Gold prices edge up amid Fed rate cut hopes; US-Russia talks awaited

Introduction & Market Context

Telefonaktiebolaget LM Ericsson (NASDAQ:ERIC) released its second quarter 2025 results on July 15, showing modest organic sales growth of 2% year-over-year, with significant margin improvements across all business segments. The Swedish telecommunications equipment manufacturer continues to navigate a challenging global market with varying regional performance, while making progress on its strategic initiatives focused on network monetization and AI innovation.

The company’s shares closed at $8.04 on July 14, 2025, and were trading slightly lower in after-hours trading, down 0.25% to $8.02. Ericsson (BS:ERICAs)’s stock has been trading near its 52-week high of $8.99, showing resilience despite ongoing market uncertainties.

Quarterly Performance Highlights

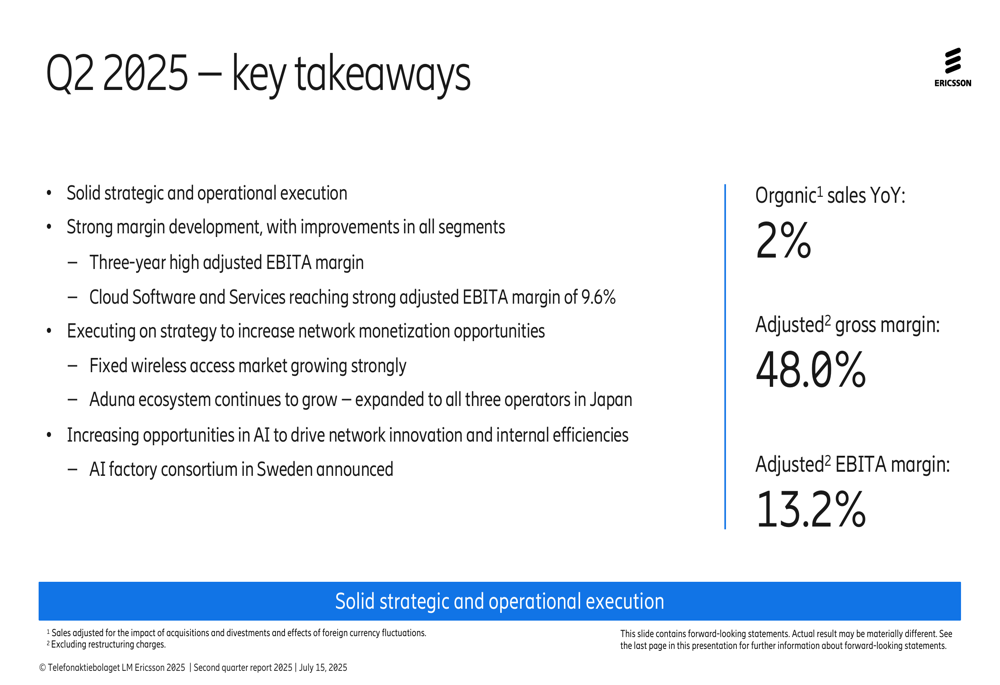

Ericsson reported solid operational execution in Q2 2025, achieving a three-year high adjusted EBITA margin of 13.2%, up from 9.5% in the same period last year. The company highlighted strong margin development across all segments, with Cloud Software (ETR:SOWGn) and Services reaching an impressive 9.6% adjusted EBITA margin.

As shown in the following key takeaways slide from the presentation:

Total (EPA:TTEF) net sales reached SEK 56.1 billion, with organic sales growth of 2% year-over-year. The adjusted gross margin improved significantly to 48.0%, while free cash flow before M&A stood at SEK 2.6 billion. The company also reported increased IPR revenues of SEK 4.9 billion, which contributed positively to the margin improvements.

Regional Performance

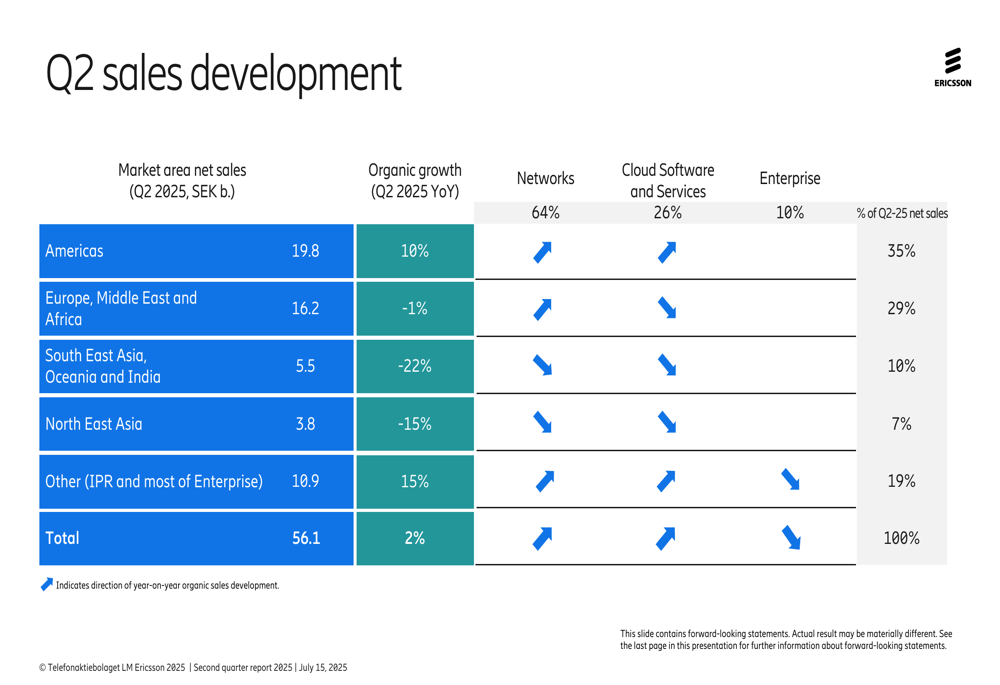

Ericsson’s regional performance showed significant divergence, with the Americas leading growth while Asian markets experienced substantial declines. The Americas region, accounting for 35% of total sales, grew 10% organically year-over-year to SEK 19.8 billion.

The following regional breakdown illustrates these contrasting performances:

Europe, Middle East, and Africa, representing 29% of sales, saw a slight decline of 1% to SEK 16.2 billion. More concerning were the steep declines in South East Asia, Oceania, and India (-22% to SEK 5.5 billion) and North East Asia (-15% to SEK 3.8 billion). These regions now account for just 10% and 7% of total sales, respectively.

This regional pattern continues a trend observed in previous quarters. In Q3 2024, Ericsson had reported strong growth in North America while India faced a slowdown following the completion of major 5G rollouts.

Detailed Financial Analysis

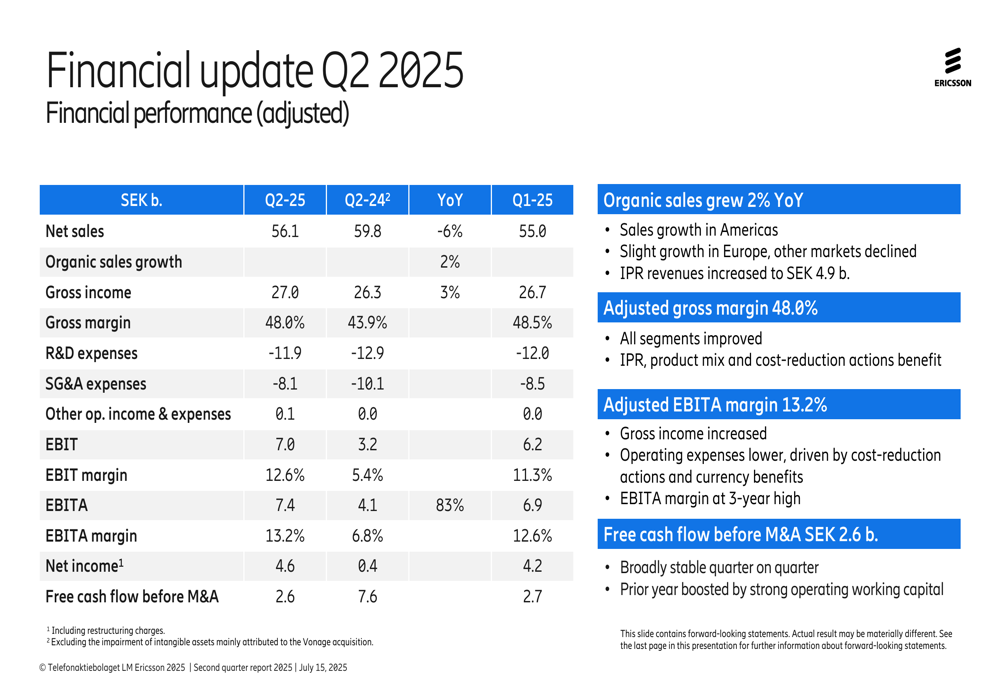

The company’s financial performance showed improvement across multiple metrics compared to the same period last year. The following financial update provides a comprehensive overview:

Net income reached SEK 4.6 billion, while R&D expenses stood at SEK 11.9 billion and SG&A expenses at SEK 8.1 billion. The presentation highlighted that organic sales growth was primarily driven by the Americas region and increased IPR revenues.

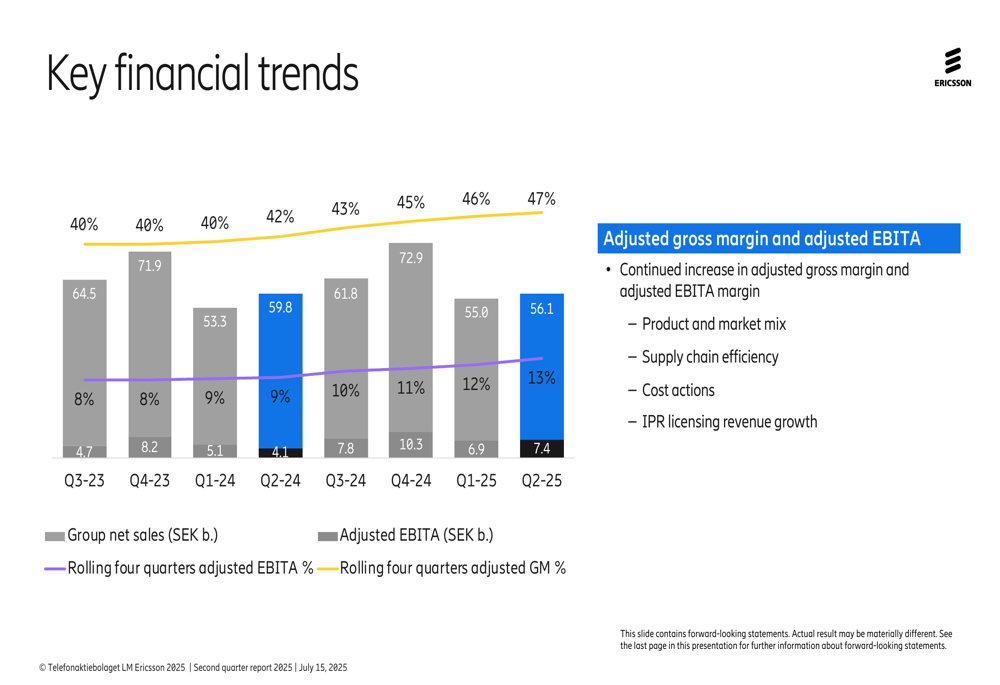

Looking at longer-term trends, Ericsson has maintained a trajectory of improving margins while stabilizing sales:

The company attributed the margin improvements to several factors, including favorable product and market mix, supply chain efficiency improvements, cost reduction actions, and growing IPR licensing revenue.

Segment Analysis

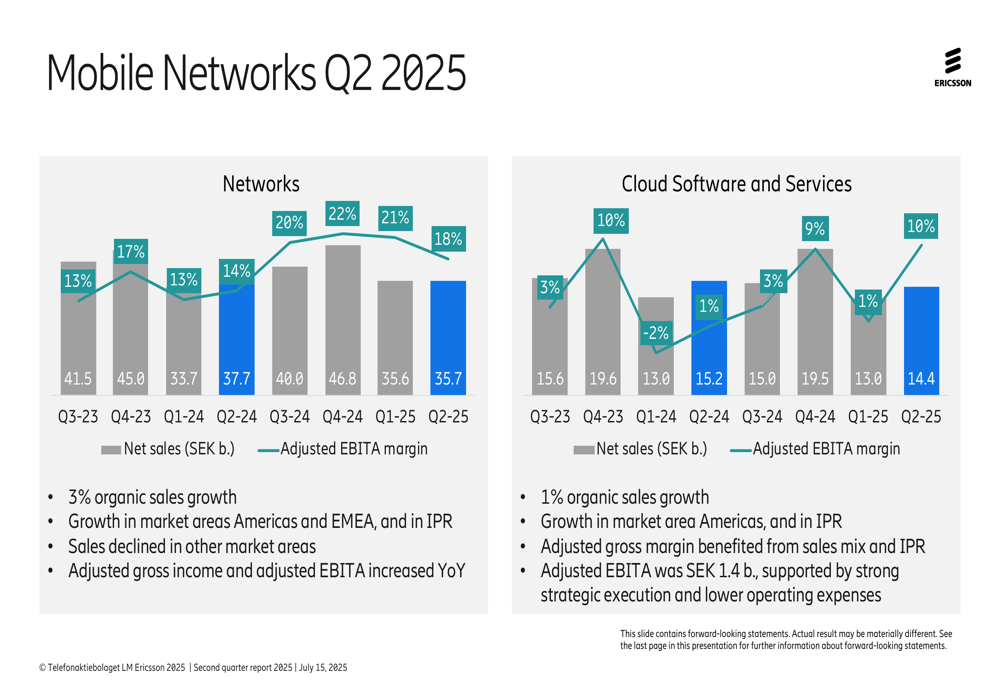

Ericsson’s business segments showed varying performance in Q2 2025. The Networks segment, which accounts for the largest portion of revenue, delivered 3% organic sales growth with an adjusted EBITA margin of 18%, as shown in the following chart:

The Cloud Software and Services segment achieved 1% organic sales growth with a significant improvement in adjusted EBITA margin to 10%. This represents substantial progress in the company’s efforts to improve profitability in this segment.

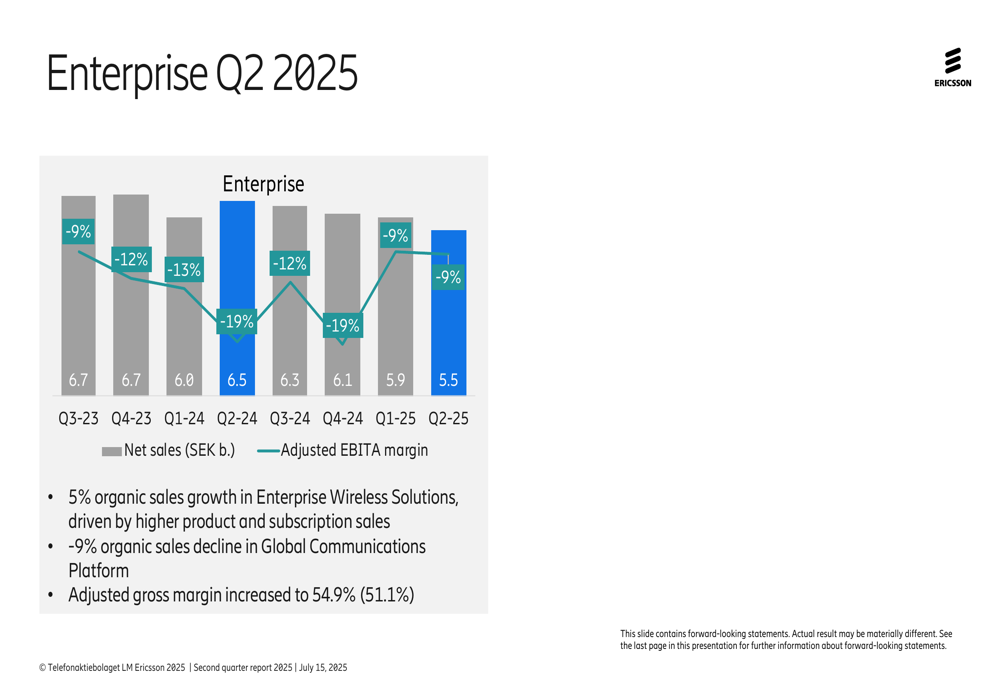

The Enterprise segment presented a more mixed picture:

While Enterprise Wireless Solutions grew 5% organically, driven by higher product and subscription sales, the Global Communications Platform experienced a 9% organic sales decline. The segment’s overall adjusted EBITA margin remained negative at -9%, though gross margin improved to 54.9%.

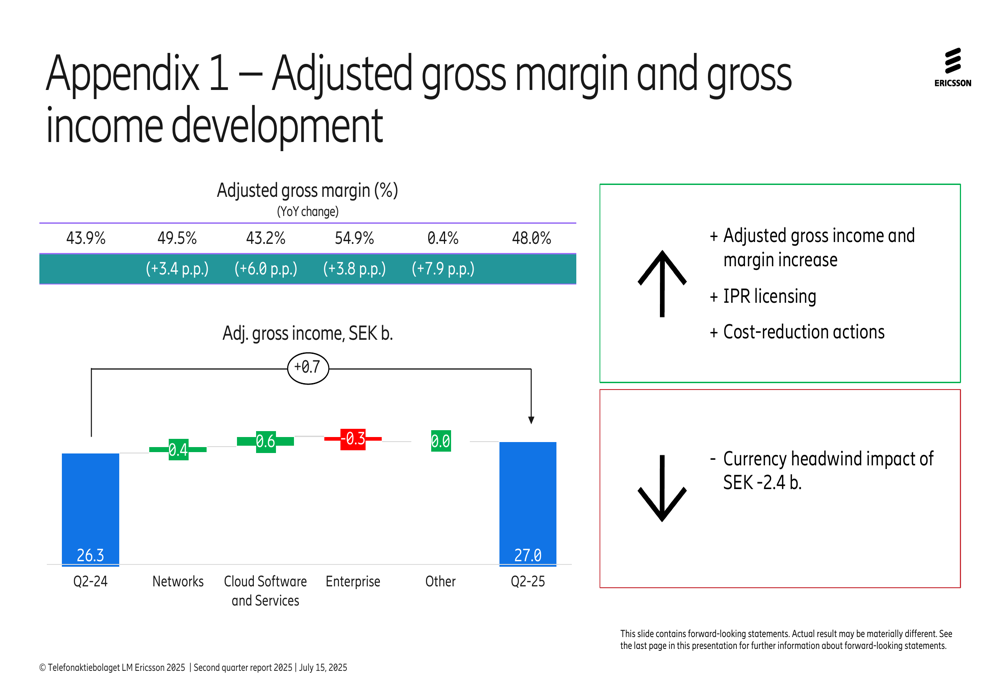

A detailed breakdown of the factors contributing to gross margin development shows the positive impact of IPR licensing and cost-reduction actions, partially offset by currency headwinds:

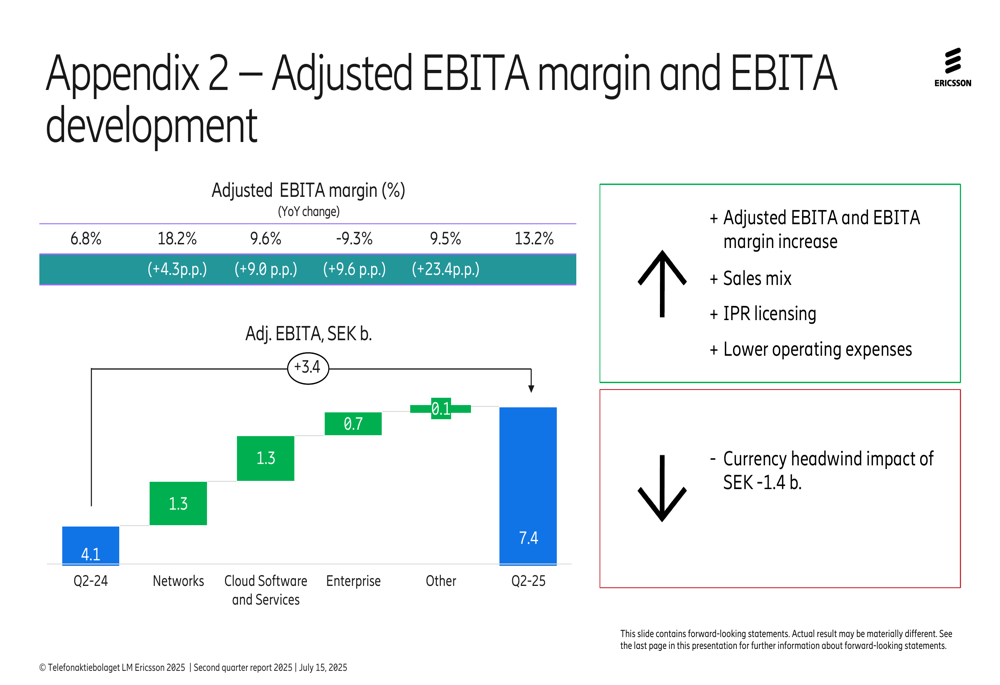

Similarly, the EBITA margin improvements were driven by favorable sales mix, IPR licensing, and lower operating expenses:

Strategic Initiatives & Outlook

Ericsson’s strategic focus remains on strengthening its competitive position through customer engagement for differentiated connectivity solutions. The company continues to invest in technology leadership while maintaining rigorous cost management.

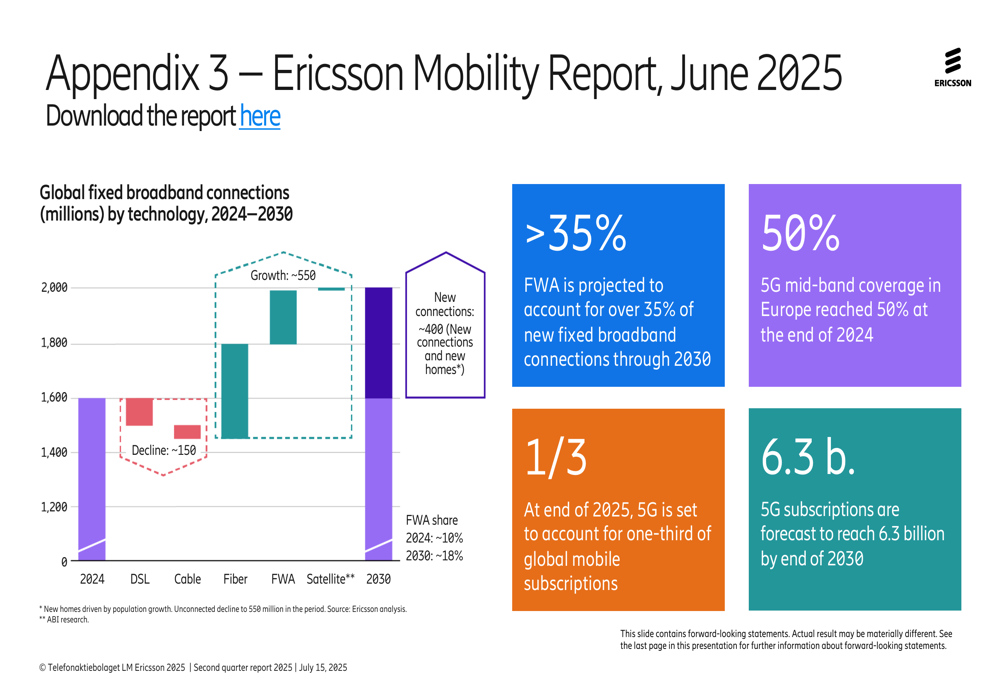

The Ericsson Mobility Report highlighted in the presentation projects significant growth opportunities, particularly in fixed wireless access (FWA), which is expected to account for over 35% of new fixed broadband connections through 2030. The company also noted that 5G mid-band coverage in Europe reached 50% at the end of 2024, with 5G subscriptions forecast to reach 6.3 billion by the end of 2030.

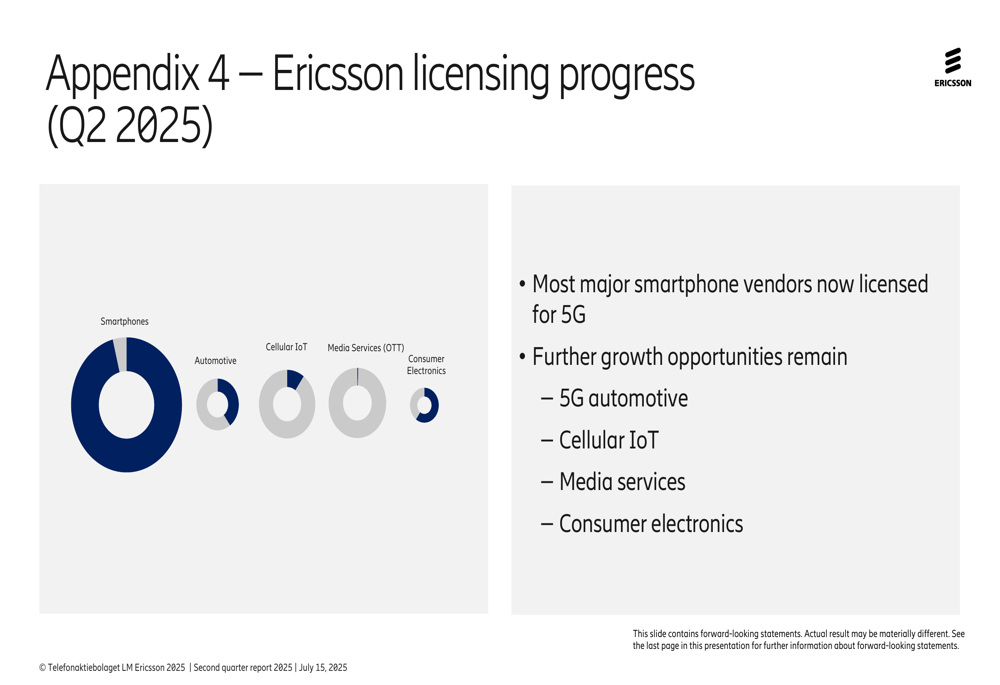

The company has made substantial progress in 5G licensing, with most major smartphone vendors now licensed. Ericsson identified further growth opportunities in 5G automotive, cellular IoT, media services, and consumer electronics:

Looking ahead, Ericsson noted increased uncertainty due to potential tariff changes and the broader macroeconomic environment. For Q3 2025, the company expects sales growth to be below the 3-year average seasonality for Networks and similar to the 3-year average seasonality for Cloud Software and Services. Adjusted gross margin in Q3 is projected to be in the range of 48% to 50%.

CEO Börje Ekholm summarized the outlook by stating that the company expects the RAN market to remain broadly stable, while Ericsson continues to focus on structurally improving the business through rigorous cost management and technology leadership investments.

The company’s ability to maintain organic growth while significantly improving margins demonstrates progress in its strategic transformation, though challenges remain in certain regions and business segments. Investors will be watching closely to see if Ericsson can sustain this momentum in the coming quarters amid ongoing market uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.