Gold prices edge higher on raised Fed rate cut hopes

Introduction & Market Context

Esquire Financial Holdings Inc (NASDAQ:ESQ) presented its first quarter 2025 results on April 24, showcasing continued strong performance across its specialized banking verticals. The financial holding company for Esquire Bank has positioned itself as a branchless, tech-enabled institution focused on two distinct national markets: litigation financing and payment processing.

Trading near $83.05, Esquire’s stock has performed well within its 52-week range of $44.55 to $90.18, reflecting investor confidence in the company’s specialized business model and consistent growth trajectory.

Quarterly Performance Highlights

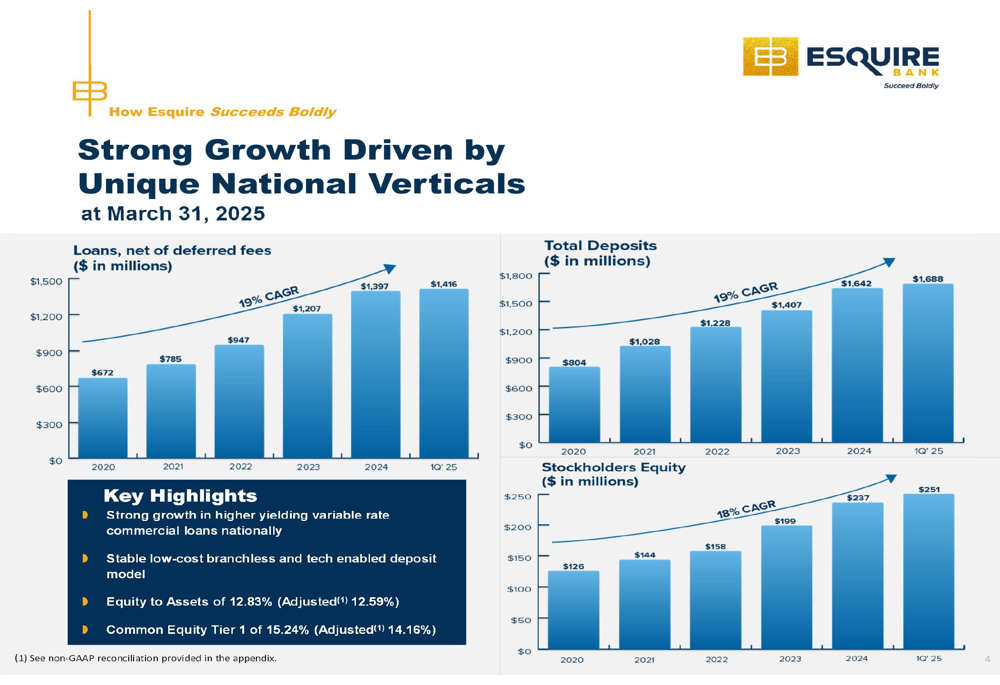

Esquire Financial reported impressive growth metrics for Q1 2025, maintaining its momentum with a 19% compound annual growth rate (CAGR) in both loans and deposits since 2020. The company’s dual-vertical strategy has yielded industry-leading profitability metrics, including a return on average assets (ROA) of 2.39% and return on tangible common equity (ROTCE) of 19.13%.

As shown in the following chart of the company’s growth trajectory:

Total (EPA:TTEF) loans reached $1.416 billion in Q1 2025, up from $672 million in 2020, while deposits grew to $1.688 billion from $804 million over the same period. Stockholders’ equity increased to $251 million, representing a 16% CAGR since 2020.

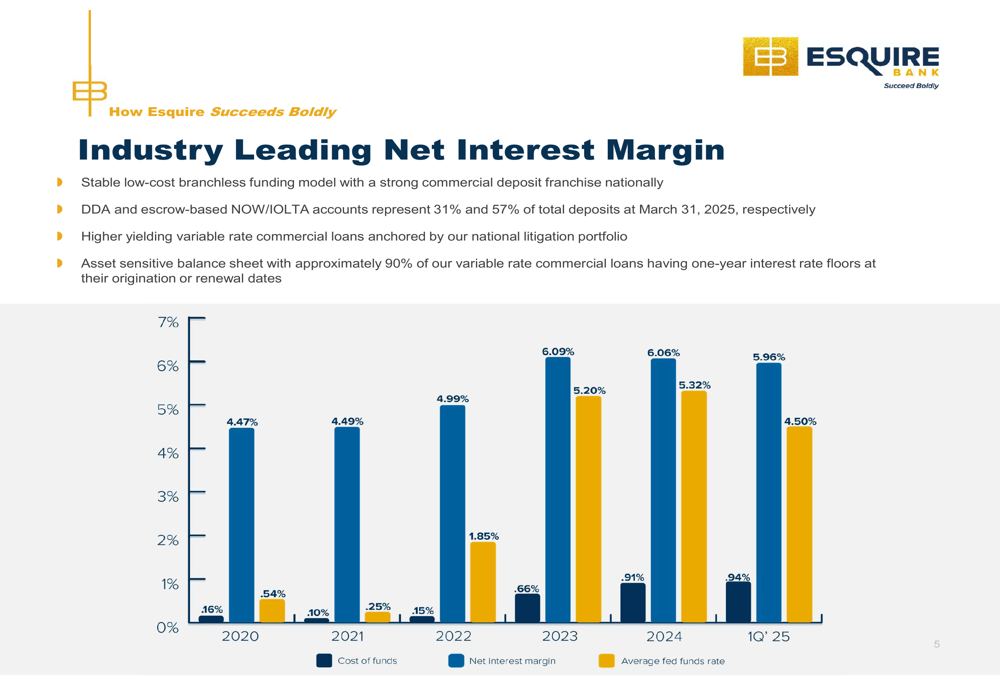

Perhaps most notably, Esquire maintained an industry-leading net interest margin (NIM) of 5.96% in Q1 2025, significantly outperforming industry averages. This exceptional margin is supported by the company’s asset-sensitive balance sheet and specialized lending model.

The following chart illustrates Esquire’s NIM performance relative to the federal funds rate:

Detailed Financial Analysis

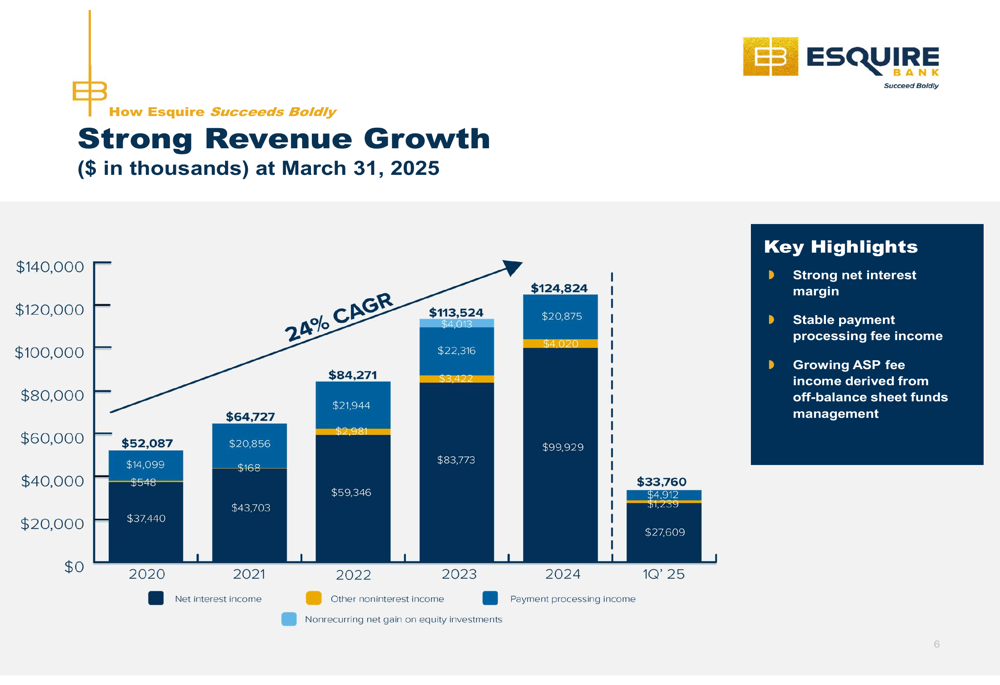

Esquire’s revenue growth has been equally impressive, with a 24% CAGR driven by both net interest income and fee-based revenue streams. The company’s payment processing vertical contributes approximately 18% of total revenue, providing important diversification.

The revenue composition and growth trend is visualized in this chart:

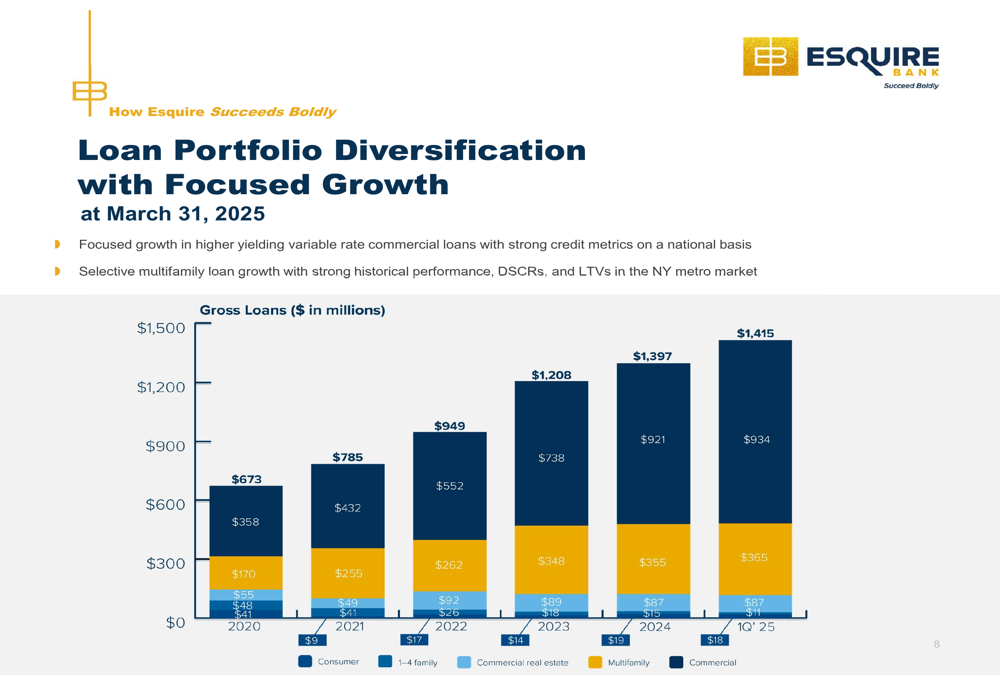

The loan portfolio remains heavily weighted toward commercial loans, particularly to law firms, which reached $934 million in Q1 2025. These loans typically yield approximately 9.45% and feature strong underwriting metrics, including personal guarantees and an average loan-to-collateral fee value of less than 13%.

The following chart shows Esquire’s loan portfolio diversification:

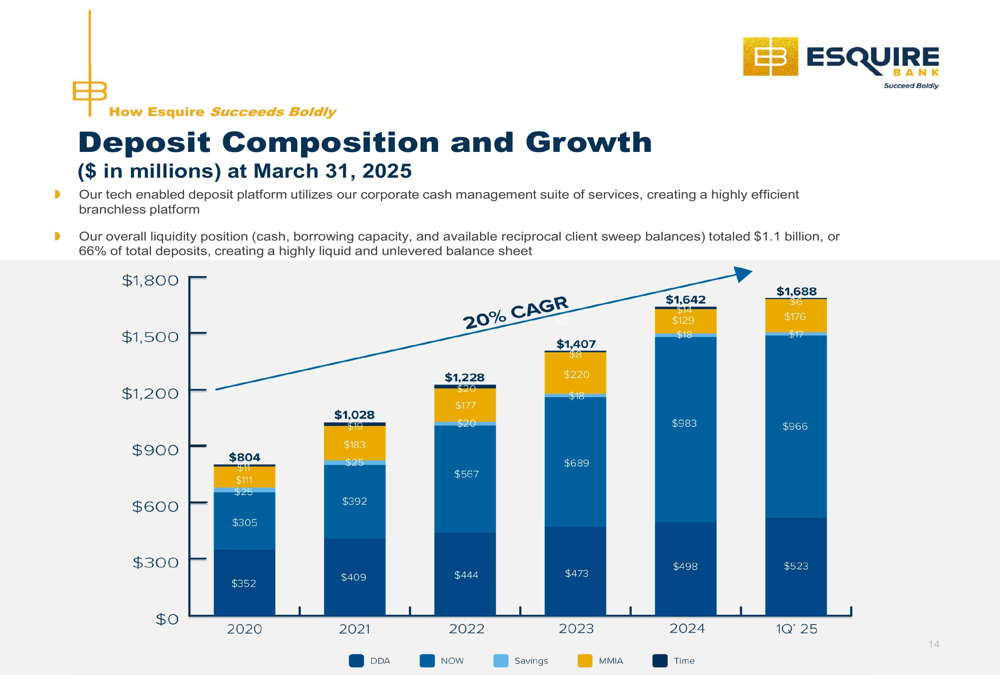

On the funding side, Esquire maintains a stable, low-cost deposit base with 88% of deposits in demand deposit accounts (DDA) and NOW accounts. Litigation and payment processing deposits represent 74% and 10% of total deposits, respectively, highlighting the company’s focus on its core verticals.

The deposit composition and growth are illustrated here:

Credit quality remains strong, with nonperforming loans at 0.57% of total loans and net charge-offs at 0.22% of average loans for Q1 2025. The allowance for credit losses stands at 1.37% of total loans, providing adequate coverage for potential losses.

Strategic Initiatives

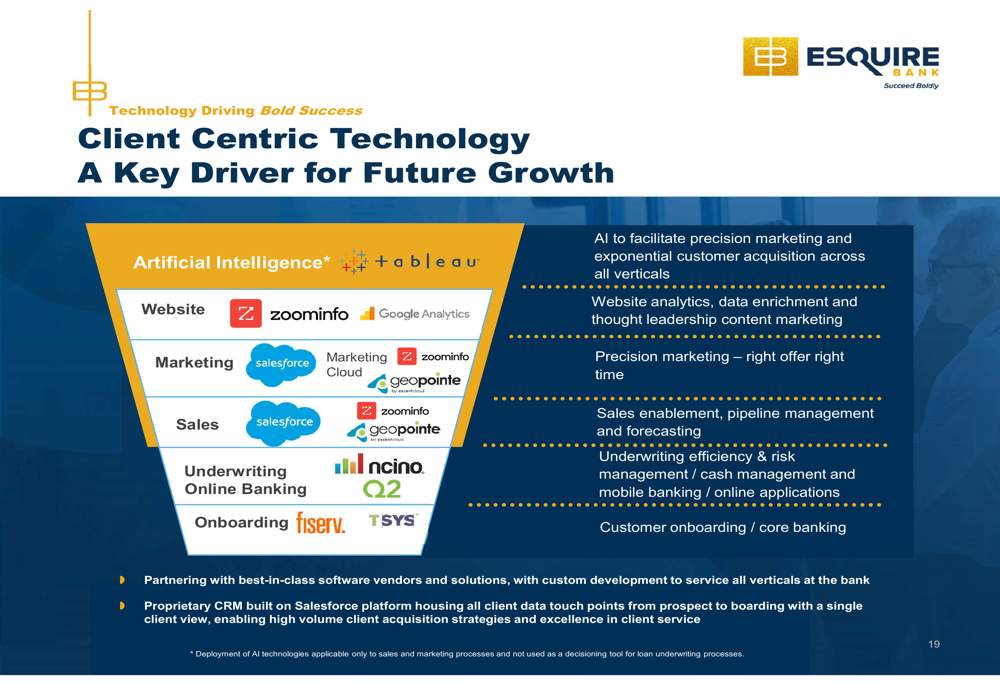

Esquire continues to leverage technology as a key differentiator in its specialized markets. The company is implementing AI-driven marketing strategies to facilitate precision targeting and customer acquisition in its niche verticals.

As shown in the following overview of Esquire’s technology partnerships:

The company’s proprietary CRM built on the Salesforce (NYSE:CRM) platform enables high-volume client acquisition and service excellence. By partnering with best-in-class software vendors, Esquire aims to maintain its competitive edge in delivering specialized financial services to its target markets.

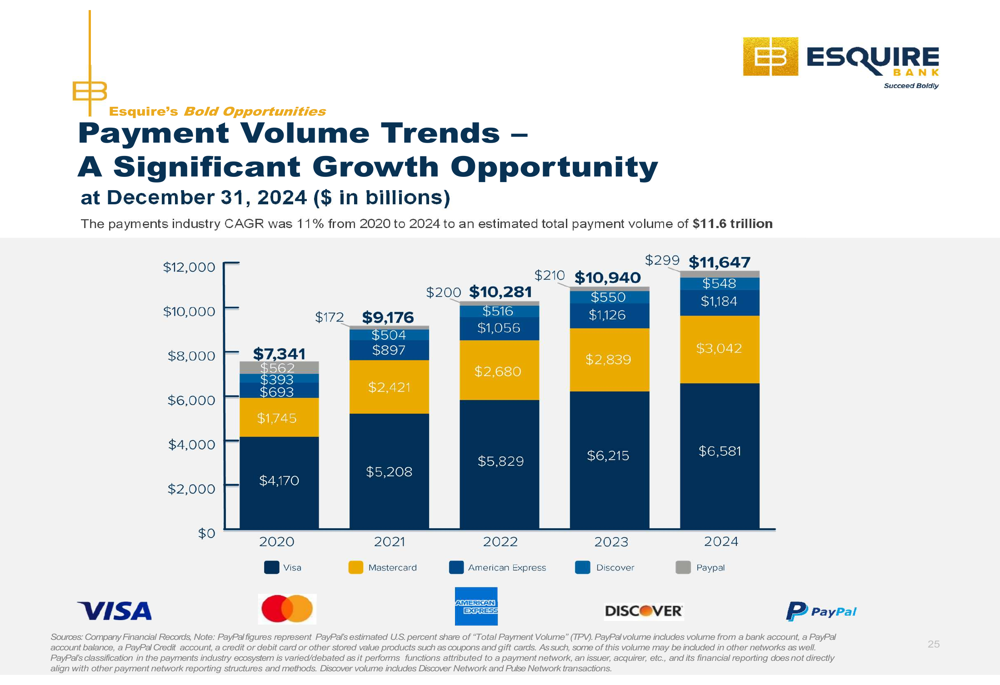

Esquire’s payment processing vertical continues to show stable growth, with the company now serving approximately 90,000 merchants nationwide. The payments industry overall has experienced an 11% CAGR from 2020 to 2024, reaching an estimated total payment volume of $11.6 trillion.

The payment volume trends are illustrated in this chart:

Forward-Looking Statements

Esquire Financial remains optimistic about its growth prospects, citing significant market opportunities in both its litigation and payment processing verticals. The U.S. litigation market is estimated at $443 billion annually (2.1% of U.S. GDP), while the payments industry continues to expand rapidly.

The company’s branchless model and specialized focus allow it to maintain superior efficiency metrics, with an efficiency ratio of 49.6%. With a strong capital position (equity to assets of 12.83% and Common Equity Tier 1 of 15.24%), Esquire is well-positioned to continue its growth trajectory while maintaining the flexibility to navigate changing economic conditions.

Book value per share reached $29.74 as of March 31, 2025, reflecting the company’s consistent profitability and disciplined capital management. Management remains focused on leveraging its technology platform and specialized expertise to continue capturing market share in its target verticals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.