NHL signs licensing deals with prediction-market startups Kalshi and Polymarket - WSJ

Introduction & Market Context

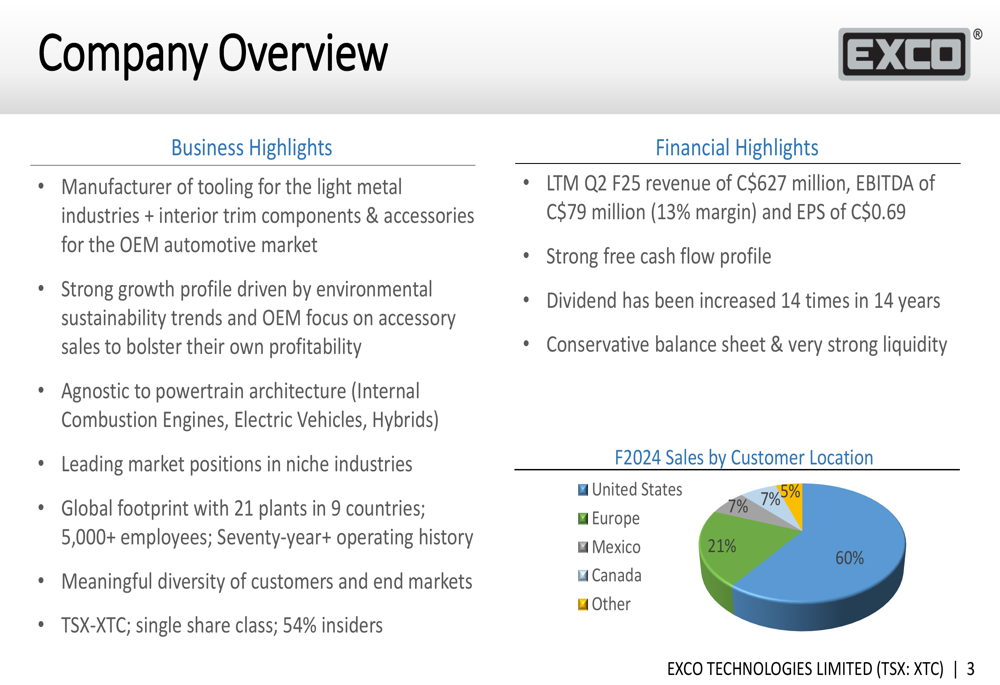

Exco Technologies Limited (TSX:XTC), a global manufacturer of tooling for light metal industries and automotive interior components, presented its investor update on May 1, 2025, highlighting the company’s financial performance through the second quarter of fiscal year 2025. The presentation showcased Exco’s diversified business model and strategic positioning in markets experiencing growing demand for aluminum components.

Trading at C$5.70 as of April 30, 2025, Exco’s stock has remained relatively stable, reflecting the company’s consistent operational performance despite facing industry-wide challenges including labor cost pressures in Mexico and fluctuating vehicle production volumes.

Executive Summary

Exco’s presentation emphasized its strong financial foundation with LTM Q2 F25 revenue of C$627 million and EBITDA of C$79 million, representing a 13% margin. The company’s business is evenly split between two segments: Automotive Solutions (51% of revenue) and Casting & Extrusion (49% of revenue), with the latter delivering a stronger EBITDA margin of 16% compared to 11% for Automotive Solutions.

The company highlighted its global manufacturing footprint spanning 21 locations across 9 countries with over 5,000 employees, positioning it to serve diverse markets and customers. Notably, Exco has maintained a strong balance sheet with decreasing leverage, falling from 1.7x in F2022 to 0.9x in F2024, while consistently increasing dividends for 14 consecutive years.

As shown in the following company overview:

Business Segment Analysis

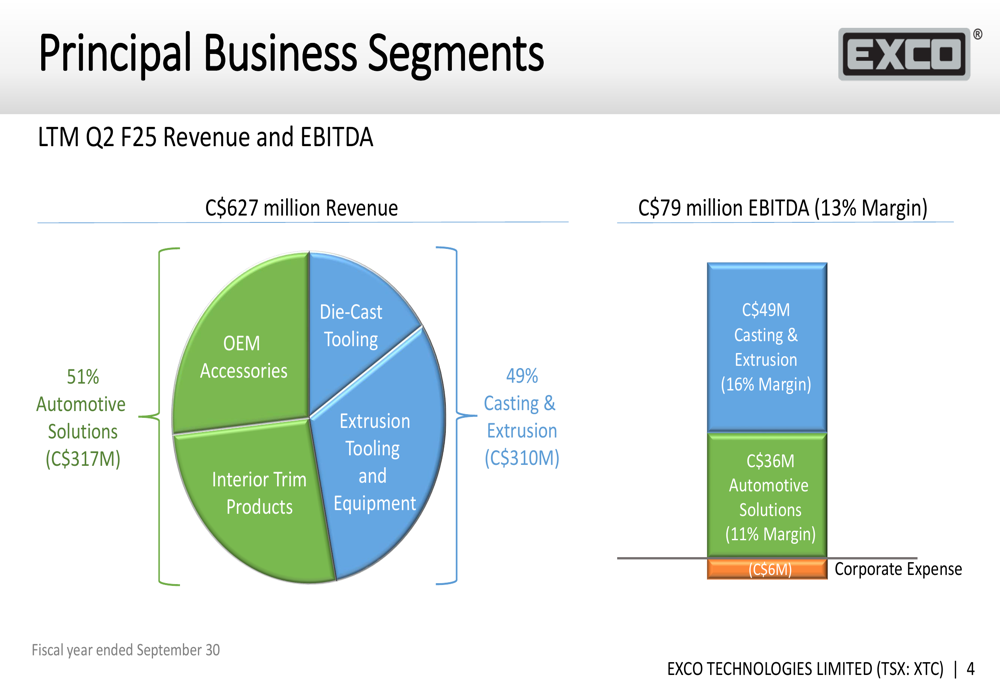

Exco’s business is nearly evenly divided between its two primary segments, with distinct financial profiles and market dynamics. The Casting & Extrusion segment, contributing 49% of revenue (C$310 million), generates a higher EBITDA margin of 16% (C$49 million), while the Automotive Solutions segment represents 51% of revenue (C$317 million) with an 11% EBITDA margin (C$36 million).

The balanced business model is illustrated in the following breakdown:

The company benefits from significant customer diversification, with its top OEM automotive customer accounting for only 9% of consolidated revenues, and the top five OEMs representing 40%. Approximately 33% of revenues come from extrusion tooling and related capital equipment serving diverse non-automotive markets, providing stability against automotive industry fluctuations.

Strategic Market Positioning

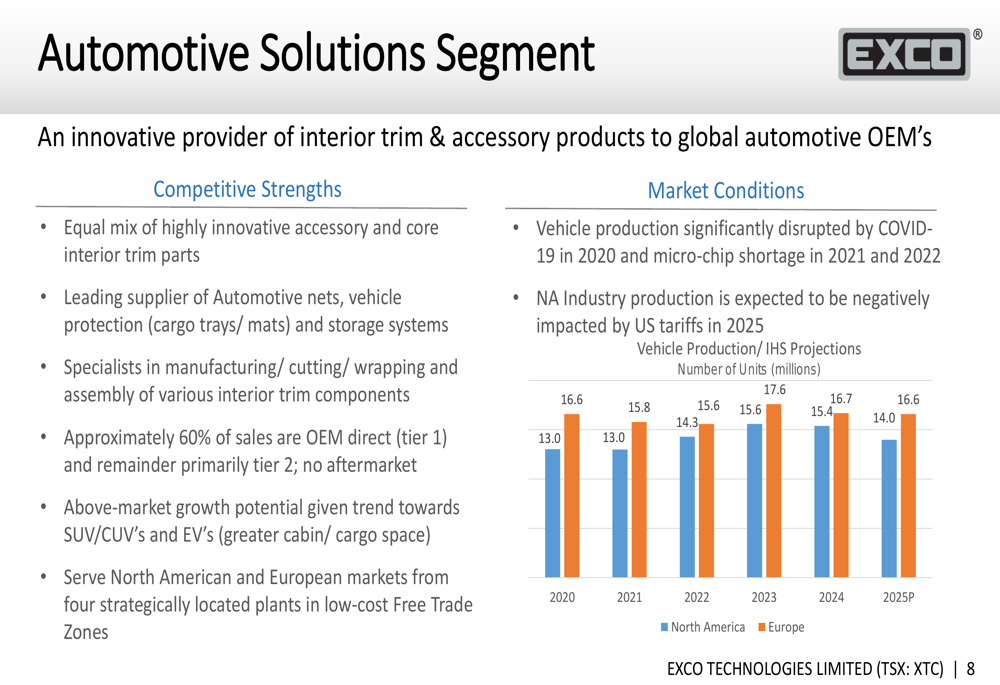

Exco’s Automotive Solutions segment manufactures a mix of innovative accessories and core interior trim parts, with 60% of sales going directly to OEMs. The segment is positioned to benefit from the industry trend toward SUVs/CUVs and electric vehicles, though management noted that North American production is expected to be negatively impacted by US tariffs in 2025.

The following chart illustrates vehicle production projections for North America and Europe:

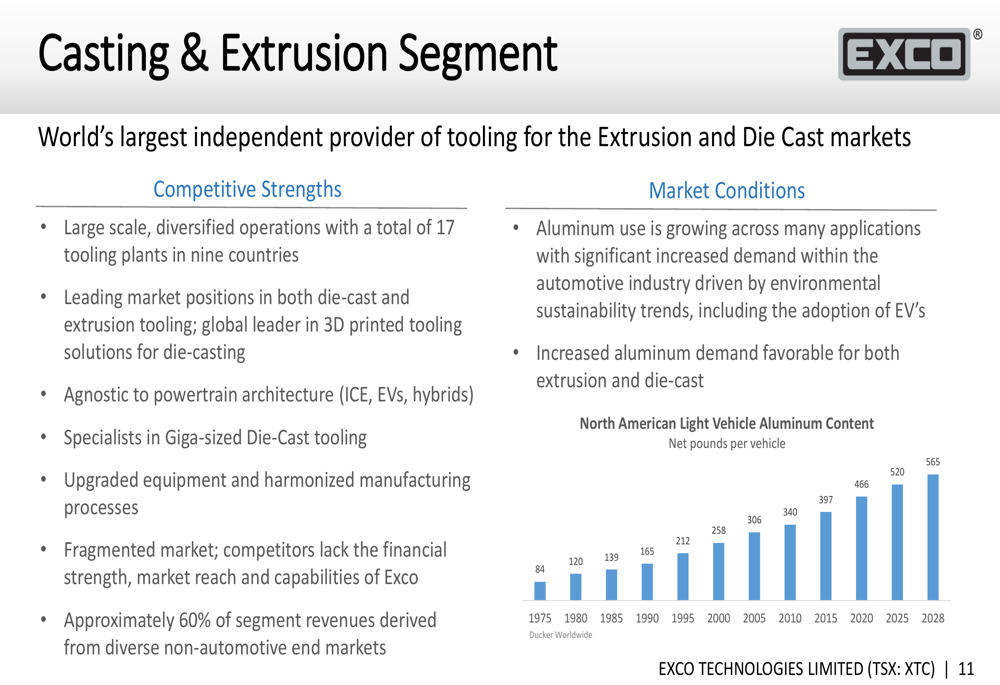

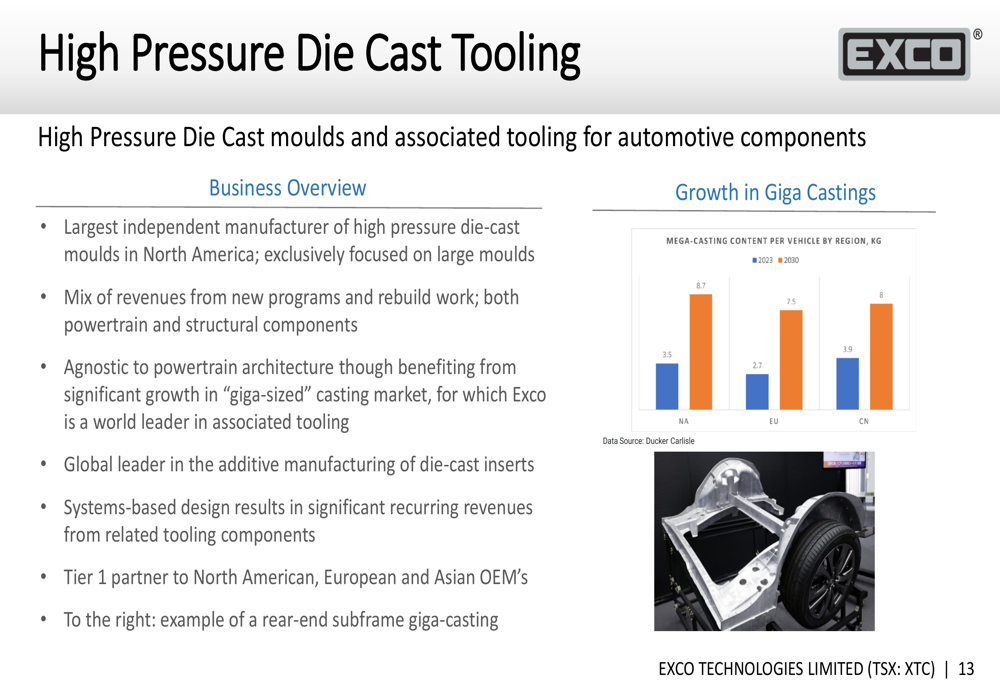

In the Casting & Extrusion segment, Exco is capitalizing on the increasing use of aluminum across various applications, particularly in the automotive sector. The company highlighted its position as the largest independent manufacturer of high-pressure die-cast moulds in North America, with expertise in producing "giga-sized" castings that are increasingly important for electric vehicle manufacturing.

The growth in aluminum content per vehicle is demonstrated in this chart:

Exco’s strategic advantage in the growing mega-casting market is illustrated by projected growth across regions:

Detailed Financial Analysis

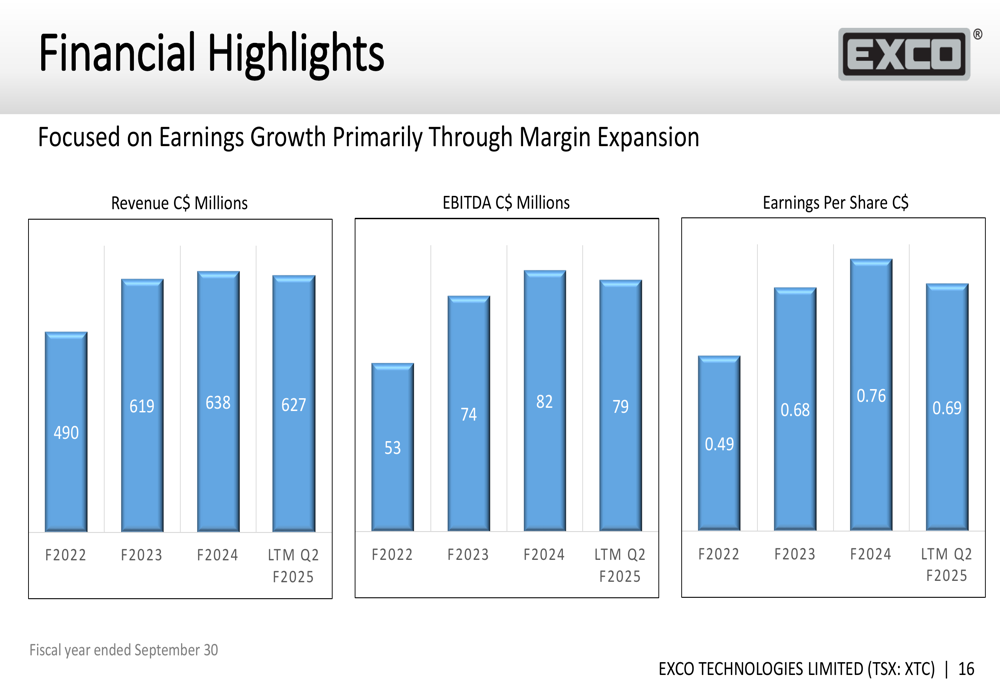

Exco’s financial performance shows steady growth from fiscal 2022 through 2024, with a slight moderation in the LTM Q2 F25 period. Revenue increased from C$490 million in F2022 to C$638 million in F2024, before slightly decreasing to C$627 million in LTM Q2 F25. Similarly, EBITDA grew from C$53 million in F2022 to C$82 million in F2024, then moderated to C$79 million in LTM Q2 F25.

Earnings per share followed a similar pattern, rising from C$0.49 in F2022 to C$0.76 in F2024, before decreasing to C$0.69 in LTM Q2 F25. These trends are visualized in the following financial highlights:

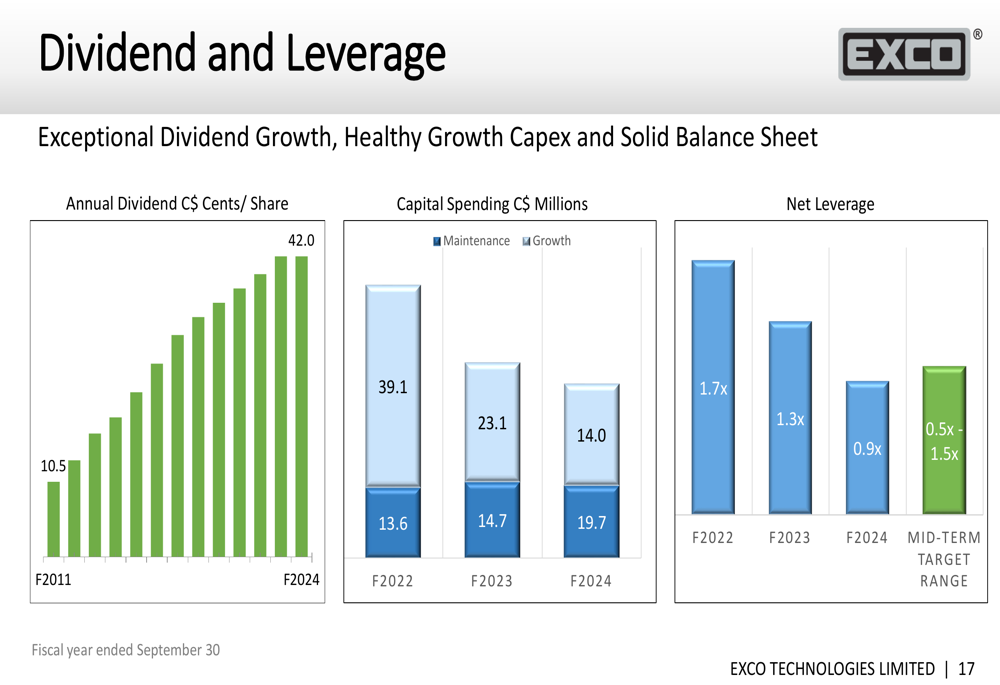

The company has maintained a strong dividend growth trajectory, increasing from 10.5 cents per share in F2011 to 42.0 cents per share in F2024, representing 14 consecutive years of dividend increases. Capital spending has been strategically managed, with growth capital declining from C$39.1 million in F2022 to C$14.0 million in F2024, while maintenance capital has increased from C$13.6 million to C$19.7 million over the same period.

Net leverage has improved significantly, decreasing from 1.7x in F2022 to 0.9x in F2024, now within the company’s mid-term target range of 0.5x to 1.5x. These financial metrics are illustrated in the following chart:

Forward-Looking Statements

Looking ahead, Exco is well-positioned to benefit from several industry trends, particularly the increasing use of aluminum in vehicles and the growth of mega-castings in electric vehicle manufacturing. The company’s agnostic approach to powertrain architecture allows it to capitalize on both traditional internal combustion engine vehicles and the growing electric vehicle market.

In its recent earnings call for Q2, management indicated that the company expects higher margins through 2026 due to capacity additions and efficiency initiatives. The company remains focused on reducing costs and improving manufacturing efficiencies, particularly in response to rising labor costs in Mexico. Executives expressed confidence in reaching a segment margin of 15% by 2026 for the Automotive Solutions segment.

Capital expenditures are anticipated to be lower than the previously projected C$49 million budget, as the company carefully manages investments to ensure optimal returns. This aligns with the reduced growth capital spending shown in the presentation.

Competitive Industry Position

Exco maintains leading market positions in both die-cast and extrusion tooling, with the ability to produce the increasingly important giga-sized die-cast tooling required for modern vehicle manufacturing. The company’s global footprint enables it to serve customers across North America, Europe, and Asia, providing a competitive advantage in an industry increasingly focused on localized supply chains.

The Extrusion Tooling and Equipment division benefits from diverse end-market exposure, with approximately 60% of segment revenue coming from non-automotive sectors, including building and construction, consumer durables, electrical, and machinery equipment. This diversification provides stability against automotive industry cyclicality.

In the High Pressure Die Cast Tooling business, Exco is the largest independent manufacturer in North America exclusively focused on large moulds. The company’s system-based design approach results in significant recurring revenues, while its leadership in additive manufacturing die-cast inserts provides technological differentiation.

As vehicle manufacturers continue to increase aluminum content and adopt mega-castings, Exco’s specialized expertise positions it to capture growth opportunities across both traditional and electric vehicle platforms.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.