How are energy investors positioned?

Introduction & Market Context

ERBUD SA (WSE:ERB) released its Q1 2025 investor presentation on May 20, 2025, highlighting a 14% year-over-year revenue increase amid challenging seasonal conditions that impacted profitability. The Polish construction group operates in a market expected to see 3.7% GDP growth in 2025, with inflation projected at 4.5% according to government forecasts.

The construction sector in Poland showed positive momentum in early 2025, with construction and assembly manufacturing growing 3.7% year-over-year in Q1. The economic trend indicator for the construction industry has also improved from -10.6 at the end of 2024 to -4.0 in April 2025, signaling gradually improving sentiment despite ongoing challenges.

As shown in the following revenue highlights, ERBUD achieved significant top-line growth despite market pressures:

Quarterly Performance Highlights

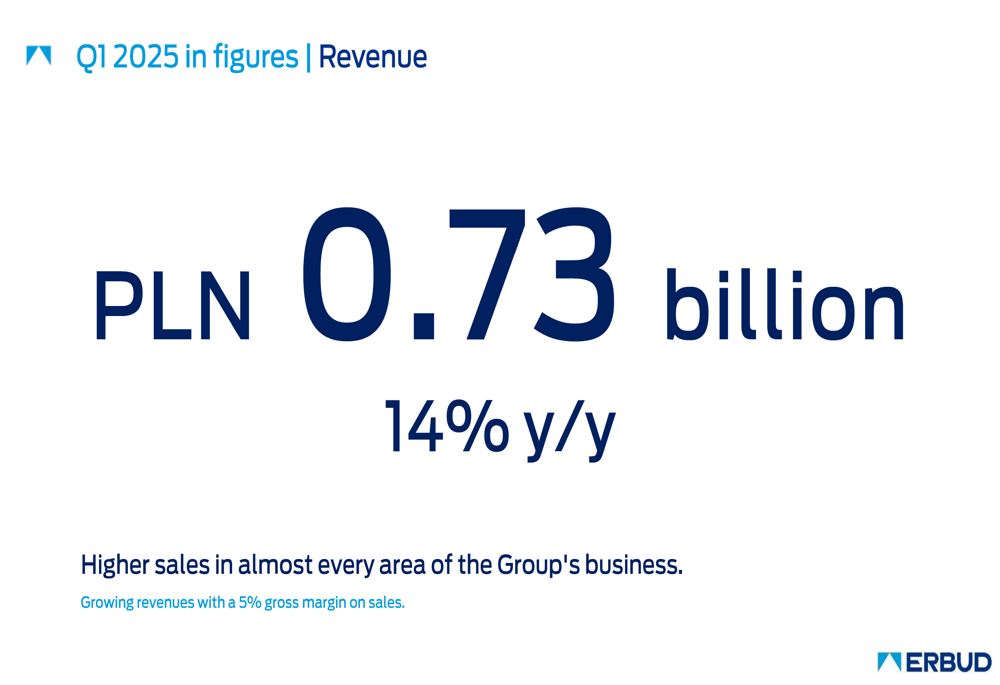

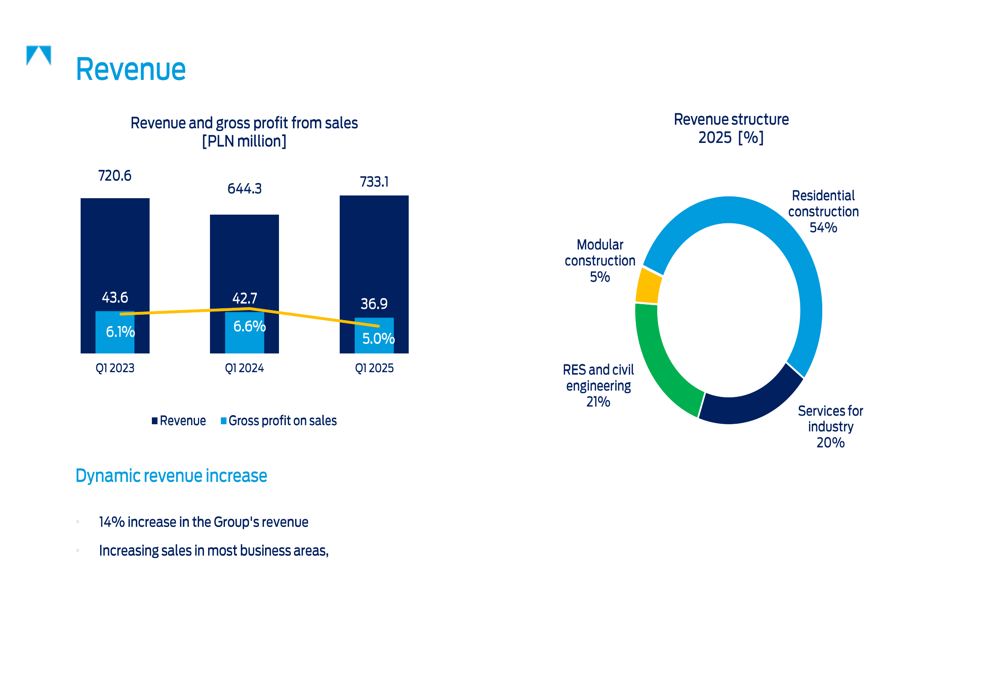

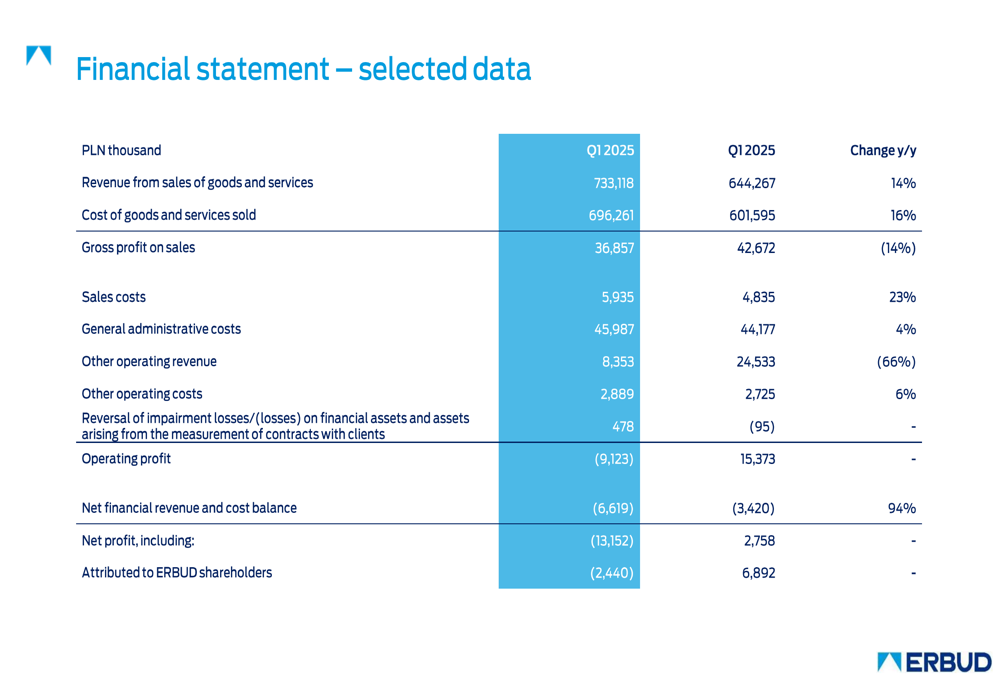

ERBUD reported revenue of PLN 0.73 billion in Q1 2025, representing a 14% increase compared to the same period last year. However, this growth came with compressed margins, as the gross profit margin declined to 5% from 6.6% in Q1 2024.

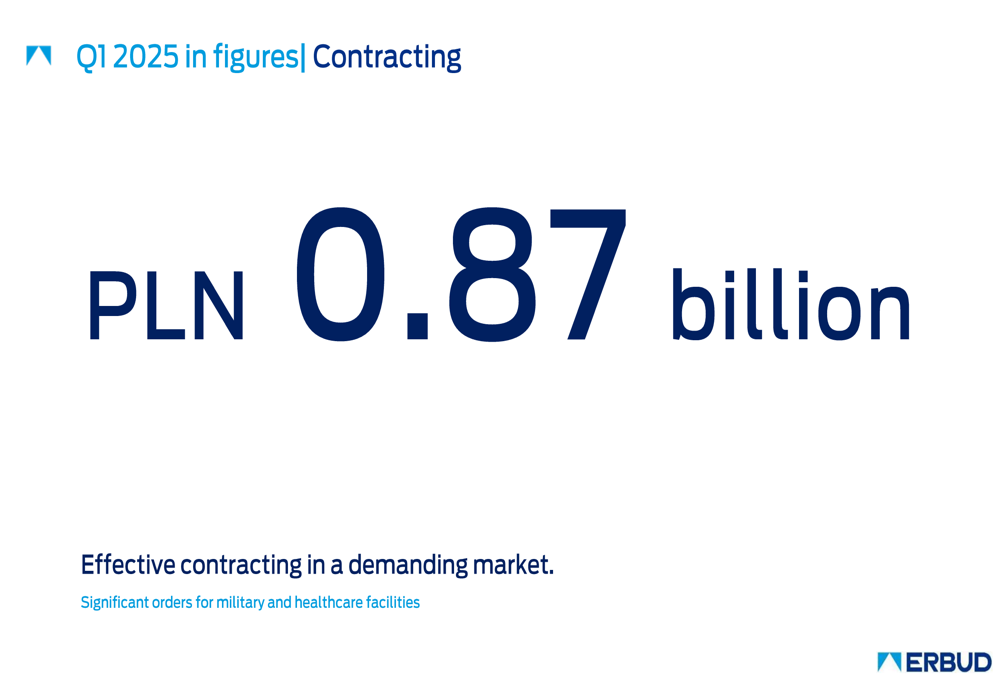

The company’s contracting activities remained robust at PLN 0.87 billion, with significant orders secured for military and healthcare facilities:

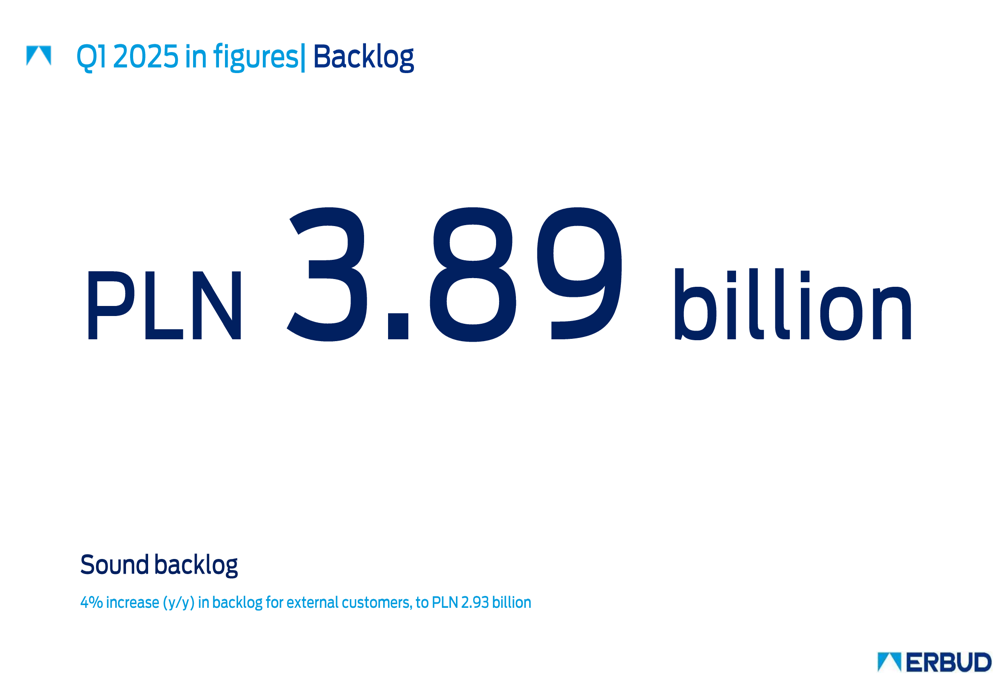

ERBUD’s backlog position strengthened to PLN 3.89 billion, with external customer backlog growing 4% year-over-year to PLN 2.93 billion, providing solid revenue visibility for the remainder of 2025:

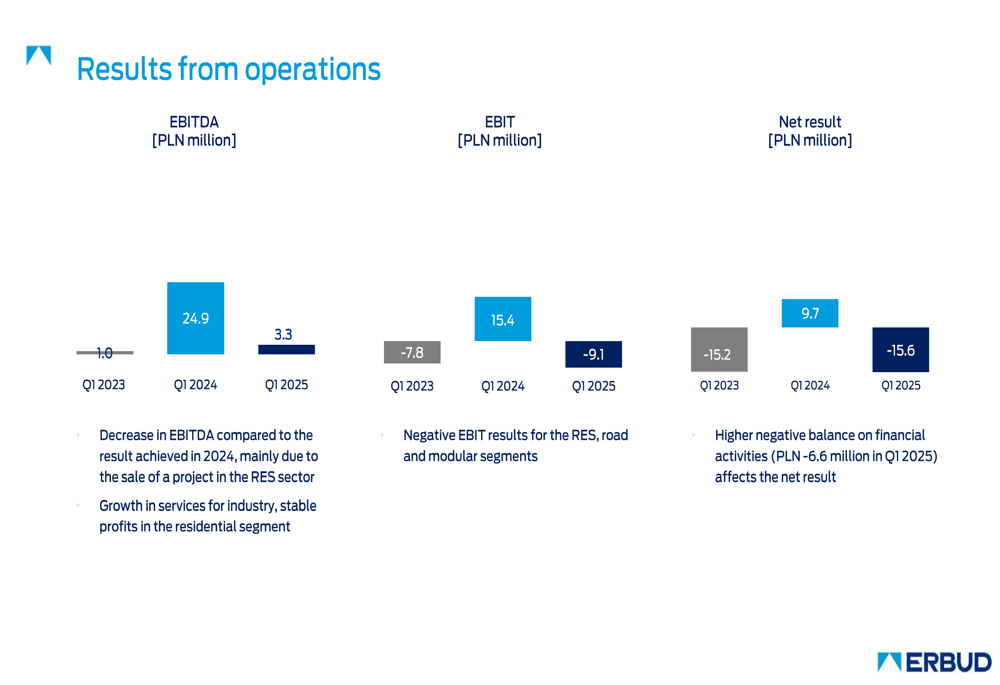

Despite the revenue growth, profitability metrics declined significantly compared to the strong Q1 2024 results. EBITDA fell to PLN 3.3 million from PLN 24.9 million in the prior year, while EBIT and net result both turned negative at PLN -9.1 million and PLN -15.6 million respectively. The company attributed this decline to seasonal factors and a strong comparative base:

The revenue structure for Q1 2025 shows residential construction dominating at 54% of total revenue, followed by RES and civil engineering at 21%, services for industry at 20%, and modular construction at 5%. This breakdown illustrates ERBUD’s diversified business model:

Segment Performance Analysis

ERBUD operates through four main business divisions, each with varying performance in Q1 2025:

1. Residential Construction: This largest segment reported sales of PLN 394 million, up from PLN 342 million in Q1 2024, with a backlog of PLN 1,757 million. The division benefits from orders worth PLN 1.2 billion to be completed in Q2-Q4 2025 and recent interest rate reductions that have improved investor sentiment.

2. RES and Civil Engineering: Operated through subsidiary ONDE, this division faced significant profitability challenges. As shown in the following chart, ONDE’s EBITDA declined to PLN -0.7 million in Q1 2025 from PLN 24.4 million in Q1 2024:

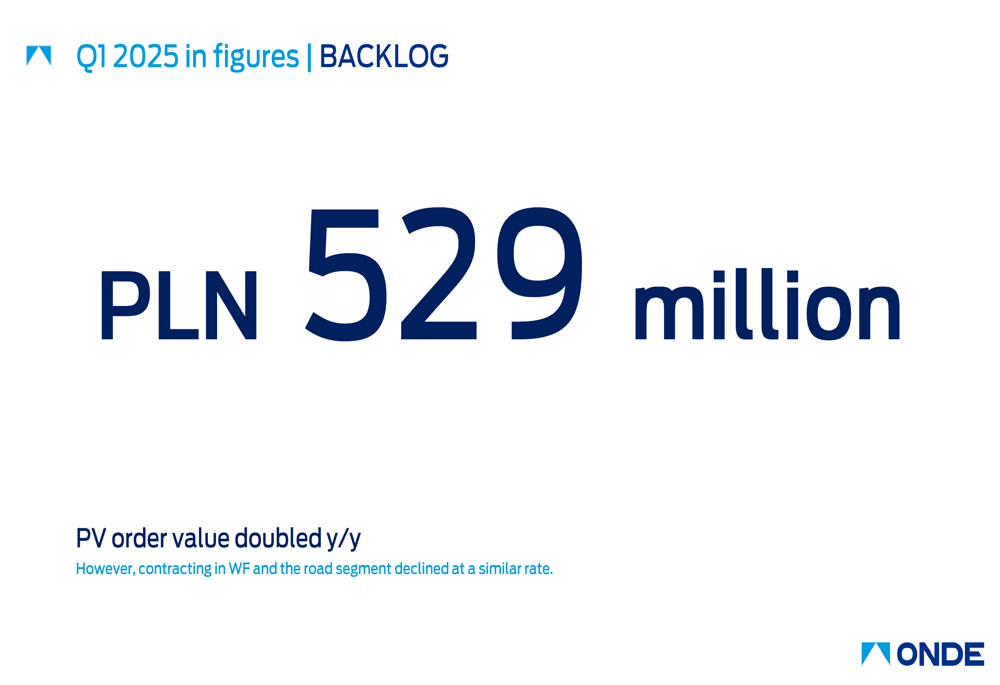

ONDE maintained a backlog of PLN 529 million, with photovoltaic order values doubling year-over-year, though contracting in wind farms and road segments declined:

Despite revenue pressure, ONDE reported a slight increase in gross sales profitability:

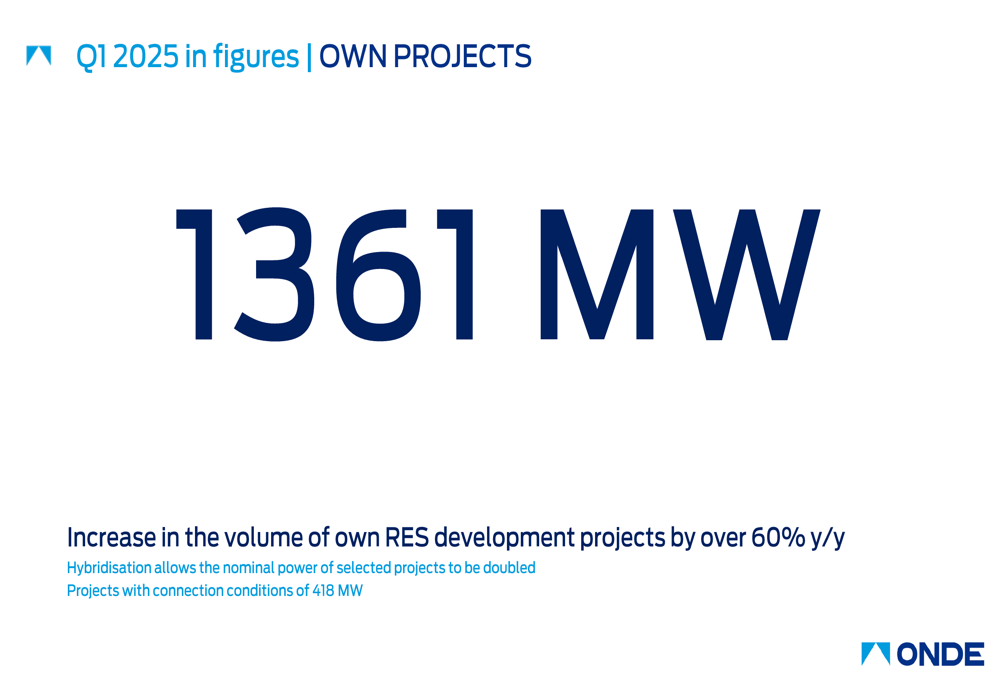

A bright spot for ONDE was the 60% year-over-year increase in its own renewable energy development projects to 1,361 MW:

3. Services for Industry: This segment showed improved performance compared to Q1 2024, with sales increasing slightly to PLN 579 million from PLN 573 million. The division reported that the increase in minimum wage had no significant impact on operations, and its domestic order portfolio offers promising prospects for the remainder of 2025.

4. Modular Timber Construction: The smallest but fastest-growing segment nearly doubled its revenue to PLN 38 million in Q1 2025 from PLN 20 million in Q1 2024. The backlog increased to PLN 231 million, supported by a recently signed contract worth EUR 10.05 million.

Financial Position and Outlook

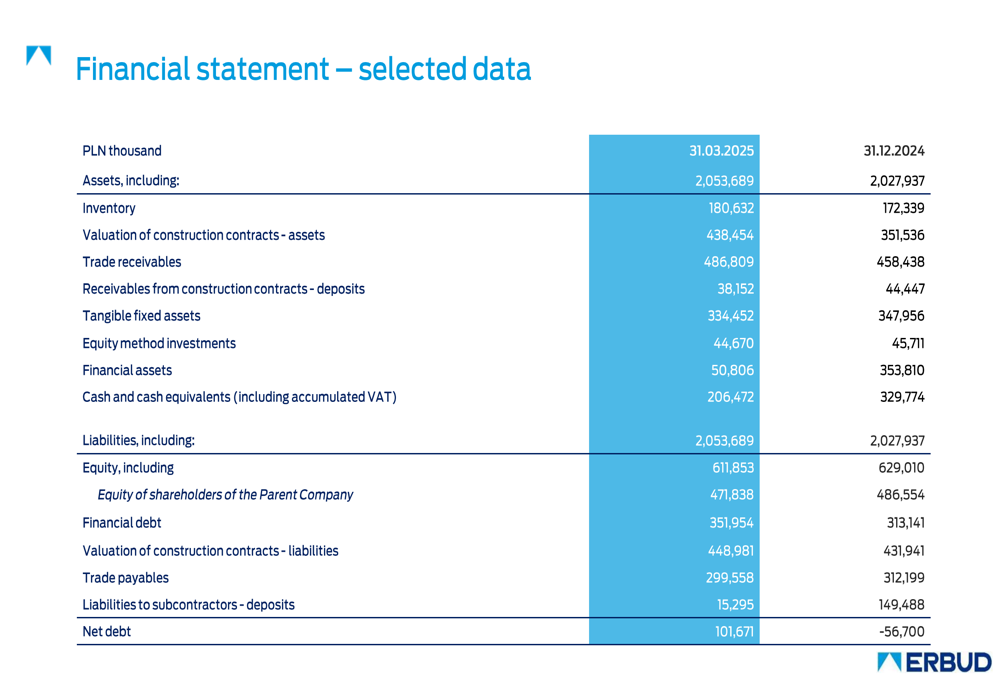

ERBUD maintained a strong balance sheet with PLN 206.5 million in cash, though net debt increased to PLN 103.7 million. The company’s financial statement shows total assets of PLN 2.05 billion as of March 31, 2025:

The income statement details reveal the pressure on profitability despite revenue growth, with cost of goods sold increasing at a faster rate (16%) than revenue (14%):

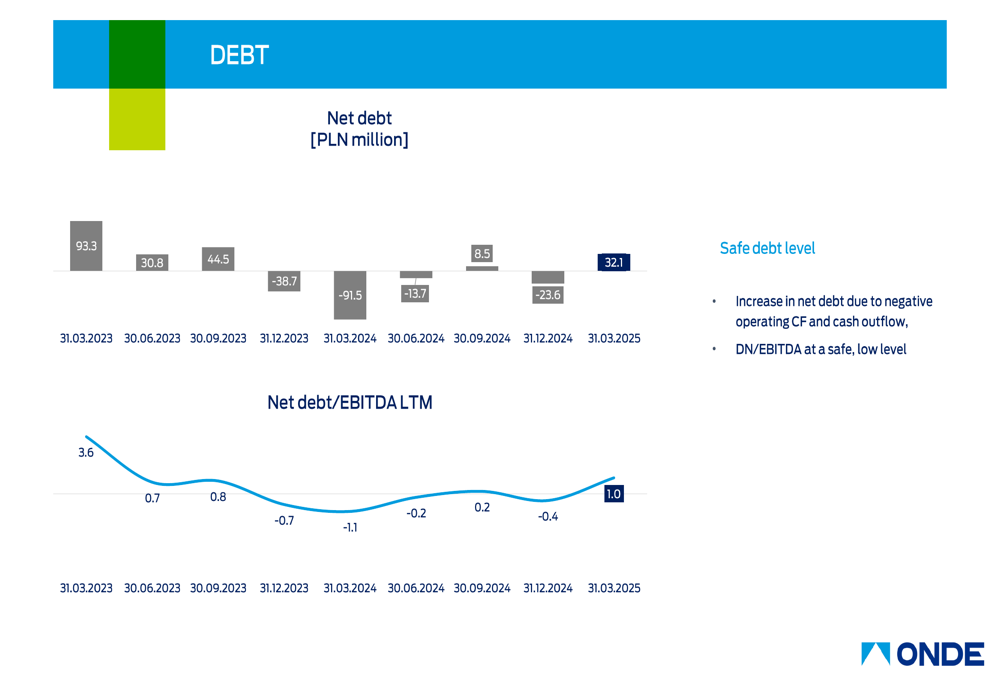

For ONDE specifically, the debt position has fluctuated significantly, moving from negative territory (net cash) back to a net debt position of PLN 32.1 million by the end of Q1 2025:

Market Challenges and Opportunities

ERBUD faces several market challenges, including downgraded economic growth forecasts for 2025, recession in Germany (affecting its industrial services division), and significant salary pressure with labor costs rising by more than 10% annually.

However, the company also identified several opportunities, including:

1. The exclusion of non-EU contractors from certain infrastructure tenders, reducing competition

2. Planned tenders worth approximately PLN 30 billion in 2025 for the Central Transportation Port (CPK)

3. Interest rate reductions improving investor sentiment

4. Government plans to allocate up to PLN 45 billion to social and municipal housing

In summary, while ERBUD demonstrated strong revenue growth in Q1 2025, the significant decline in profitability highlights the seasonal challenges and competitive pressures in the Polish construction market. The company’s diversified business model, solid backlog, and strong cash position provide some resilience as it navigates these challenges throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.