One & One Green Technologies stock soars 100% after IPO debut

Introduction & Market Context

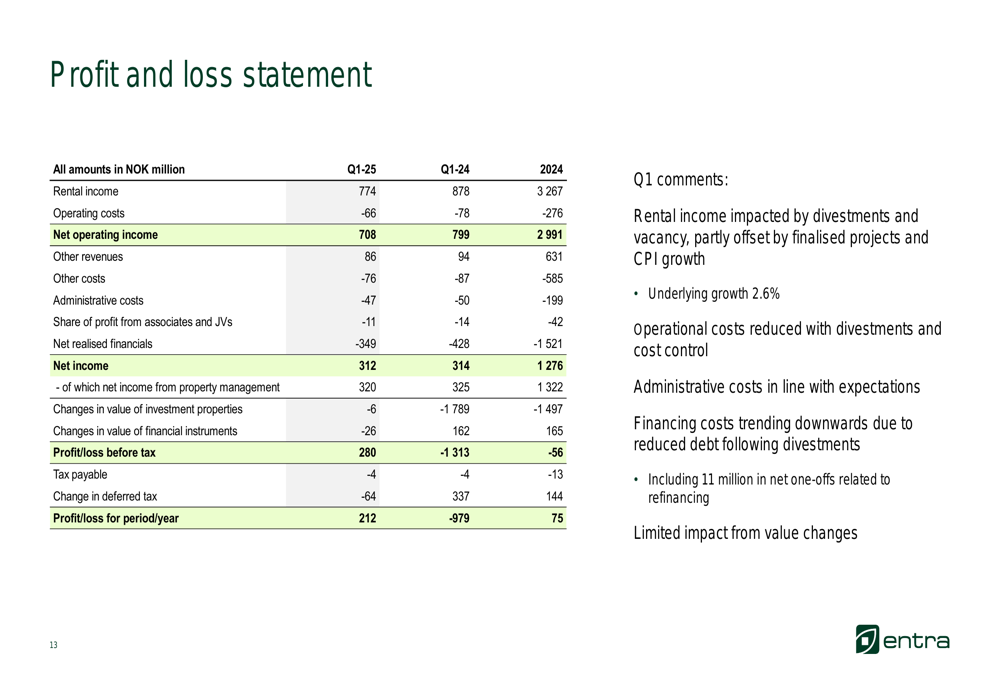

Norwegian commercial real estate company Entra reported a significant turnaround in profitability for the first quarter of 2025, according to its presentation released on April 29. The company posted a profit before tax of NOK 280 million, a substantial improvement from the NOK 1,331 million loss in the same period last year, despite ongoing challenges with negative net letting and reduced rental income.

Entra operates in a Norwegian economy described as "solid and stable," supported by the sovereign wealth fund, with March 2025 CPI at 2.6% and the key policy rate at 4.5%. The company noted positive market trends including a reversal of work-from-home patterns, increasing tenant search activity, and low overall vacancy rates in its core markets.

Quarterly Performance Highlights

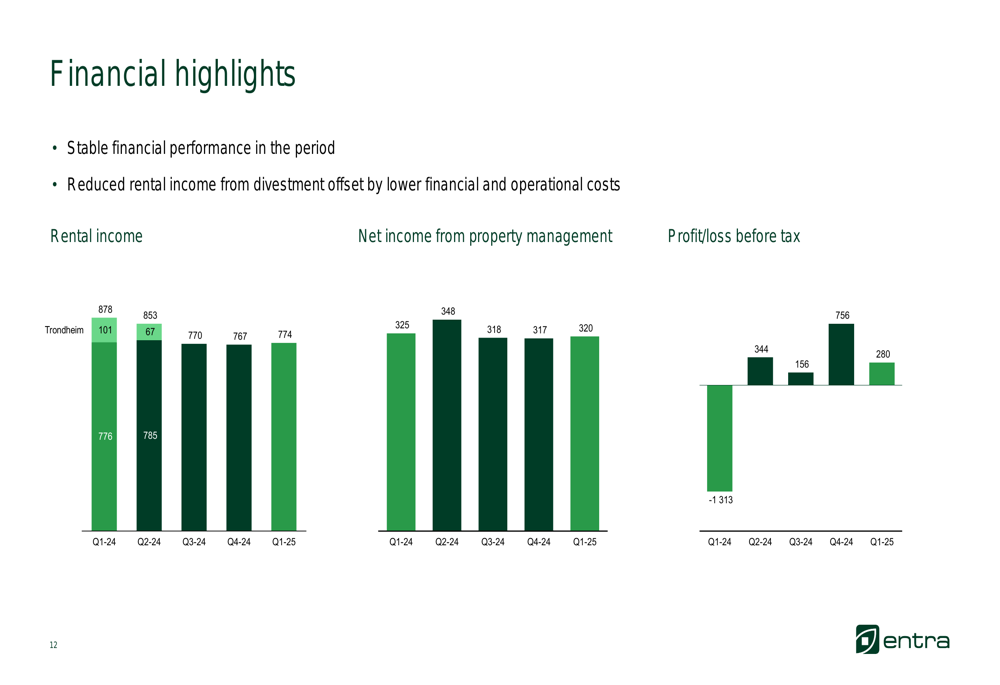

Entra reported rental income of NOK 774 million for Q1 2025, down from NOK 878 million in Q1 2024, primarily due to property divestments. However, the company achieved underlying rental income growth of 2.6% when adjusted for these divestments.

Net income from property management reached NOK 320 million, slightly below the NOK 325 million reported in Q1 2024 but showing resilience despite the reduced rental income base. The most significant improvement came in net value changes, which were only NOK -32 million compared to NOK -1,553 million in Q1 2024, suggesting a stabilization of property values after previous declines.

As shown in the following financial highlights chart:

The company’s profit before tax of NOK 280 million represents a dramatic improvement from the NOK 1,331 million loss in Q1 2024, indicating a potential turning point in Entra’s financial performance.

Operational Updates

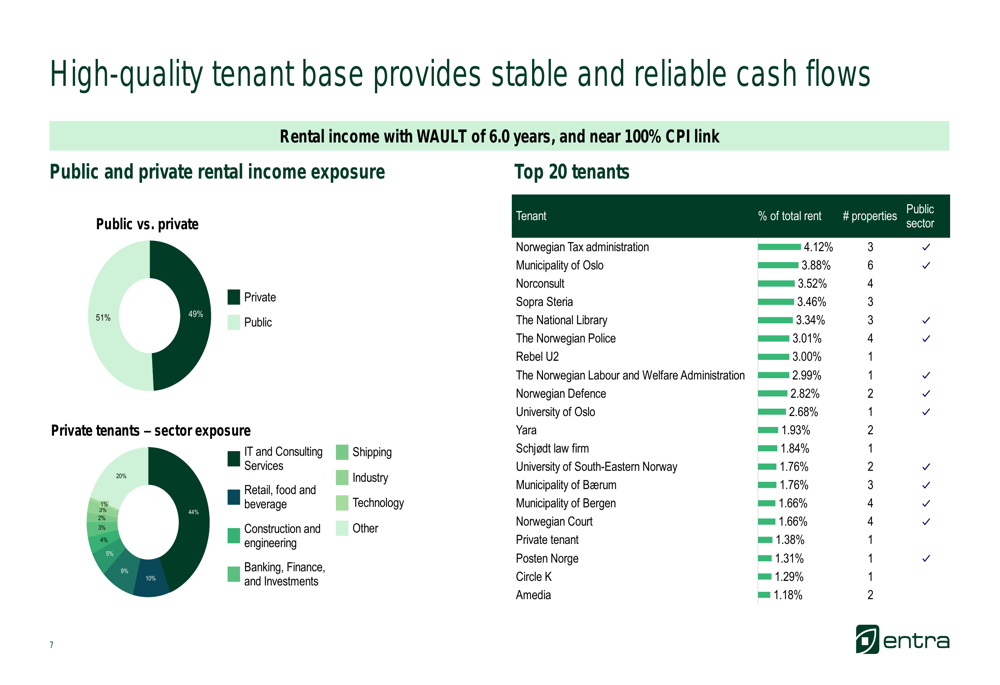

Entra’s operational metrics showed mixed performance. The company reported negative net letting of NOK 73 million for the quarter, with new and renewed leases of NOK 98 million (34,900 sqm) offset by terminated contracts of NOK 117 million (30,400 sqm). Occupancy stood at 93.8%, with a weighted average unexpired lease term (WAULT) of 6.0 years.

The company maintains a high-quality tenant base with 51% of rental income coming from public sector tenants, providing stability to its cash flows. The remaining 49% comes from private sector tenants diversified across IT and consulting services (20%), banking and finance (10%), and construction and engineering (9%).

The following slide illustrates the company’s tenant base composition and rental income stability:

Entra’s development portfolio includes several ongoing projects, with the largest being Brynsengfaret 6 in Oslo (35,400 sqm, 76% occupancy) and Nonnesetergaten 4 in Bergen (17,300 sqm, 55% occupancy). These projects are expected to contribute to future rental income growth upon completion.

Financial Position

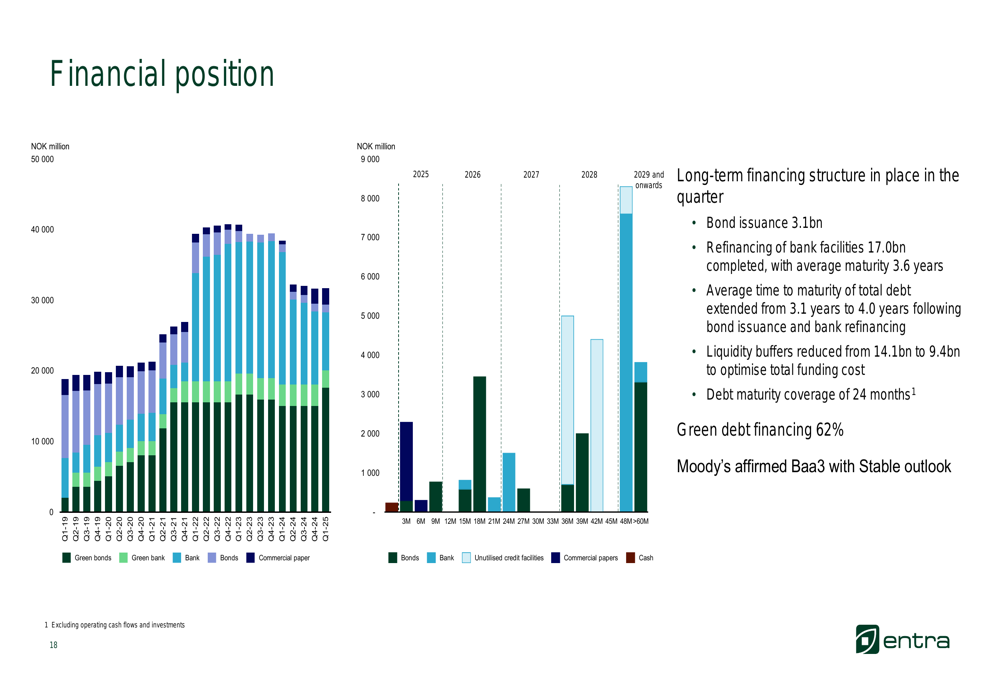

A significant focus during the quarter was strengthening Entra’s financial position through debt refinancing. The company placed bonds of NOK 3.1 billion and closed bank refinancing of NOK 17.0 billion, extending the average time to maturity of debt to 4.0 years from 3.1 years at the end of Q4 2024.

Key debt metrics showed improvement, with the interest coverage ratio increasing to 1.98x from 1.91x in Q4 2024, and the leverage ratio decreasing by 0.2 percentage points to 49.1%. Net debt to EBITDA remained stable at 11.7x. Moody’s affirmed Entra’s Baa3 credit rating with a stable outlook.

The company’s debt structure and maturity profile are illustrated in the following chart:

Entra reported that 62% of its debt financing is now classified as green, aligning with its sustainability focus. The company also highlighted its strong performance in EU Taxonomy alignment, with 46% of revenues and 71% of capex being taxonomy-aligned.

Forward-Looking Statements

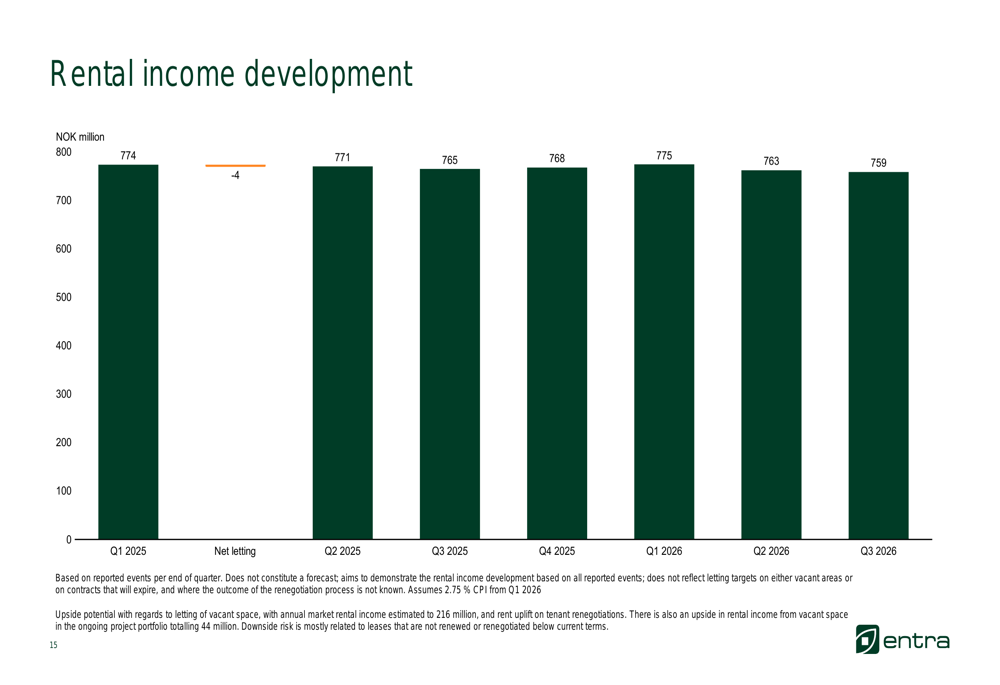

Looking ahead, Entra expects rental income growth to be driven by CPI adjustments, completion of development projects, rent uplift potential, and letting of vacant space. The company forecasts rental income to remain relatively stable through Q3 2026, assuming 2.75% CPI from Q1 2026.

The following chart shows Entra’s rental income development forecast:

Property values appear to have stabilized, with the total property value increasing by 0.6% in the quarter to NOK 63,045 million. The portfolio net yield for the next twelve months is projected at 4.86%, down from 4.99% in Q4 2024.

Entra’s management expressed confidence in the Norwegian economy, noting that "fiscal policy and public spending will continue to stabilise the economy," with expectations for lower interest rates and real wage growth. The transaction market was described as "active" with property values appearing to have "bottomed out."

Detailed Financial Analysis

The company’s profit and loss statement reveals the details behind its improved performance. While rental income decreased year-over-year, operating and administrative costs were also reduced. Financial costs decreased compared to Q1 2024, reflecting the benefits of the company’s refinancing activities.

The most significant factor in the improved bottom line was the minimal negative impact from property value changes (NOK -6 million) compared to the substantial negative adjustments (NOK -1,789 million) in Q1 2024.

The full profit and loss comparison is shown below:

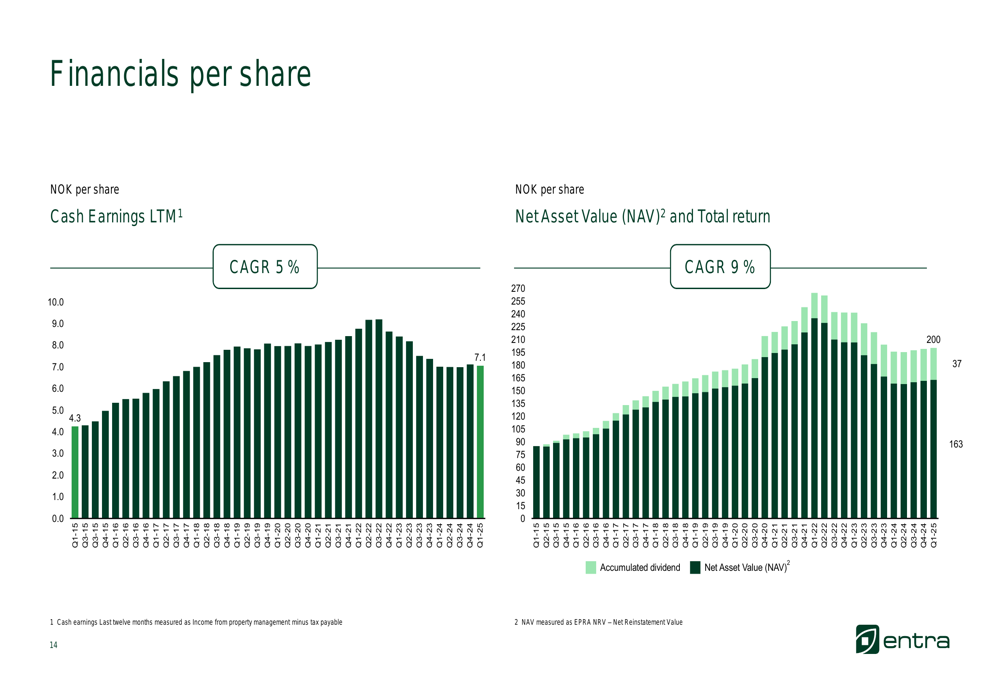

Net asset value (NRV) increased to NOK 163 per share, providing a measure of the underlying value of Entra’s property portfolio. Cash earnings and net asset value per share have shown consistent growth over time, with cash earnings achieving a 5% CAGR and net asset value a 9% CAGR.

Despite the improved profitability, Entra continues to face challenges with negative net letting and the need to offset the impact of property divestments on rental income. The company’s focus on debt refinancing and extending debt maturity appears to be a strategic priority to strengthen its financial position in anticipation of future growth opportunities as market conditions improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.