Gold prices edge higher with focus on Ukraine-Russia, Jackson Hole

Introduction & Market Context

Essential Properties Realty Trust (NYSE:EPRT) released its April 2025 investor presentation on April 24, coinciding with its Q1 2025 earnings announcement. The net lease REIT, which focuses on single-tenant properties across service-oriented and experience-based industries, reported mixed Q1 results with revenue exceeding expectations at $129.35 million but earnings per share slightly missing forecasts at $0.29 versus the anticipated $0.30.

The stock declined 0.65% following the earnings release, trading at $32.10, still well above its 52-week low of $25.60 but below its high of $34.88. Despite the minor earnings miss, the company’s presentation highlighted strong portfolio fundamentals and significant liquidity to support continued growth.

Portfolio Performance Highlights

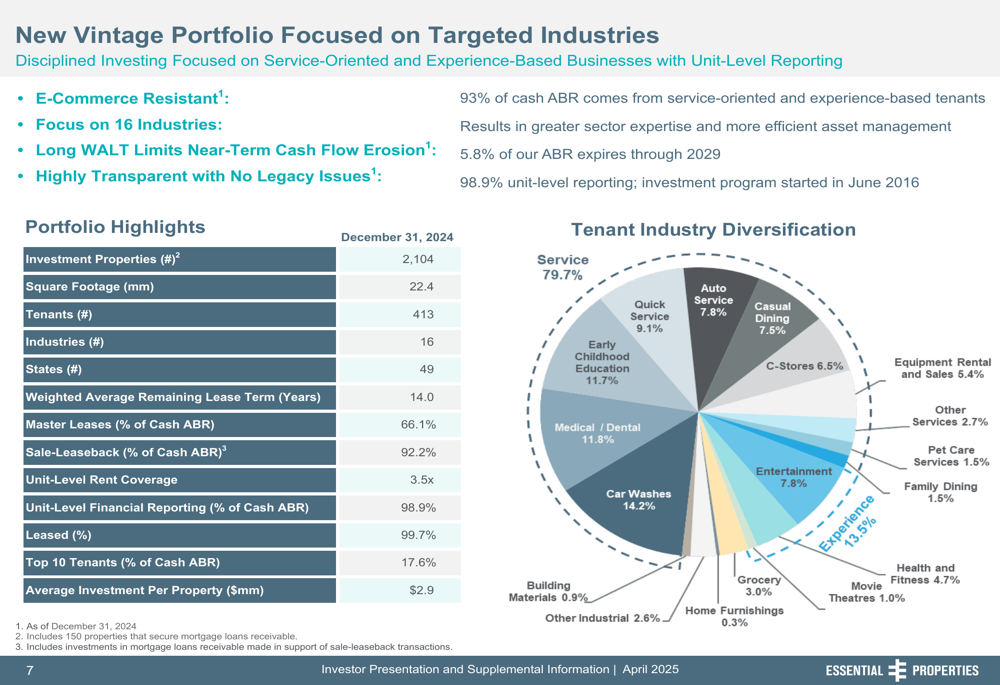

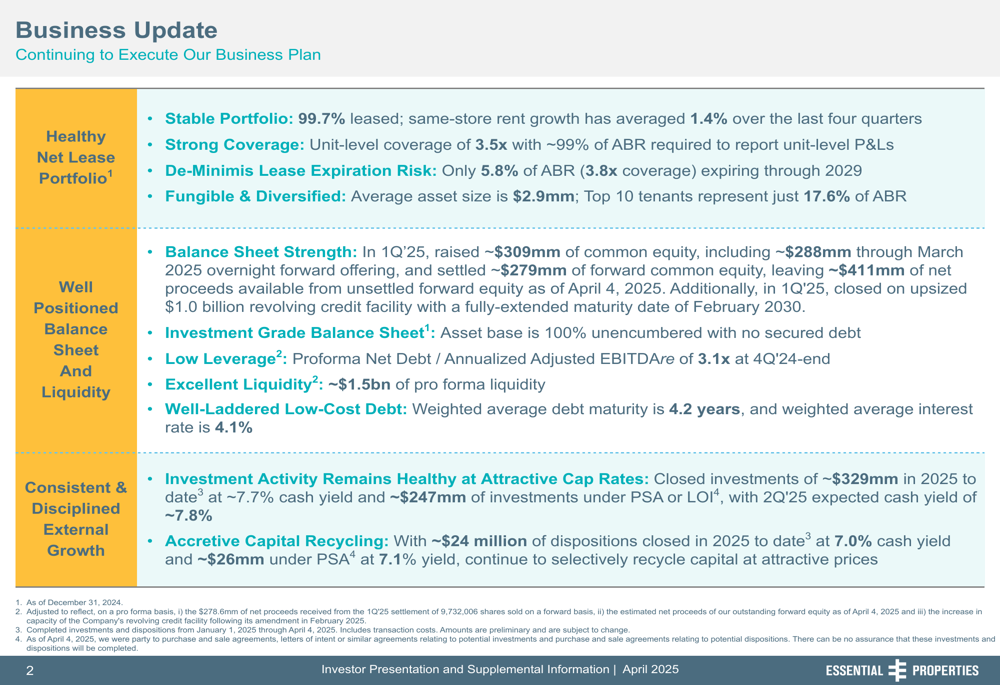

Essential Properties’ presentation emphasized the health of its portfolio, which maintained an impressive 99.7% occupancy rate with 1.4% average same-store rent growth. The company’s portfolio comprises 2,104 properties across 49 states, leased to 413 tenants in 16 industries, with a weighted average remaining lease term of 14.0 years.

As shown in the following portfolio highlights slide, the company maintains strong tenant diversification with top 10 tenants representing just 17.6% of annualized base rent (ABR), and an average investment size of $2.9 million per property:

The portfolio demonstrates strong credit quality with 3.5x average unit-level rent coverage and 98.9% of properties providing unit-level financial reporting. The company’s tenant mix is heavily weighted toward service-oriented businesses (79.7%), followed by experience-based tenants (13.5%), retail (3.3%), and industrial (3.5%).

A detailed breakdown of tenant and industry diversification reveals Equipment Share as the largest tenant at 4.2% of ABR across 59 properties, followed by Chicken N Pickle (1.9%) and Yesway (1.6%):

The company’s geographic footprint is well-diversified, with approximately 51% of ABR coming from Sunbelt states. Texas represents the largest concentration at 12.6% of ABR, aligning with the company’s strategy of investing in high-growth markets:

Financial Position & Liquidity

Essential Properties highlighted its strong balance sheet and conservative capital structure in the presentation. The company raised approximately $309 million in common equity during Q1 2025 and closed a $1.0 billion revolving credit facility with maturity extended to February 2030.

The company maintains low leverage with a 3.1x proforma net debt to adjusted EBITDAre ratio and a weighted average debt maturity of 4.2 years at a 4.1% interest rate. The debt structure is 100% unsecured with no significant maturities until 2027, as illustrated in the following slide:

With approximately $1.5 billion in proforma liquidity, Essential Properties is well-positioned to execute on its investment pipeline. This strong liquidity position supports management’s confidence in achieving the upper half of its $900-$1,100 million annual investment guidance:

In Q1 2025, the company reported AFFO per share of $0.45, representing a 7% year-over-year increase, despite the slight EPS miss. Total (EPA:TTEF) AFFO rose by 21% compared to the same period last year, reaching $85.7 million.

Competitive Positioning

Essential Properties differentiates itself from peers through its focus on service-oriented and experience-based industries, which are generally more resistant to e-commerce disruption. The company’s presentation highlighted several competitive advantages, including stronger unit-level coverage, greater transparency in financial reporting, and less reliance on top tenants compared to peers:

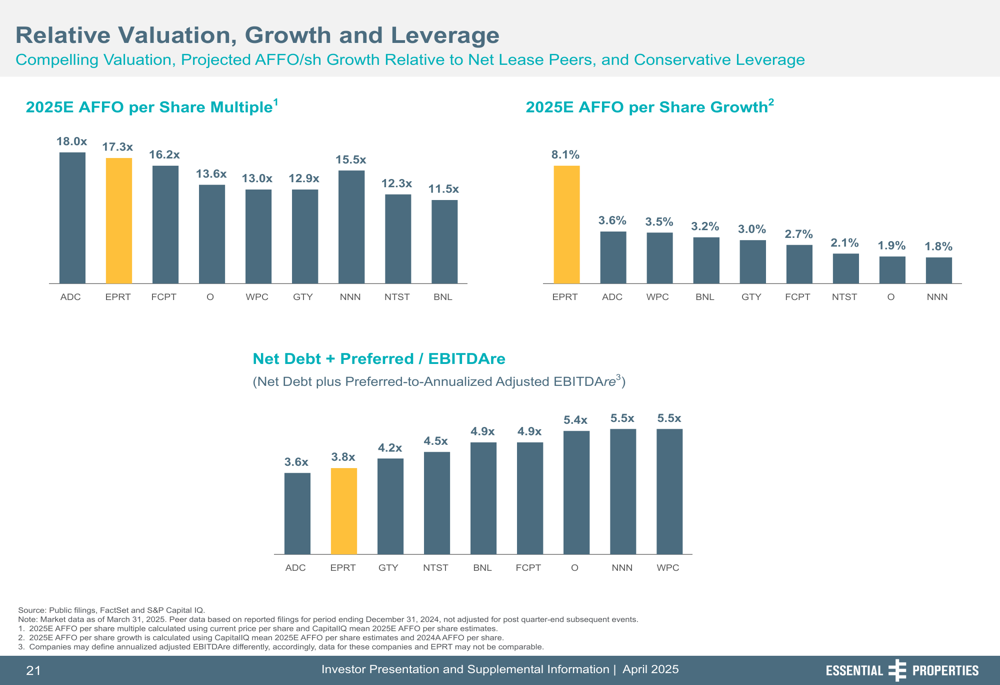

The company also compares favorably on valuation metrics, with a 2025E AFFO per share multiple of 17.3x, in line with industry leader Agree Realty (NYSE:ADC). Essential Properties’ expected AFFO growth rate positions it among the top performers in the net lease sector:

Investment Strategy & ESG Initiatives

Essential Properties’ investment strategy focuses on providing bespoke capital solutions through sale-leaseback transactions. In Q4 2024, 100% of the company’s investments were structured as sale-leasebacks, targeting middle-market tenants across 16 core industries.

The company closed approximately $329 million in investments at a 7.7% cash yield in Q4 2024, with an additional $247 million under purchase and sale agreements or letters of intent at an expected 7.8% yield. This investment activity is supported by the company’s strong liquidity position and disciplined underwriting approach.

Essential Properties also highlighted its commitment to environmental, social, and governance (ESG) initiatives, with 98% of new leases in 2024 structured as green leases. The company maintains strong governance practices with 86% board independence and emphasizes diversity with 43% of employees being women:

Forward Outlook

Despite the slight Q1 earnings miss, Essential Properties reaffirmed its 2025 AFFO per share guidance of $1.85-$1.89, indicating confidence in its operational strategy and market position. CEO Pete Mavoides emphasized the company’s focus on owning real estate with durable cash flows that grow over time during the earnings call.

The company’s presentation highlighted several key investment advantages, including consistent sector-leading annual AFFO growth of approximately 9% since IPO, methodical pipeline expansion, and platform efficiency:

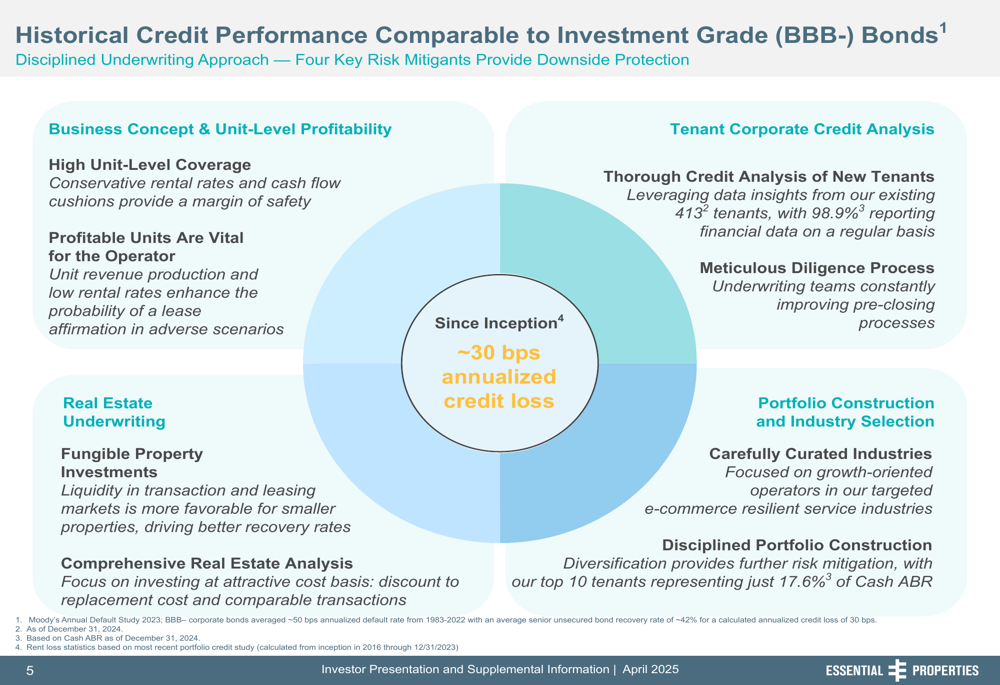

Management noted that the middle-market credit environment remains a focus area requiring ongoing monitoring, though the company’s historical credit performance has been strong with only approximately 30 basis points of annualized credit loss since inception.

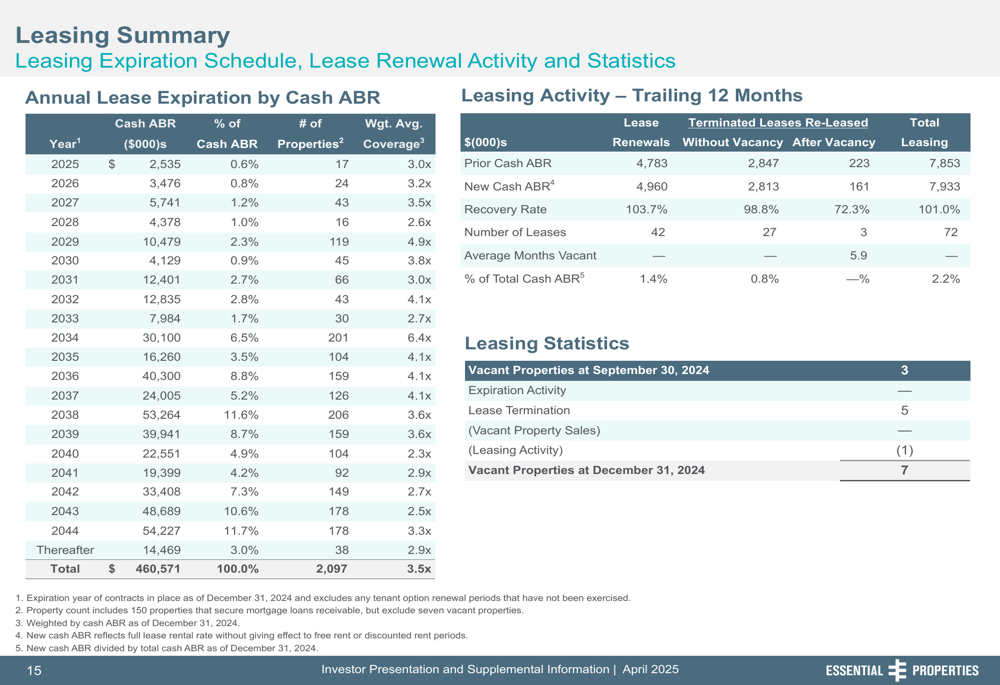

With minimal near-term lease expirations (only 5.8% of ABR expiring through 2029), a well-laddered debt maturity schedule, and significant liquidity, Essential Properties appears well-positioned to continue executing its growth strategy despite the minor earnings miss in Q1 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.