Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Enterprise Financial Services Corp (NASDAQ:EFSC) presented its first quarter 2025 earnings results on April 29, showing modest earnings growth and announcing a strategic branch acquisition to expand its footprint in the Southwest and Midwest regions.

Quarterly Performance Highlights

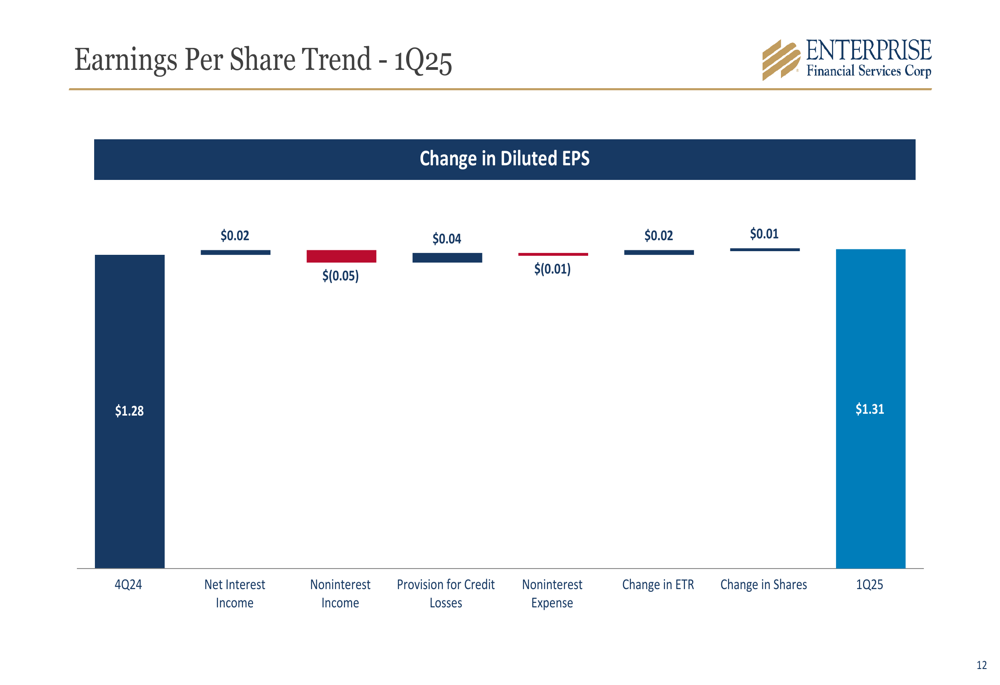

Enterprise Financial reported net income of $50.0 million for Q1 2025, up $1.1 million from the previous quarter, with earnings per share rising to $1.31 from $1.28 in Q4 2024. This represents a slight sequential improvement, though it falls just short of the $1.32 EPS reported in Q4 2024 as mentioned in previous earnings coverage.

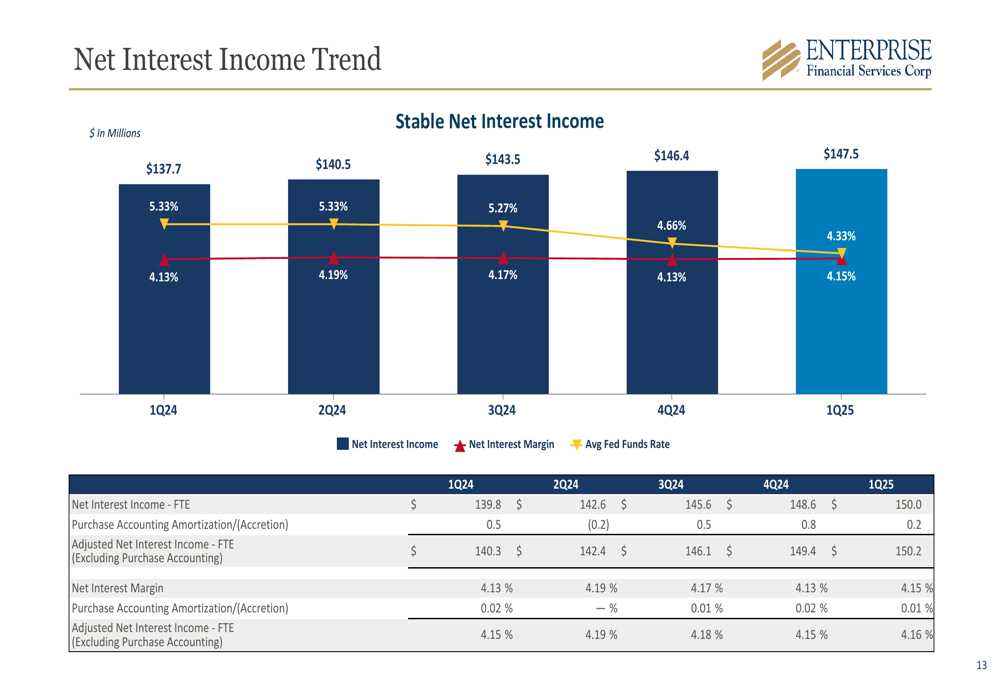

Net interest income increased to $147.5 million, up $1.1 million from the linked quarter, with the net interest margin improving slightly to 4.15% from 4.13%. This stability is notable given the declining interest rate environment, with the average Fed Funds rate decreasing from 5.33% in Q1 2024 to 4.33% in Q1 2025.

As shown in the following chart of net interest income trends, the company has maintained consistent growth over five consecutive quarters despite rate fluctuations:

Pre-provision net revenue (PPNR) declined to $66.1 million, down $3.4 million from the previous quarter, while adjusted return on average assets (ROAA) slightly decreased to 1.29% from 1.31%. The company’s tangible book value per share continued to grow, reaching $38.54 compared to $37.27 in the previous quarter.

The following slide breaks down the key drivers behind the quarterly EPS change:

Strategic Branch Acquisition

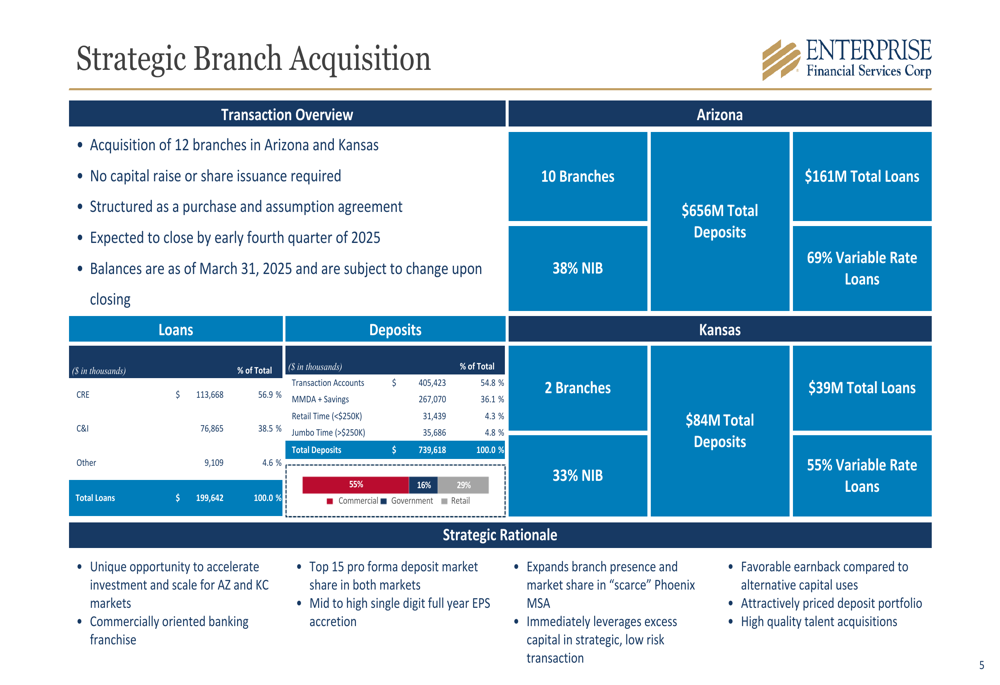

A significant highlight of the presentation was the announcement of a strategic branch acquisition involving 12 branches across Arizona and Kansas. The transaction, structured as a purchase and assumption agreement with no capital raise or share issuance required, is expected to close by early Q4 2025.

The acquisition will add approximately $739.6 million in deposits and $199.6 million in loans to Enterprise Financial’s balance sheet. Notably, the Arizona portion comprises 10 branches with $656 million in deposits (38% non-interest bearing) and $161 million in loans, while the Kansas portion includes 2 branches with $84 million in deposits and $39 million in loans.

The strategic rationale and transaction details are illustrated in the following slide:

"This acquisition offers a unique opportunity to accelerate investment and scale for our Arizona and Kansas City markets," the company noted in its presentation, adding that it expects "mid to high single digit full year EPS accretion" from the transaction.

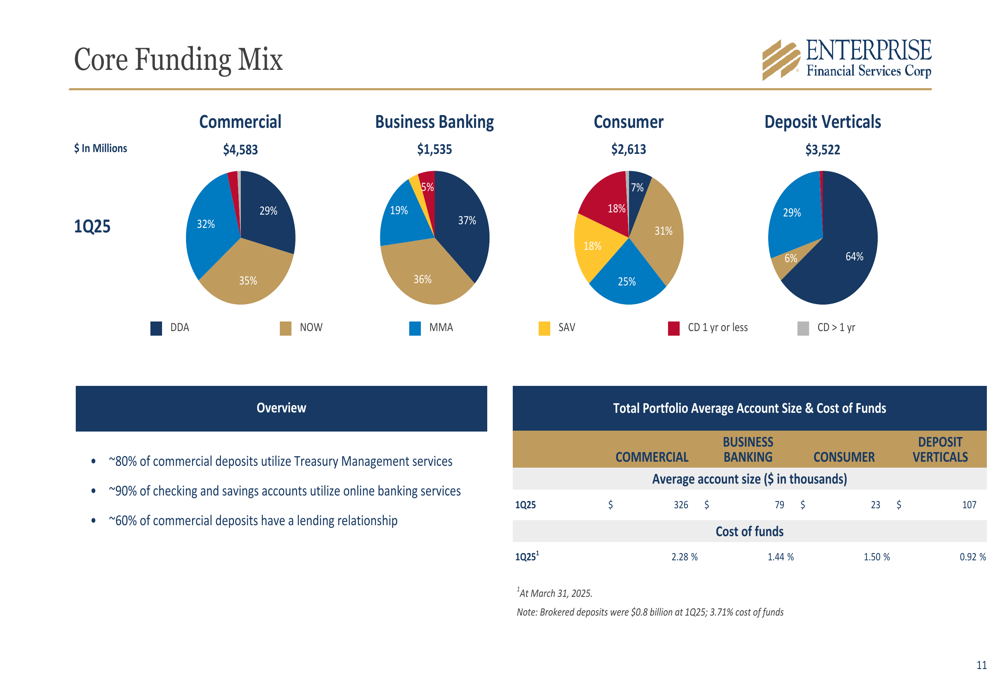

Deposit Strategy and Funding Mix

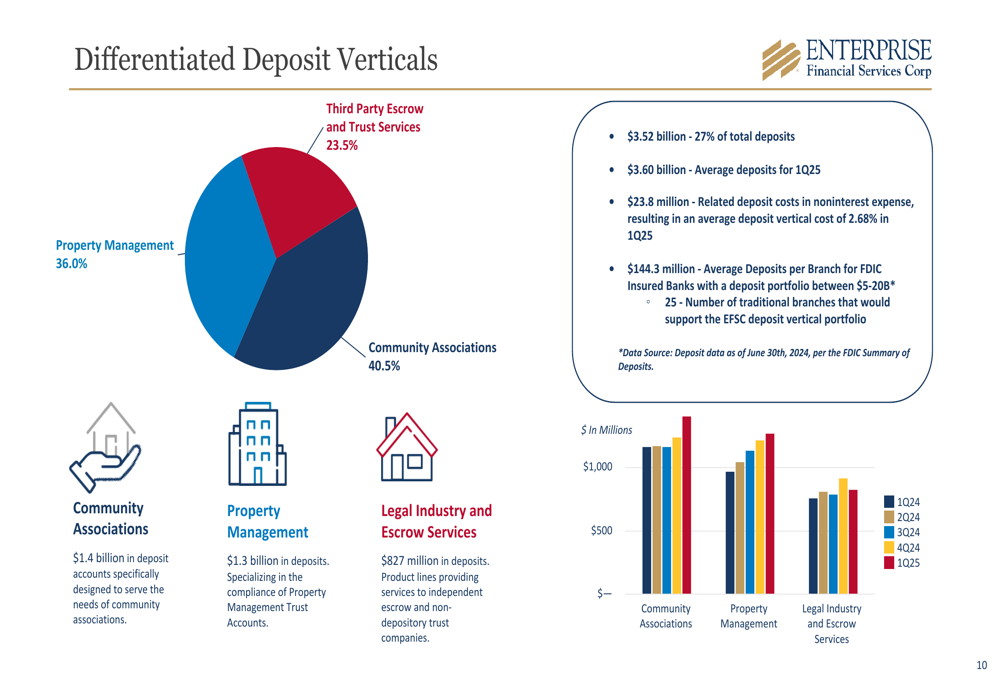

Enterprise Financial continues to emphasize its differentiated deposit strategy, highlighting specialized verticals that now represent 27% of total deposits, or $3.52 billion. These verticals include third-party escrow and trust services (23.5%), property management (36.0%), and community associations (40.5%).

The company’s deposit vertical strategy is detailed in the following slide, showing the composition and efficiency of these specialized deposit relationships:

These deposit verticals generated average deposits of $3.60 billion in Q1 2025, with related deposit costs in noninterest expense resulting in an average deposit vertical cost of 2.68%. The company emphasized that these specialized verticals provide significant efficiency advantages, with average deposits per branch far exceeding industry averages for similarly sized banks.

The core funding mix across commercial, business banking, consumer, and deposit verticals segments is illustrated below:

Total (EPA:TTEF) deposits stood at $13.0 billion at quarter-end, down $112.3 million from the previous quarter. Noninterest-bearing deposits represented 33% of total deposits, reflecting the company’s focus on maintaining a favorable deposit mix in a competitive funding environment.

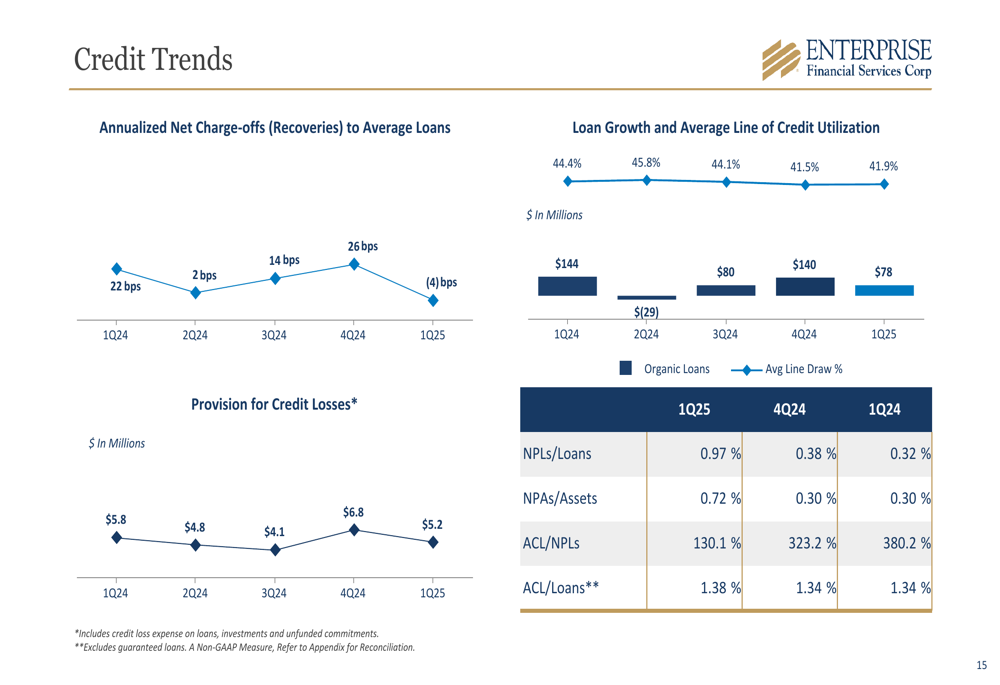

Credit Quality and Loan Portfolio

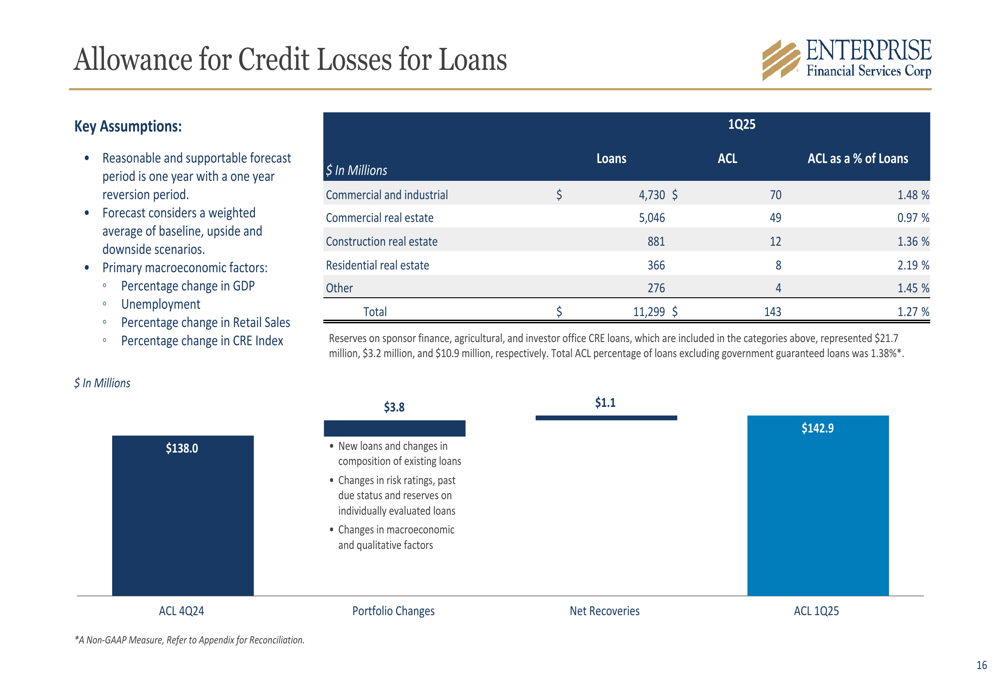

Enterprise Financial reported continued strong credit quality metrics in Q1 2025. The company recorded net recoveries of $1.1 million during the quarter, compared to net charge-offs in previous periods. The allowance for credit losses for loans stood at $143 million, representing 1.27% of total loans.

The following slide illustrates the improving credit trends:

Total loans increased to $11.3 billion, up $78.4 million from the previous quarter, with growth across multiple regions. The loan-to-deposit ratio was 86.7%, indicating a well-balanced balance sheet with ample liquidity.

The allowance for credit losses by loan category is detailed below:

Forward-Looking Statements

Looking ahead, Enterprise Financial appears well-positioned for continued growth, particularly with the pending branch acquisition expected to close by early Q4 2025. The company maintained its strong capital position with a CET1 ratio of 11.8% and continued to return capital to shareholders through $10.6 million in common stock repurchases during the quarter.

The company also increased its quarterly common stock dividend to $0.29 per share in Q1 2025, a $0.01 increase from the previous quarter, demonstrating confidence in its financial outlook.

Based on the presentation and recent trading data, Enterprise Financial’s stock closed at $51.99 on April 28, 2025, representing a 1.34% increase from the previous close of $51.34. The stock has traded between $37.28 and $63.13 over the past 52 weeks.

With its stable net interest margin, improving credit quality, and strategic expansion plans, Enterprise Financial appears focused on leveraging its differentiated deposit strategy and regional growth opportunities to drive future performance in what remains a challenging banking environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.