The Home Health segment, while facing year-over-year challenges, showed signs of stabilization with sequential growth. Meanwhile, the Hospice segment continued its strong performance trajectory.

The Home Health segment reported revenue of $205.9 million, down 2.0% year-over-year but up 2.6% sequentially. Total (EPA:TTEF) admissions grew 1.3% year-over-year, with non-Medicare admissions increasing 5.2%. The segment maintained cost discipline with cost per patient day remaining flat compared to the prior year. However, gross margin declined to 47.9%, lower both sequentially and year-over-year.

The Hospice segment delivered impressive results with revenue increasing 19.4% year-over-year to $60.2 million. Average daily census (ADC) grew 12.3% year-over-year, marking the sixth consecutive quarter of sequential growth. Admissions increased 8.7% compared to Q2 2024. The segment’s adjusted EBITDA surged 53.8% year-over-year, with gross margin expanding 240 basis points to 53.0%.

The following consolidated results table provides a detailed comparison of Q2 2025 performance against the prior year:

Financial Health

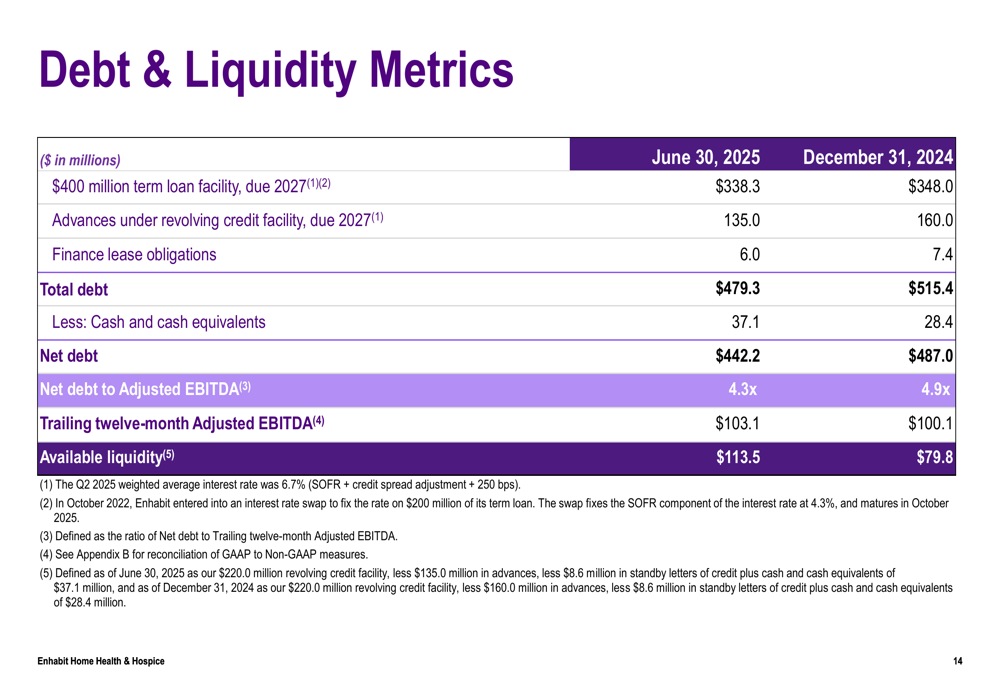

Enhabit continued to strengthen its balance sheet in Q2 2025, reducing bank debt by $10 million during the quarter. Since Q1 2024, the company has lowered its bank debt by $70 million, resulting in $3.2 million in interest expense savings over the same period.

As of June 30, 2025, Enhabit reported total debt of $479.3 million, down from $515.4 million at the end of 2024. Net debt to adjusted EBITDA improved to 4.3x from 4.9x at year-end 2024, reflecting the company’s consistent deleveraging efforts. Available liquidity increased to $113.5 million from $79.8 million at the end of 2024.

The following debt and liquidity metrics highlight the company’s progress in strengthening its financial position:

Adjusted diluted earnings per share reached $0.13 in Q2 2025, representing an 85.7% increase from $0.07 in Q2 2024. This improvement aligns with the company’s performance in Q1 2025, when Enhabit reported EPS of $0.10, exceeding analyst expectations of $0.06 and driving a nearly 11% stock price increase following the announcement.

Strategic Initiatives

Enhabit outlined its strategic priorities for 2025, focusing on growth, financial health, quality, and people. The company highlighted several achievements in Q2, including the successful renegotiation of a national payer agreement resulting in a low double-digit percentage rate increase for Home Health services.

The company continued its de novo expansion strategy, opening three new locations in Q2, bringing the year-to-date total to four. Enhabit remains on track to achieve its goal of opening 10 new locations in 2025.

The following slide details the company’s strategic priorities and Q2 execution highlights:

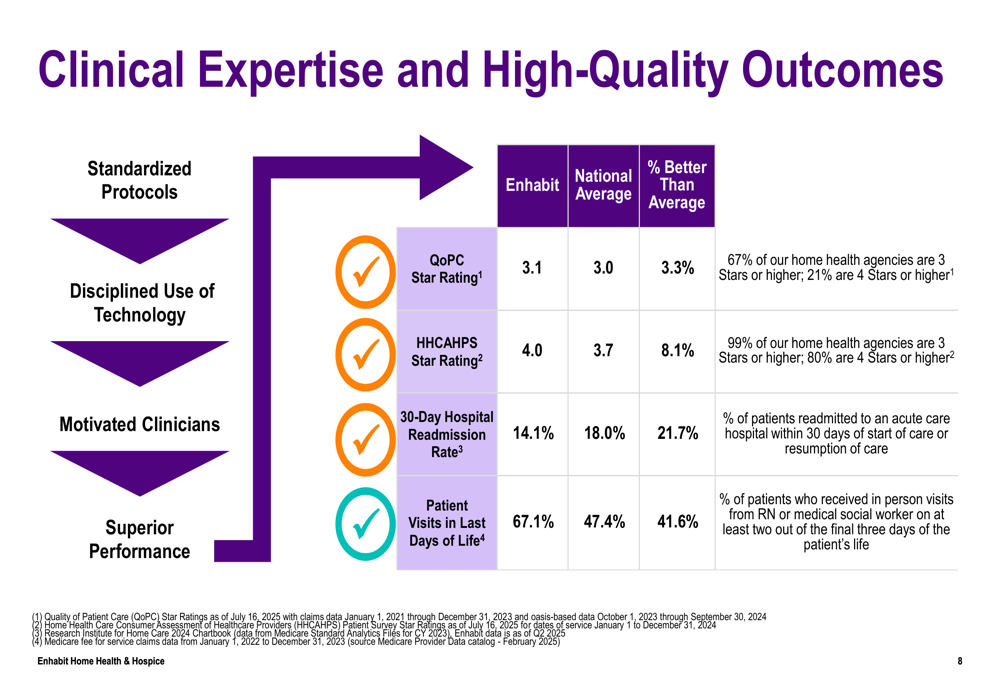

Quality metrics remain a key focus area, with Enhabit outperforming national averages across several measures. The company reported a Quality of Patient Care (QoPC) Star Rating of 3.1 versus the national average of 3.0, with 67% of home health agencies rated 3 Stars or higher. The HHCAHPS Star Rating was 4.0 compared to the national average of 3.7, with 99% of agencies rated 3 Stars or higher.

Forward-Looking Statements

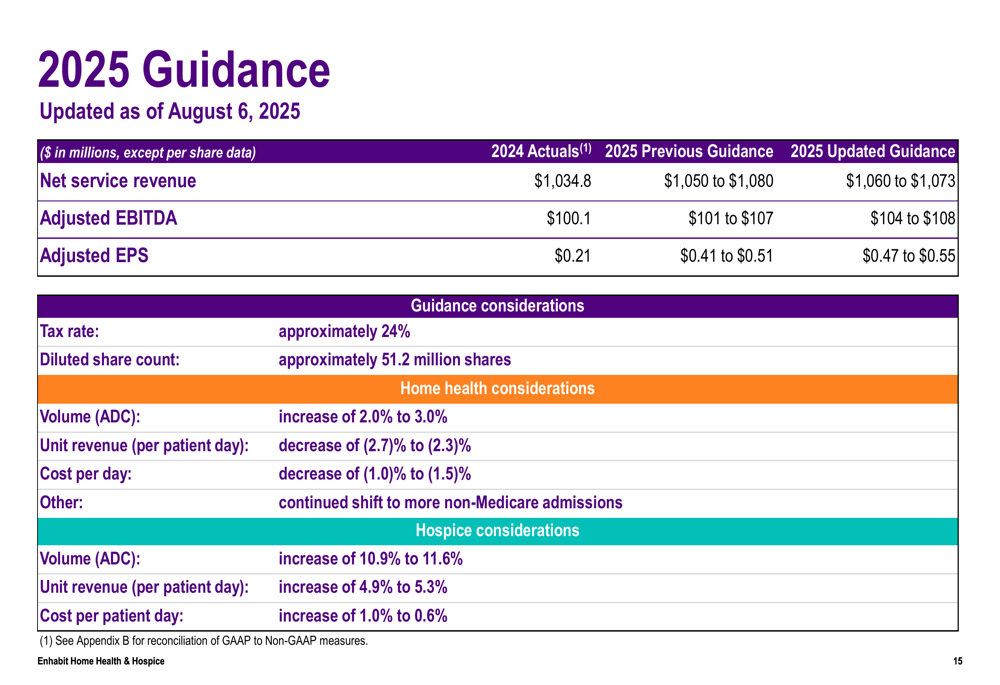

Enhabit updated its 2025 guidance, projecting net service revenue of $1,060 to $1,073 million, adjusted EBITDA of $104 to $108 million, and adjusted EPS of $0.47 to $0.55. The company expects Home Health volume to increase 2.0% to 3.0% and Hospice volume to grow 10.9% to 11.6%.

The updated guidance reflects management’s confidence in continued operational improvements despite ongoing challenges in the Home Health segment:

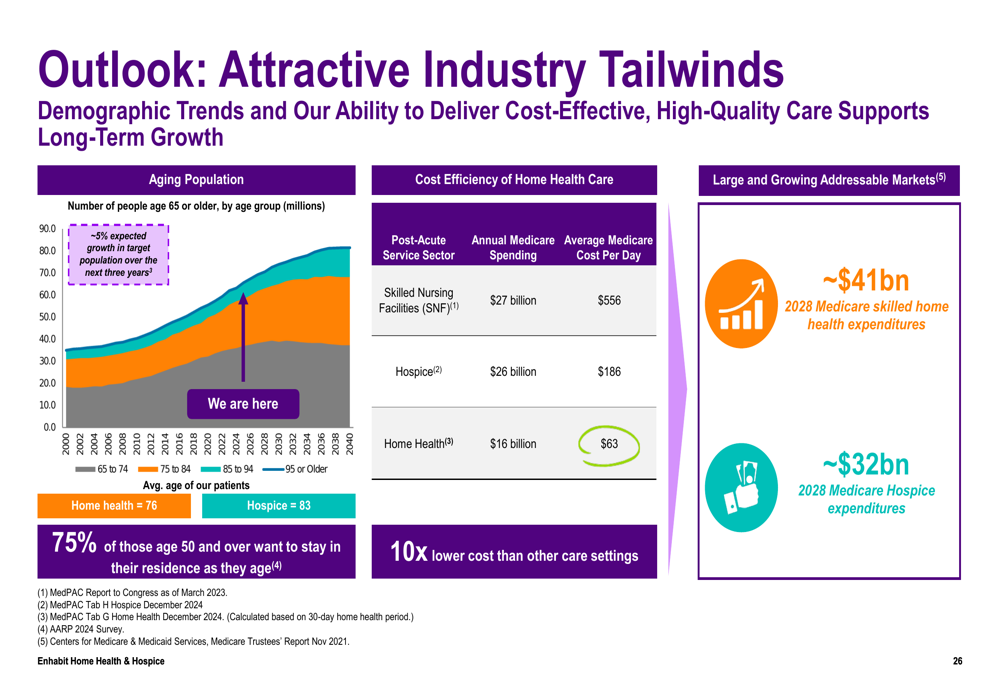

The company highlighted favorable industry tailwinds supporting its long-term growth strategy. These include demographic trends with approximately 5% expected growth in the target population over the next three years, cost efficiency advantages compared to skilled nursing facilities, and large addressable markets with projected Medicare expenditures of $41 billion for skilled home health and $32 billion for hospice by 2028.

The following slide illustrates these industry tailwinds:

Market Context

Enhabit’s stock closed at $6.69 on August 6, 2025, up 1.2% for the day. The stock has traded between $6.47 and $10.91 over the past 52 weeks, currently trading near the lower end of that range despite the company’s improving financial performance.

The Q2 results build on momentum from Q1 2025, when the company exceeded EPS expectations but fell short on revenue. The continued focus on operational efficiencies and strategic growth initiatives appears to be yielding results, particularly in the Hospice segment, though challenges persist in Home Health.

With its consistent debt reduction strategy and focus on high-growth areas within its business, Enhabit is positioning itself to capitalize on favorable demographic trends and the growing preference for home-based care over institutional settings.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.