Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

Envista Holdings Corp (NYSE:NVST) presented its second quarter 2025 results on July 31, revealing accelerated growth and improved profitability across its dental portfolio. The company reported core sales growth of 5.6% and raised its full-year guidance, signaling confidence in its operational strategy despite ongoing macroeconomic uncertainties in the dental market.

The stock closed at $19.22 on the day of the presentation, up 1.2% in regular trading, though it dipped 1.77% in aftermarket trading to $18.88, suggesting mixed investor reaction to the results. According to the company, dental market fundamentals remain stable, providing a solid foundation for Envista’s performance improvement initiatives.

Quarterly Performance Highlights

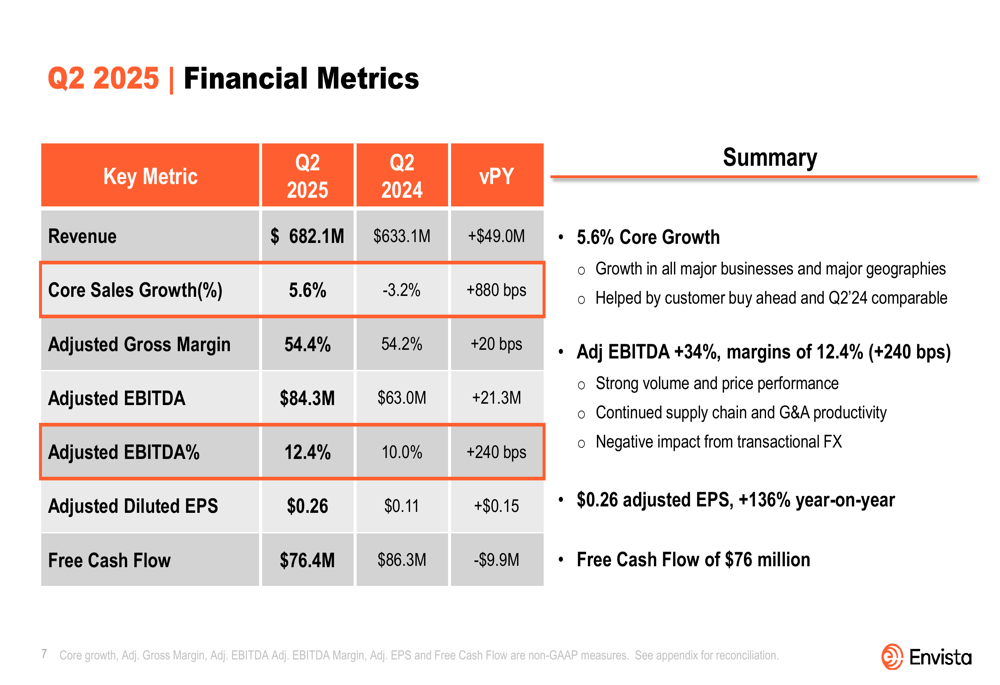

Envista reported Q2 2025 revenue of $682.1 million, representing a $49.0 million increase compared to the same period last year. Core sales growth reached 5.6%, a significant improvement of 880 basis points year-over-year. The company’s profitability metrics showed substantial enhancement, with adjusted EBITDA of $84.3 million, up $21.3 million from Q2 2024, and adjusted EBITDA margin expanding 240 basis points to 12.4%.

As shown in the following financial metrics summary:

Adjusted gross margin improved slightly to 54.4%, up 20 basis points year-over-year. Adjusted diluted EPS more than doubled to $0.26, representing a 136% increase compared to $0.11 in the prior year. Free cash flow remained strong at $76.4 million, though it decreased by $9.9 million compared to Q2 2024.

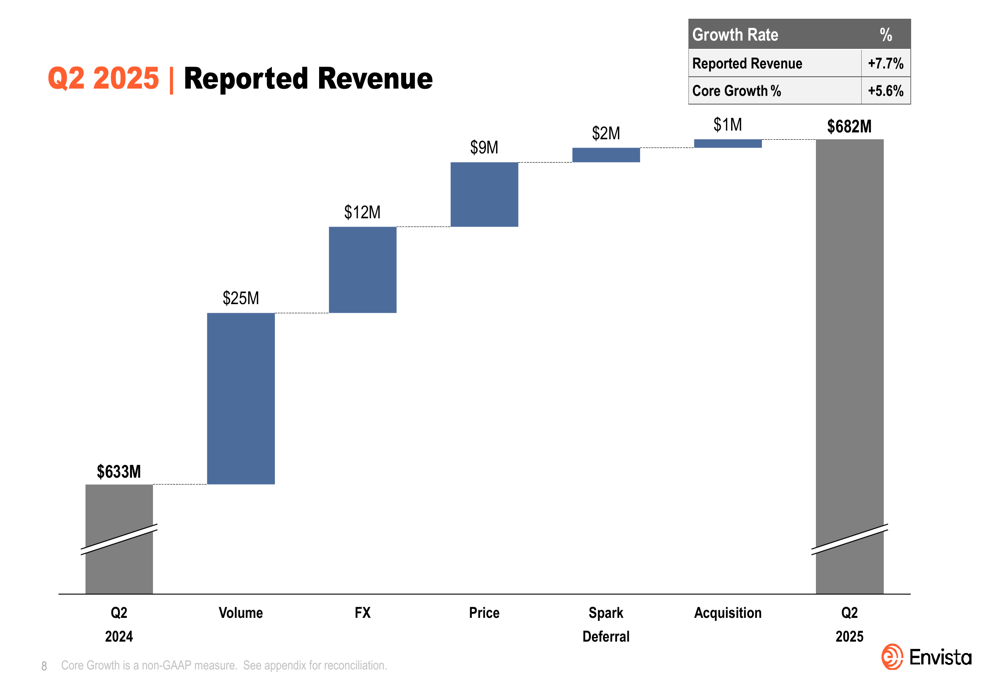

The company’s revenue growth was driven by multiple factors, as illustrated in this waterfall chart:

Volume contributed $25 million to the revenue increase, while favorable foreign exchange added $12 million and pricing actions contributed $9 million. These positive factors were partially offset by a $5 million reduction related to Spark deferral, with acquisitions adding a modest $2 million to the total.

Segment Performance

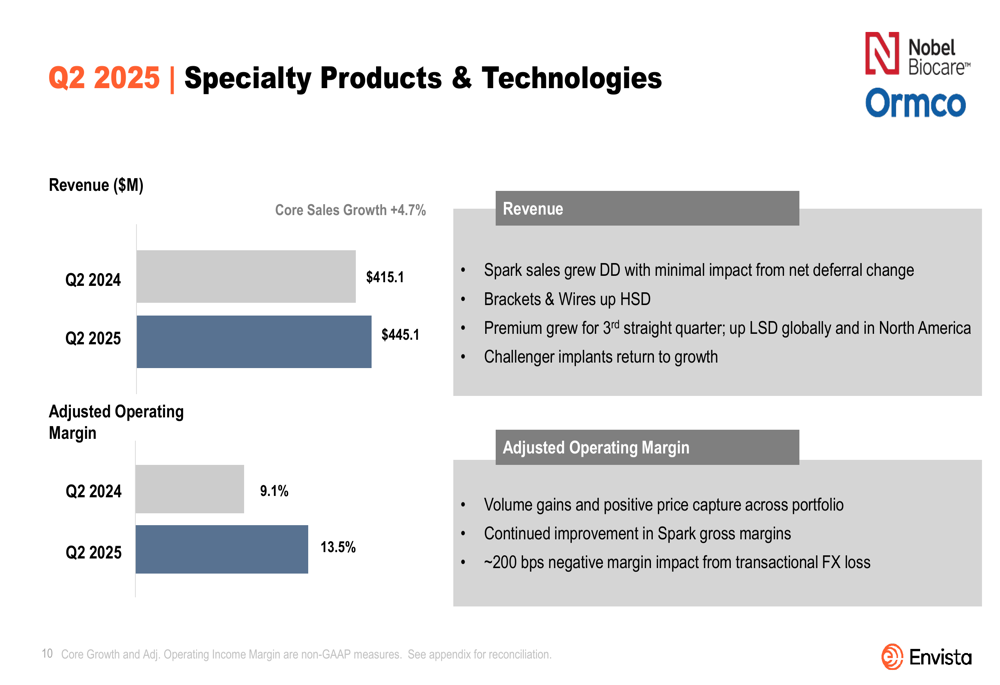

Envista’s two business segments both delivered solid performance in the quarter. The Specialty Products & Technologies segment, which includes the company’s orthodontic and implant businesses, reported revenue of $445.1 million, representing core sales growth of 4.7%. The adjusted operating margin for this segment improved dramatically to 13.5% from 9.1% in the prior year.

The segment’s performance details are illustrated below:

Notably, Spark clear aligners achieved double-digit growth with minimal impact from net deferral change, while brackets and wires grew at high single digits. The challenger implants business returned to growth, and the company reported continued improvement in Spark gross margins, a key focus area for investors.

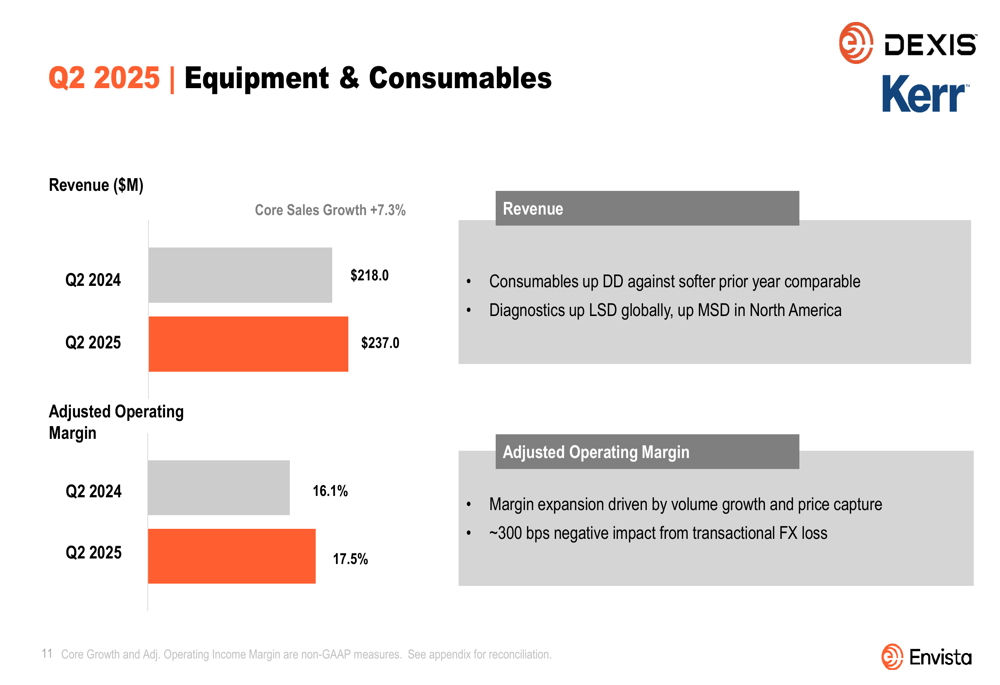

The Equipment & Consumables segment also performed well, with revenue reaching $237.0 million and core sales growth of 7.3%. The adjusted operating margin for this segment improved to 17.5% from 16.1% in the prior year.

The segment’s performance is summarized in the following slide:

Consumables grew at double-digit rates against softer prior year comparables, while Diagnostics grew at low single digits globally and mid-single digits in North America. The segment’s adjusted operating margin was driven by volume growth and price capture, though it included approximately 300 basis points of negative impact from transactional foreign exchange losses.

Updated Guidance and Outlook

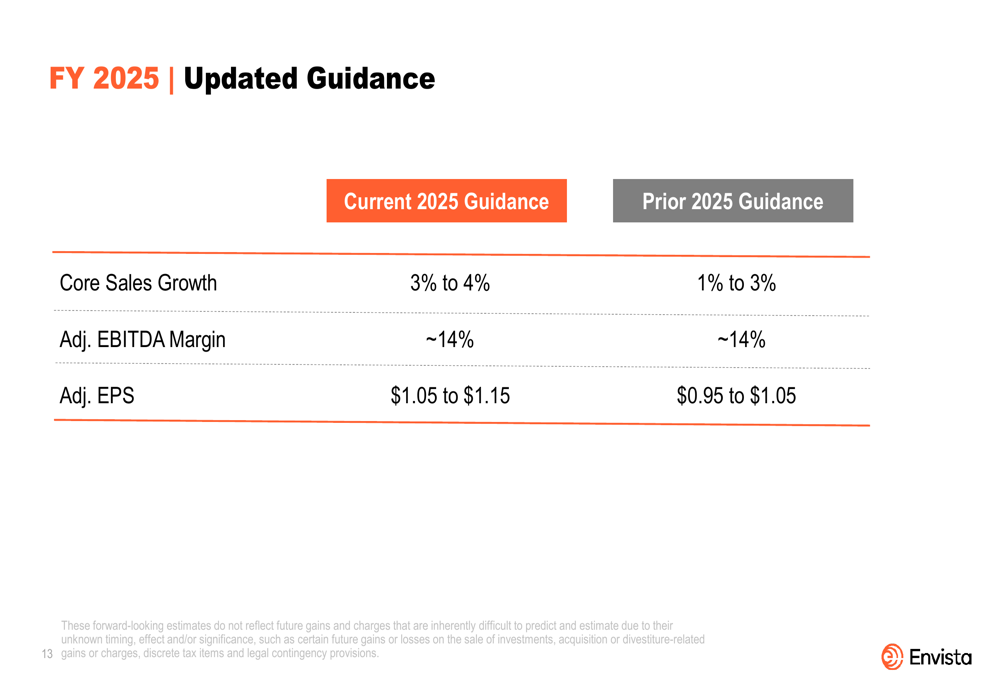

Based on the strong first-half performance, Envista raised its full-year 2025 guidance. The company now expects core sales growth of 3-4%, up from the previous guidance of 1-3%. Adjusted EPS guidance was also increased to $1.05-$1.15, compared to the previous range of $0.95-$1.05. The adjusted EBITDA margin guidance remained unchanged at approximately 14%.

The updated guidance is summarized in the following slide:

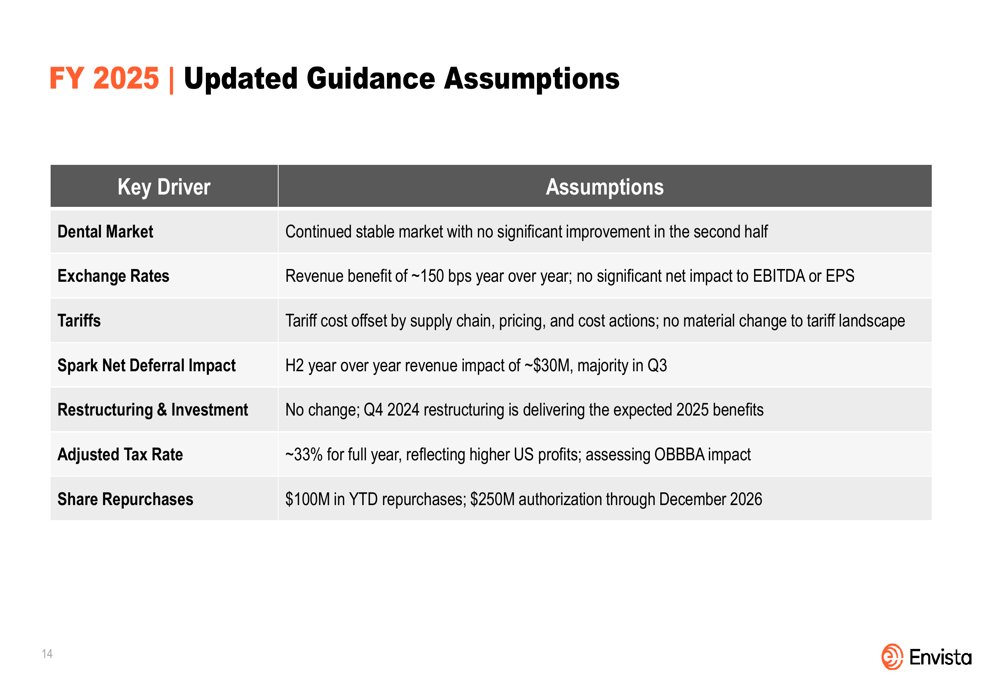

The guidance is based on several key assumptions, including a continued stable dental market, a revenue benefit of approximately 150 basis points year-over-year from exchange rates, and successful offset of tariff costs through supply chain and pricing actions. The company also expects a $30 million impact in the second half from Spark net deferral.

Additional guidance assumptions include:

Strategic Initiatives and Value Creation Plan

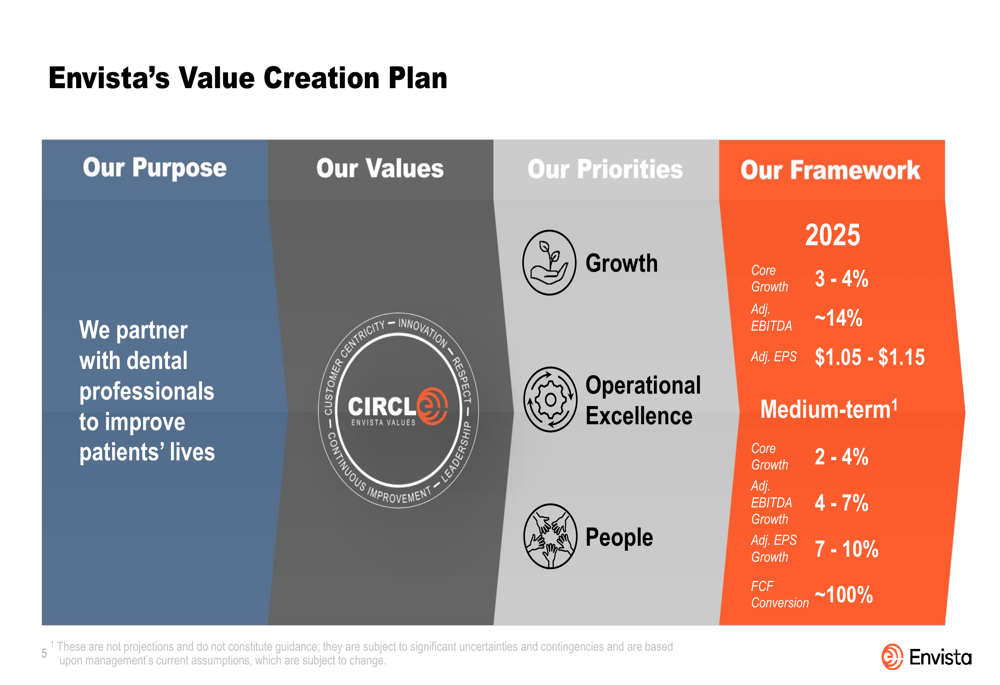

Envista’s performance improvements reflect the ongoing execution of its value creation plan, which focuses on growth, operational excellence, and people development. The company aims to achieve medium-term targets of 2-4% core growth, 4-7% adjusted EBITDA growth, and 7-10% adjusted EPS growth, with approximately 100% free cash flow conversion.

The company’s strategic framework is illustrated below:

In the first half of 2025, Envista increased its R&D investments by 14% to drive innovation and expanded its sales and marketing investments by 5%. The company also reported operational improvements, with G&A spending down 15% and customer service levels exceeding 95%.

During the quarter, Envista continued its share repurchase program, buying back 4.8 million shares. The company maintains a strong balance sheet with a net debt to adjusted EBITDA ratio of approximately 1x, providing financial flexibility for future investments and capital returns.

While the presentation highlighted numerous positive developments, investors should note potential risks mentioned in the earnings call, including the impact of China’s volume-based procurement on orthodontics, market acceptance of new pricing strategies, and possible delays in equipment purchases due to economic uncertainties. The company also faces a high projected tax rate of 33% for the full year, which could impact bottom-line results.

Overall, Envista’s Q2 2025 presentation demonstrated meaningful progress in the company’s strategic initiatives, with improved financial performance and raised guidance suggesting continued momentum in the second half of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.