US stock futures edge lower after S&P 500 hits record high; PCE data in focus

Introduction & Market Context

Esquire Financial Holdings (NASDAQ:ESQ) recently shared its Q2 2025 investor presentation, highlighting the company’s continued strong performance through its specialized focus on litigation and payment processing verticals. The Melville, NY-based financial holding company for Esquire Bank has maintained its growth trajectory while delivering industry-leading returns. The stock is currently trading at $102.51 in premarket trading, down 1.21% from the previous close of $103.77.

Esquire’s branchless, technology-enabled banking model has allowed it to capitalize on two substantial market opportunities: the $529 billion litigation market with over 100,000 law firms, and the $11.6 trillion payment processing market with more than 10 million merchants.

Executive Summary

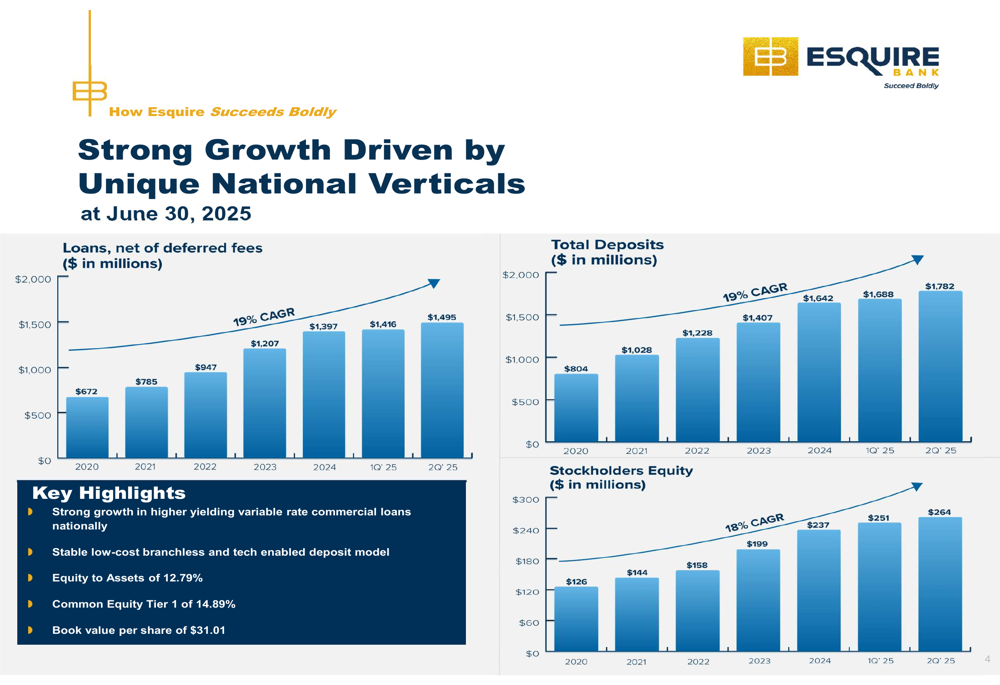

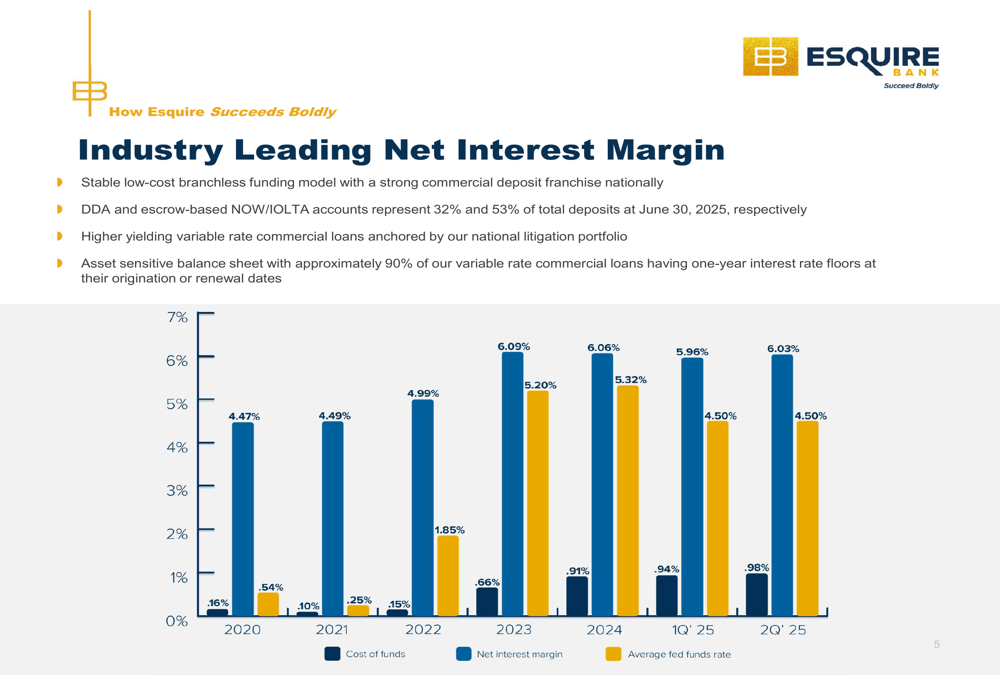

Esquire Financial has demonstrated consistent growth across all key metrics, with both loans and deposits achieving a 19% CAGR from 2020 through Q2 2025. The company’s focus on higher-yielding variable-rate commercial loans, particularly in the litigation sector, combined with its stable low-cost deposit base, has enabled it to maintain an industry-leading net interest margin of 6.03%.

As shown in the following chart of the company’s growth in loans, deposits, and stockholders’ equity:

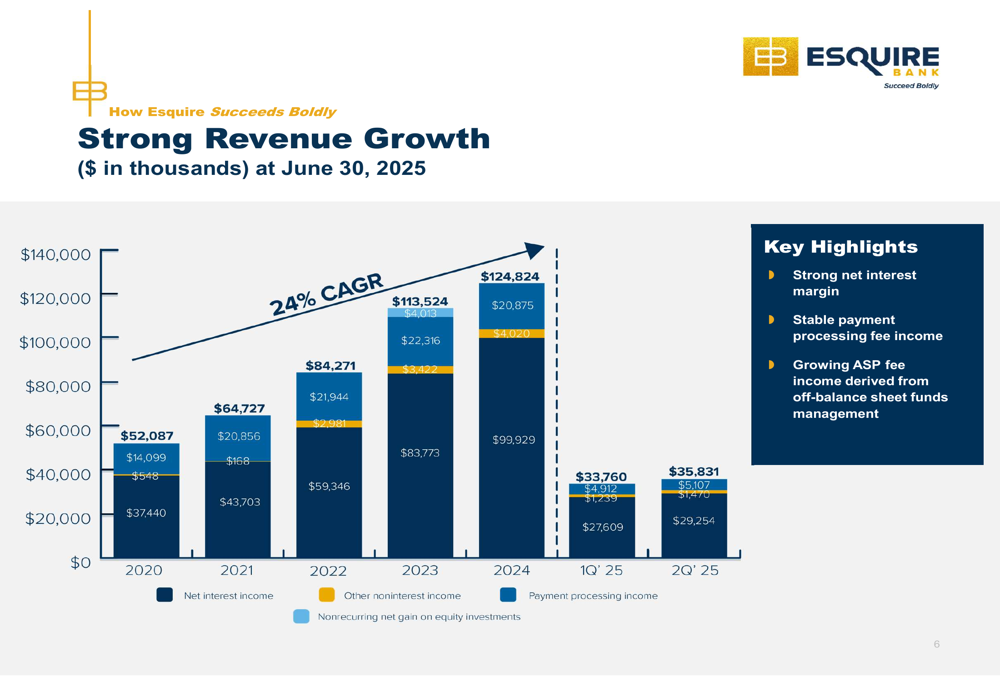

The company’s total revenues have increased at a 24% CAGR since 2020, reaching $124.8 million in Q2 2025. This growth has translated into impressive profitability metrics, with return on average assets of 2.37% and return on average stockholders’ equity of 18.74% in Q2 2025.

Quarterly Performance Highlights

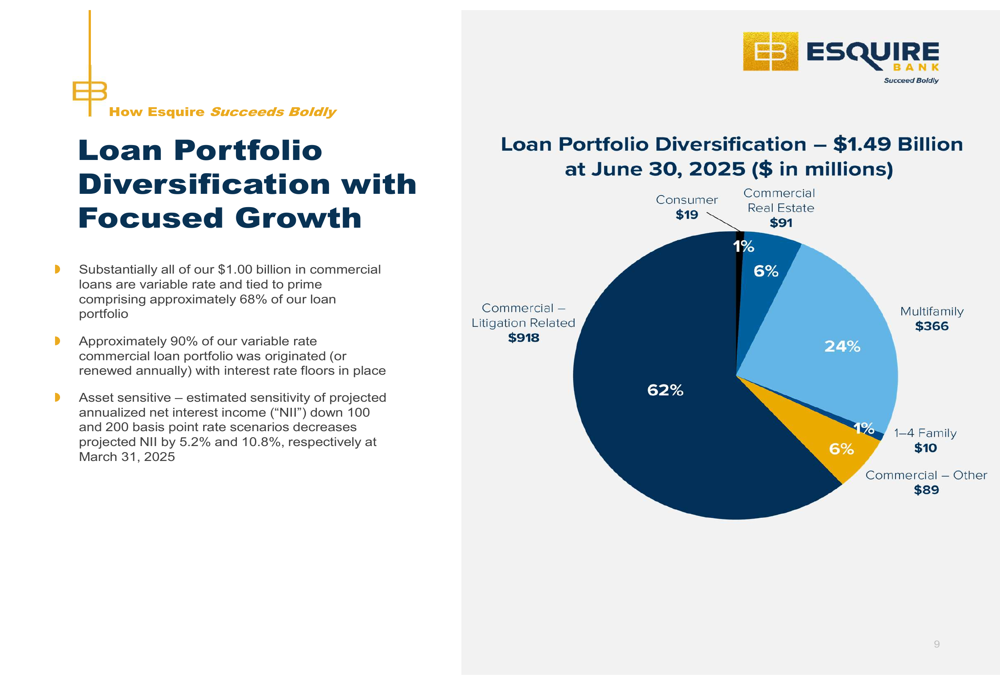

Esquire’s Q2 2025 results showcase the strength of its dual-vertical strategy. The company’s loan portfolio reached $1.49 billion, with commercial litigation-related loans representing 62% of the total. These loans are primarily variable-rate and tied to prime, providing an asset-sensitive balance sheet that benefits from the current interest rate environment.

The company’s net interest margin has expanded significantly, growing from 4.47% in 2020 to 6.03% in Q2 2025, as illustrated in the following chart:

On the deposit side, Esquire maintains a stable, low-cost funding model with demand deposit accounts (DDA) and escrow-based NOW/IOLTA accounts representing 32% and 53% of total deposits, respectively. This deposit composition has been a key driver of the company’s strong net interest margin.

The payment processing vertical continues to show robust growth, with fee income increasing from $14.1 million in 2020 to $29.3 million in Q2 2025. The number of merchants served has grown from 54,000 to 92,000 during the same period, while processing volume has increased from $14.8 billion to $40 billion.

Detailed Financial Analysis

Esquire’s revenue growth has been driven by both net interest income and noninterest income, with the latter comprising payment processing fees and other sources. The following chart illustrates this balanced growth approach:

The company’s earnings per share has grown at a 33% CAGR since 2020, reflecting both revenue growth and operational efficiency. Esquire maintains a strong efficiency ratio of 47.6%, allowing a significant portion of revenue growth to flow to the bottom line.

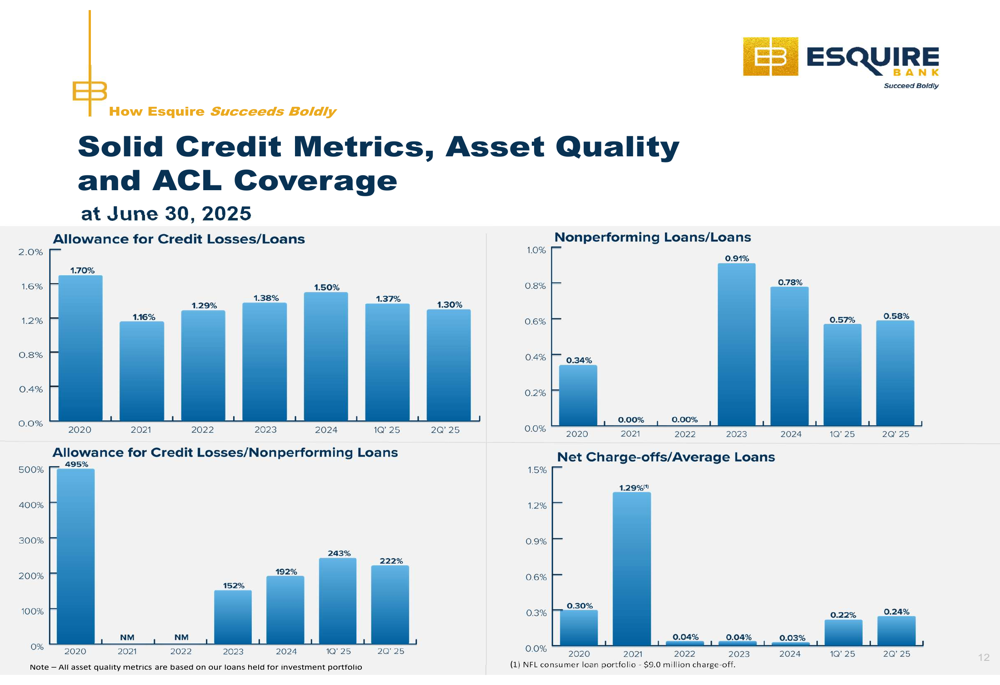

Asset quality remains solid, with nonperforming loans representing just 0.58% of total loans in Q2 2025. The allowance for credit losses stands at 1.30% of loans, providing 222% coverage of nonperforming loans. Net charge-offs remain low at 0.24% of average loans.

The loan portfolio shows significant diversification, with a focus on commercial litigation loans (62%), followed by multifamily (24%), commercial real estate (6%), and other commercial loans (6%). Consumer and 1-4 family loans each represent just 1% of the portfolio.

Strategic Initiatives

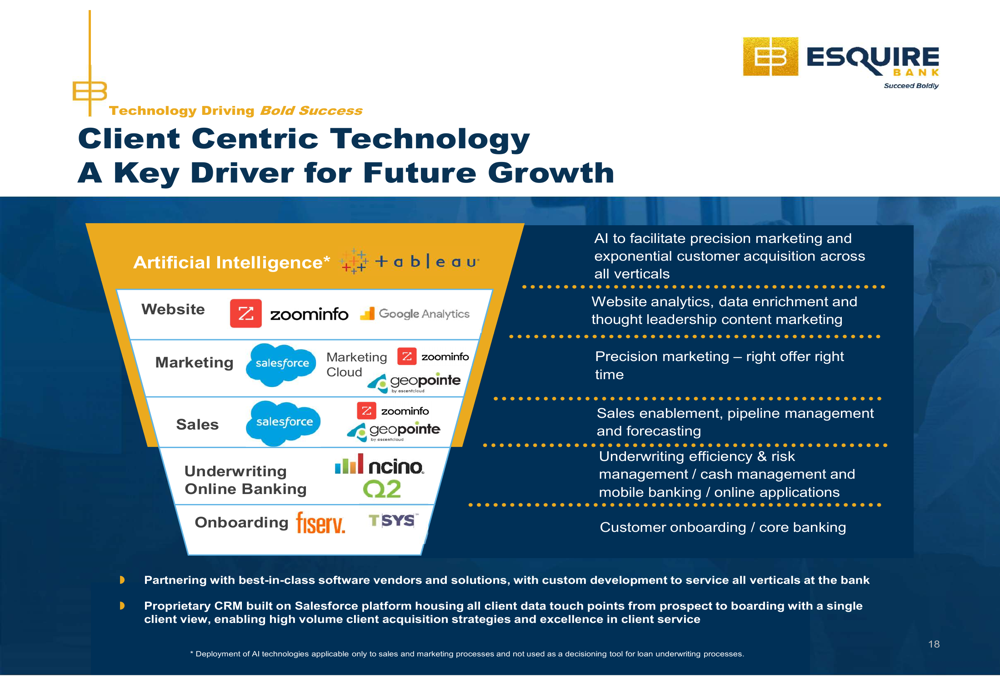

Esquire’s growth strategy centers on leveraging technology to enhance client acquisition and service across both verticals. The company is implementing artificial intelligence to facilitate precision marketing and customer acquisition, along with advanced analytics and data enrichment to support its sales efforts.

The company’s technology stack includes Salesforce (NYSE:CRM) for marketing and sales, nCino for underwriting and online banking, and Fiserv (NYSE:FI) for onboarding. This integrated approach aims to deliver tailored products and services to clients in both the litigation and payment processing verticals.

Esquire’s payment processing business continues to expand, with increasing merchant count and processing volume. The company maintains strong reserves to protect against merchant chargebacks and returns, with ISO and merchant DDA reserves totaling $161 million in Q2 2025.

Forward-Looking Statements

Esquire Financial sees significant growth opportunities in both of its target verticals, noting that its current market share represents only a fraction of the total addressable markets. The company’s differentiated approach and specialized expertise position it well for continued expansion.

As illustrated in the following slide, Esquire believes it is well-positioned for future success due to its focus on large, underserved markets and its technology-enabled approach:

The company’s asset-sensitive balance sheet is structured to perform well in various interest rate environments, with approximately 90% of variable-rate commercial loans having one-year interest rate floors. This provides some protection against potential rate decreases, with projected net interest income decreasing by 5.2% and 10.8% in down 100 and 200 basis point scenarios, respectively.

Esquire’s strong capital position, with equity to assets of 12.79% and a Common Equity Tier 1 ratio of 14.89%, provides a solid foundation for continued organic growth while maintaining the flexibility to pursue strategic opportunities as they arise.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.