SAP sued by o9 Solutions over alleged trade secret theft

Introduction & Market Context

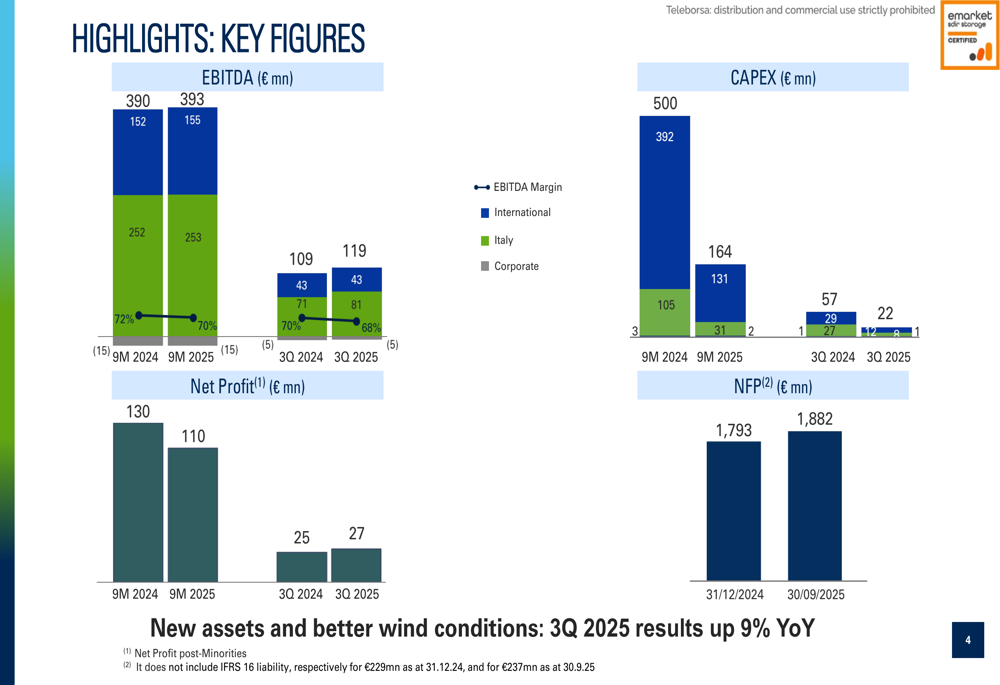

ERG reported a 9% year-over-year increase in third-quarter EBITDA to €119 million, driven by new assets and improved wind conditions. Despite these positive results presented on November 14, 2025, the company's stock dropped 3.78% to €22.20 in early trading, suggesting investors may have expected even stronger performance or were concerned about other aspects of the report.

The renewable energy company confirmed its full-year guidance while highlighting strategic initiatives including commissioning its first battery energy storage system (BESS) and bringing a new wind farm online in Northern Ireland.

Quarterly Performance Highlights

ERG's third-quarter results showed solid improvement over the same period last year. EBITDA reached €119 million, up 9% from €109 million in Q3 2024, while adjusted net profit grew to €27 million from €25 million in the prior year period.

Energy production increased significantly to 1,590 GWh in Q3 2025, up 10.3% from 1,441 GWh in Q3 2024, primarily due to new asset contributions and better wind conditions. However, the EBITDA margin compressed slightly from 70% to 68% year-over-year.

As shown in the following financial highlights chart, the company's performance metrics demonstrate growth in key areas despite some margin pressure:

For the first nine months of 2025, ERG reported EBITDA of €393 million, marginally higher than the €390 million recorded in the same period of 2024. However, net profit for the nine-month period decreased to €110 million from €130 million a year earlier, primarily due to higher financial expenses.

Detailed Financial Analysis

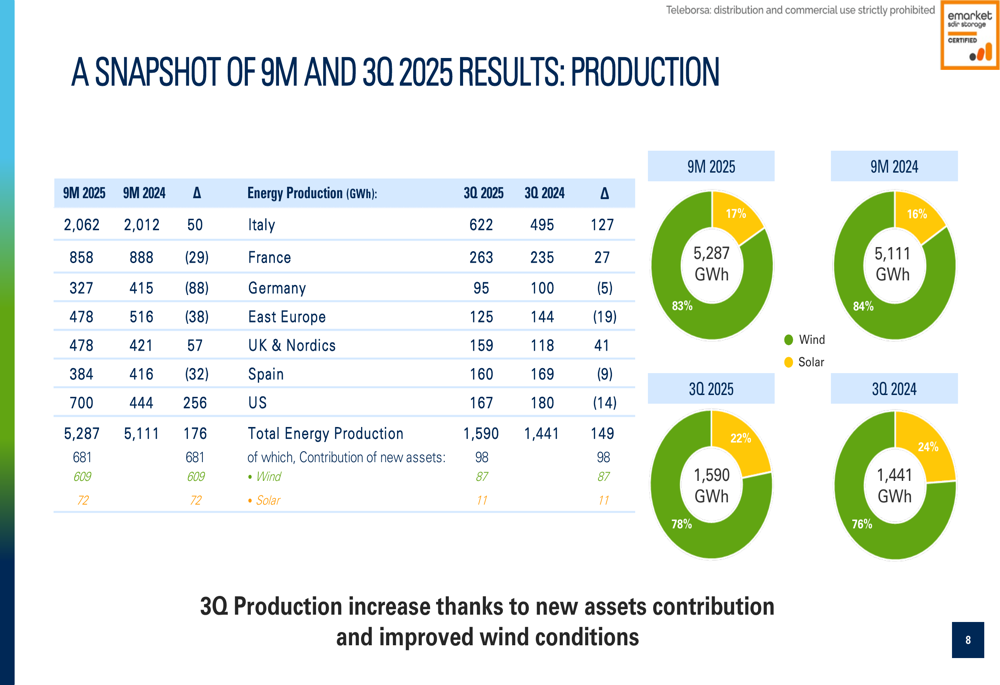

ERG's production snapshot reveals strong performance across multiple geographies, with particularly notable improvements in Italy, France, and the UK & Nordics regions during the third quarter. Total production increased by 149 GWh compared to Q3 2024.

The geographic breakdown of production demonstrates the company's diversified portfolio:

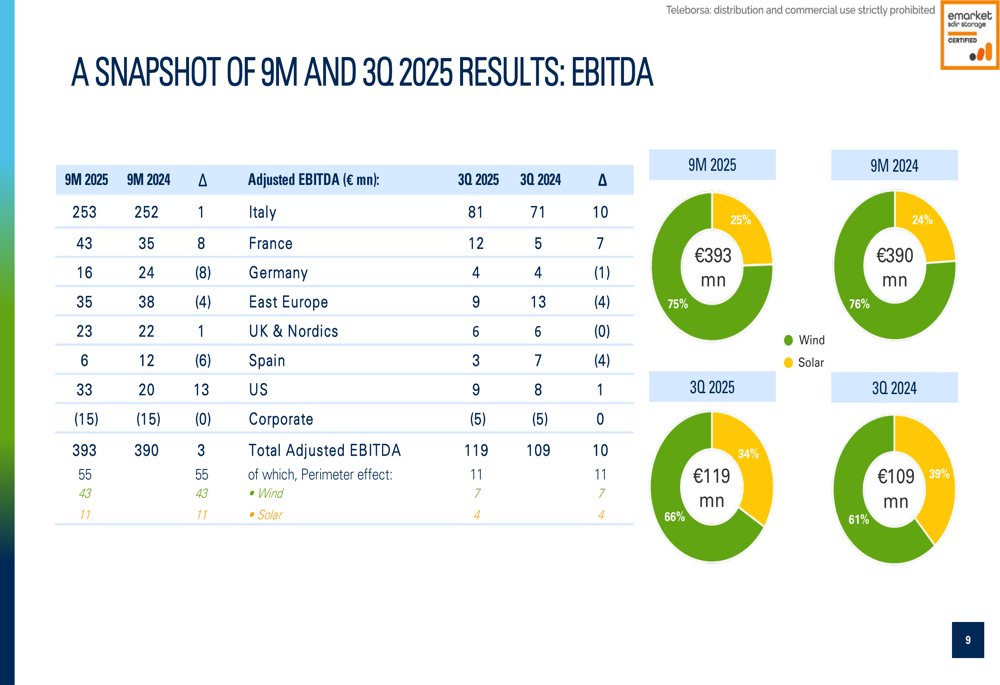

This production growth translated into improved EBITDA performance across several regions. Italy led the way with a €10 million increase in Q3 EBITDA, followed by France with a €7 million improvement. However, some markets including Eastern Europe and Spain showed declining performance.

The EBITDA breakdown by country illustrates these regional variations:

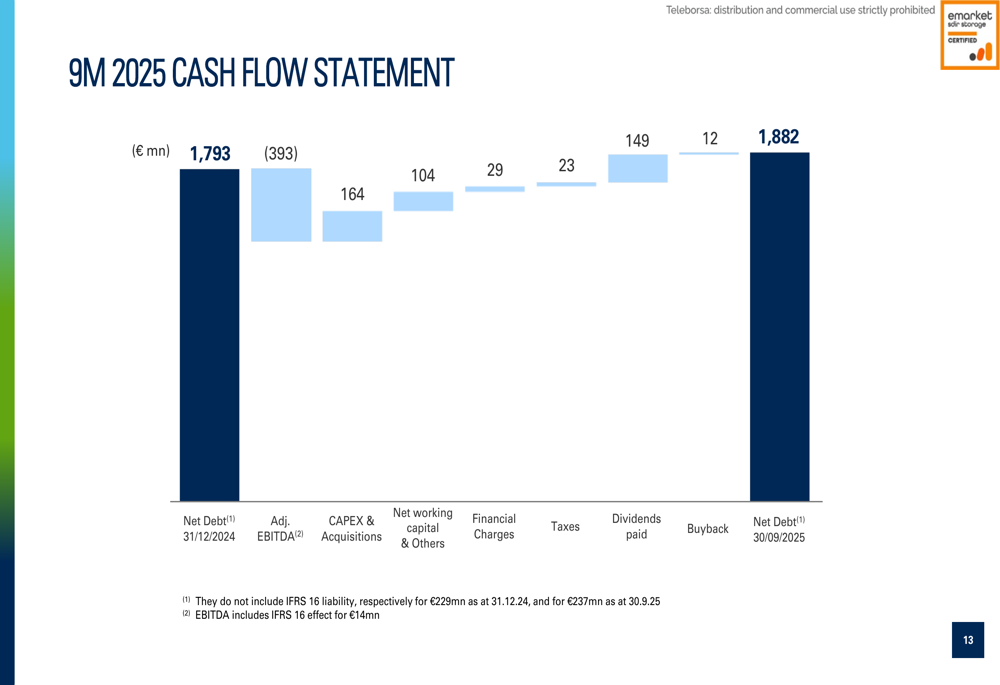

The company's financial position showed a slight increase in net debt, which rose to €1,882 million as of September 30, 2025, compared to €1,793 million at the end of 2024. This increase was primarily due to dividend payments of €149 million and share buybacks of €12 million, partially offset by strong operational cash flow.

The cash flow statement provides a clear view of the factors affecting ERG's financial position:

Strategic Initiatives

ERG continues to execute its strategic plan with several notable developments in the third quarter. The company commissioned the Corlacky wind farm (47MW) in Northern Ireland in late July and completed its first electrochemical storage facility, a 12.5MW BESS plant in Vicari, Sicily.

The company is also securing future revenue streams through power purchase agreements (PPAs), having signed three 5-10 year PPAs with FS Group for a total of 1.2TWh of energy (185GWh annually). Additionally, ERG is participating in renewable energy auctions, with three projects totaling 148MW submitted to the FERX auction (results expected in December) and 12MW participating in a German auction.

These strategic initiatives demonstrate ERG's commitment to growth and diversification:

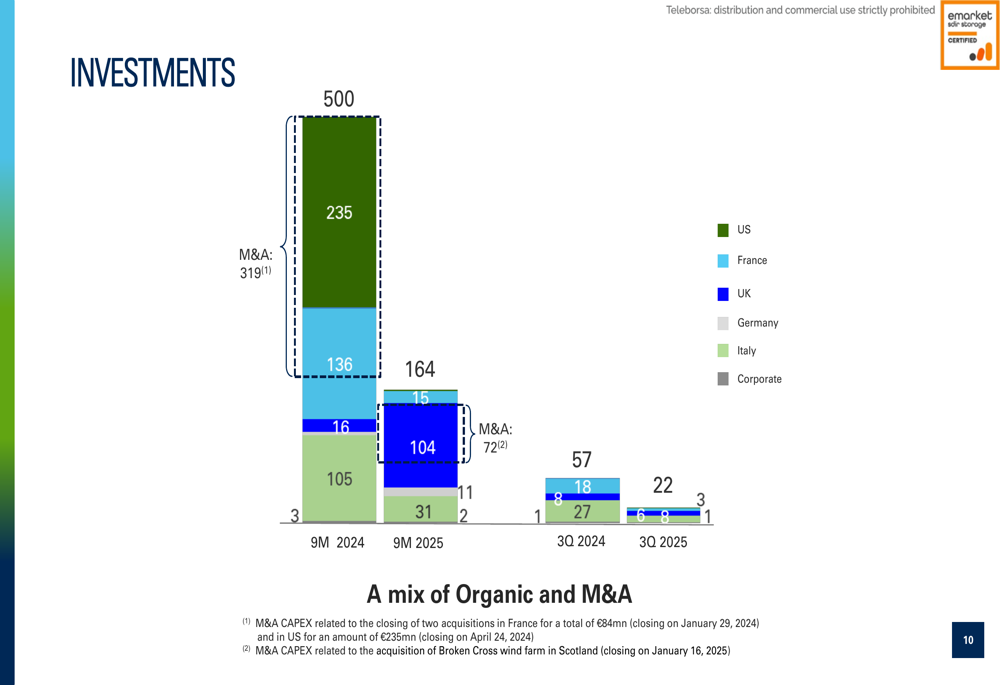

Investment activity has moderated compared to the previous year, with CAPEX of €22 million in Q3 2025 versus €31 million in Q3 2024. For the nine-month period, total investments including M&A reached €164 million, significantly lower than the €392 million spent in the same period of 2024.

The investment breakdown shows a strategic shift in capital allocation:

Forward-Looking Statements

ERG confirmed its 2025 guidance, projecting full-year EBITDA between €540-600 million, CAPEX of €190-240 million, and an adjusted net financial position of €1,850-1,950 million. The company's nine-month results suggest it is on track to meet these targets.

During the earnings call, CEO Paolo Merli emphasized the company's strategic focus, stating, "We are consistently on track, both with our strategy to grow the asset portfolio, but also with our strategy on the road to market to secure revenues through CFDs and PPAs." He highlighted the growth in the PPA portfolio, noting, "In 2021, we had zero PPA in our portfolio. Now we have 3.7 terawatt-hour per year of production covered by PPA with high-level off-takers across the world."

The company's guidance compared to current performance is illustrated in this chart:

Looking ahead, ERG anticipates improved wind conditions in December, which could positively impact fourth-quarter results. The company plans to increase its volume hedging to 80-85% by year-end, providing greater revenue stability in an uncertain market environment.

Despite the positive operational performance and confirmed guidance, investors will be watching closely to see if ERG can maintain its momentum in the face of industry challenges including potential supply chain issues, market saturation in the renewable energy sector, and fluctuations in turbine pricing that could affect project economics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.