Praxis Precision Medicines general counsel sells $4.8m in shares

Introduction & Market Context

EOG Resources (NYSE:EOG) released its second-quarter 2025 earnings presentation on August 8, showcasing solid financial results amid the integration of its strategic Encino acquisition. The company's stock closed at $115.97 on August 7, representing a modest recovery from its position after Q1 earnings, when it closed at $111.68 following a 1.74% drop.

The presentation highlights EOG's continued focus on its four strategic pillars: capital discipline, operational excellence, sustainability, and culture. These elements form the foundation of the company's approach to creating sustainable value through industry cycles, positioning EOG among the highest return and lowest cost producers in the sector.

Quarterly Performance Highlights

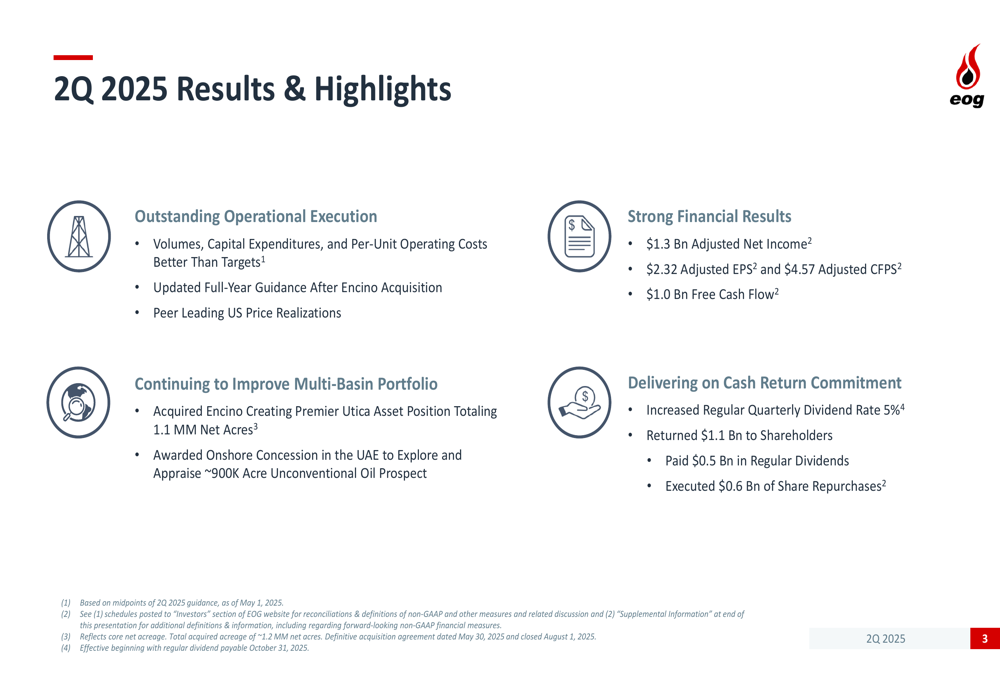

EOG reported adjusted net income of $1.3 billion for Q2 2025, translating to adjusted earnings per share of $2.32 and adjusted cash flow per share of $4.57. The company generated $1.0 billion in free cash flow during the quarter, demonstrating strong operational execution with volumes, capital expenditures, and per-unit operating costs all performing better than targets.

As shown in the following comprehensive overview of the quarter's performance:

Notably, EOG's Q2 2025 adjusted EPS of $2.32 represents a decrease from the $2.87 reported in Q1 2025, indicating some quarter-over-quarter pressure on earnings despite operational achievements. However, the company maintained strong price realizations across its product portfolio, significantly outperforming industry peers.

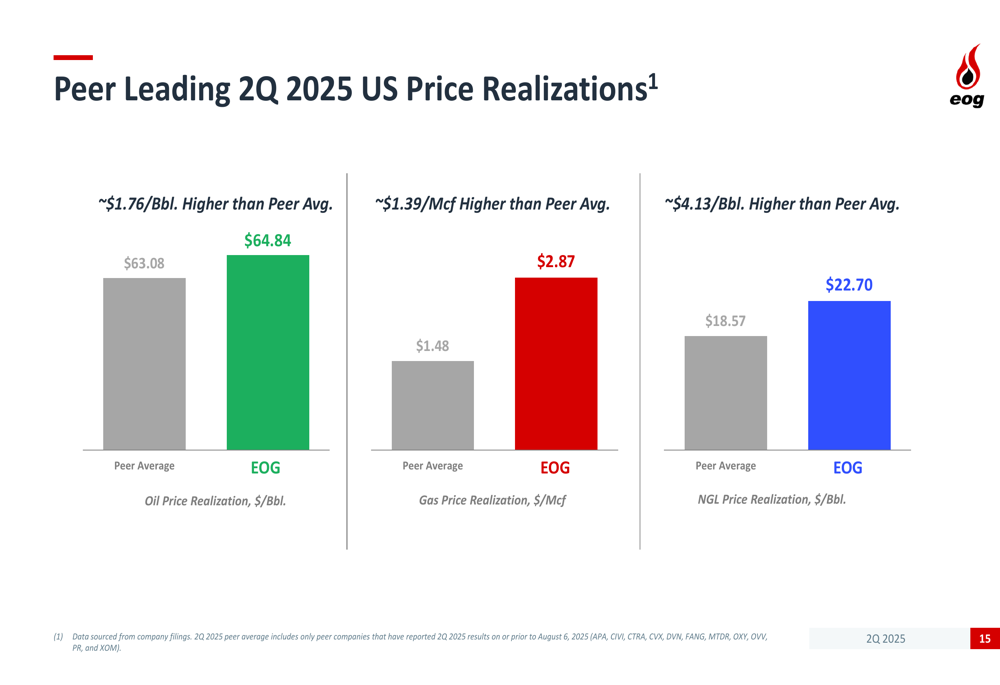

EOG achieved remarkable price realizations in Q2 2025, with oil prices at $64.84 per barrel (compared to peer average of $63.08), natural gas at $2.87 per Mcf (peer average:$1.48), and NGLs at $22.70 per barrel (peer average:$18.57). These superior realizations highlight the effectiveness of EOG's marketing strategy and infrastructure investments.

The following chart illustrates EOG's price realization advantage compared to peers:

Encino Acquisition & Portfolio Expansion

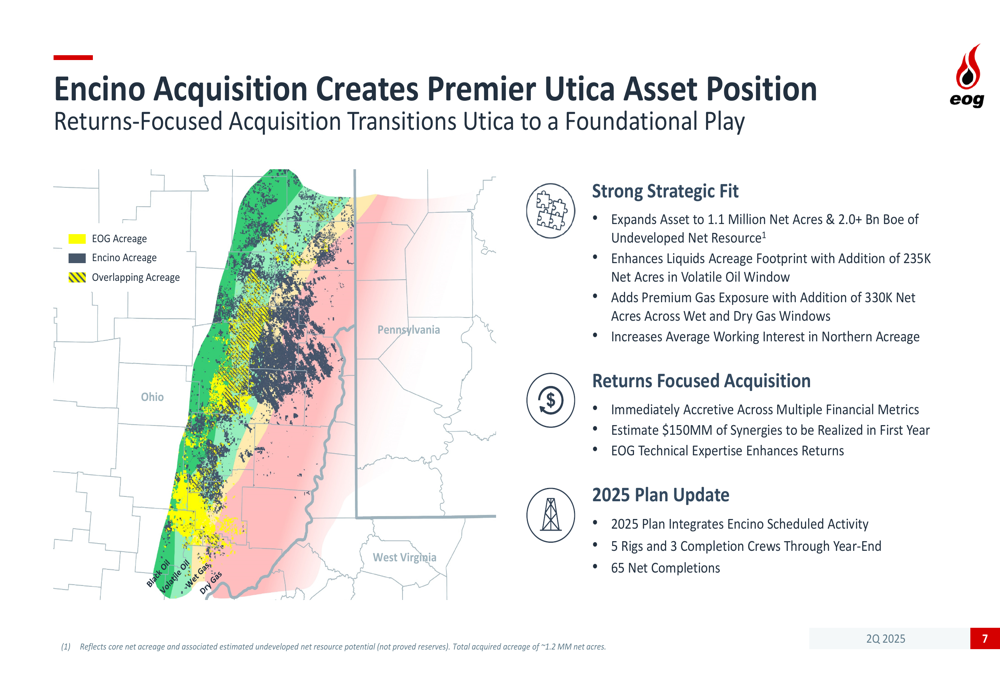

A significant focus of the presentation was EOG's recent acquisition of Encino, which has transformed the company's Utica asset into a premier position and foundational play. The acquisition enhances EOG's footprint to 1.1 million net acres with over 2.0 billion barrels of oil equivalent in undeveloped net resources in the Utica.

The strategic benefits of this acquisition are illustrated in the following slide:

EOG expects to realize $150 million in synergies during the first year following the acquisition. The company has already begun integrating Encino's scheduled activity, with plans for 5 rigs and 3 completion crews through year-end, resulting in 65 net completions.

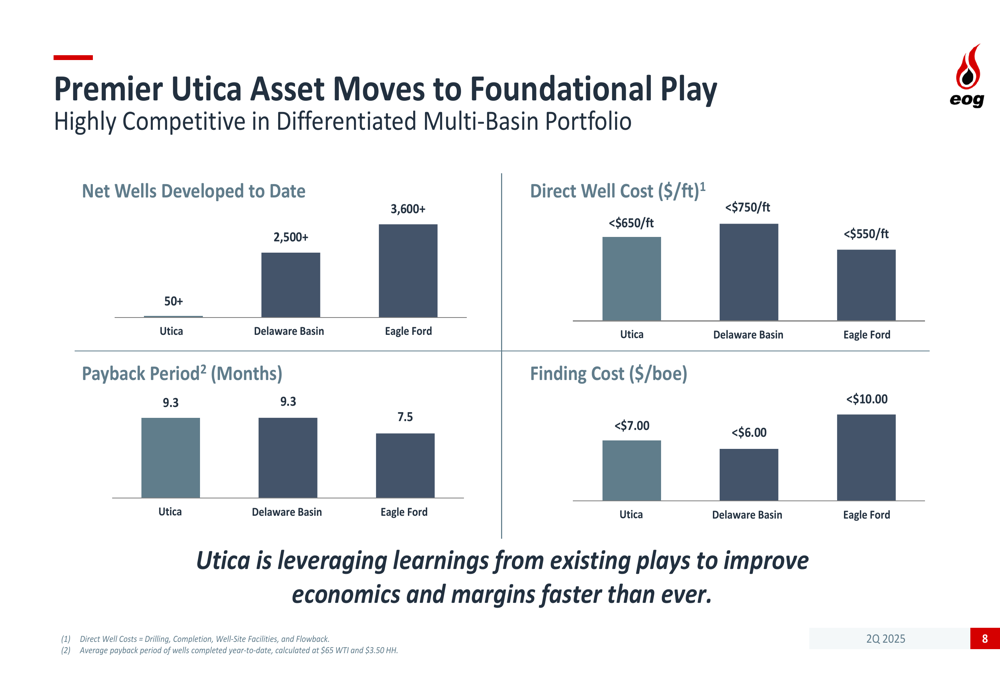

The Utica assets compare favorably with EOG's established plays in the Delaware Basin and Eagle Ford, as demonstrated in the following competitive metrics:

Beyond the Encino acquisition, EOG continues to expand internationally, securing an exploration concession in the UAE in partnership with ADNOC and establishing a JV partnership with Bapco in Bahrain. These international ventures leverage EOG's core competencies in exploration and technical expertise to improve its multi-basin portfolio.

Financial Position & Shareholder Returns

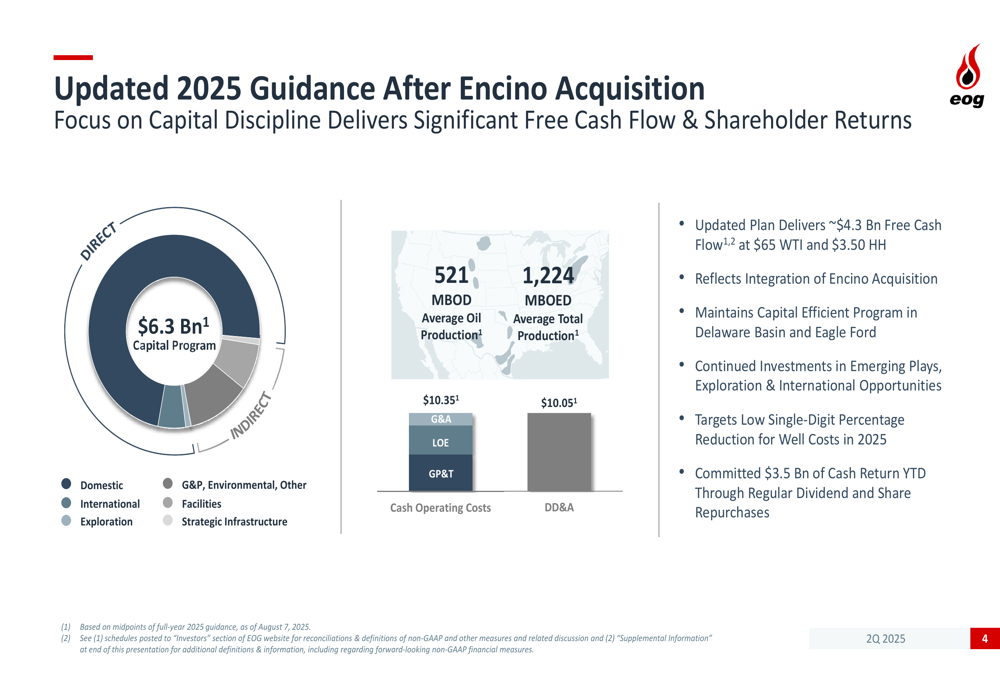

Following the Encino acquisition, EOG has updated its 2025 guidance, projecting approximately $4.3 billion in free cash flow at $65 WTI and $3.50 Henry Hub prices. The company's capital program for 2025 stands at $6.3 billion, with average oil production expected to reach 521 thousand barrels of oil per day (MBOD) and total production of 1,224 thousand barrels of oil equivalent per day (MBOED).

The updated guidance is detailed in the following slide:

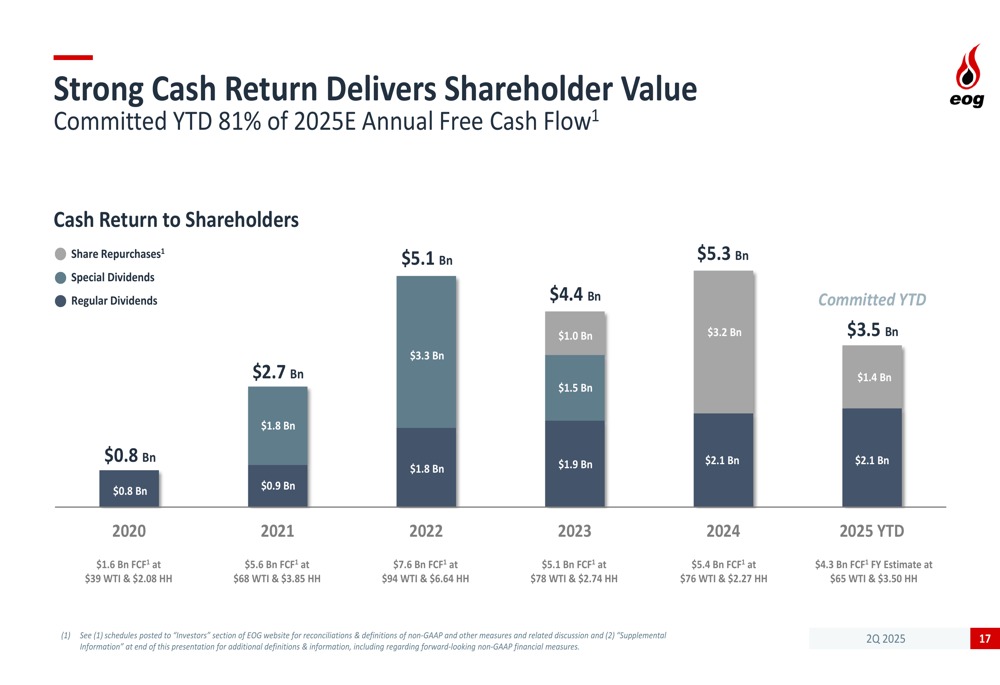

EOG continues to prioritize shareholder returns, increasing its regular quarterly dividend by 5% and returning $1.1 billion to shareholders in Q2 through $0.5 billion in regular dividends and $0.6 billion in share repurchases. Year-to-date, the company has committed $3.5 billion to shareholder returns, representing 81% of its estimated 2025 annual free cash flow.

The company's strong cash return strategy is illustrated in this chart:

EOG's commitment to sustainable and growing dividends remains a cornerstone of its shareholder return policy, with 2025 marking the 27th consecutive year of dividend payments. The company has increased its regular dividend by 8% for 2025, with a total cash return commitment of $2.1 billion through regular dividends alone.

Forward-Looking Statements

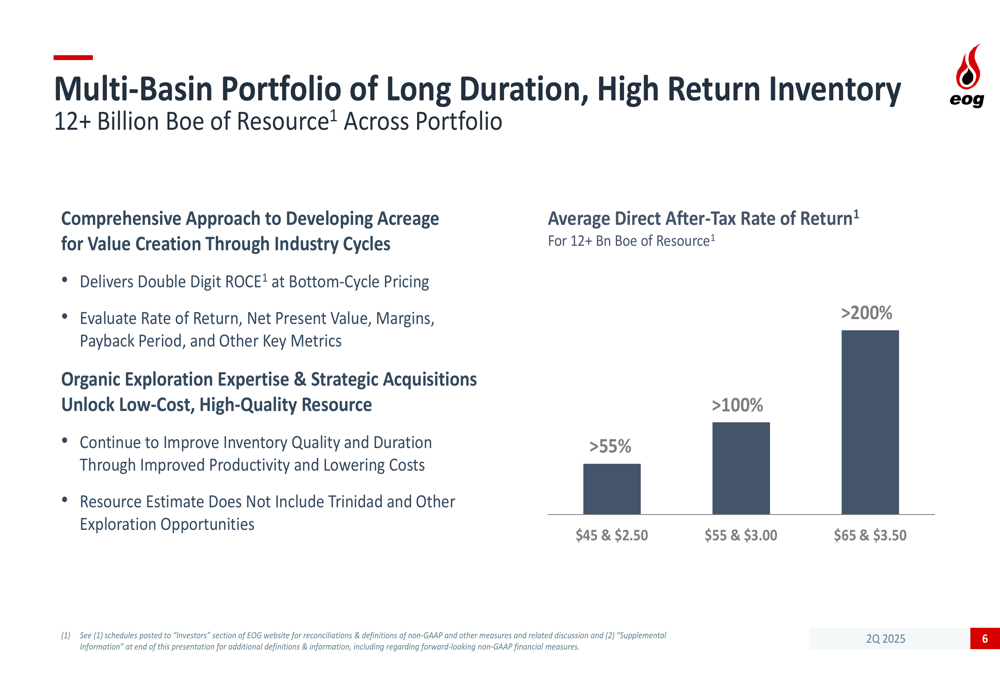

Looking ahead, EOG's multi-basin portfolio strategy continues to position the company for success across industry cycles. The company estimates it has over 12 billion barrels of oil equivalent in resources across its portfolio, delivering double-digit returns on capital employed even at bottom-cycle pricing.

The following slide illustrates the return profile of EOG's portfolio under various pricing scenarios:

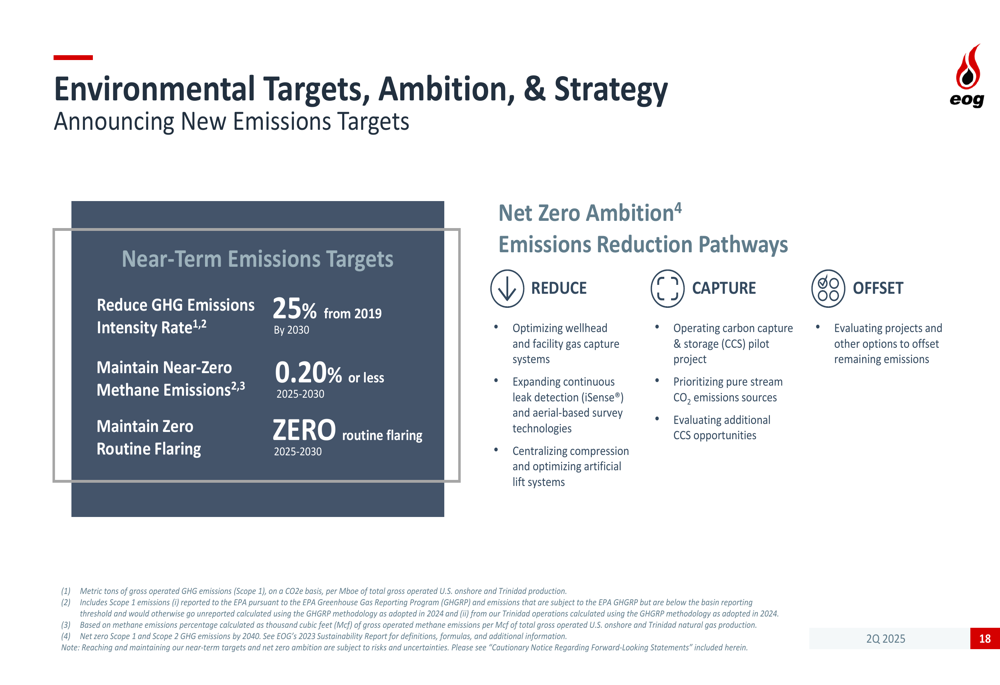

EOG also remains committed to its environmental targets, aiming to reduce greenhouse gas emissions intensity by 25% from 2019 levels by 2030, while maintaining near-zero methane emissions and zero routine flaring between 2025 and 2030. The company's long-term ambition is to achieve net zero emissions through a combination of reduction, capture, and offset strategies.

The company's environmental commitments are outlined here:

With its disciplined capital approach, operational excellence across multiple basins, and strategic portfolio expansion, EOG appears well-positioned to continue delivering strong returns to shareholders while navigating industry cycles and advancing its sustainability goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.