Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

Eris Lifesciences Ltd (NSE:ERIS) presented its Q1 FY26 results on August 5, 2025, highlighting significant profit growth despite modest revenue increases. The pharmaceutical company, which focuses on chronic disease segments in the Indian market, continues its strategic shift toward higher-margin business segments while reducing exposure to lower-margin operations.

The company’s stock closed at ₹1,803.10 on the presentation day, up 0.32% from the previous close. The shares have traded between ₹1,080 and ₹1,910 over the past 52 weeks, indicating strong performance relative to their trading range.

Quarterly Performance Highlights

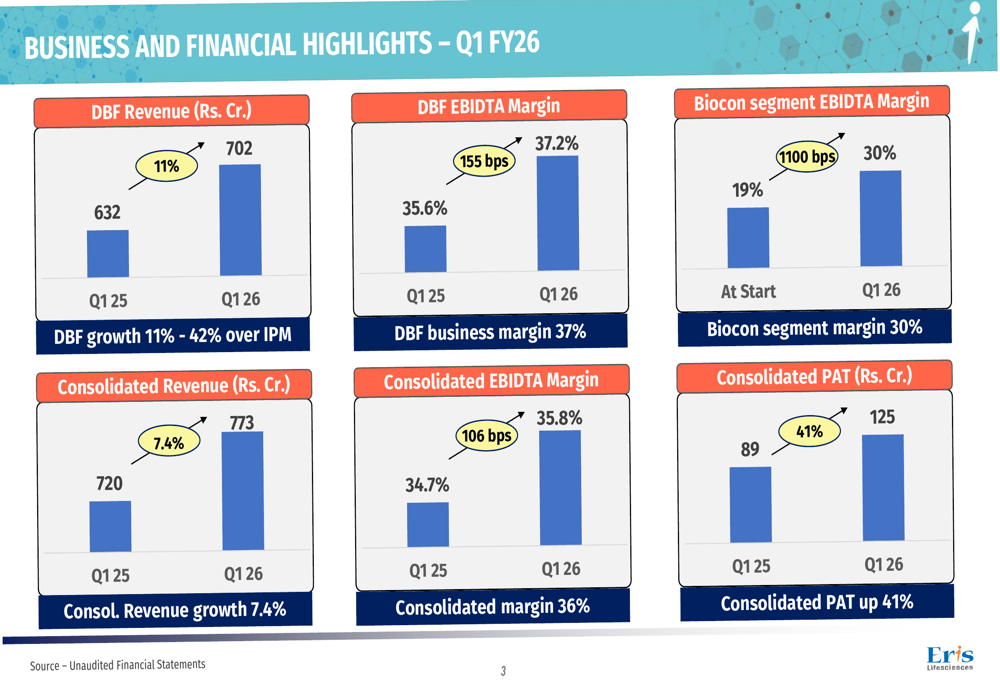

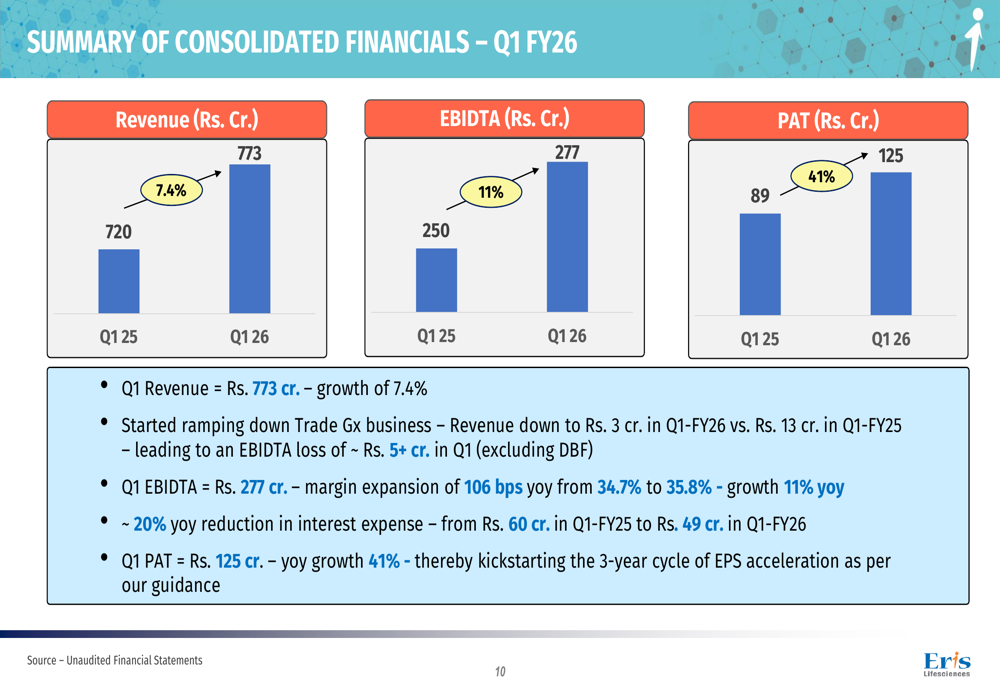

Eris Lifesciences reported consolidated revenue of ₹773 crore for Q1 FY26, representing a 7.4% year-over-year increase. More impressively, consolidated profit after tax (PAT) surged 41% to ₹125 crore, demonstrating the company’s ability to significantly improve bottom-line performance through operational efficiencies and strategic focus on higher-margin segments.

The company’s Domestic Branded Formulations (DBF) business, which forms the core of its operations, grew by 11% year-over-year to ₹702 crore, outperforming the Indian Pharmaceutical Market (IPM) by approximately 330 basis points. This growth came despite challenges from discontinued fixed-dose combinations and insulin shortages.

As shown in the following chart of quarterly financial performance:

The DBF segment’s EBITDA margin expanded by 155 basis points to 37.2%, even after adding over 300 medical representatives during the period. This margin expansion demonstrates the company’s ability to scale efficiently while maintaining profitability.

The Biocon business segment showed particularly strong margin improvement, reaching 30% in Q1 FY26 compared to 19% at the time of acquisition, representing an 1,100 basis point increase. This significant margin expansion reflects successful integration and operational improvements in the acquired business.

Strategic Initiatives

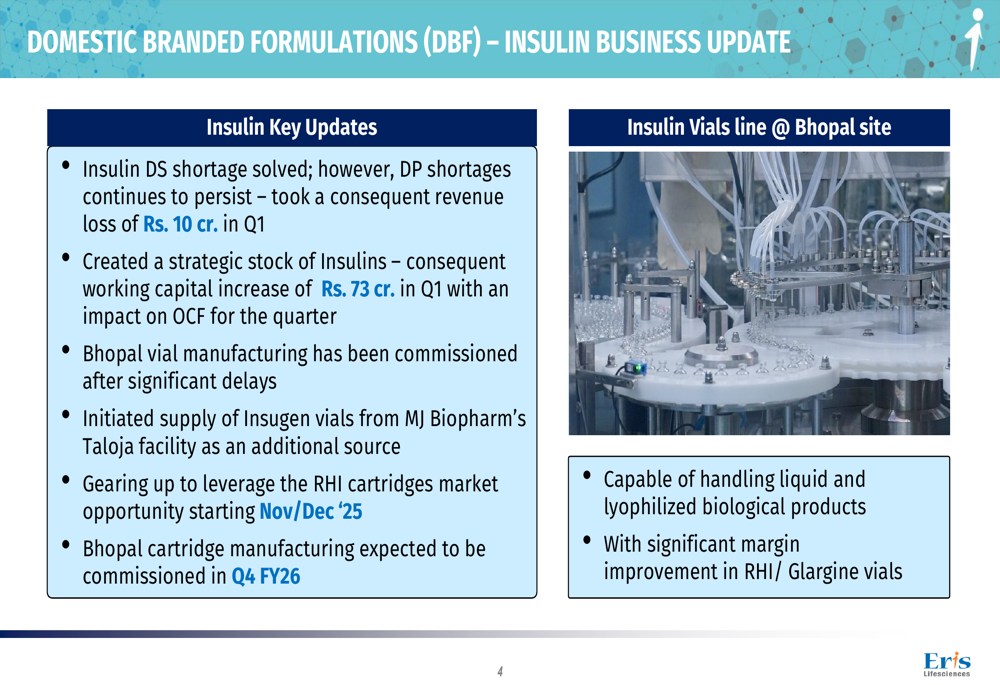

Eris Lifesciences is making significant progress on several strategic initiatives aimed at future growth. The company has commissioned insulin vial manufacturing at its Bhopal facility and expects insulin cartridge production to commence from Q4 FY26. This vertical integration is expected to improve margins and reduce dependency on external suppliers.

The company provided the following update on its insulin business:

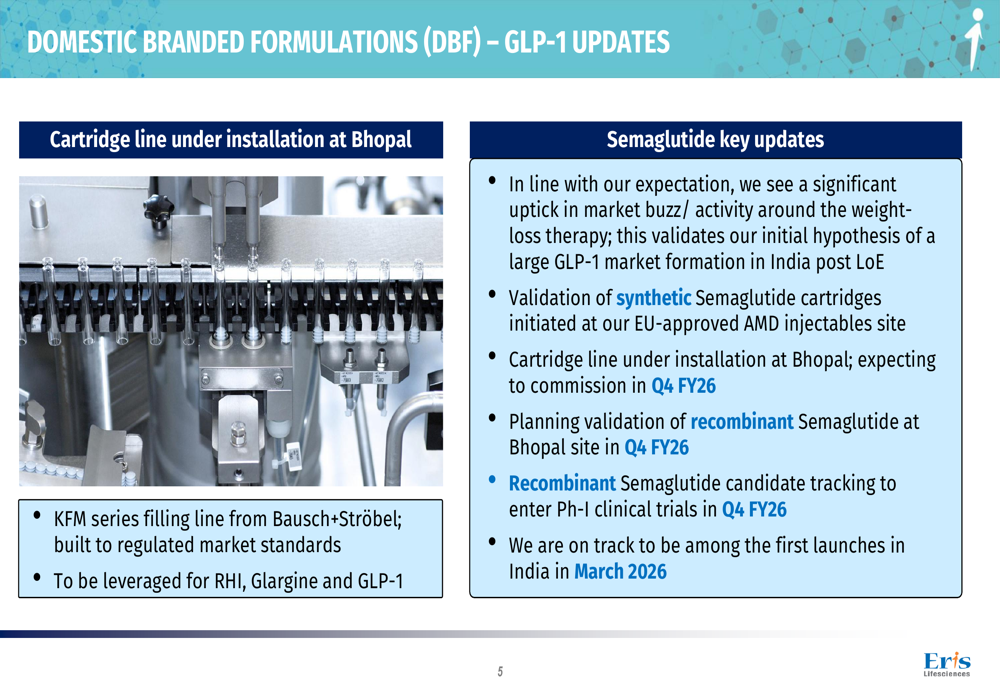

In the growing GLP-1 (glucagon-like peptide-1) segment, which has seen significant global interest for weight management and diabetes treatment, Eris is positioning itself to be among the first to launch in India by March 2026. The company has initiated validation of synthetic Semaglutide cartridges at its EU-approved AMD injectables site and is installing a cartridge line at the Bhopal facility.

The GLP-1 strategy is outlined in this slide:

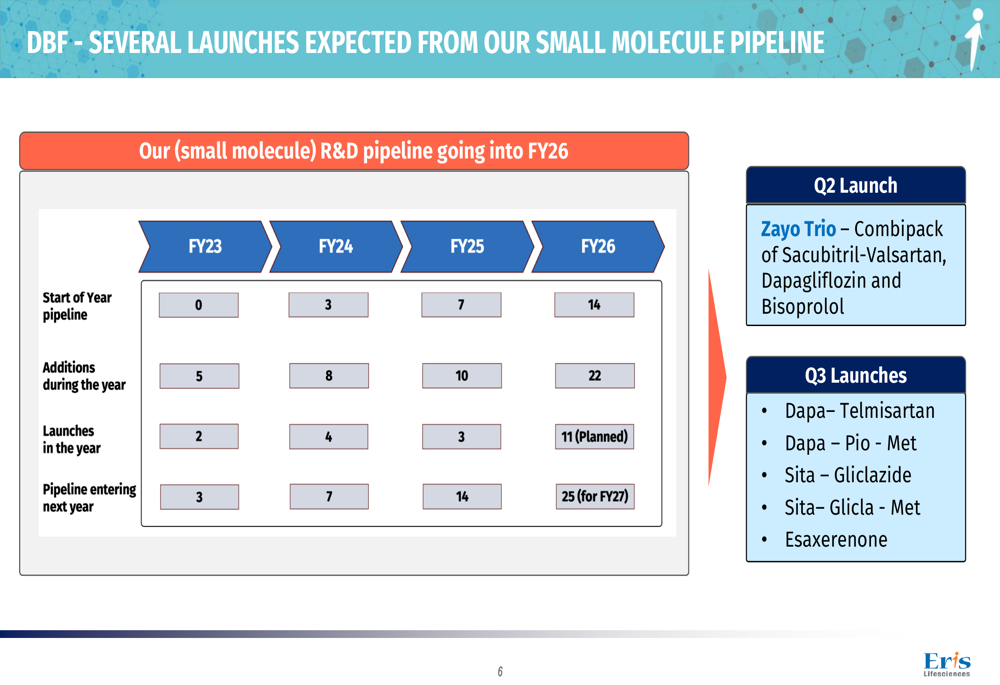

The company is also expanding its R&D pipeline, with 14 products at the start of FY26 and plans to add 22 more during the year. This represents a significant increase from previous years and demonstrates the company’s commitment to organic growth through new product development.

In its international business, Eris is pivoting toward higher-value European markets through a Contract Development and Manufacturing Organization (CDMO) model. The company has secured contracts worth over ₹100 crore in annual revenue, which are expected to contribute to growth starting from FY27.

Financial Analysis

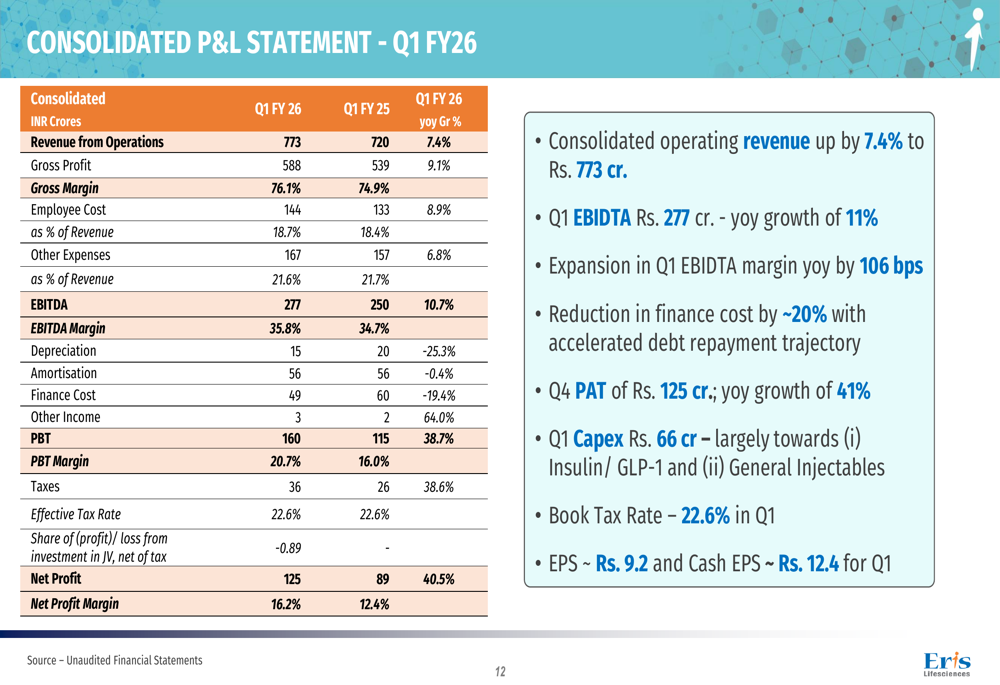

The consolidated financial performance shows strong improvement across key metrics, with EBITDA growing 11% year-over-year to ₹277 crore and margins expanding by 106 basis points to 35.8%. The company has also reduced its interest expense by approximately 20% year-over-year, from ₹60 crore in Q1 FY25 to ₹49 crore in Q1 FY26, reflecting its accelerated debt repayment strategy.

The detailed financial results are presented in the following consolidated summary:

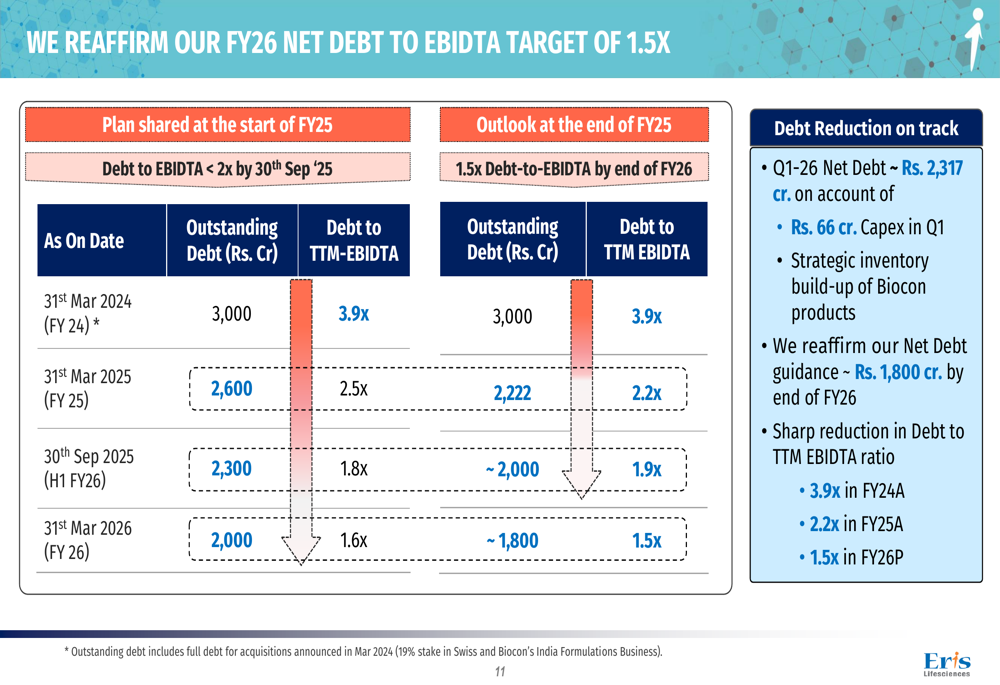

Eris continues to make progress on its debt reduction targets. The company’s net debt stood at approximately ₹2,317 crore in Q1 FY26, with a strategic inventory build-up of Biocon products affecting the quarter’s figures. The company reaffirmed its guidance of reducing net debt to approximately ₹1,800 crore by the end of FY26, which would bring the Debt to TTM EBITDA ratio down to 1.5x from 3.9x in FY24.

The full consolidated profit and loss statement provides additional detail on the company’s financial performance:

Forward-Looking Statements

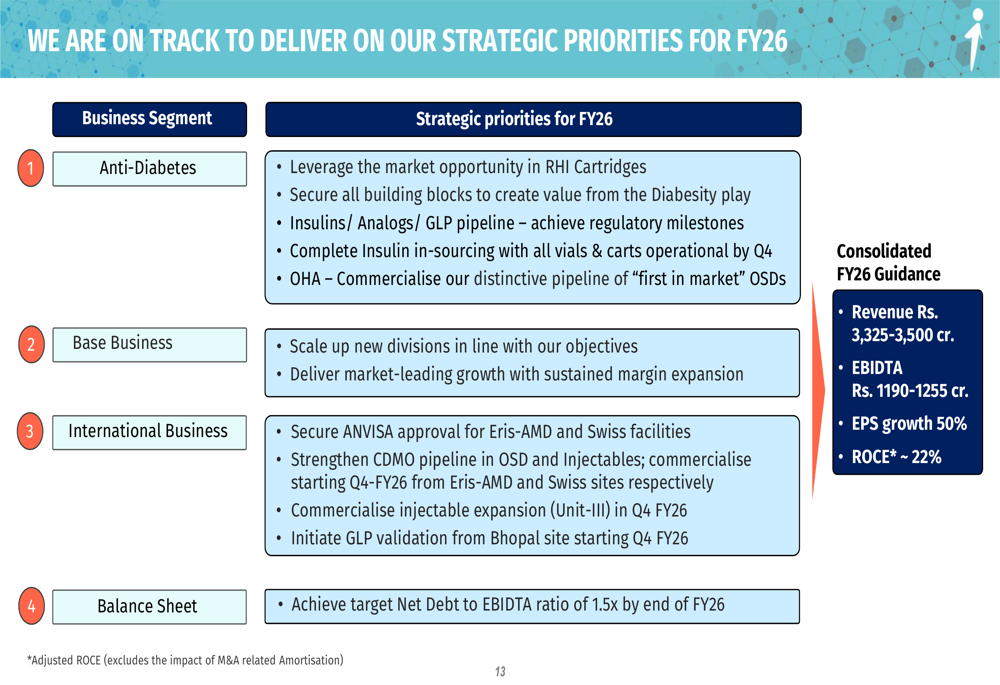

Eris Lifesciences has outlined clear strategic priorities for FY26 across its business segments. In the anti-diabetes segment, the company plans to leverage market opportunities in insulin cartridges and develop its pipeline for insulins, analogs, and GLP-1 products. For its base business, the focus remains on scaling up new divisions while delivering market-leading growth with sustained margin expansion.

The company provided the following strategic roadmap:

For FY26, Eris has provided consolidated guidance of ₹3,325-3,500 crore in revenue, ₹1,190-1,255 crore in EBITDA, 50% EPS growth, and a return on capital employed of approximately 22%. These targets reflect management’s confidence in continuing the strong performance demonstrated in Q1 FY26.

The company’s focus on high-margin segments, debt reduction, and strategic investments in future growth drivers positions it well for sustained profitability improvement, even as it navigates challenges in certain product categories and markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.