Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

Esperion Therapeutics Inc (NASDAQ:ESPR) presented its Q1 2025 earnings results on May 6, highlighting significant growth in U.S. product sales despite a headline revenue decline affected by a one-time payment in the prior year. The company’s stock closed at $1.05 on May 5, down 3.67% ahead of the earnings presentation, reflecting ongoing market skepticism despite the company’s positive operational metrics.

The presentation emphasized Esperion’s three-pillar strategic approach focused on global expansion of its bempedoic acid franchise, achieving sustainable operating profitability, and advancing its product pipeline beyond its current cardiovascular offerings.

Quarterly Performance Highlights

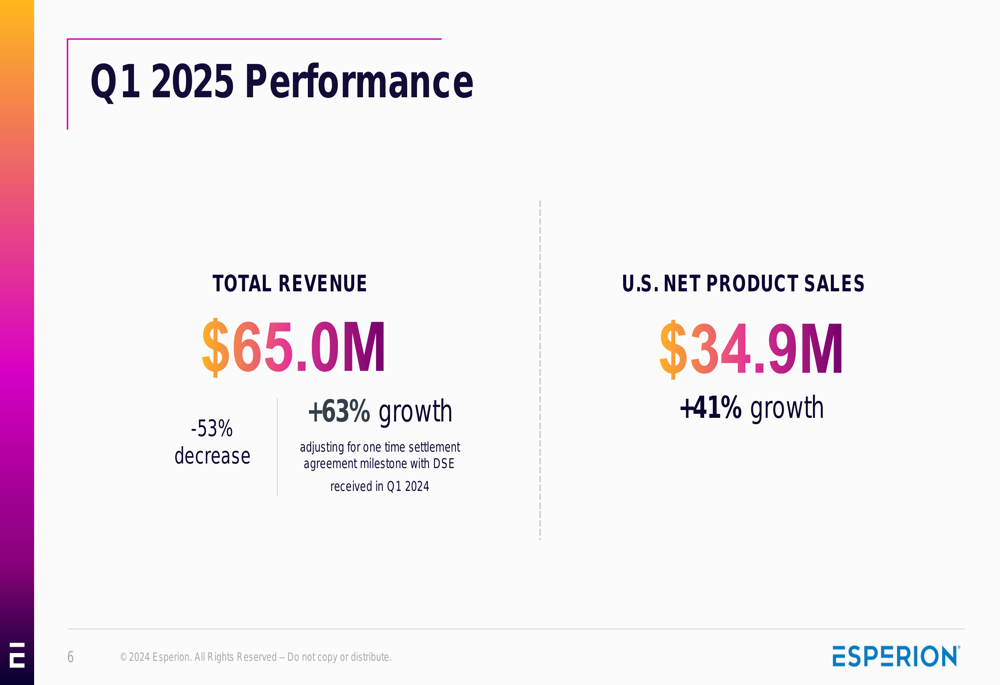

Esperion reported total revenue of $65.0 million for Q1 2025, representing a 53% year-over-year decrease. However, when adjusted for a one-time settlement agreement milestone with DSE received in Q1 2024, revenue actually grew by 63%.

U.S. net product sales showed particularly strong performance, reaching $34.9 million, a 41% increase compared to the same period last year. Meanwhile, collaboration revenue totaled $30.1 million, down 73% year-over-year but up 97% when adjusted for the one-time settlement payment.

As shown in the following financial performance summary:

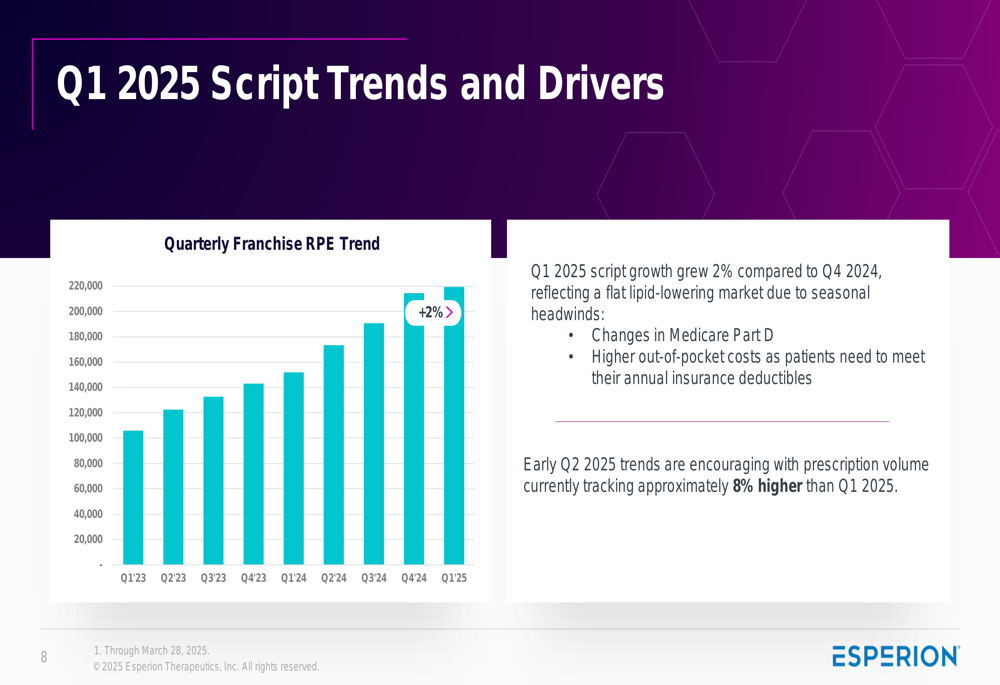

Prescription trends showed modest but steady growth, with Q1 2025 scripts increasing 2% compared to Q4 2024. More encouragingly, early Q2 2025 data indicates prescription volume is tracking approximately 8% higher than Q1 2025, suggesting potential acceleration in the current quarter.

Market Access and Clinical Validation

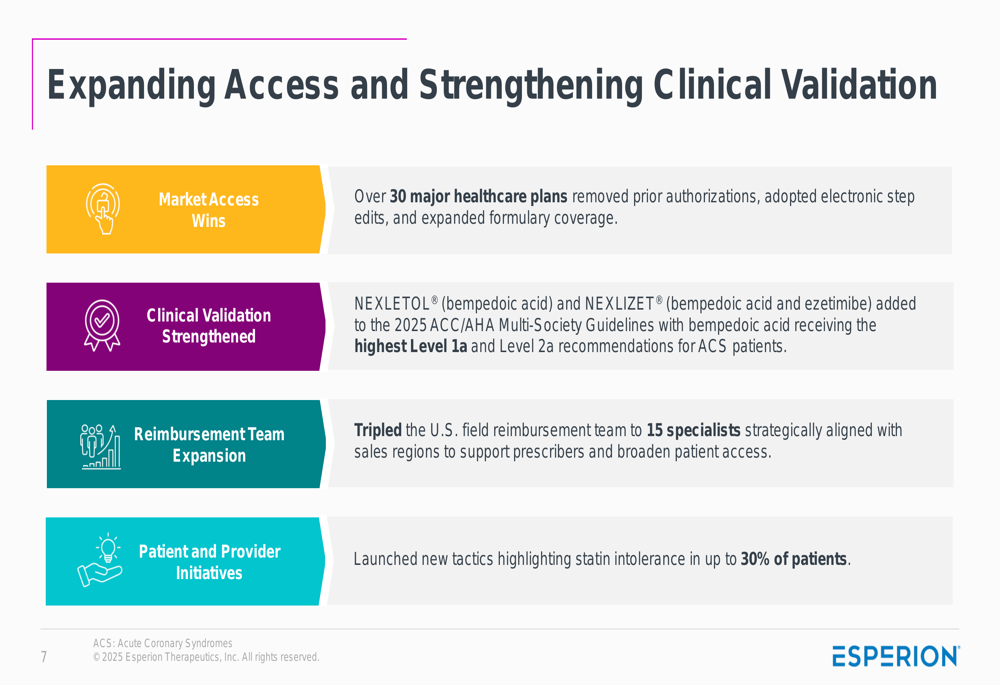

The company highlighted significant progress in expanding market access and strengthening clinical validation for its products. Over 30 major healthcare plans removed prior authorizations, adopted electronic step edits, and expanded formulary coverage during the quarter.

A major milestone was the inclusion of NEXLETOL® (bempedoic acid) and NEXLIZET® (bempedoic acid and ezetimibe) in the 2025 ACC/AHA Multi-Society Guidelines, with bempedoic acid receiving the highest Level 1a and Level 2a recommendations for acute coronary syndrome patients.

To capitalize on these developments, Esperion tripled its U.S. field reimbursement team to 15 specialists strategically aligned with sales regions to support prescribers and broaden patient access.

As detailed in the following slide:

Strategic Initiatives

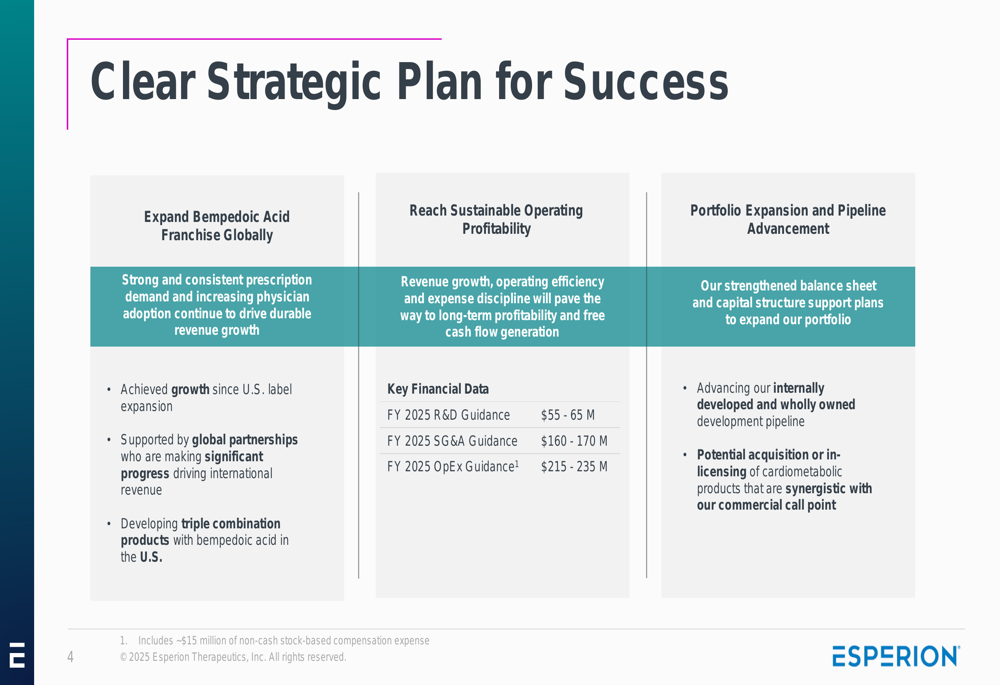

Esperion outlined its comprehensive strategic plan centered around three key pillars: expanding its bempedoic acid franchise globally, achieving sustainable operating profitability, and advancing its product pipeline.

The company provided financial guidance for fiscal year 2025, projecting R&D expenses of $55-65 million and SG&A expenses of $160-170 million, resulting in total operating expenses of $215-235 million, including approximately $15 million in non-cash stock-based compensation.

On the international front, Esperion continues to expand its global reach through strategic partnerships across Europe, Japan, Asia, South America, Israel, Australia, New Zealand, and Canada. The company’s products have now been approved in 40 countries, with approximately 472,500 patients treated through February 2025.

Pipeline Development

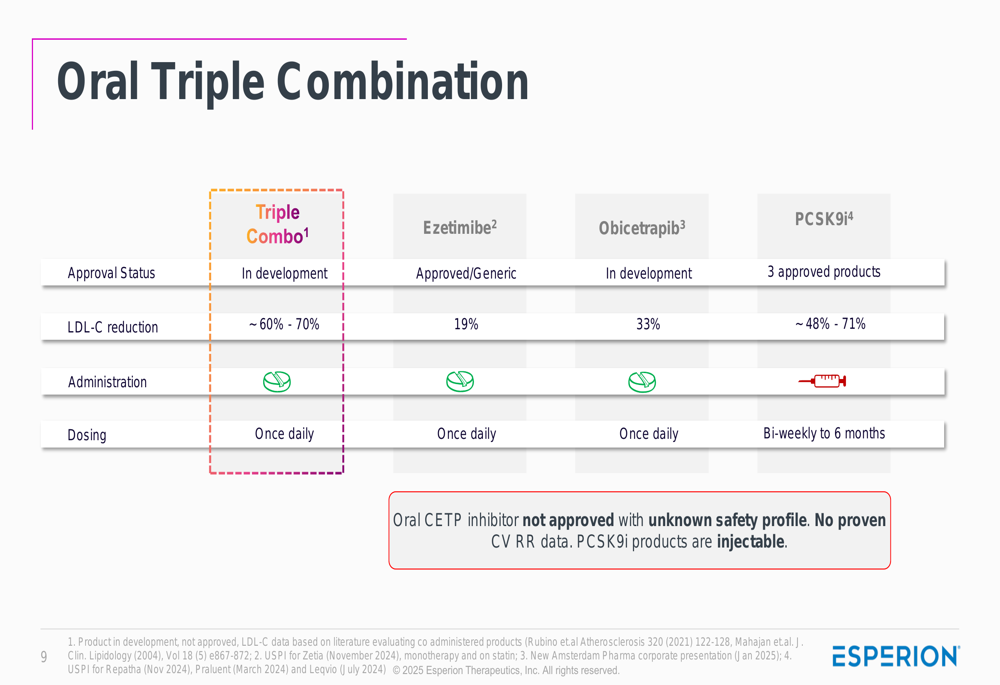

A significant focus of the presentation was Esperion’s pipeline expansion beyond its current cardiovascular products. The company is developing two triple combination therapies (bempedoic acid, ezetimibe, and either atorvastatin or rosuvastatin) targeting New Drug Application submissions in 2027. These combinations aim to achieve 60-70% LDL-C reduction with once-daily oral dosing.

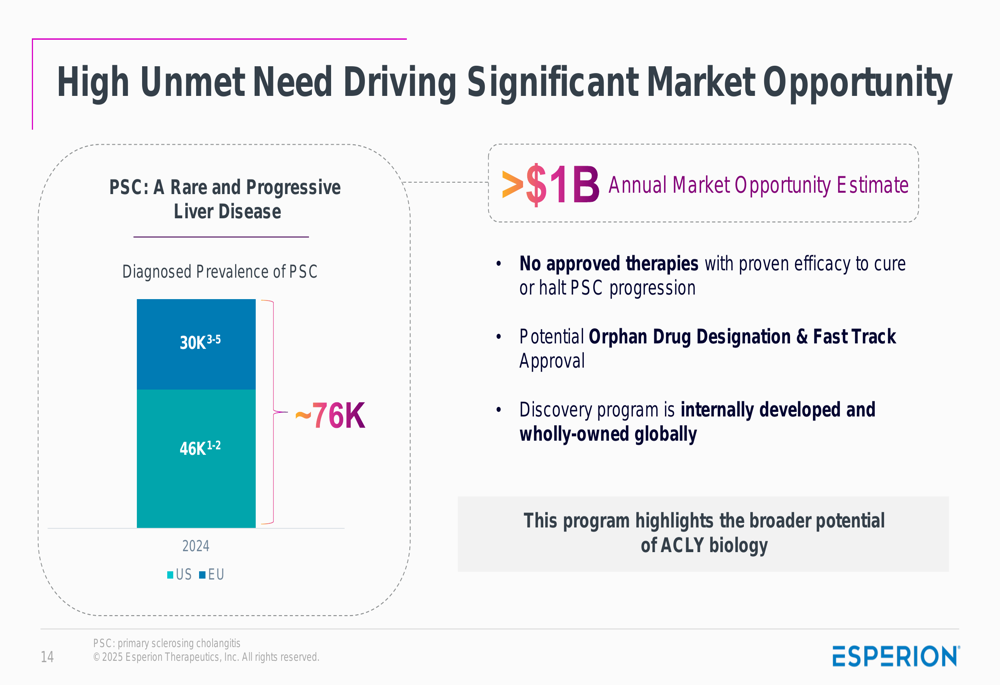

Esperion is also expanding into new therapeutic areas, particularly Primary Sclerosing Cholangitis (PSC), a rare and progressive liver disease with high unmet medical needs. The company estimates a diagnosed prevalence of approximately 76,000 patients in the U.S. and EU combined, representing a potential annual market opportunity exceeding $1 billion. Esperion plans to file an Investigational New Drug application for its PSC program in 2026.

Forward-Looking Statements

Looking ahead, Esperion aims to build on its market access wins and growing prescription trends. The company’s strategy focuses on leveraging its strengthened balance sheet to advance both internal pipeline development and potential acquisition or in-licensing of synergistic cardiometabolic products.

While the presentation highlighted positive operational metrics and strategic initiatives, investors should note the contrast between the company’s optimistic outlook and its current stock performance. Since reporting strong Q4 2024 results (which showed 114% year-over-year revenue growth), Esperion’s stock has declined from $1.63 to $1.05, suggesting ongoing market concerns about the company’s path to sustainable profitability despite its growth in U.S. product sales.

The company’s ability to accelerate prescription growth, successfully expand internationally, and advance its pipeline while managing operating expenses will be critical factors for investors to monitor in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.