NVIDIA launches Jetson Thor robotics computers for physical AI systems

Introduction & Market Context

Evertec Inc (NYSE:EVTC) presented its second quarter 2025 earnings results on July 30, showing solid performance with revenue and earnings growth despite some mixed segment results. The payment processing and technology company reported 8% revenue growth, with Latin America emerging as a key growth driver. The company’s stock closed at $33.44 on the day of the earnings call, down 2.02% from the previous session.

Following a strong first quarter that saw 11.4% revenue growth, Evertec’s Q2 results indicate continued momentum, albeit at a slightly moderated pace. The company maintained its full-year outlook, suggesting management confidence in its growth trajectory for the remainder of 2025.

Quarterly Performance Highlights

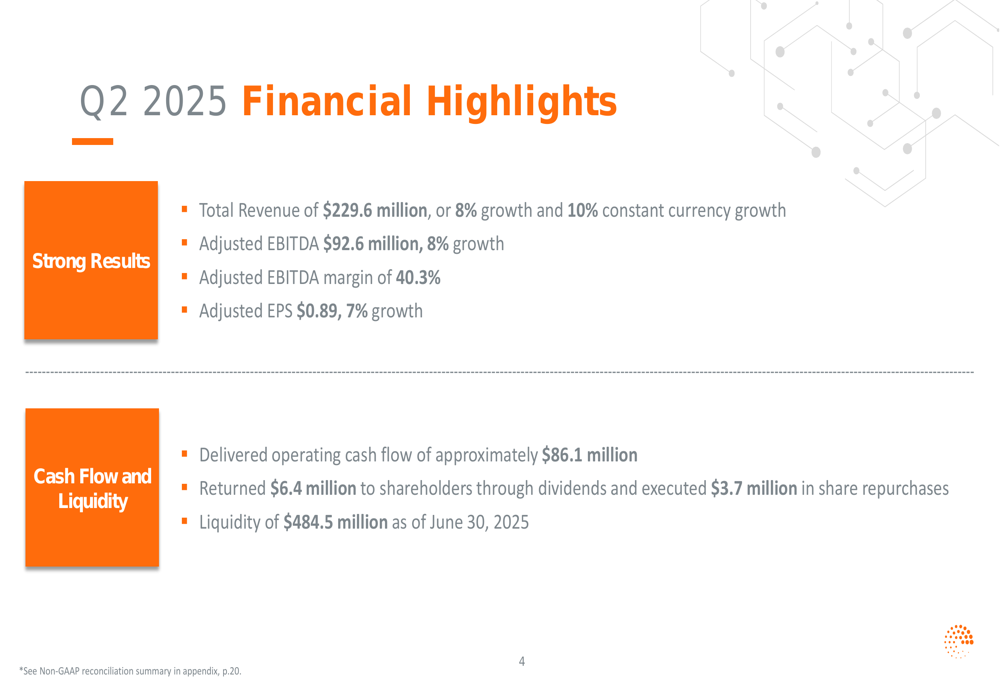

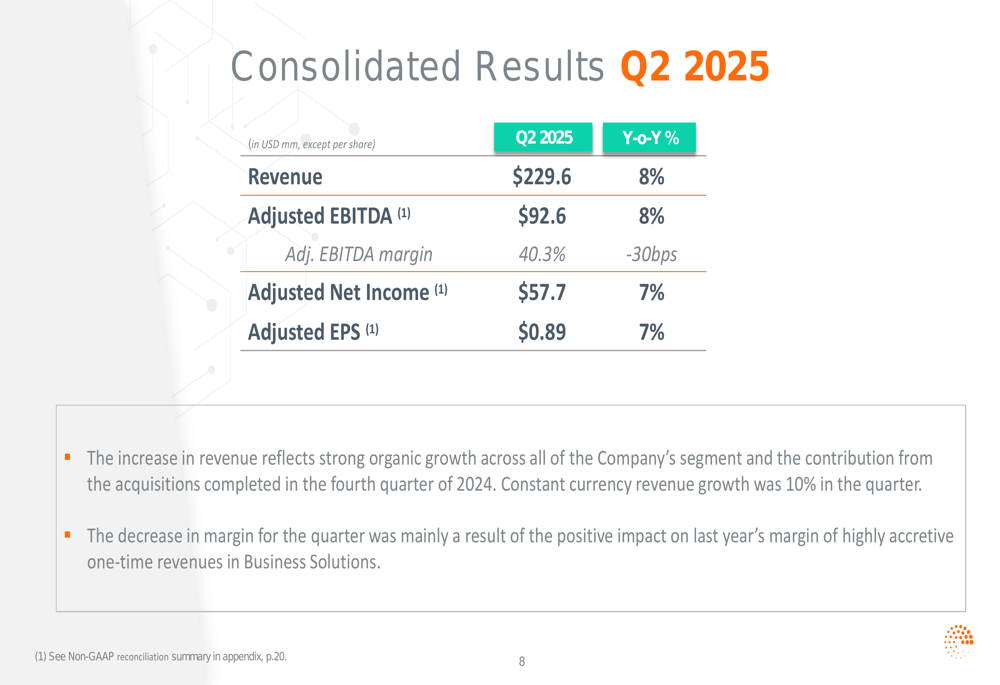

Evertec reported total revenue of $229.6 million for Q2 2025, representing an 8% increase year-over-year, or 10% on a constant currency basis. Adjusted EBITDA rose to $92.6 million, also up 8% compared to the same period last year, while adjusted earnings per share reached $0.89, a 7% improvement.

As shown in the following financial highlights:

The company generated operating cash flow of approximately $86.1 million and maintained strong liquidity of $484.5 million as of June 30, 2025. Evertec continued to return value to shareholders, distributing $6.4 million in dividends and executing $3.7 million in share repurchases during the quarter.

The consolidated results show consistent performance across key metrics:

While revenue and adjusted EBITDA both grew at 8%, the adjusted EBITDA margin experienced a slight decrease of 30 basis points to 40.3%. Management attributed this decline to the comparison against highly accretive one-time revenues in the Business Solutions segment during the same quarter last year.

Segment Analysis

Evertec’s performance varied across its four business segments, with Latin America emerging as the standout performer.

The Merchant Acquiring segment delivered solid results with 4% revenue growth to $47.3 million, driven by an improved spread that benefited from pricing initiatives and sales volume growth. Adjusted EBITDA for this segment increased by 10% to $20.0 million, with margin expanding 200 basis points to 42.3%.

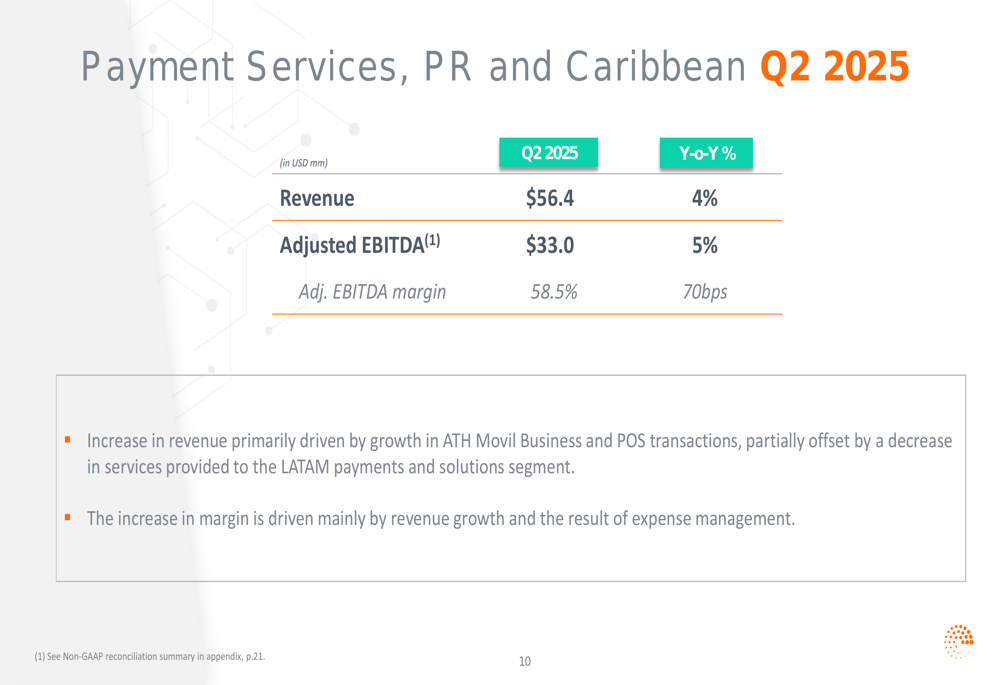

The Payment Services segment for Puerto Rico and the Caribbean also showed steady growth, with revenue increasing 4% to $56.4 million. This growth was primarily driven by ATH Movil Business and higher POS transaction volume. Adjusted EBITDA rose 5% to $33.0 million, with margin improving 70 basis points to 58.5%.

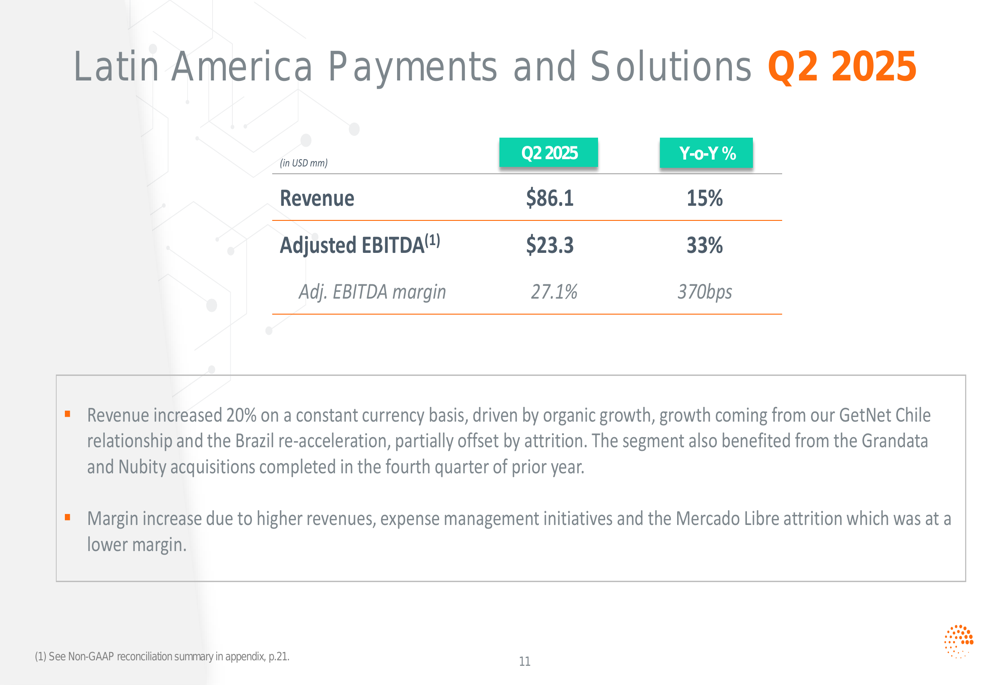

The Latin America Payments and Solutions segment was the company’s growth engine in Q2, with revenue surging 15% (20% on a constant currency basis) to $86.1 million. This impressive performance was driven by organic growth, particularly from the GetNet Chile relationship and Brazil re-acceleration, as well as contributions from the Grandata and Nubity acquisitions. Adjusted EBITDA for this segment jumped 33% to $23.3 million, with margin expanding 370 basis points to 27.1%.

The Business Solutions segment presented a more challenging picture. While revenue increased 4% to $64.5 million, adjusted EBITDA declined 13% to $26.0 million, with margin contracting significantly by 750 basis points to 40.3%. Management explained that this decline was due to the comparison against highly accretive multi-year project revenues recognized in the prior year.

Financial Position

Evertec maintained a strong financial position in Q2 2025, with improvements in its debt profile and cash position. The company’s cash balance increased from $314.6 million at the beginning of the quarter to $333.0 million by the end, supported by $86.1 million in operating activities.

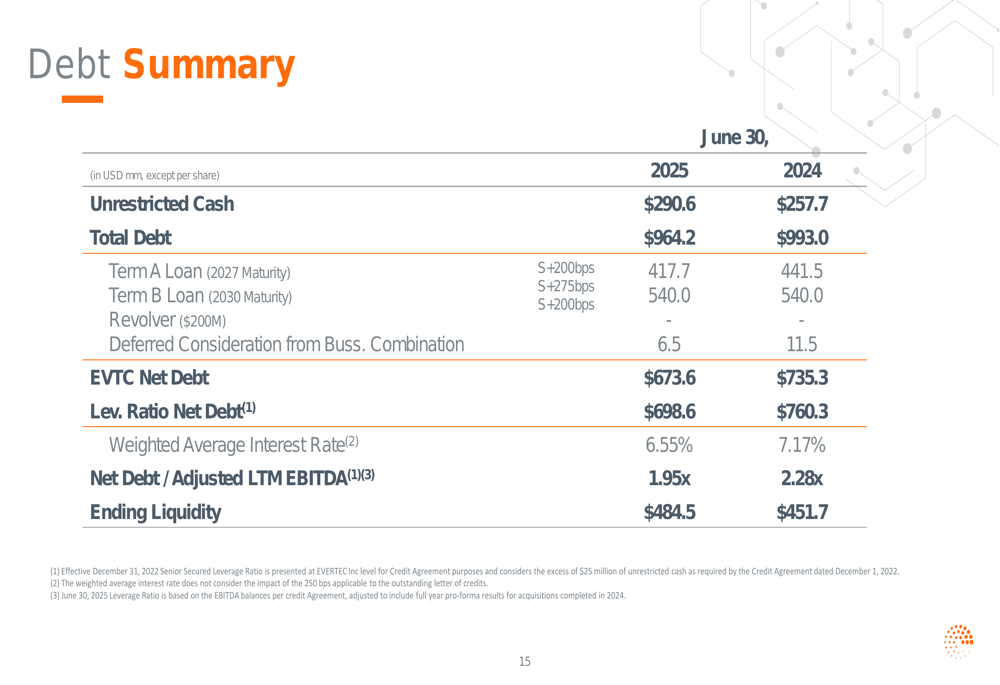

The company’s debt summary shows a healthier position compared to the same period last year:

Total (EPA:TTEF) debt decreased to $964.2 million from $993.0 million a year earlier, while unrestricted cash increased to $290.6 million from $257.7 million. The weighted average interest rate improved to 6.55% from 7.17%, and the net debt to adjusted LTM EBITDA ratio strengthened to 1.95x from 2.28x, indicating improved leverage.

Regional Performance

Puerto Rico’s economic environment remained stable during the quarter, with the unemployment rate at 5.2% and strong tourism indicated by an 11% increase in airport arrivals. This stability supported Evertec’s consistent performance across its Puerto Rico-focused segments, with both Merchant Acquiring and Payments PR growing revenue by 4%.

Latin America continued to be a bright spot for Evertec, with 15% revenue growth (20% on a constant currency basis). The company noted that its active pipeline should lead to business wins in 2025, though management remains vigilant about potential tariffs that might be imposed in countries where they operate.

Outlook & Guidance

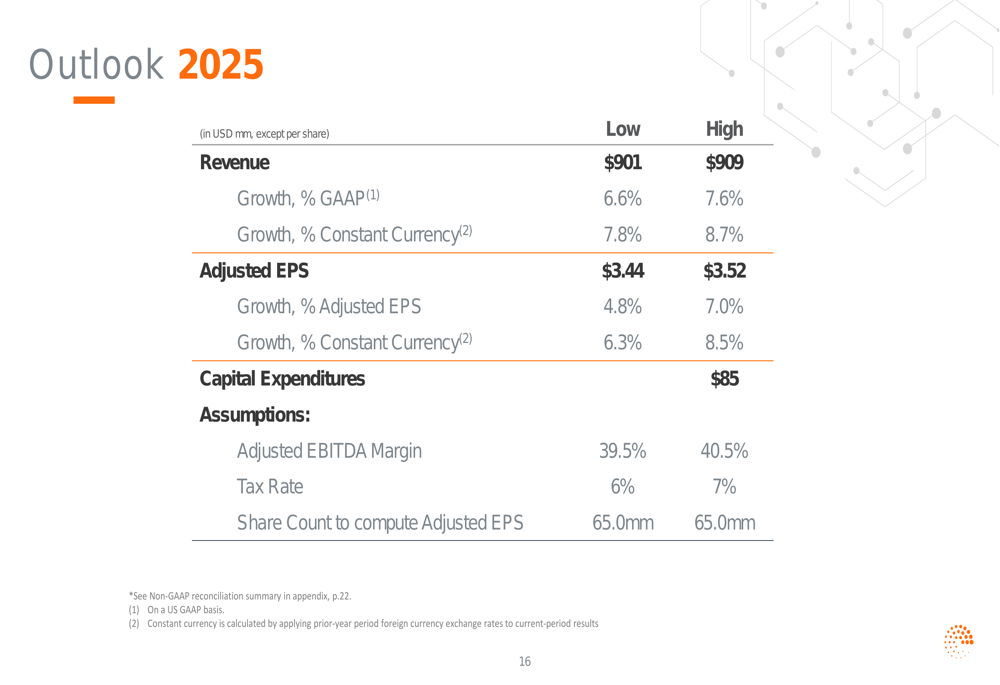

Evertec maintained its full-year 2025 outlook, projecting revenue between $901 million and $909 million, representing growth of 6.6% to 7.6% (7.8% to 8.7% on a constant currency basis). The company expects adjusted earnings per share between $3.44 and $3.52, reflecting growth of 4.8% to 7.0%.

The detailed outlook is presented in the following slide:

The company anticipates an adjusted EBITDA margin between 39.5% and 40.5% for the full year, with capital expenditures projected at $85 million. The effective tax rate is expected to range from 6% to 7%, and the share count for computing adjusted EPS is estimated at 65.0 million.

This outlook aligns with the guidance provided after Q1 results, suggesting that management remains confident in the company’s ability to execute its strategy despite some segment-specific challenges.

Conclusion

Evertec’s Q2 2025 results demonstrate the company’s ability to generate consistent growth across its diverse business segments, with Latin America emerging as a particularly strong performer. While the Business Solutions segment faced margin pressure due to tough year-over-year comparisons, the overall financial health of the company remains strong, with improved debt metrics and solid cash generation.

The maintained full-year outlook suggests management confidence in continued execution for the remainder of 2025, though investors will likely monitor the company’s ability to navigate potential headwinds from tariffs in Latin America and maintain growth momentum across all segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.