BofA warns Fed risks policy mistake with early rate cuts

Introduction & Market Context

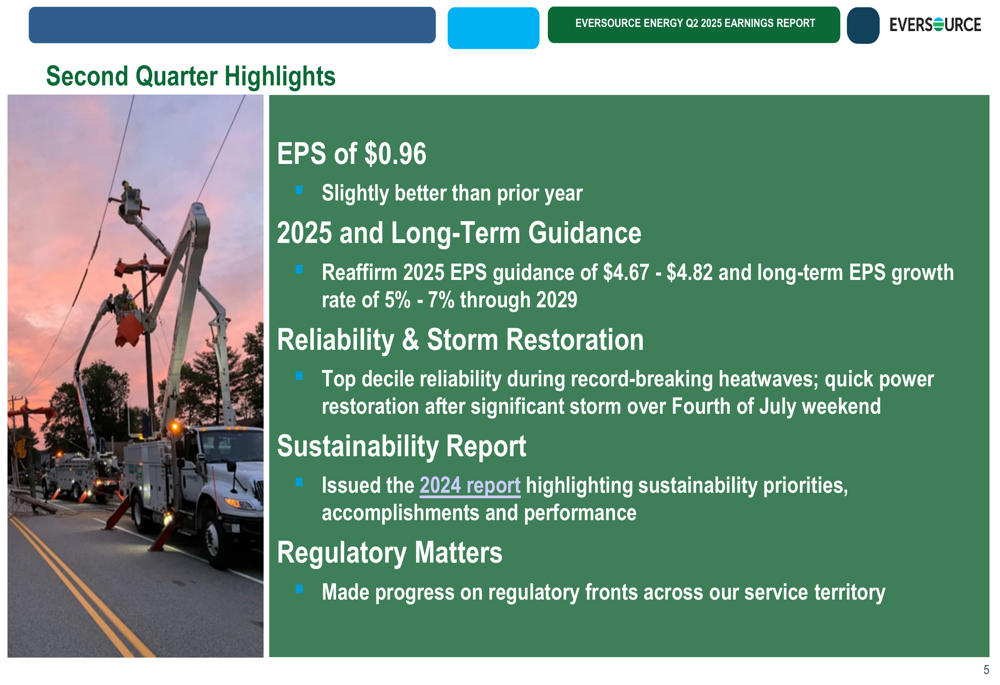

Eversource Energy (NYSE:ES) reported modest earnings growth in its Q2 2025 financial results presentation on August 1, 2025, with earnings per share (EPS) of $0.96, slightly above the $0.95 reported in the same period last year. The New England utility reaffirmed its 2025 EPS guidance range of $4.67-$4.82 and maintained its long-term EPS growth target of 5-7% through 2029.

The company’s stock closed at $66.10 on July 31, 2025, up 0.17% for the day, and has traded in a 52-week range of $52.28 to $69.01. Following its Q1 2025 results, which showed a slight EPS miss but significant revenue beat, investors have been closely monitoring Eversource’s progress on strengthening its balance sheet and advancing regulatory initiatives.

Quarterly Performance Highlights

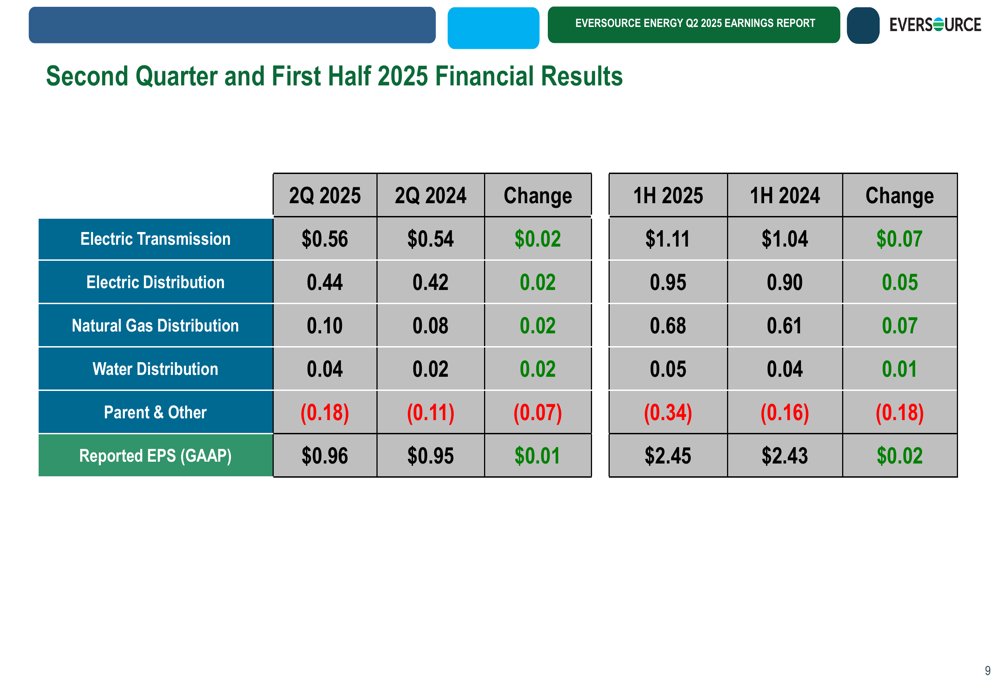

Eversource reported year-over-year improvements across all core business segments in Q2 2025, with the exception of its Parent & Other category. The company’s regulated utility operations continue to drive steady earnings growth.

As shown in the following detailed financial results table:

Electric transmission contributed the largest portion of earnings at $0.56 per share (up from $0.54 in Q2 2024), while electric distribution added $0.44 per share (up from $0.42). Natural gas distribution contributed $0.10 per share (up from $0.08), and water distribution added $0.04 per share (up from $0.02). These gains were partially offset by increased losses in the Parent & Other category, which reported -$0.18 per share compared to -$0.11 in the prior year.

The company highlighted its operational achievements during the quarter, including top decile reliability performance during record-breaking heatwaves and efficient storm restoration following severe weather over the Fourth of July weekend.

Regulatory Progress

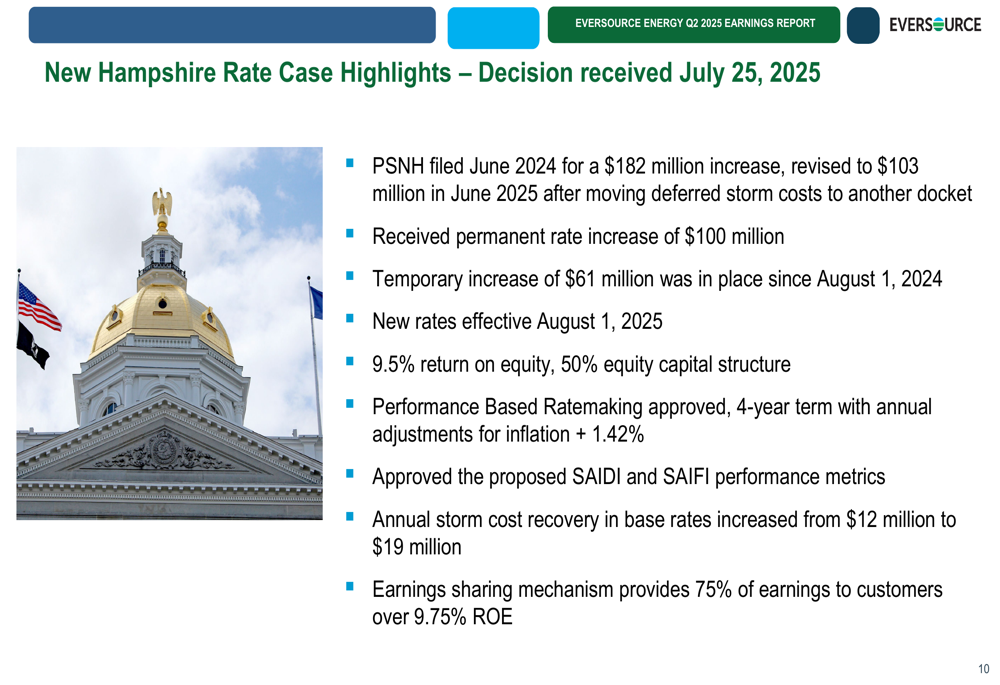

A significant focus of Eversource’s presentation was the regulatory progress achieved across its service territories. On July 25, 2025, the company received approval for a $100 million permanent rate increase for its New Hampshire subsidiary (PSNH), effective August 1, 2025. The decision includes a 9.5% return on equity with a 50% equity capital structure and approval of performance-based ratemaking with a four-year term.

In Massachusetts, Eversource has secured rate increases for both its gas and electric businesses. EGMA will receive a $77 million rate increase effective November 2024 and a $62 million increase in November 2025. NSTAR Gas will see a $12 million increase in November 2024, while NSTAR Electric received a $56 million increase effective January 2025.

In Connecticut, the company awaits a final decision on its Yankee Gas rate case, expected in October 2025, while CL&P customers have seen a 6% bill reduction following a recent RAM decision.

Strategic Initiatives

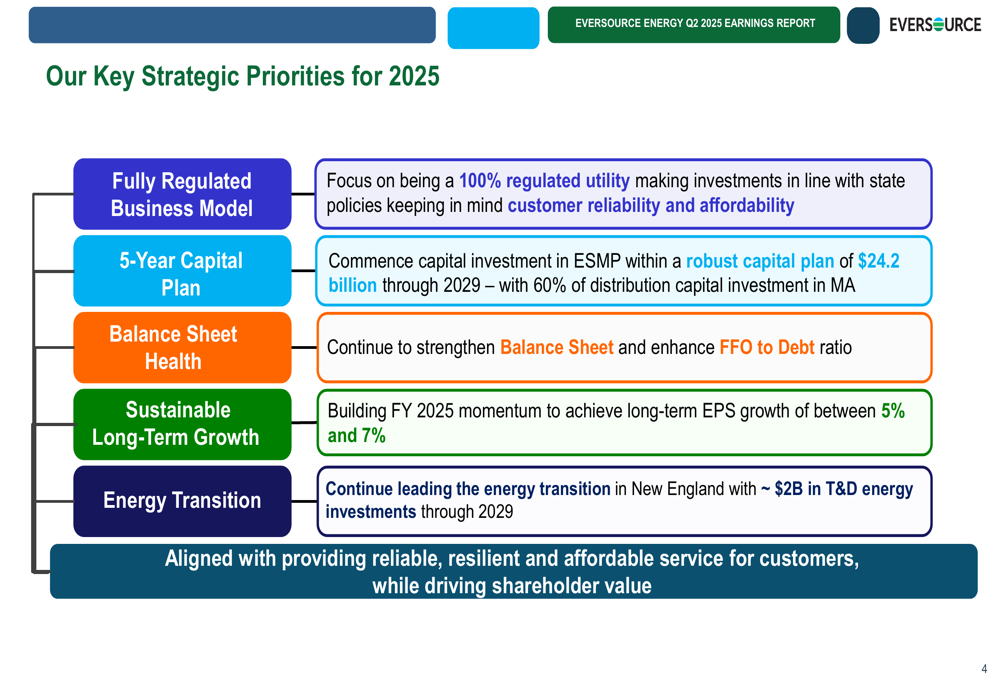

Eversource outlined its key strategic priorities for 2025, emphasizing its fully regulated business model and focus on infrastructure investments aligned with state energy policies.

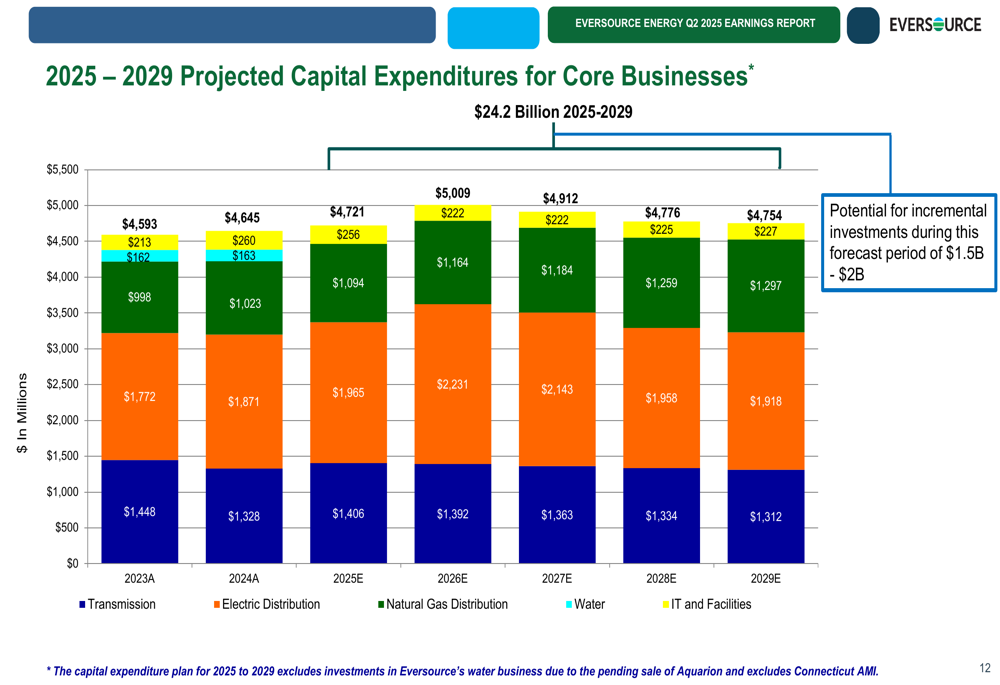

The company’s five-year capital plan includes $24.2 billion in investments through 2029, with approximately 60% of distribution capital investments targeted for Massachusetts. The plan supports an 8% compound annual growth rate in rate base from $26.4 billion in 2023 to a projected $41.9 billion by 2029.

The projected capital expenditures are broken down by business segment as follows:

Eversource continues to invest in critical infrastructure projects, including advanced metering infrastructure (AMI) deployment in Massachusetts, the Cambridge Underground Substation, and battery storage systems. The company highlighted that its Outer Cape Battery Energy Storage System was recognized as one of Energy Systems Integration Group’s 2025 Excellence Award winners.

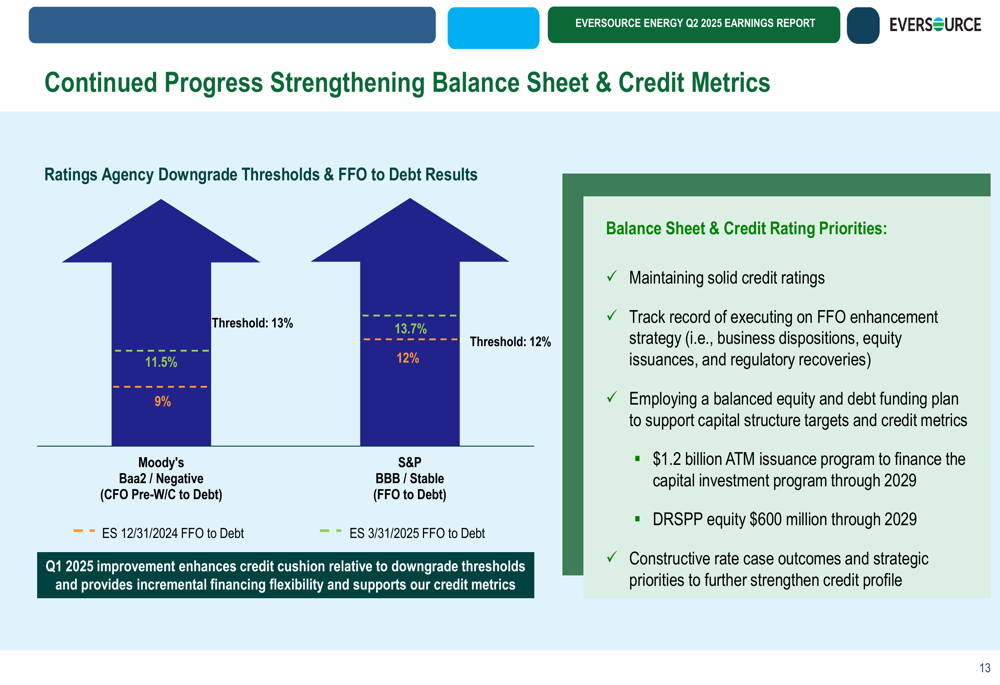

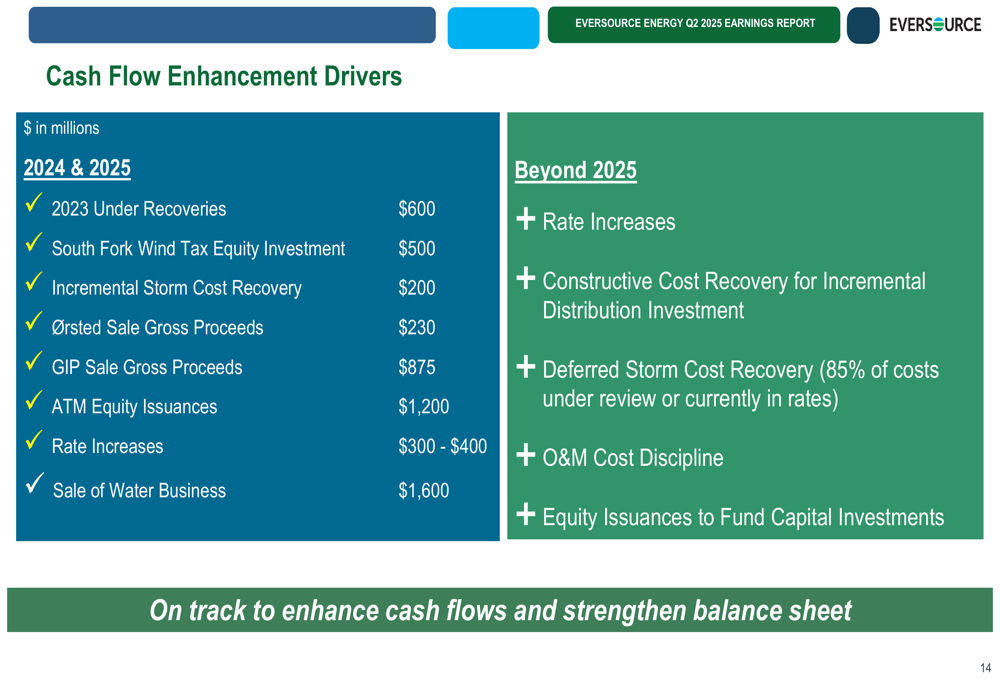

Balance Sheet Strengthening

A key focus for Eversource has been strengthening its balance sheet and credit metrics. The company reported progress in improving its FFO to debt ratios, with Moody’s metrics at 11.5% (against a 13% threshold) and S&P metrics at 13.7% (against a 12% threshold).

The company outlined several cash flow enhancement drivers, including the sale of its water business (Aquarion) for $1.6 billion, proceeds from the Ørsted sale ($230 million) and GIP sale ($875 million), and ATM equity issuances of $1.2 billion. These initiatives, combined with rate increases and storm cost recovery, are expected to significantly improve Eversource’s financial position.

Forward-Looking Statements

Eversource reaffirmed its 2025 EPS guidance range of $4.67-$4.82 and maintained its long-term EPS growth target of 5-7% through 2029. This outlook is supported by the company’s $24.2 billion capital plan and expected rate base growth of 8% annually through 2029.

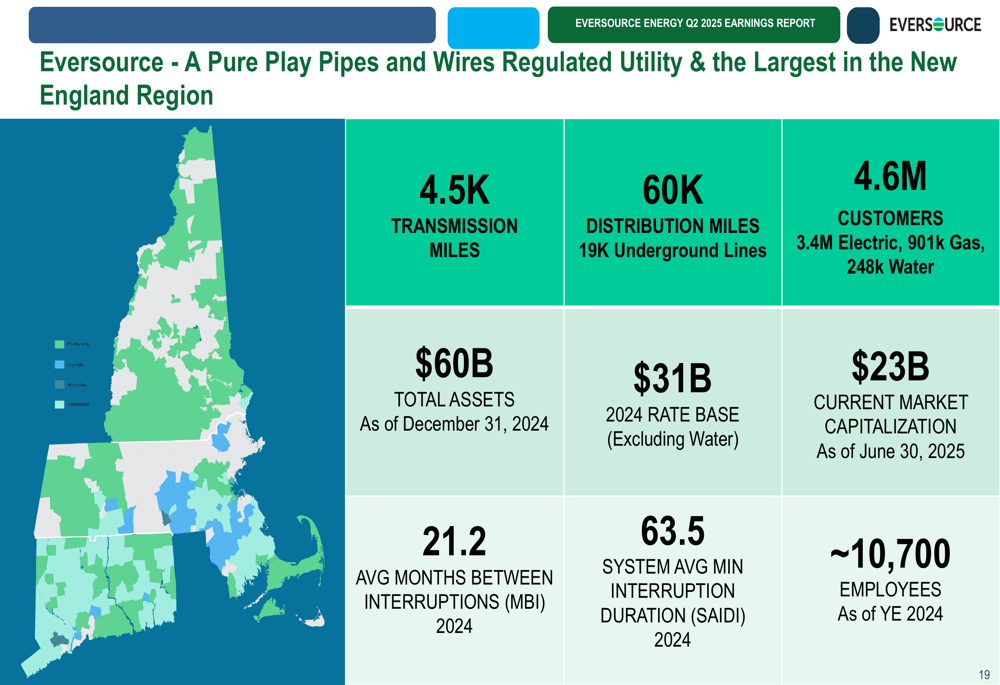

The company positions itself as a "pure play pipes and wires regulated utility" – the largest in the New England region – with 4.5K transmission miles, 60K distribution miles, and 4.6 million customers across electric, gas, and water services.

During the Q1 2025 earnings call, CEO Joe Nolan had emphasized that Eversource was "uniquely positioned to leverage our strengths in transmission and distribution investment opportunities," a strategy that continues to guide the company’s approach. The Q2 presentation reinforced this focus on regulated utility operations and infrastructure investments.

Eversource also highlighted its various recognitions, including being named #1 in Utilities & Energy in USA TODAY’s America’s Climate Leaders 2025 and inclusion in Newsweek’s America’s Most Responsible Companies 2025.

As Eversource continues to execute its strategic plan, investors will be watching closely for continued progress on balance sheet strengthening, regulatory outcomes, and the company’s ability to deliver on its long-term growth targets while maintaining reliable service across its New England service territories.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.