Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

Online insurance marketplace EverQuote Inc (NASDAQ:EVER) released its Q2 2025 investor presentation on August 4, highlighting strong year-over-year growth across key financial metrics while unveiling new capital allocation initiatives. The company, which connects insurance providers with consumers, reported significant expansion in both revenue and profitability as it continues to capitalize on the growing digital transformation in the property and casualty (P&C) insurance industry.

The presentation comes after the stock closed at $24.10, up 6.93% in regular trading, with minimal movement in after-hours trading. While the Q2 results show substantial year-over-year improvements, they represent a sequential decline from the company’s record Q1 2025 performance, when revenue reached $166.6 million.

Quarterly Performance Highlights

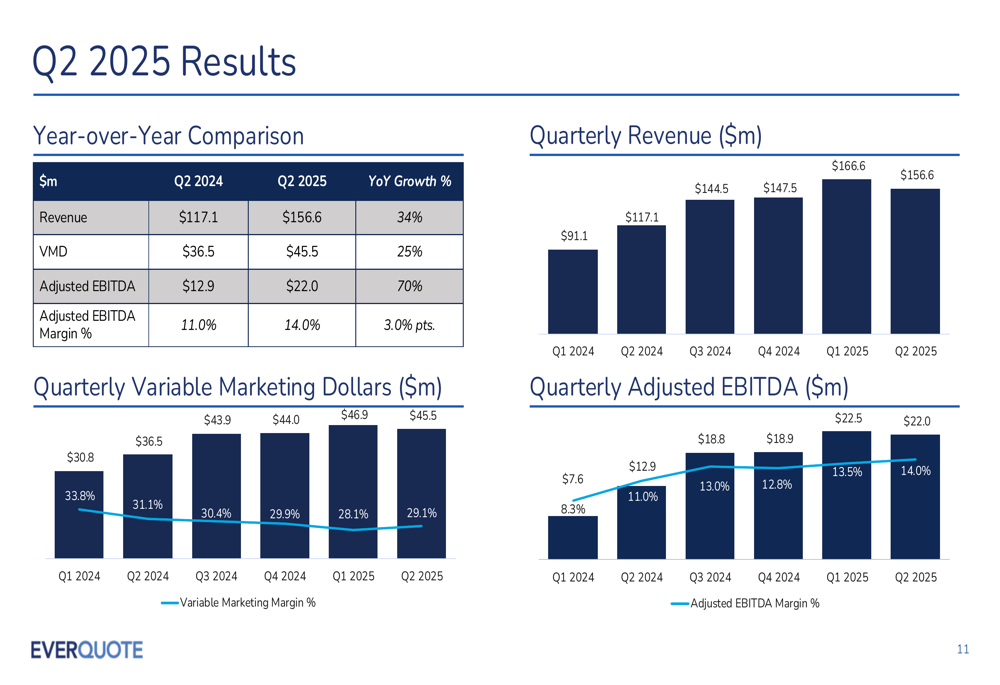

EverQuote reported Q2 2025 revenue of $156.6 million, representing a 34% increase compared to the same period last year. The company’s profitability metrics showed even stronger improvement, with Adjusted EBITDA reaching $22.0 million, a 70% year-over-year jump, and Adjusted EBITDA margin expanding by 3.0 percentage points to 14.0%.

As shown in the following chart of quarterly performance metrics, the company has maintained strong momentum in both revenue and adjusted EBITDA:

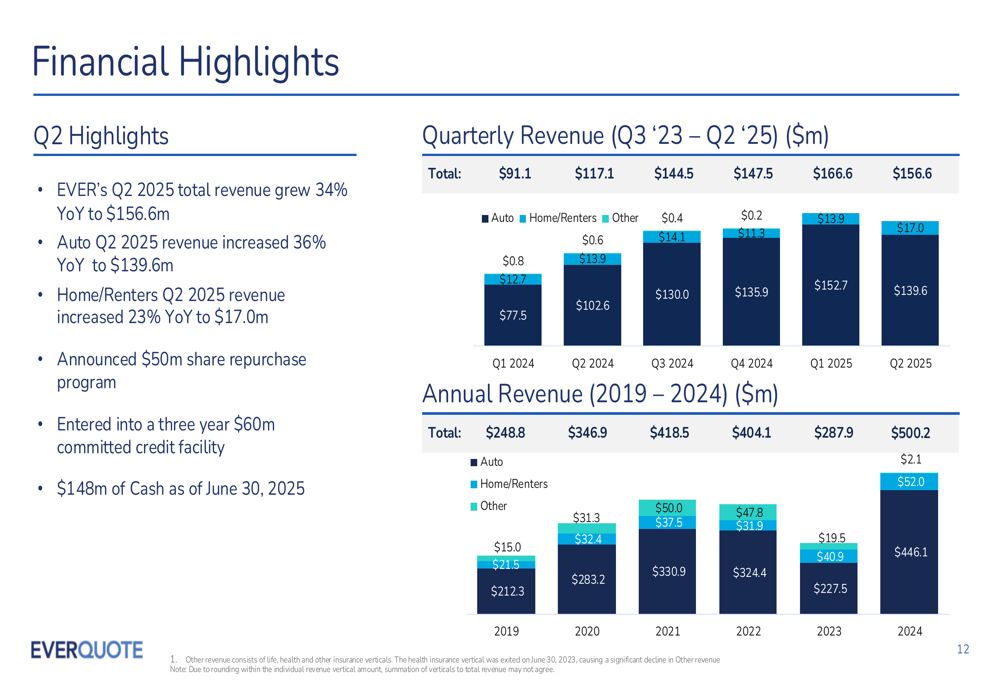

Breaking down revenue by segment, auto insurance continues to be EverQuote’s primary growth driver, with Q2 2025 auto revenue increasing 36% year-over-year to $139.6 million. The home and renters insurance vertical grew 23% year-over-year to $17.0 million. This segment breakdown illustrates the company’s continued dominance in auto insurance while making progress in diversifying its revenue streams.

The following chart provides a detailed view of quarterly and annual revenue trends across segments:

Despite the strong year-over-year growth, it’s worth noting that Q2 revenue of $156.6 million represents a sequential decline from the $166.6 million reported in Q1 2025. This sequential dip appears across both the auto and home/renters segments, though it falls within the company’s previously issued guidance range of $155-160 million for the quarter.

Strategic Initiatives and Market Opportunity (SO:FTCE11B)

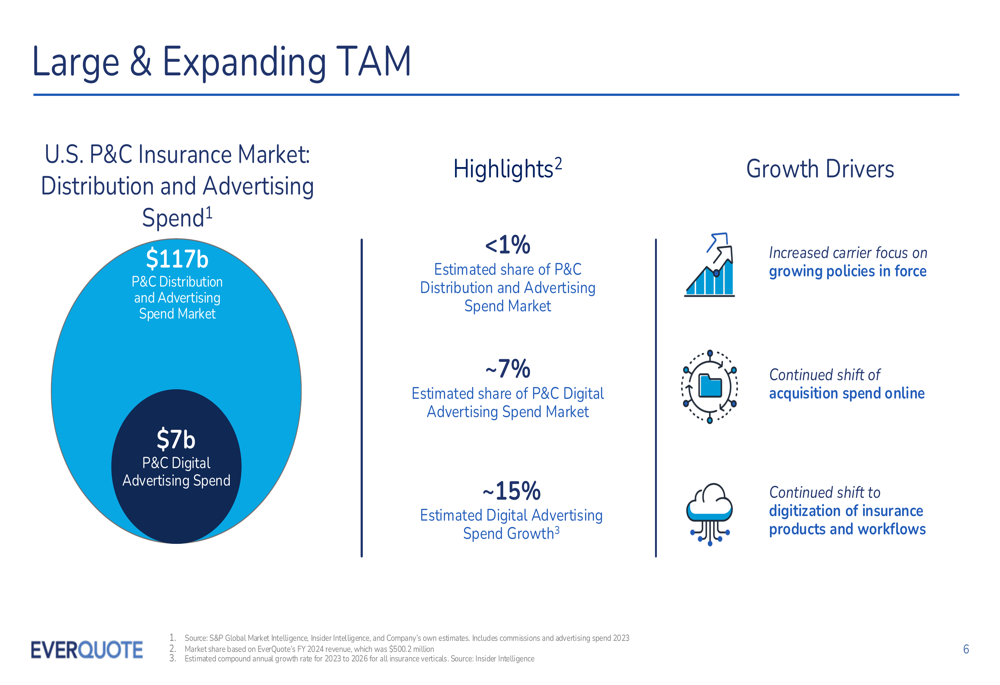

EverQuote continues to position itself as a leader in the digital transformation of insurance distribution, highlighting a massive total addressable market (TAM) of $117 billion in annual P&C insurance distribution and advertising spend. The company currently captures less than 1% of this total market and approximately 7% of the $7 billion P&C digital advertising segment, suggesting significant room for expansion.

The following visualization illustrates the scale of EverQuote’s market opportunity:

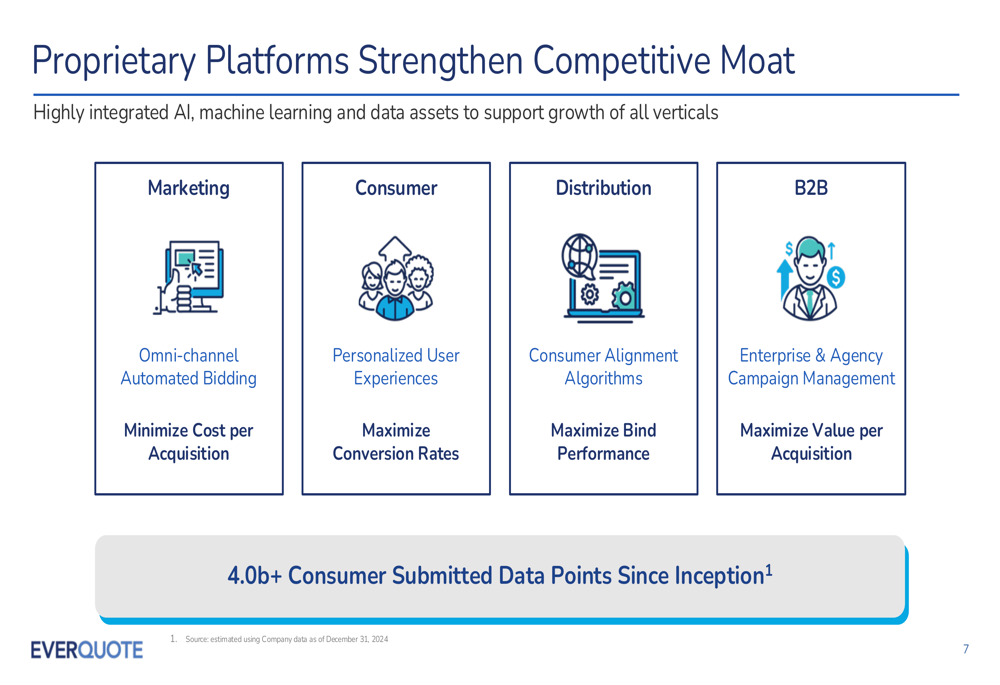

The company’s competitive advantage stems from its proprietary technology platforms and extensive data assets. EverQuote has accumulated over 4.0 billion consumer-submitted data points since inception (as of December 31, 2024), which it leverages across its marketing, consumer, distribution, and B2B platforms to optimize performance.

As shown in the following slide, these proprietary platforms create a significant competitive moat:

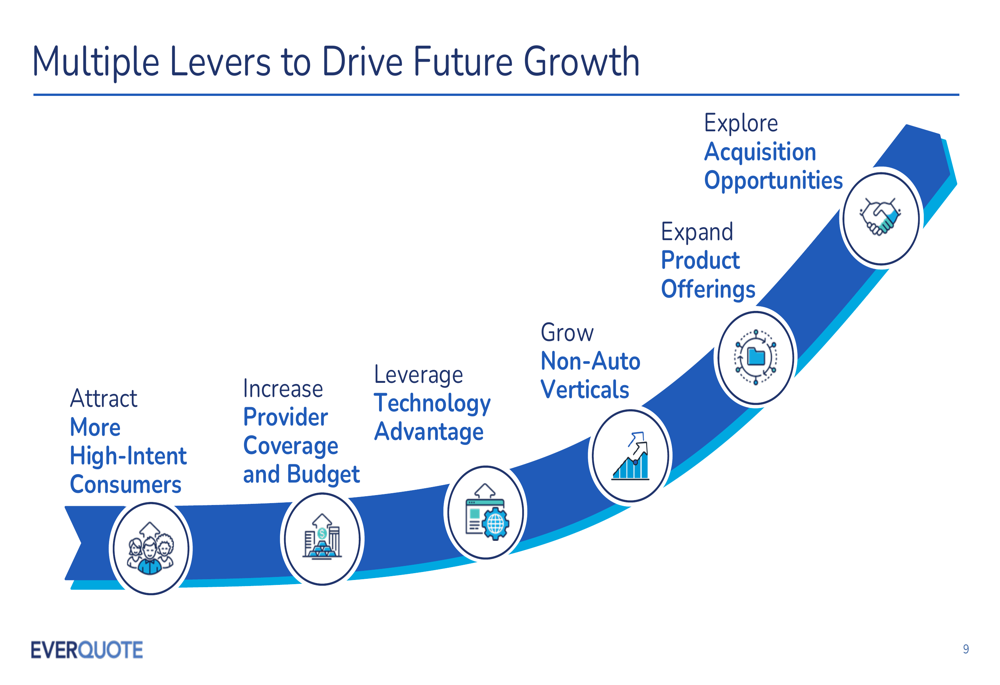

EverQuote’s growth strategy encompasses multiple levers, including attracting more high-intent consumers, increasing provider coverage and budgets, leveraging its technology advantage, growing non-auto verticals, expanding product offerings, and exploring acquisition opportunities.

Financial Position and Capital Allocation

The presentation revealed that EverQuote has significantly strengthened its financial position, with $148 million in cash as of June 30, 2025, up from $125 million reported at the end of Q1. The company also announced two significant capital allocation initiatives: a $50 million share repurchase program and entry into a three-year $60 million committed credit facility, signaling management’s confidence in the business and providing additional financial flexibility.

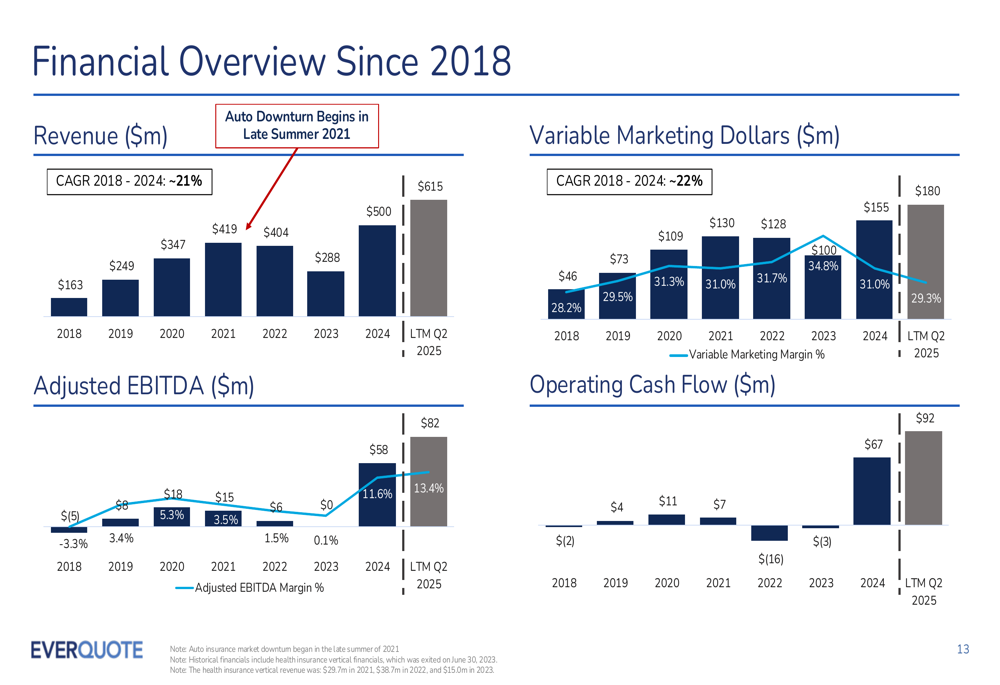

Looking at the company’s long-term financial trajectory, EverQuote has demonstrated consistent growth since 2018, with revenue increasing from $163 million to $500 million in 2024, representing a compound annual growth rate (CAGR) of approximately 21%. This growth has been accompanied by improving profitability metrics, with Adjusted EBITDA growing from $8 million in 2018 to $58 million in 2024 and $82 million for the twelve months ended Q2 2025.

The following chart illustrates this long-term financial progression:

Forward-Looking Statements

EverQuote’s presentation emphasized several growth drivers for the P&C insurance market, including increased carrier focus on growing policies in force, continued shift of acquisition spend online, and accelerating digitization of insurance products and workflows. The company expects digital advertising spend in the P&C sector to grow at approximately 15% CAGR from 2023 to 2026.

While the presentation did not provide specific guidance for Q3 2025 or full-year results, the company’s strategic focus remains on leveraging its proprietary technology and data assets to expand its market share in the large and growing P&C insurance distribution market. The new share repurchase program and credit facility suggest management’s confidence in the company’s future cash generation capabilities and commitment to delivering shareholder value.

Investors will likely be watching for signs that EverQuote can reverse the sequential revenue decline seen in Q2 and return to the growth trajectory demonstrated in Q1 2025, when the company achieved record revenue of $166.6 million. The company’s ability to continue expanding its adjusted EBITDA margin, which reached 14.0% in Q2 2025, will also be a key performance indicator to monitor in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.