Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

Enterprise Products Partners L.P. (NYSE:EPD) released its second quarter 2025 earnings support slides on July 28, highlighting modest growth in gross operating margin despite mixed segment performance. The midstream energy infrastructure company continues to demonstrate resilience in its business model, maintaining its 27-year streak of consecutive distribution increases while advancing a substantial capital project portfolio.

The company’s presentation comes amid ongoing volatility in energy markets, with EPD’s stock closing at $31.55 on July 25, down 0.75% for the day and trading well below its 52-week high of $34.63. This follows a first quarter that saw the company miss earnings expectations with EPS of $0.64 versus a forecasted $0.70, despite revenue exceeding expectations.

Quarterly Performance Highlights

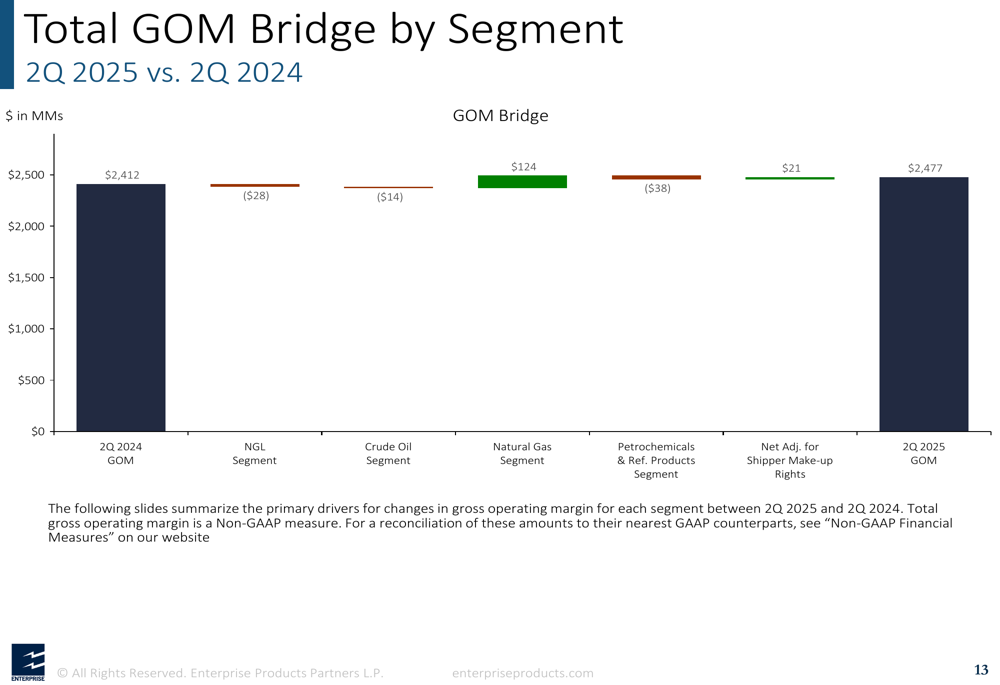

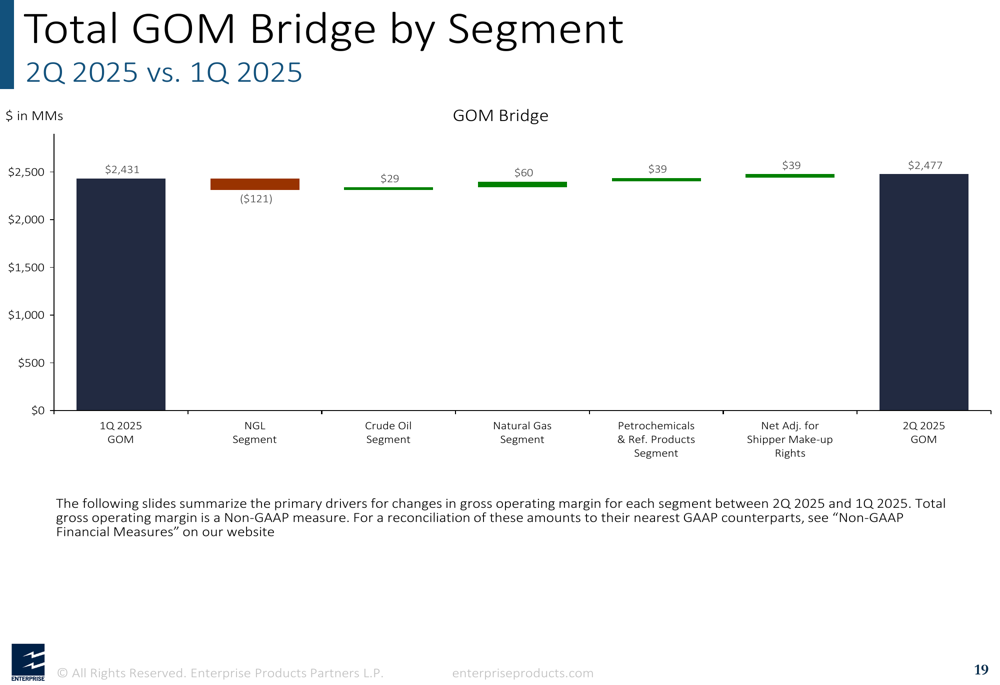

Enterprise Products reported total gross operating margin (GOM) of $2,477 million for Q2 2025, representing a $65 million increase compared to Q2 2024 ($2,412 million) and a $46 million increase from Q1 2025 ($2,431 million). This growth was primarily driven by strong performance in the Natural Gas segment, which offset declines in other business units.

As shown in the following chart breaking down the year-over-year GOM changes by segment:

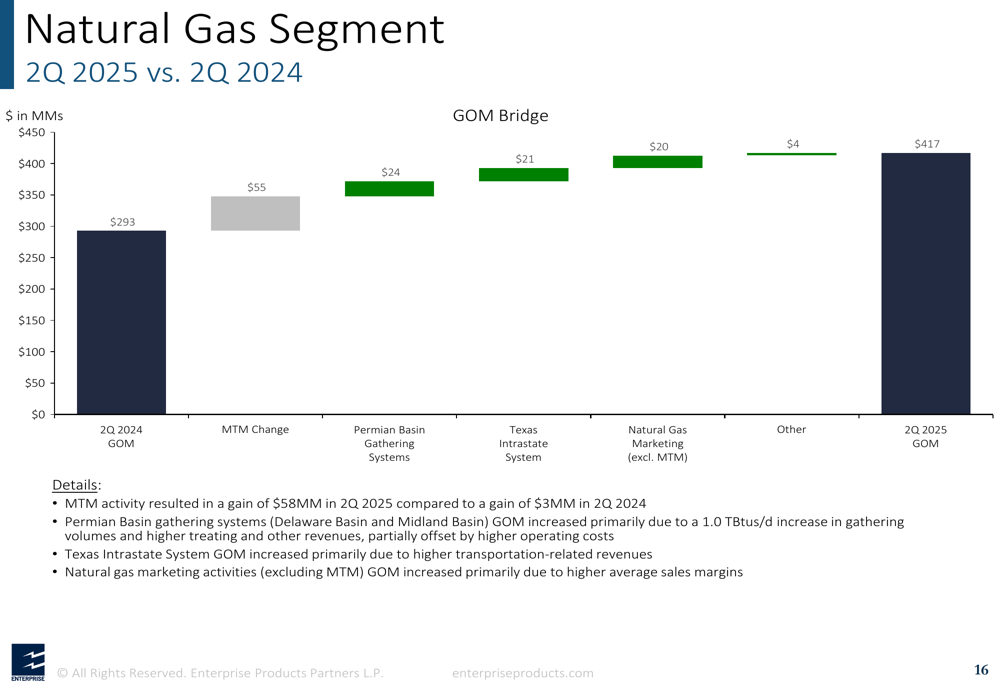

The Natural Gas segment was the standout performer with a $124 million increase compared to Q2 2024, largely attributable to a $55 million mark-to-market change, $24 million growth in Permian Basin Gathering Systems, and $21 million improvement in the Texas Intrastate System. This strong performance was partially offset by declines in the NGL segment (-$28 million), Crude Oil segment (-$14 million), and Petrochemicals & Refined Products segment (-$38 million).

Quarter-over-quarter performance showed similar trends, with Natural Gas delivering a $60 million increase compared to Q1 2025:

Segment Performance Analysis

The NGL segment, which remains Enterprise’s largest business unit, posted GOM of $1,297 million in Q2 2025, down from $1,325 million in Q2 2024. The year-over-year decline was driven by negative impacts from mark-to-market changes (-$16 million), HSC Terminals and Related Pipeline System (-$28 million), and Permian Basin Processing Facilities (-$14 million). These were partially offset by positive contributions from Permian Basin & Rocky Mountain NGL Pipelines ($23 million) and Eastern Ethane Pipelines ($14 million).

The Natural Gas segment showed the strongest growth, with GOM increasing to $417 million in Q2 2025 from $293 million in Q2 2024. This 42% year-over-year growth was driven by favorable mark-to-market changes and strong performance across multiple assets.

The following chart details the Natural Gas segment’s impressive performance:

The Crude Oil segment experienced a slight decline with GOM of $403 million in Q2 2025 compared to $417 million in Q2 2024, primarily due to negative impacts from mark-to-market changes and reduced performance in Crude Oil Assets & Marketing.

The Petrochemicals & Refined Products segment reported GOM of $354 million in Q2 2025, down from $392 million in Q2 2024, with the decline largely attributed to a $52 million decrease in Octane Enhancement & Related Plant Operations.

Capital Allocation Strategy

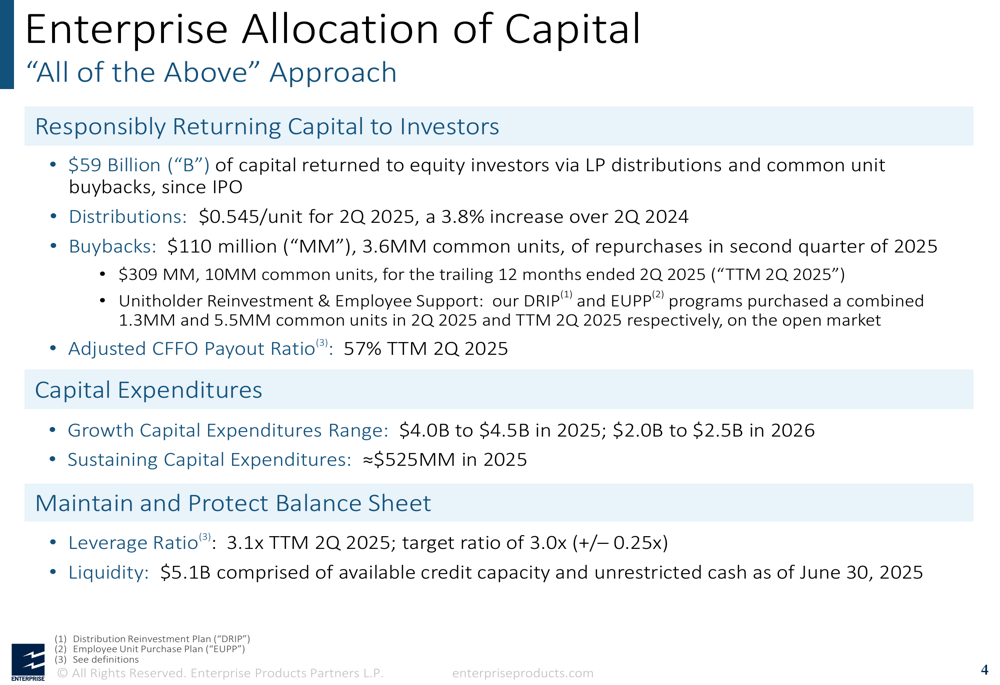

Enterprise Products continues to demonstrate a balanced approach to capital allocation, focusing on returning capital to investors while funding strategic growth initiatives. The company increased its quarterly distribution to $0.545 per unit for Q2 2025, representing a 3.8% increase over Q2 2024 and extending its 27-year streak of consecutive distribution growth.

The company’s capital allocation strategy is clearly illustrated in the following slide:

In addition to distributions, Enterprise repurchased $110 million (3.6 million units) during Q2 2025 and $309 million (10 million units) for the trailing twelve months ended Q2 2025. The company maintained an adjusted cash flow from operations payout ratio of 57%, demonstrating its commitment to sustainable distributions.

Enterprise’s financial position remains strong with a leverage ratio of 3.1x for TTM Q2 2025, slightly above its target ratio of 3.0x (+/- 0.25x). The company reported $5.1 billion in liquidity as of June 30, 2025, providing ample flexibility for future investments.

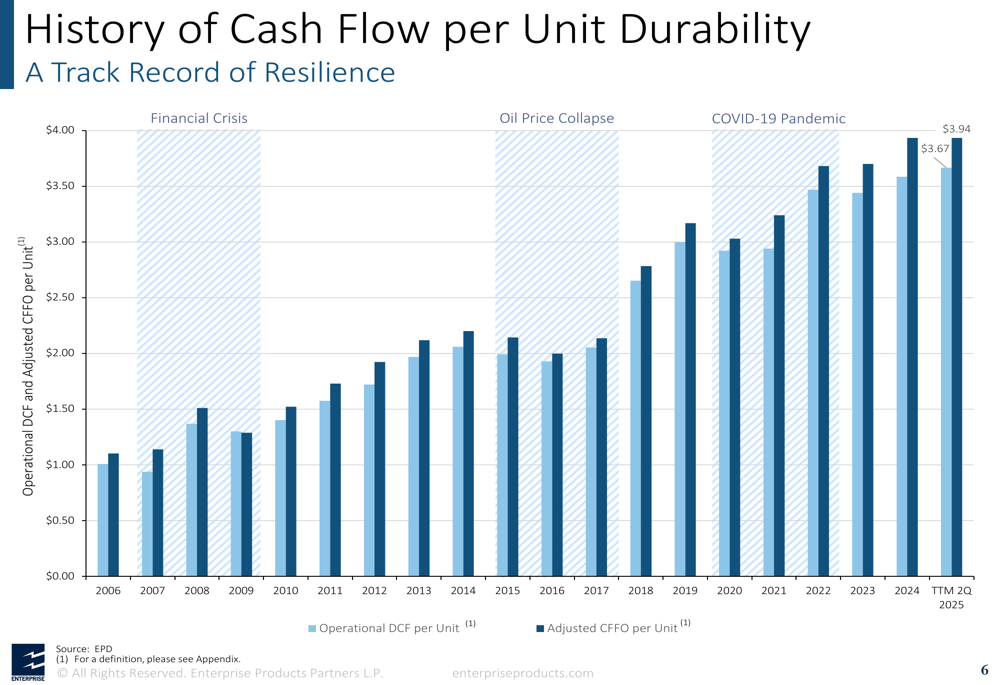

The following chart demonstrates Enterprise’s history of maintaining durable cash flow through various economic cycles:

Strategic Growth Initiatives

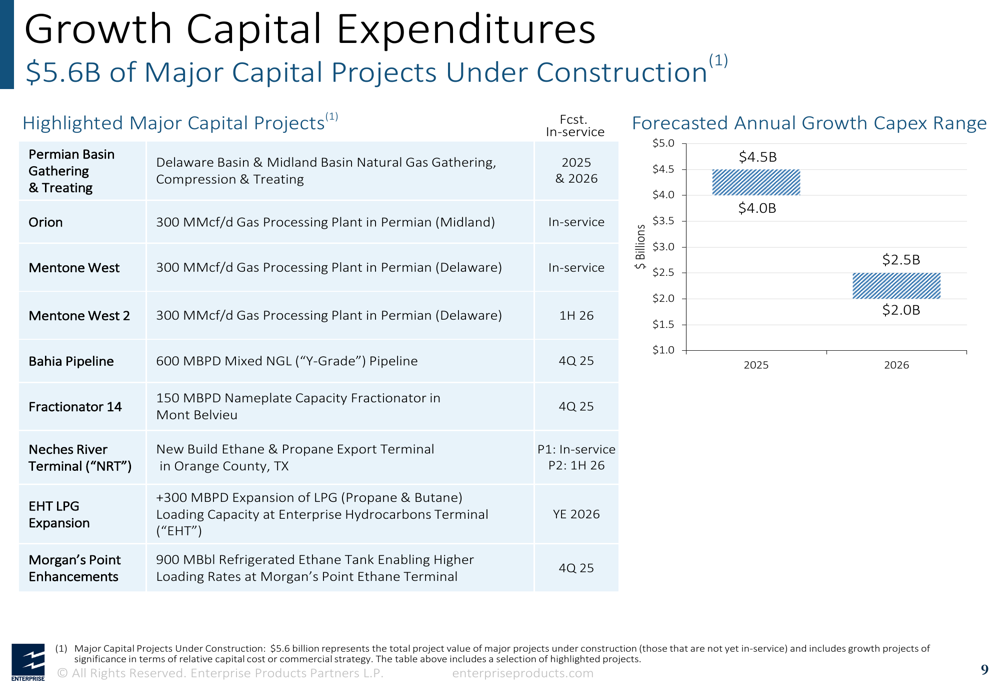

Enterprise Products has $5.6 billion of major capital projects currently under construction, with forecasted annual growth capital expenditures of $4.0-$4.5 billion in 2025 and $2.0-$2.5 billion in 2026. These investments are focused on expanding the company’s integrated midstream network, particularly in high-growth areas like the Permian Basin.

Key projects include the Permian Basin Gathering & Treating facilities, Orion, Mentone West, Mentone West 2, Bahia Pipeline, Fractionator 14, Neches River Terminal, EHT LPG Expansion, and Morgan’s Point Enhancements, as shown in the following slide:

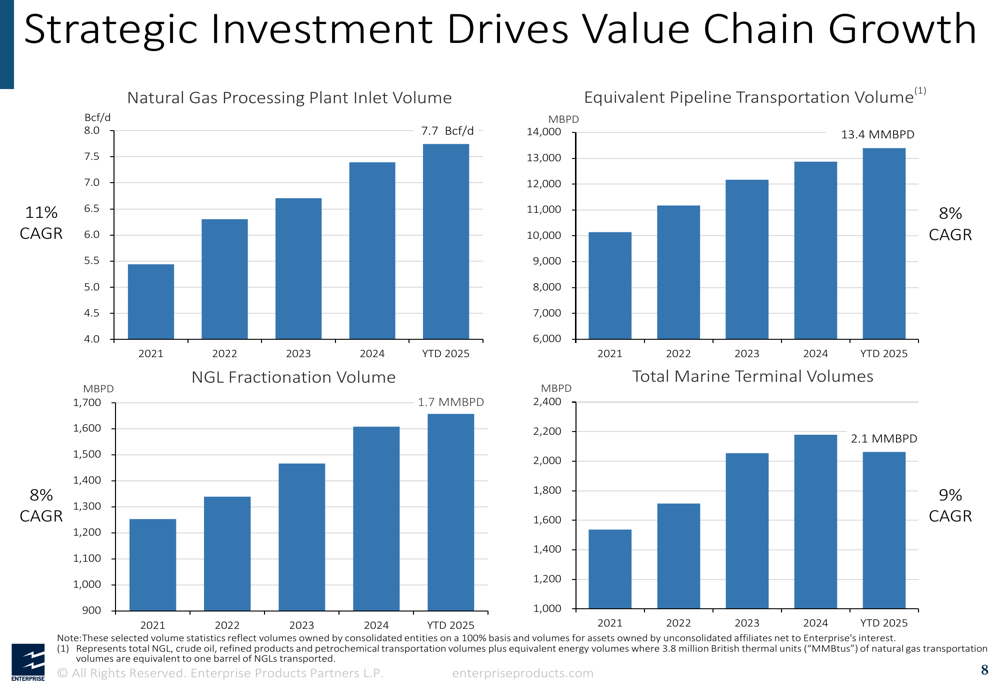

These strategic investments have driven significant volume growth across key metrics, with Natural Gas Processing Plant Inlet Volume growing at a CAGR of 11%, NGL Fractionation Volume at 8% CAGR, and Total (EPA:TTEF) Marine Terminal Volumes at 9% CAGR:

Forward-Looking Statements

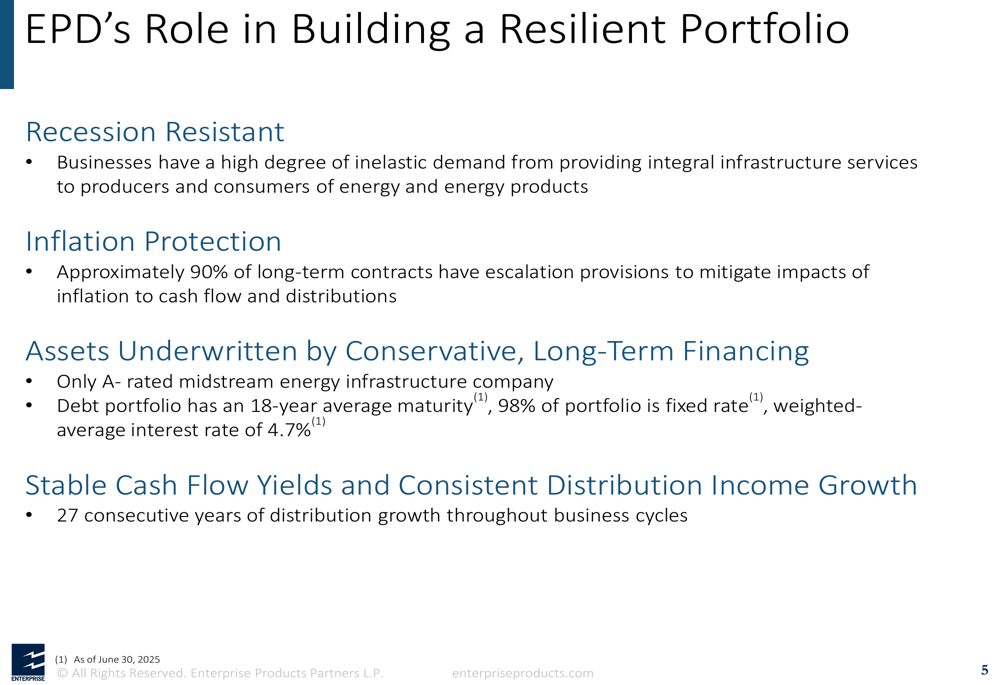

Enterprise Products emphasized its resilient business model, highlighting that approximately 90% of its long-term contracts have escalation provisions to mitigate the impacts of inflation. As the only A- rated midstream energy infrastructure company, Enterprise maintains a strong financial position with a debt portfolio featuring an 18-year average maturity, 98% fixed rate, and a weighted-average interest rate of 4.7% as of June 30, 2025.

The company’s resilient portfolio characteristics are summarized in the following slide:

Looking ahead, Enterprise Products expects to maintain its disciplined approach to capital allocation while advancing its strategic growth initiatives. The company’s focus on fee-based contracts and integrated value chain should continue to provide stability in cash flows, even amid market volatility.

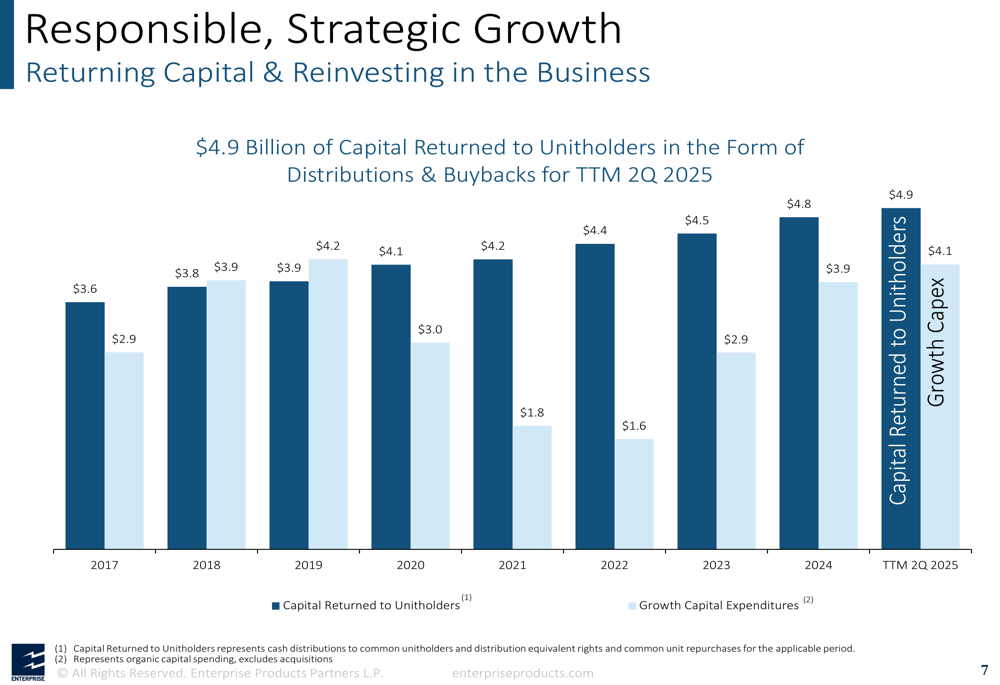

This balanced approach to growth and capital returns is illustrated in the following chart, showing the relationship between capital returned to unitholders and growth capital expenditures:

While Enterprise Products’ Q2 2025 presentation highlights the company’s operational strengths and strategic initiatives, investors will be watching closely to see if the company can translate its gross operating margin growth into improved earnings per unit after the previous quarter’s EPS miss. With substantial capital projects underway and a consistent focus on returning capital to unitholders, Enterprise Products appears positioned to maintain its long-term growth trajectory despite near-term segment performance variations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.