EUR/USD likely to find a peak near 1.25: UBS

Introduction & Market Context

Enovis Corporation (NYSE:ENOV) released its second quarter 2025 results on August 7, showing accelerated growth and improved profitability that prompted management to raise full-year guidance. The medical technology company reported 7% revenue growth and a 27% increase in adjusted earnings per share, demonstrating momentum across its business segments despite ongoing market challenges.

The company’s stock traded up 1.86% in premarket at $26.24, showing a modest positive reaction to the results. This comes after Enovis shares have struggled in recent months, trading near their 52-week low of $25.47, despite consistently improving operational performance.

Quarterly Performance Highlights

Enovis reported total revenue of $565 million for Q2 2025, representing 7% year-over-year growth on a reported basis and 5% organic growth. The company highlighted continued momentum across its business segments, with particularly strong performance in its Reconstructive division.

As shown in the following quarterly highlights slide:

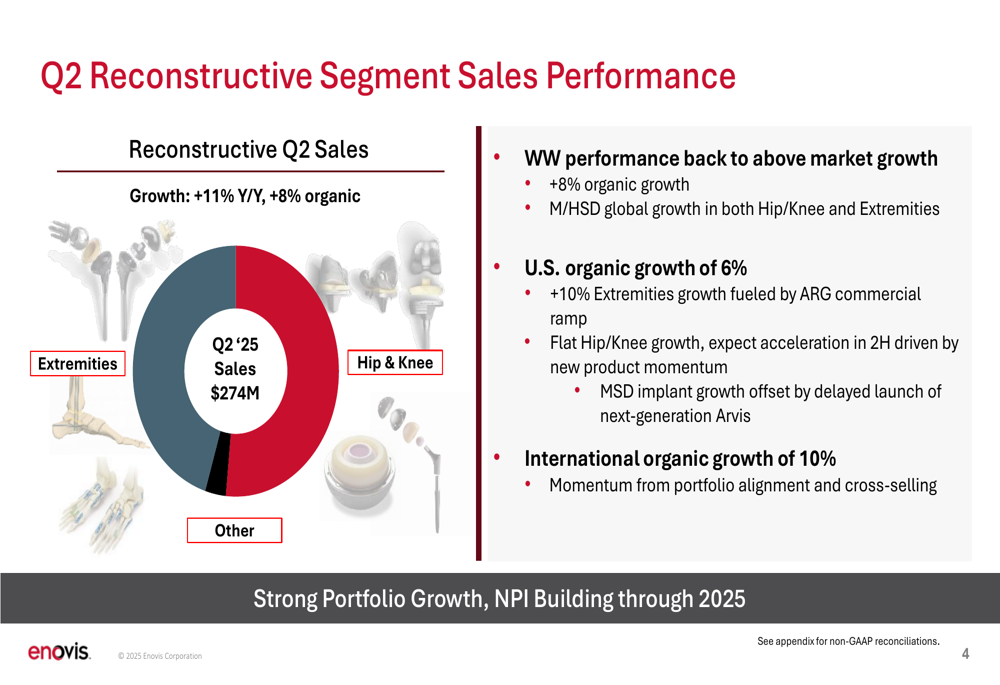

The Reconstructive segment delivered impressive results with 11% year-over-year growth and 8% organic growth, reaching $274 million in quarterly sales. This performance was driven by strong growth in both the Hip/Knee and Extremities product lines globally, as well as successful new product launches including ARG in Shoulder, and Nebula and Surgical Impactor in Hip.

The segment breakdown reveals particular strength in international markets:

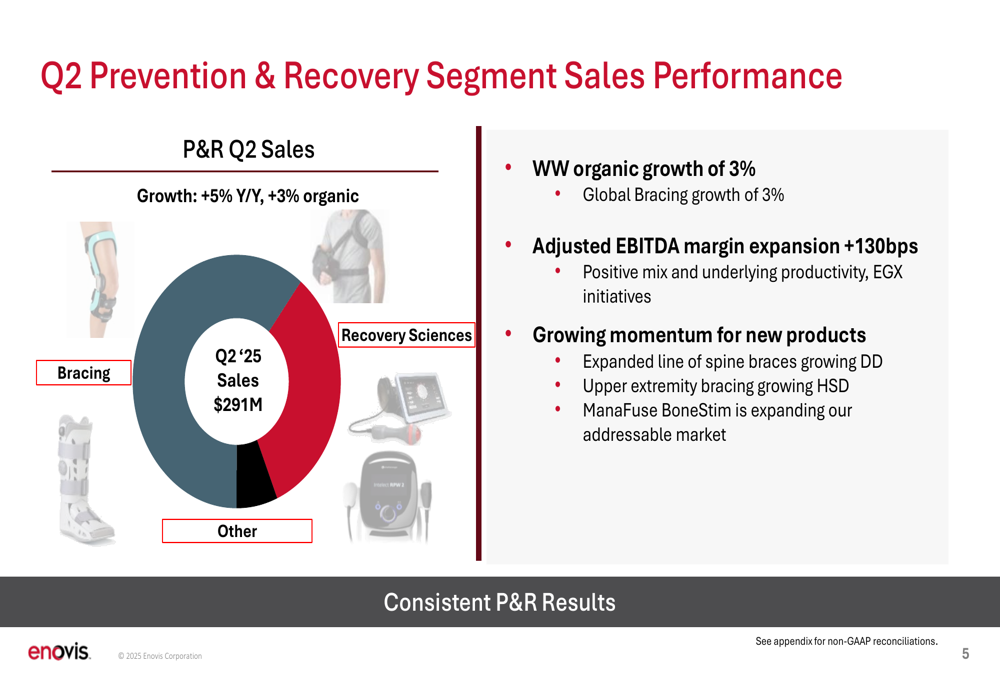

Meanwhile, the Prevention & Recovery (P&R) segment showed more modest but stable growth at 5% year-over-year and 3% organic growth, with quarterly sales of $291 million. The segment benefited from consistent bracing performance and margin improvements through positive mix and productivity initiatives.

Detailed Financial Analysis

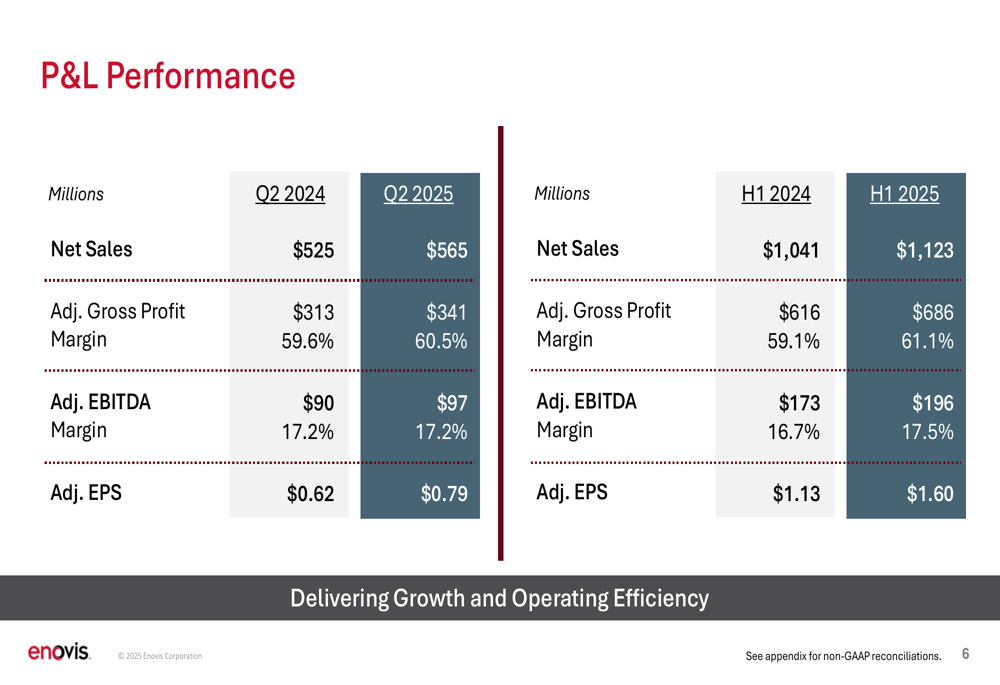

Enovis demonstrated improved profitability metrics in the second quarter, with adjusted gross profit margin expanding to 60.5% from 59.6% in the prior year period. Adjusted EBITDA reached $97 million, maintaining a margin of 17.2%, while adjusted earnings per share jumped 27% to $0.79 compared to $0.62 in Q2 2024.

The company’s first-half performance showed even stronger improvement, with adjusted EBITDA margin expanding 80 basis points to 17.5% and adjusted EPS growing 42% to $1.60.

The financial results reflect a significant gap between GAAP and non-GAAP metrics, with Q2 GAAP net loss of $36.5 million compared to adjusted net income of $45.7 million. This difference is primarily due to acquisition-related non-cash adjustments of $49.5 million and other adjustments of $32.2 million, as detailed in the company’s reconciliation tables.

Forward-Looking Statements

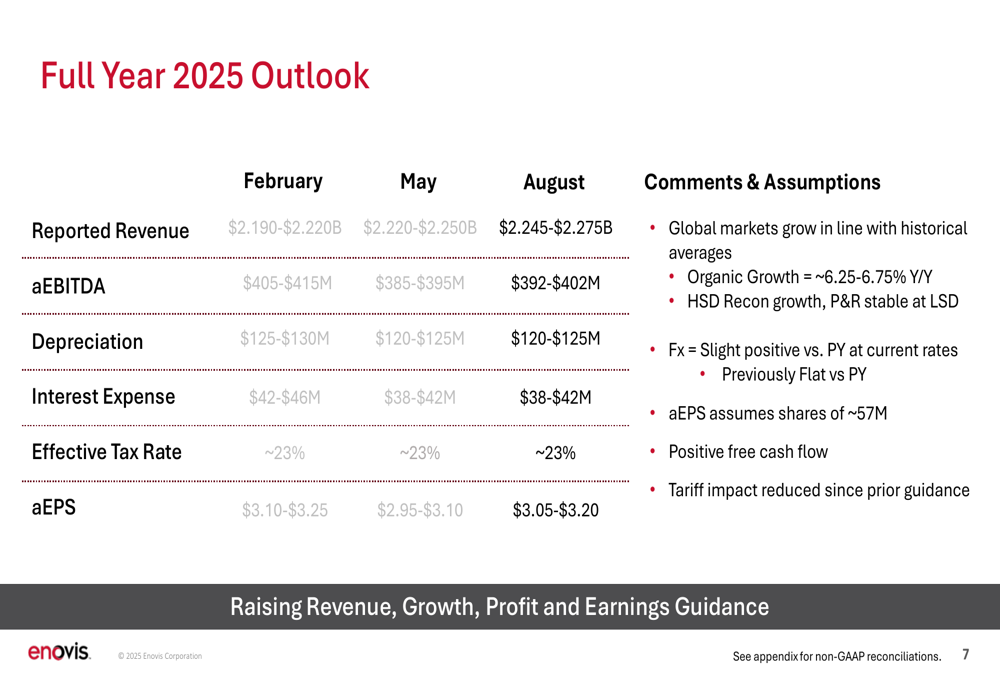

In a sign of growing confidence, Enovis raised its full-year 2025 guidance across all key metrics. The company now expects:

- Revenue of $2.245-$2.275 billion (up from $2.220-$2.250 billion in May)

- Adjusted EBITDA of $392-$402 million (up from $385-$395 million)

- Adjusted EPS of $3.05-$3.20 (up from $2.95-$3.10)

The revised outlook is based on expectations of approximately 6.25-6.75% organic growth for the year, with high single-digit growth in the Reconstructive segment and low single-digit growth in Prevention & Recovery.

Management also noted that the impact of tariffs has been reduced since their prior guidance, suggesting effective mitigation strategies. The company continues to expect positive free cash flow for the full year.

Strategic Initiatives

Enovis highlighted several key product launches that are expected to drive future growth. In the Reconstructive segment, the company is seeing strong commercial ramp of its ARG shoulder product, which contributed to 10% growth in Extremities. New hip and knee products are expected to accelerate growth in the second half of the year.

In the Prevention & Recovery segment, the company is expanding its addressable market with products like the ManaFuse BoneStim, while its expanded line of spine braces is growing at double-digit rates.

The company summarized its strategic position and outlook in its closing slide:

Market Perspectives

Despite Enovis’s improving financial performance and raised guidance, investor sentiment remains cautious. This pattern mirrors the company’s Q1 2025 results, when the stock fell 8.85% despite beating earnings expectations with an adjusted EPS of $0.81 versus the forecast of $0.74.

The disconnect between operational performance and stock price may reflect broader market concerns about the medical device sector, ongoing global trade tensions, or skepticism about the company’s ability to maintain growth momentum in a challenging economic environment.

The company’s GAAP results, which continue to show net losses despite strong adjusted metrics, may also be contributing to investor caution. For Q2 2025, Enovis reported a GAAP net loss of $36.5 million, wider than the $18.5 million loss in the same period last year.

Nevertheless, management’s decision to raise full-year guidance suggests confidence in the company’s trajectory for the remainder of 2025, with particular emphasis on new product momentum and continued margin expansion opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.