These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Evolent Health Inc (NYSE:EVH) released its first quarter 2025 financial results on May 8, showing a significant year-over-year revenue decline while maintaining its full-year guidance. The healthcare company, which provides value-based care delivery solutions, saw its shares rise 6.68% in after-hours trading to $11.50, following a 3.06% gain during the regular session.

The company’s presentation highlighted strategic moves in oncology care management while addressing previously disclosed contracting changes that impacted revenue. Despite the revenue decline, Evolent maintained its full-year guidance, signaling confidence in its growth trajectory for the remainder of 2025.

Quarterly Performance Highlights

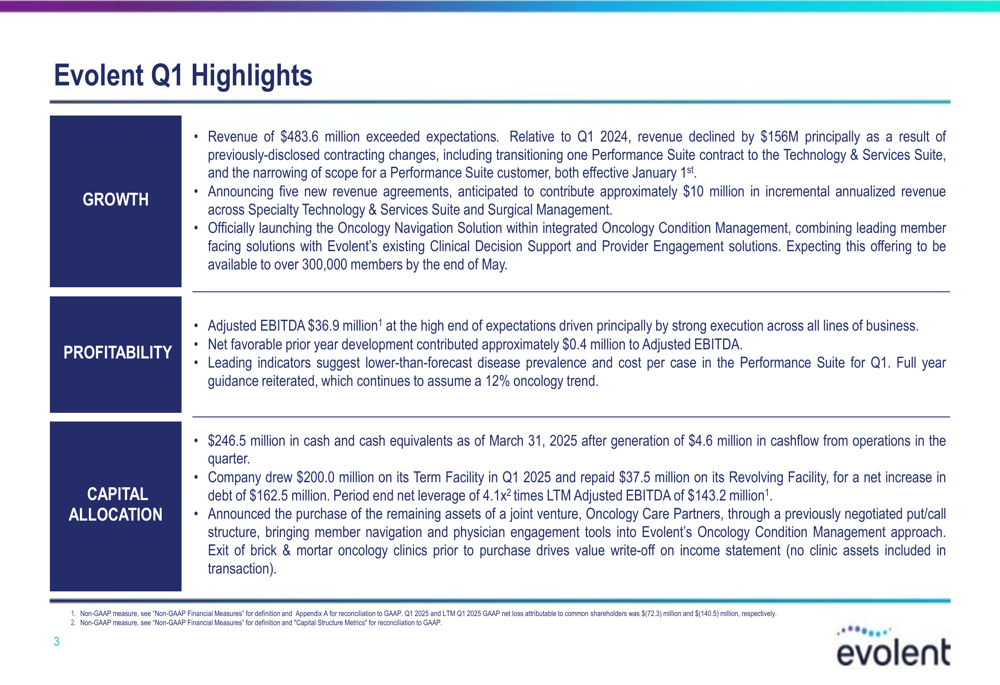

Evolent reported Q1 2025 revenue of $483.6 million, down $156 million year-over-year, attributed to previously disclosed contracting changes. Despite this decline, the company secured five new revenue agreements expected to contribute $10 million in incremental annualized revenue.

Adjusted EBITDA came in at $36.9 million, reaching the high end of the company’s expectations, aided by $0.4 million in net favorable prior-year development. The company noted that leading indicators suggest lower disease prevalence and cost per case in its Performance Suite.

As shown in the following quarterly highlights:

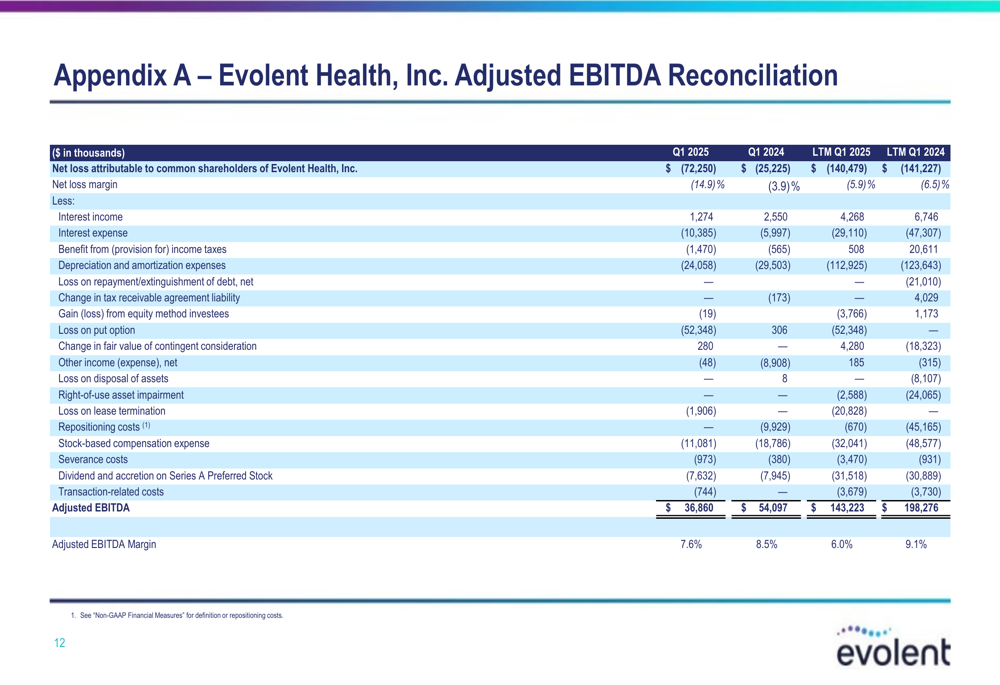

The company’s net loss attributable to common shareholders widened significantly to $72.2 million in Q1 2025 from $25.2 million in Q1 2024, as detailed in the EBITDA reconciliation:

Strategic Initiatives

A key strategic development in the quarter was the launch of Evolent’s Oncology Navigation Solution, which is expected to be available to over 300,000 members by the end of May 2025. The company also announced the purchase of the remaining assets of Oncology Care Partners, integrating member navigation and physician engagement tools into its oncology condition management approach.

This acquisition represents a continuation of Evolent’s focus on expanding its specialty care management capabilities, particularly in oncology. The company noted a brick & mortar oncology clinic exit that drove a value write-off, though no clinic assets were included in the transaction.

Detailed Financial Analysis

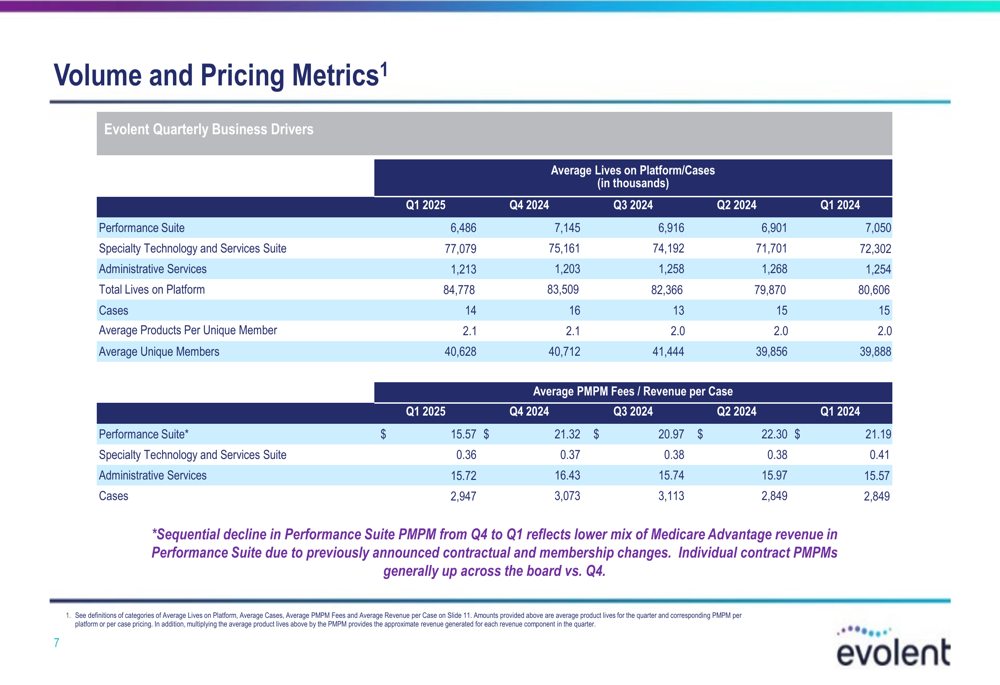

Evolent’s operational metrics showed mixed results across its business segments. Total (EPA:TTEF) lives on the platform increased to 84,778 thousand in Q1 2025 from 80,606 thousand in Q1 2024, primarily driven by growth in the Specialty Technology and Services segment.

However, the Performance Suite segment experienced both decreased membership (from 7,050 thousand to 6,486 thousand) and significantly lower PMPM fees (from $21.19 to $15.57) compared to the same period last year. The company attributed this sequential decline to a lower mix of Medicare Advantage revenue due to contractual and membership changes.

The following volume and pricing metrics illustrate these trends:

Forward-Looking Statements

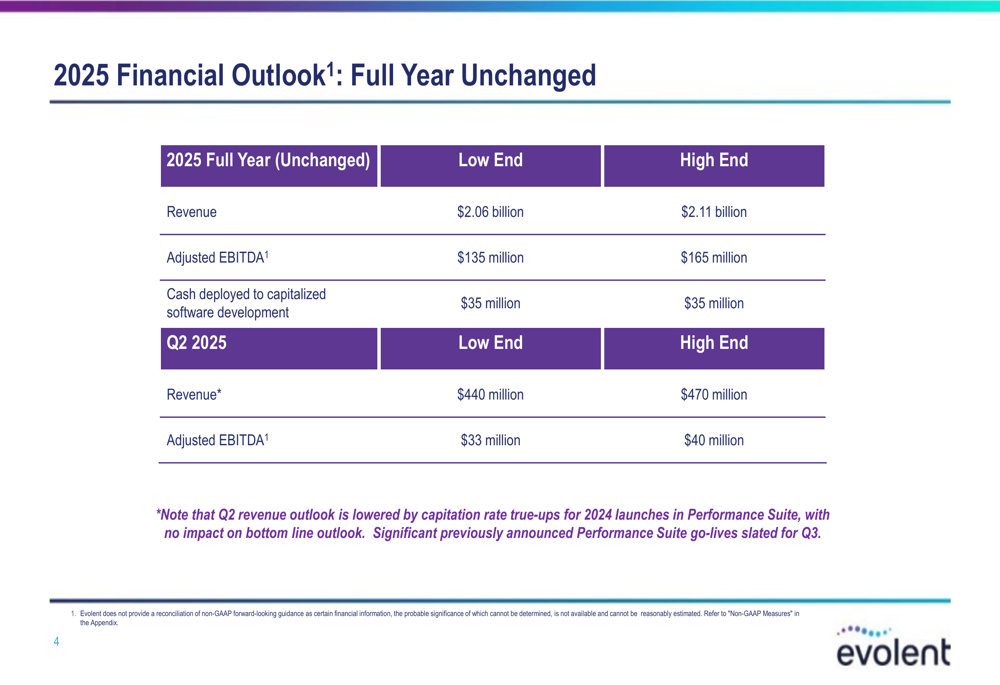

Despite the Q1 revenue decline, Evolent maintained its full-year 2025 guidance, projecting revenue between $2.06 billion and $2.11 billion and adjusted EBITDA between $135 million and $165 million. For Q2 2025, the company expects revenue of $440-470 million and adjusted EBITDA of $33-40 million.

The company noted that its Q2 revenue outlook is impacted by capitation rate true-ups for 2024 launches in the Performance Suite, though this is expected to have no impact on the bottom line. Importantly, Evolent highlighted significant previously announced Performance Suite go-lives slated for Q3, suggesting potential revenue acceleration in the second half of the year.

The financial outlook is summarized in the following guidance table:

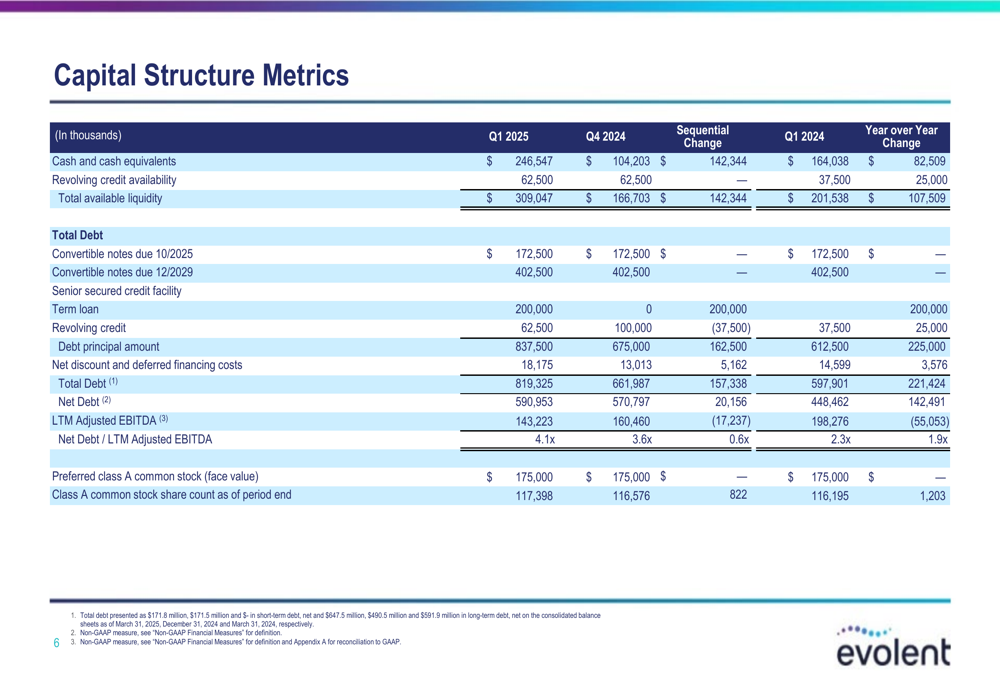

Capital Structure and Liquidity

Evolent’s capital structure saw significant changes in Q1 2025. The company ended the quarter with $246.5 million in cash and cash equivalents, up from $164 million a year earlier. However, total debt increased to $837.5 million from $612.5 million in Q1 2024, resulting in net debt of $591 million.

The company drew $200 million on its Term Facility and repaid $37.5 million on its Revolving Facility during the quarter. This resulted in a net debt to LTM Adjusted EBITDA ratio of 4.1x, a significant increase from 2.3x in Q1 2024, indicating higher leverage.

The capital structure metrics are detailed in the following table:

The company generated $4.6 million in cash flow from operations during the quarter, maintaining its liquidity position despite the increased debt levels. Total available liquidity stood at $309 million as of March 31, 2025.

Conclusion

Evolent Health’s Q1 2025 results reflect a company in transition, managing revenue challenges while advancing strategic initiatives in specialty care management, particularly oncology. While revenue declined significantly year-over-year, the maintained full-year guidance suggests management’s confidence in growth resuming in the second half of 2025.

The increased debt levels and leverage ratio bear watching, as they could limit financial flexibility if operational performance doesn’t improve as anticipated. However, the positive market reaction to the results indicates investors may be focusing on the company’s strategic positioning and maintained guidance rather than the quarterly revenue decline.

As Evolent continues to execute on its oncology-focused strategy and prepares for significant Performance Suite go-lives in Q3, the coming quarters will be critical in determining whether the company can return to growth and improve its financial position.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.