Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Evolent Health Inc (NYSE:EVH) released its second quarter 2025 results on August 7, showing a significant year-over-year revenue decline while maintaining a slightly improved EBITDA margin. The healthcare company’s stock closed at $9.69, up 2.98% on the day, but remains near its 52-week low of $7.06 and far from its high of $33.63.

The presentation comes after a challenging first quarter where Evolent missed EPS forecasts but exceeded revenue expectations. The Q2 results reveal continued pressure on the company’s top line and increasing debt leverage, though management maintains a positive outlook for the remainder of 2025.

Quarterly Performance Highlights

Evolent reported Q2 2025 revenue of $444.3 million, representing a substantial 31.3% decline from $647.1 million in the same period last year. Adjusted EBITDA came in at $37.5 million, down from $51.9 million in Q2 2024, though the adjusted EBITDA margin improved slightly to 8.5% from 8.0% year-over-year.

The company highlighted four new revenue arrangements announced in its Tech & Services and Performance Suite segments during the quarter, bringing the year-to-date total to 11. Management also noted a normalized oncology trend of 10.5% and strong late-stage pipeline activity.

As shown in the following quarterly highlights slide:

Detailed Financial Analysis

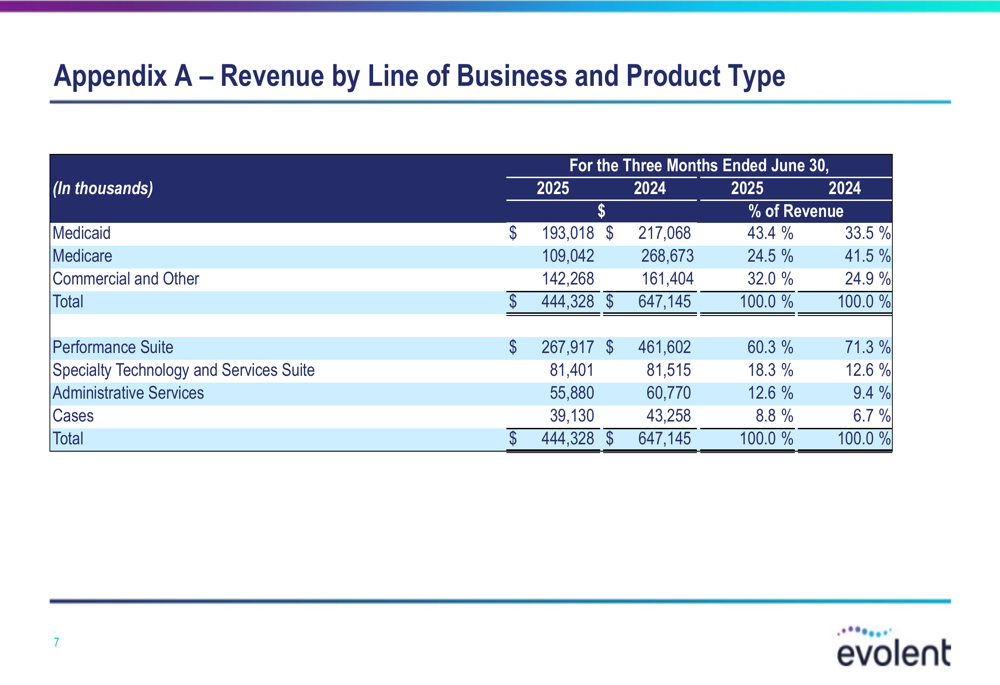

Evolent’s revenue mix underwent significant changes compared to the previous year. Medicaid revenue increased to 43.4% of total revenue (from 33.5% in Q2 2024), while Medicare revenue decreased substantially to 24.5% (from 41.5%). Commercial and other revenue grew to 32.0% of the total (from 24.9%).

The company’s product mix also shifted, with the Performance Suite declining to 60.3% of revenue (from 71.3% in Q2 2024), while the Specialty Technology and Services Suite increased to 18.3% (from 12.6%). Administrative Services grew to 12.6% of revenue (from 9.4%), and Cases increased to 8.8% (from 6.7%).

This revenue breakdown is illustrated in the following slide:

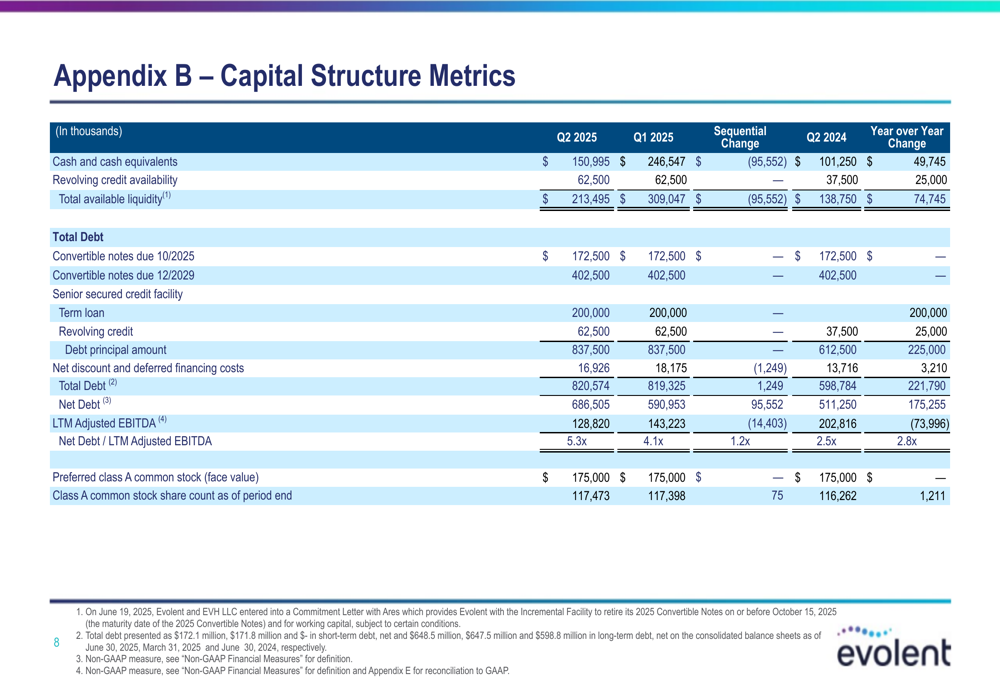

The company’s capital structure metrics reveal increasing financial leverage. Cash and cash equivalents stood at $151.0 million, down from $246.5 million in Q1 2025. Total (EPA:TTEF) debt increased to $820.6 million from $598.8 million in Q2 2024. Most concerning is the Net Debt to LTM Adjusted EBITDA ratio, which rose to 5.3x from 2.5x a year ago, indicating significantly higher leverage.

The following slide details these capital structure metrics:

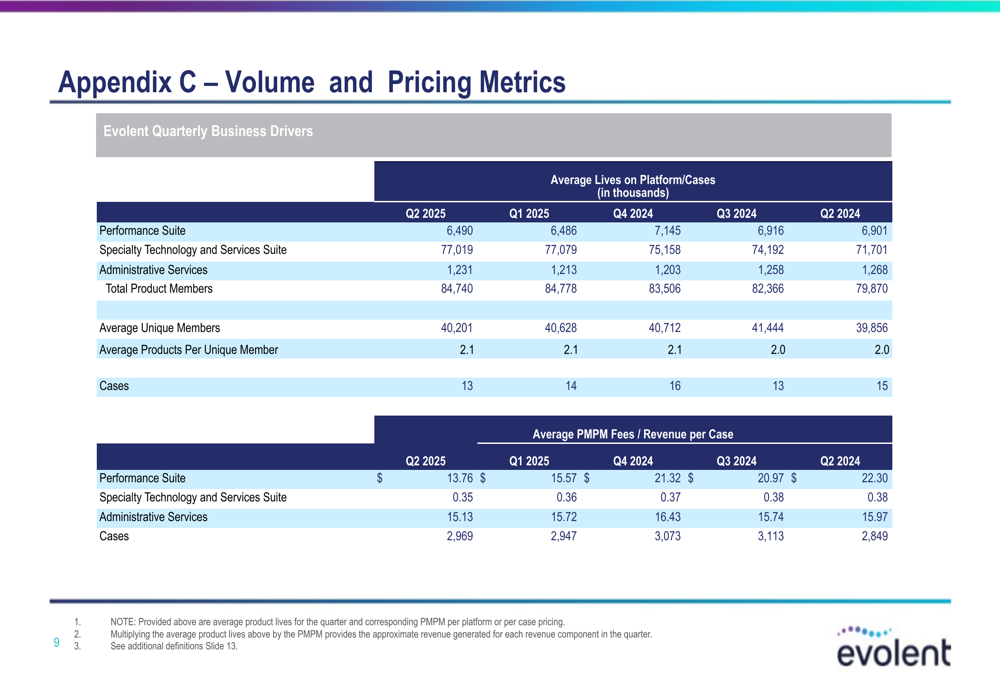

Evolent’s volume metrics remained relatively stable quarter-over-quarter, with Performance Suite lives at 6.49 million and total product members at 84.7 million. However, pricing metrics showed some pressure, with Performance Suite average PMPM fees declining to $13.76 from $15.57 in Q1 2025.

The volume and pricing metrics are presented in this slide:

Adjusted EBITDA Analysis

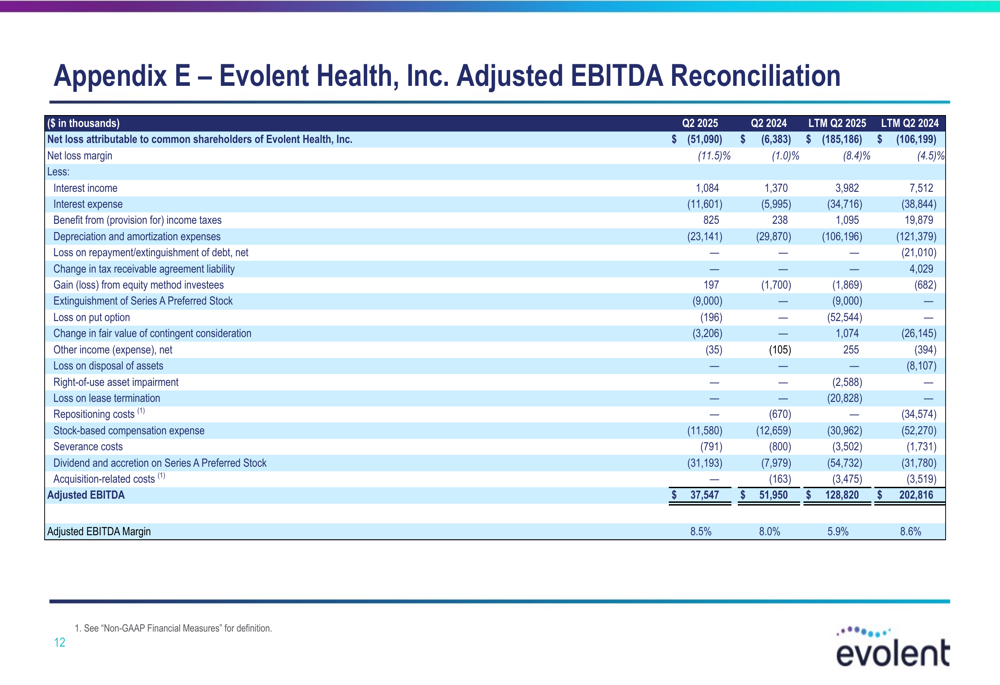

The reconciliation of net loss to Adjusted EBITDA reveals a widening gap between GAAP and non-GAAP results. The company reported a net loss attributable to common shareholders of $51.1 million in Q2 2025, compared to a loss of $6.4 million in Q2 2024. After adjustments for interest, taxes, depreciation, amortization, and other items, Adjusted EBITDA reached $37.5 million.

On a last twelve months (LTM) basis, the company’s Adjusted EBITDA declined significantly to $128.8 million from $202.8 million in the prior year period, representing a 36.5% decrease. This decline in LTM Adjusted EBITDA is a key factor in the company’s rising leverage ratio.

The detailed reconciliation is shown in the following slide:

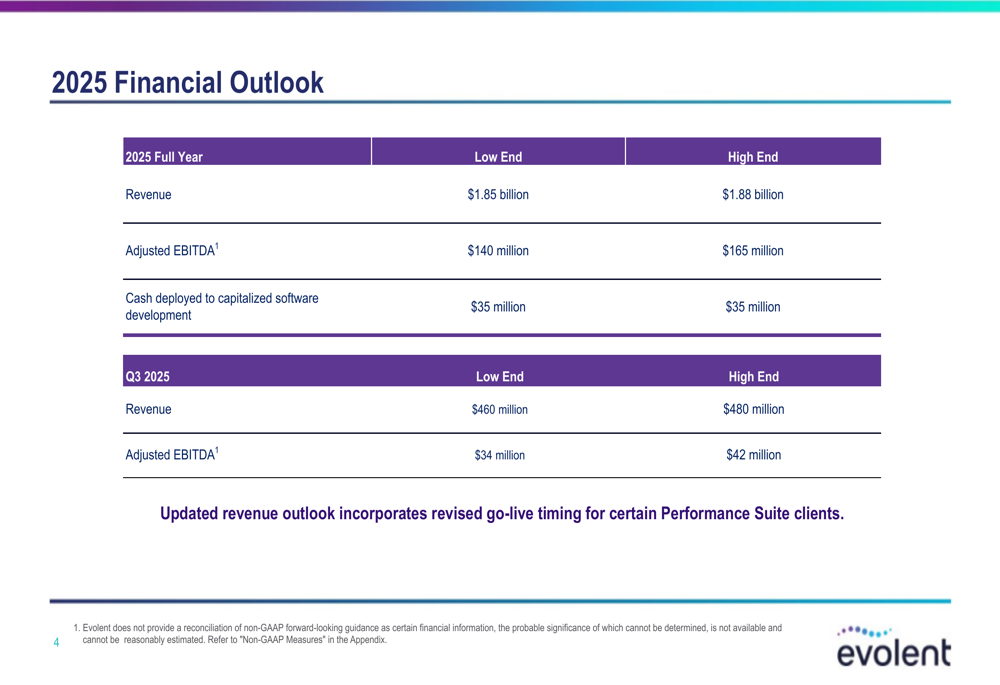

Forward-Looking Statements

Despite the challenging quarterly results, Evolent maintained a positive outlook for the remainder of 2025. The company projects full-year revenue between $1.85 billion and $1.88 billion, with Adjusted EBITDA between $140 million and $165 million. For Q3 2025, Evolent expects revenue of $460-480 million and Adjusted EBITDA of $34-42 million.

The company noted that its updated revenue outlook incorporates revised go-live timing for certain Performance Suite clients, suggesting some implementation delays that could affect near-term results.

The financial outlook is presented in this slide:

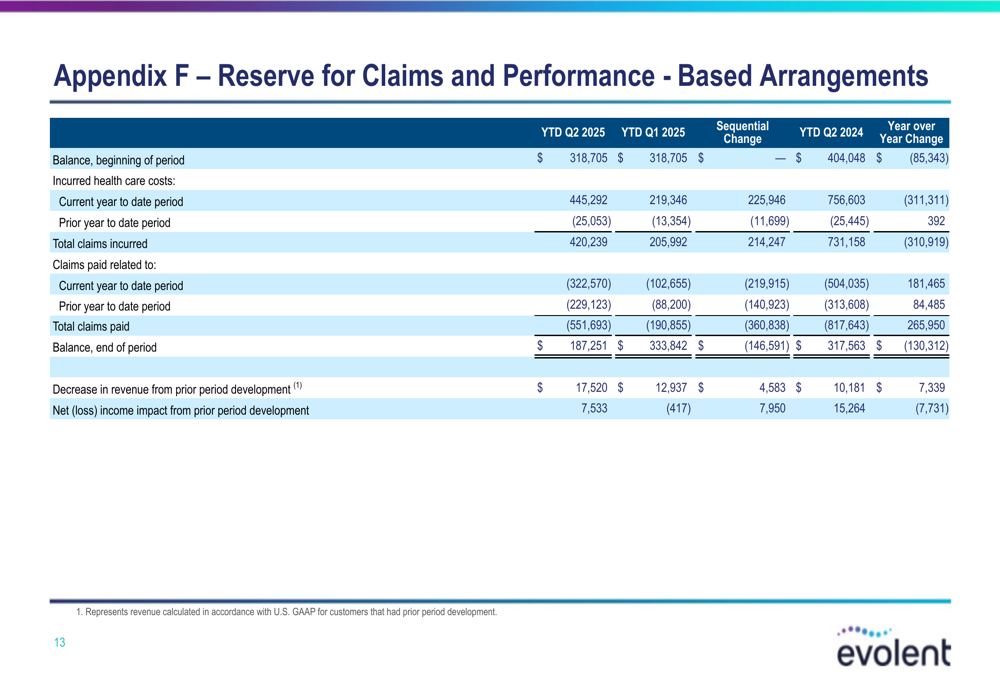

Operational Metrics

Evolent’s reserve for claims and performance-based arrangements showed a significant decrease, with the end-of-period balance falling to $187.3 million in Q2 2025 from $317.6 million in Q2 2024. This decline reflects lower incurred healthcare costs of $420.2 million (versus $731.2 million in the prior year period) and reduced claims payments.

The company reported a $17.5 million decrease in revenue from prior period development, though the net income impact was positive at $7.5 million. These figures suggest some favorable development in the company’s medical cost estimates.

The reserves data is detailed in the following slide:

Market Outlook

Evolent Health faces significant challenges as it navigates declining revenue and increasing debt leverage. The shift in revenue mix toward Medicaid and away from Medicare represents a strategic pivot that may affect margins and growth prospects. While the company maintains a positive outlook for the remainder of 2025, the substantial year-over-year declines in revenue and Adjusted EBITDA raise questions about long-term growth trajectory.

The stock’s performance reflects these concerns, trading near its 52-week low despite the slight uptick following the earnings release. Investors will likely focus on whether the company can stabilize its revenue, improve its leverage ratio, and successfully execute on its pipeline opportunities in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.