Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Eurogroup Laminations SpA (BIT:EGLA) presented its Q1 2025 results on May 20, 2025, revealing a period of revenue growth accompanied by margin pressures. The company’s stock responded positively to the presentation, surging 11.16% to €3.01, moving away from its 52-week low of €2.10 but still well below its 52-week high of €4.46.

The results come after a challenging Q4 2024, when the company missed revenue forecasts. This quarter shows signs of recovery in some segments while highlighting ongoing challenges in profitability as the company continues its strategic expansion in key markets.

Quarterly Performance Highlights

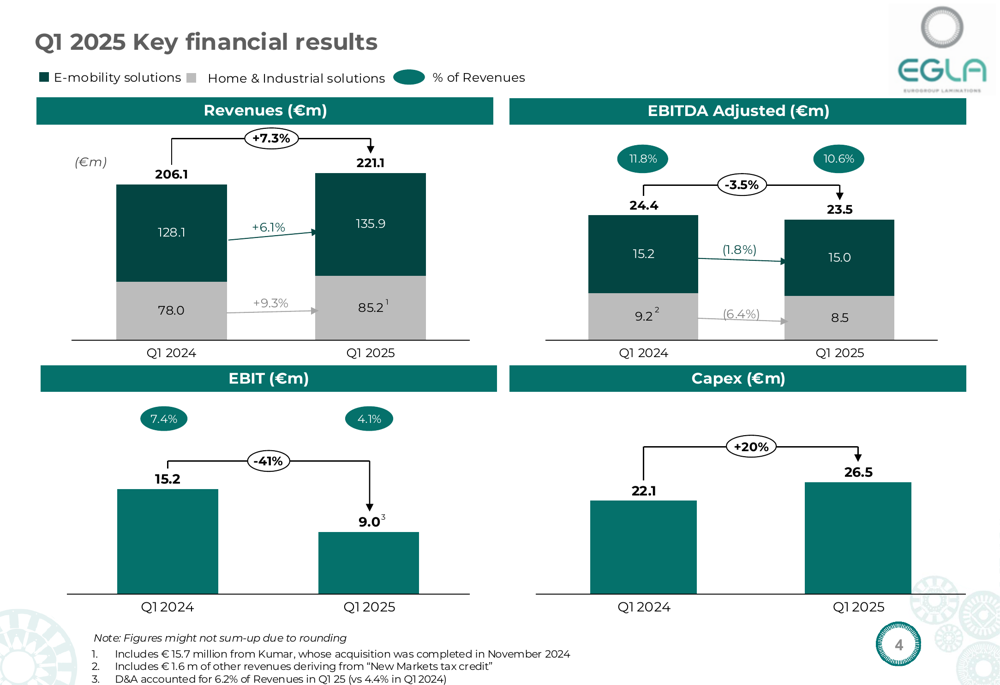

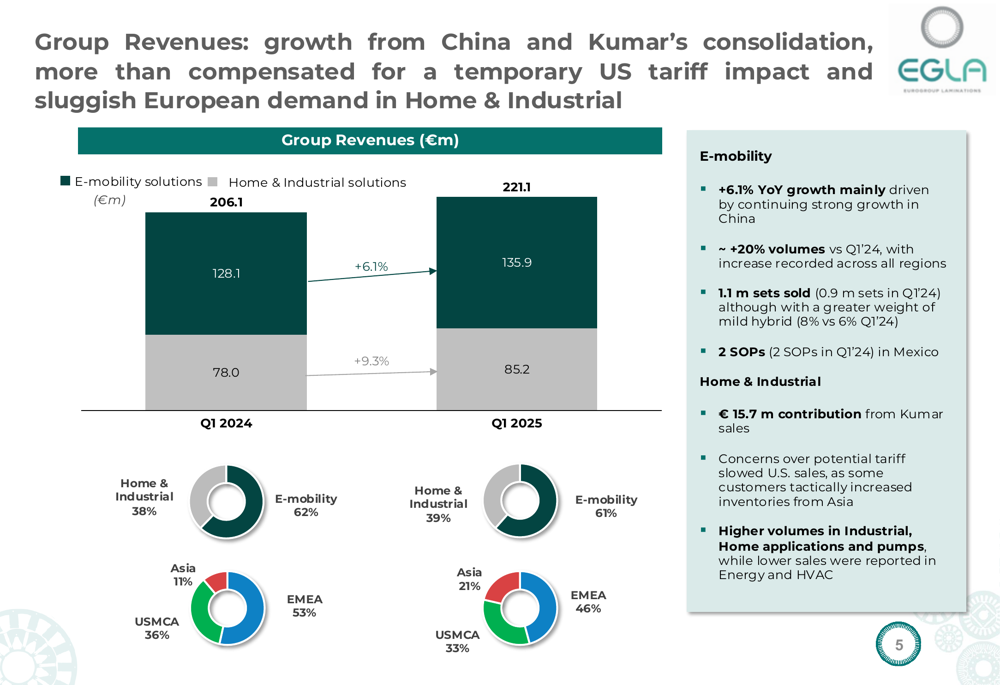

Eurogroup Laminations reported Q1 2025 revenues of €221.1 million, representing a 7.3% increase compared to Q1 2024. This growth was driven by a 9.3% increase in E-mobility solutions revenue to €85.2 million and a 6.1% rise in Home & Industrial solutions revenue to €135.9 million.

The E-mobility segment benefited from approximately 20% volume growth, with an increasing contribution from China. Meanwhile, the Home & Industrial segment was bolstered by the consolidation of Kumar, an acquisition completed in November 2024, which contributed €15.7 million to revenues.

As shown in the following breakdown of the company’s financial results:

Despite revenue growth, adjusted EBITDA declined by 3.5% to €23.5 million, with margins under pressure in both business segments. The E-mobility segment faced challenges due to new project ramp-ups, while the Home & Industrial segment was affected by lower volumes in the US market.

More concerning was the 41% drop in EBIT to €9.0 million and a swing to a €2 million loss for the period, compared to an €8 million profit in Q1 2024. This decline was partly attributed to €5.9 million in unrealized forex losses.

Detailed Financial Analysis

The company’s revenue growth shows geographic diversification, with increasing contributions from Asian markets, particularly China. The following chart illustrates the revenue breakdown by segment and region:

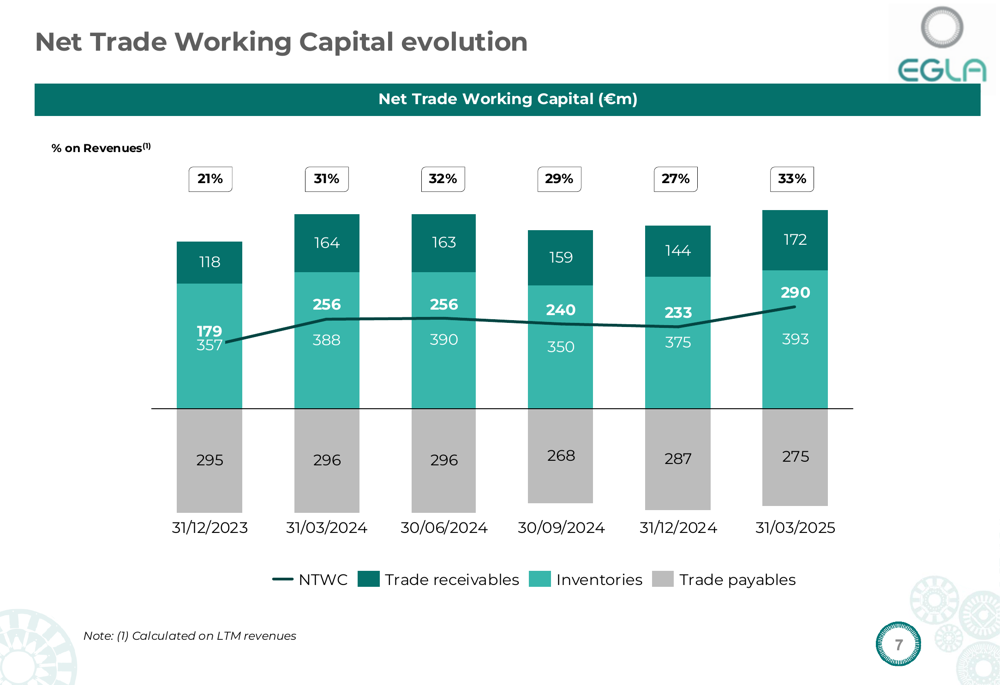

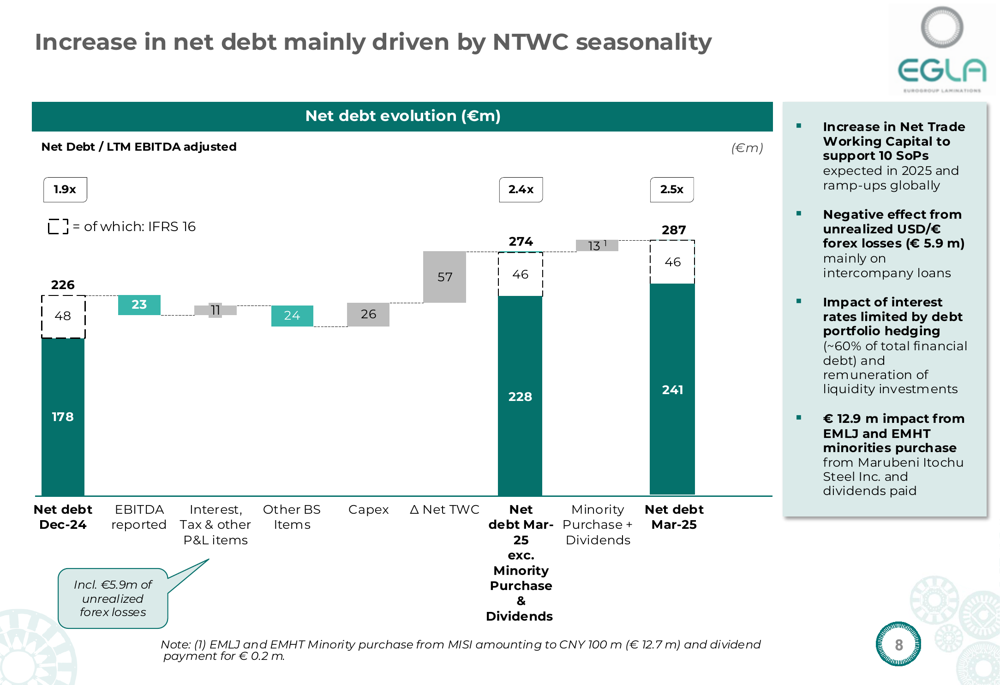

Working capital management remains a challenge for Eurogroup Laminations. The company’s net debt increased to €241 million, with a Net Debt/LTM EBITDA adjusted ratio of 1.9x, unchanged from the previous quarter but indicating growing leverage as EBITDA declined.

The increase in net debt was primarily driven by higher net trade working capital and increased capital expenditures, which rose 20% year-over-year to €26.5 million. This waterfall chart demonstrates the factors contributing to the net debt increase:

The company’s consolidated profit and loss statement reveals the impact of these challenges on bottom-line performance. While revenues grew, the profit margin turned negative at -0.9% compared to a positive 4.0% in Q1 2024. This deterioration reflects both operational challenges and significant unrealized forex losses.

Cash flow from operating activities improved from -€48 million in Q1 2024 to -€14 million in Q1 2025, but remained negative, indicating ongoing pressure on the company’s liquidity position.

Strategic Initiatives

Eurogroup Laminations continues to pursue strategic expansion in high-growth markets, particularly in Asia. The company disclosed ongoing discussions for new joint ventures in China and India, building on its existing presence in these markets.

This strategic focus aligns with the company’s previous statements about pivoting toward markets with higher growth potential, as mentioned in their Q4 2024 earnings call when CFO Matteo Perna noted, "We are considering a robust growth both in China and in USMCA whilst a reduction in Europe."

The Kumar acquisition, completed in November 2024, is already contributing positively to the Home & Industrial segment, helping to offset challenges in the US market. This acquisition represents part of the company’s strategy to diversify its revenue streams and expand its global footprint.

Forward-Looking Statements

Despite the profitability challenges in Q1, Eurogroup Laminations has maintained its guidance for both FY 2025 and mid-term (2025-2028) targets. The company expects continued growth with a focus on increased profitability, selective capital expenditure, and improved investment returns.

The following slide details the company’s financial targets:

For FY 2025, Eurogroup Laminations projects year-over-year sales growth of approximately 10%, with an adjusted EBITDA margin of around 12%. Capital expenditure is expected to be approximately €70 million, with positive operating free cash flow.

In the mid-term (2025-2028), the company targets a sales CAGR of 10-15%, an average EBITDA margin of around 13%, and average CAPEX intensity of 4-5%. The company aims to achieve a return on capital employed (ROCE) of 15-20% by 2028.

These targets assume stable macroeconomic conditions and represent a commitment to improving profitability while maintaining growth momentum. The company’s stable orderbook of €5.2 billion and pipeline of €3.2 billion provide some confidence in its ability to achieve these targets, despite the current margin pressures.

The market’s positive reaction to the presentation suggests investors are focusing on the company’s growth potential and strategic initiatives rather than the short-term profitability challenges. However, Eurogroup Laminations will need to demonstrate progress in margin recovery in upcoming quarters to maintain this investor confidence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.