BofA warns Fed risks policy mistake with early rate cuts

Expand Energy Corp (NYSE:EXE) reported strong first-quarter 2025 results on April 29, with production exceeding expectations and significant progress on synergy capture following its recent merger. The company’s stock closed at $107.11 on the day of the announcement, up 0.34% from the previous close.

Quarterly Performance Highlights

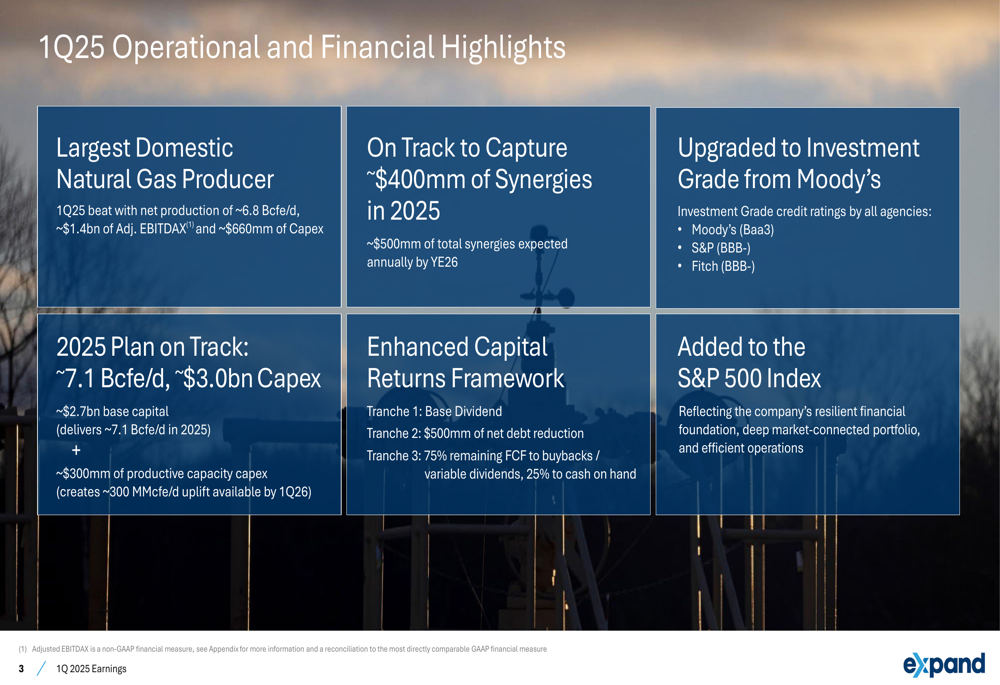

Expand Energy, now the largest domestic natural gas producer in the United States, reported net production of approximately 6.8 Bcfe/d for Q1 2025, along with Adjusted EBITDAX of approximately $1.4 billion and capital expenditures of around $660 million. These results exceeded expectations and demonstrated the company’s operational efficiency.

As shown in the following operational and financial highlights from the presentation:

The company achieved several significant milestones during the quarter, including an upgrade to investment grade from Moody’s, completing the trifecta with all three major rating agencies now assigning investment grade ratings. Additionally, Expand Energy was added to the S&P 500 Index, reflecting its enhanced scale and financial stability.

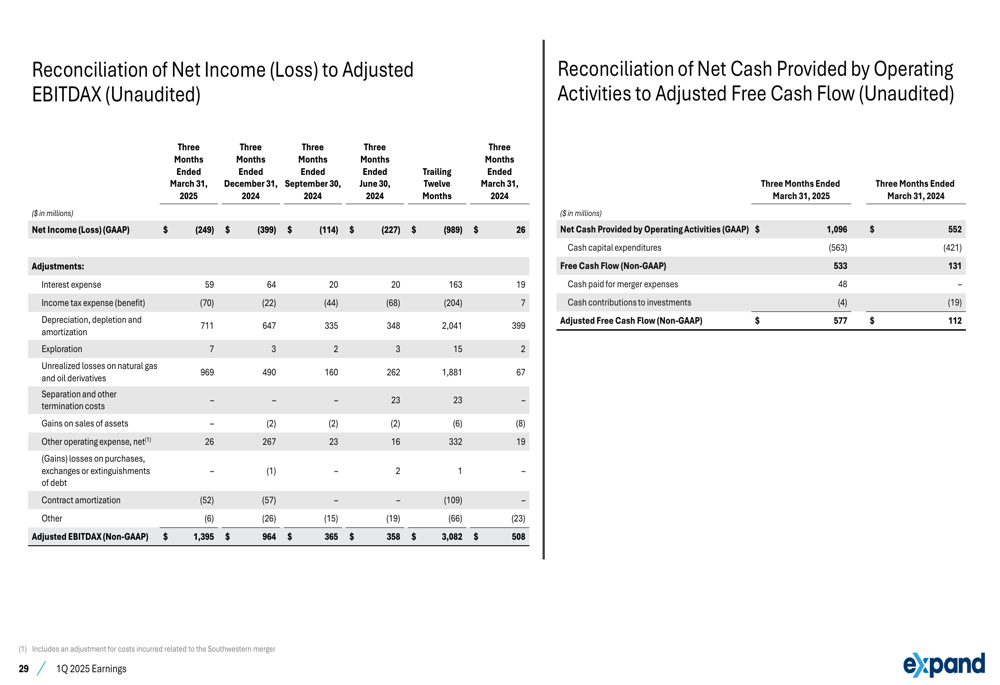

Net income for the quarter was negative at $(249) million, while Adjusted EBITDAX reached $1,395 million, as detailed in the company’s reconciliation:

Strategic Initiatives & Synergy Capture

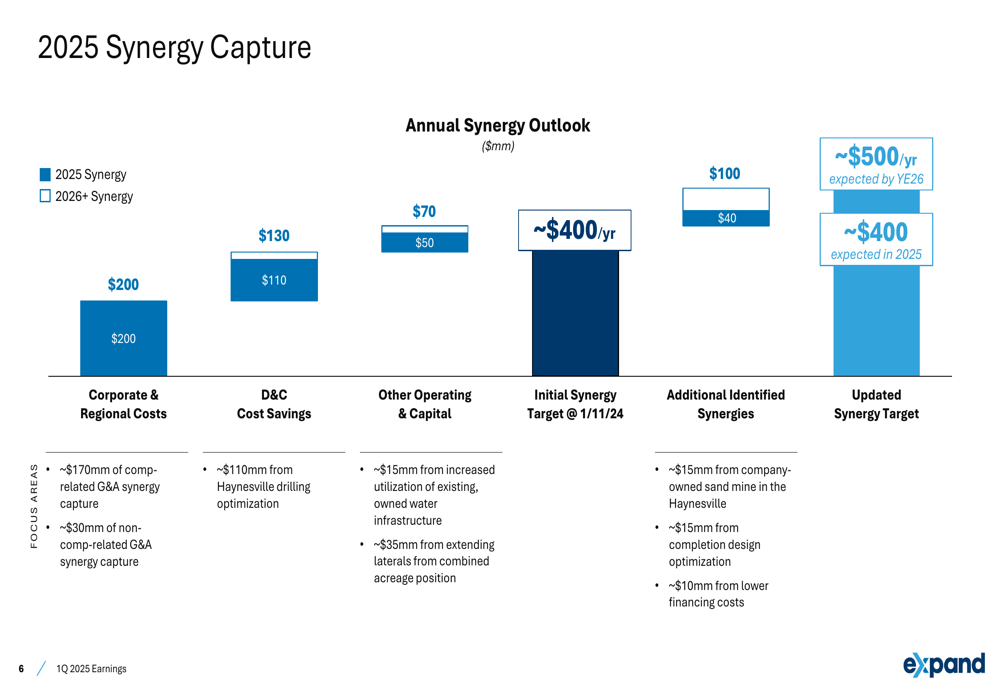

A key focus for Expand Energy following its merger has been capturing operational and financial synergies. The company reported being on track to capture approximately $400 million of synergies in 2025, with expectations to reach approximately $500 million annually by year-end 2026.

The following chart details the breakdown of these synergy initiatives:

The synergy capture spans multiple areas, with significant contributions from corporate and regional cost reductions ($200 million), drilling and completion cost savings ($110 million), and various operational improvements. The company reduced its gross debt by approximately $440 million in Q1 2025, bringing the total debt reduction to approximately $1 billion since the merger closed.

Financial Position & Capital Allocation

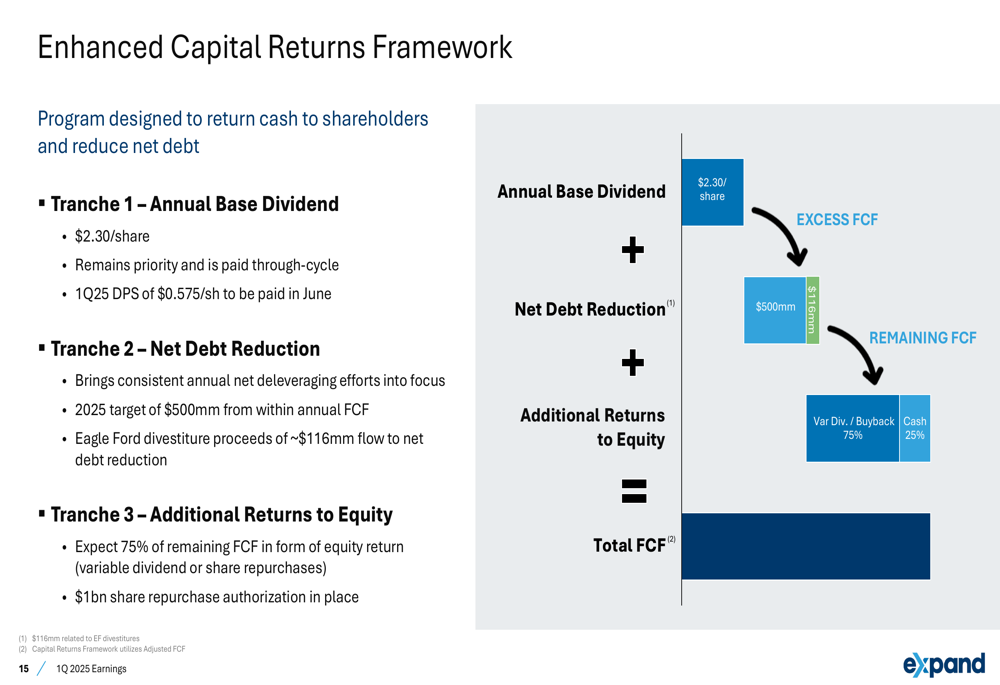

Expand Energy outlined an enhanced capital returns framework that balances shareholder returns with strengthening the company’s balance sheet. The framework includes a base annual dividend of $2.30 per share, a targeted net debt reduction of $500 million in 2025, and additional returns to equity through variable dividends or share repurchases.

The company’s capital allocation strategy is illustrated in the following slide:

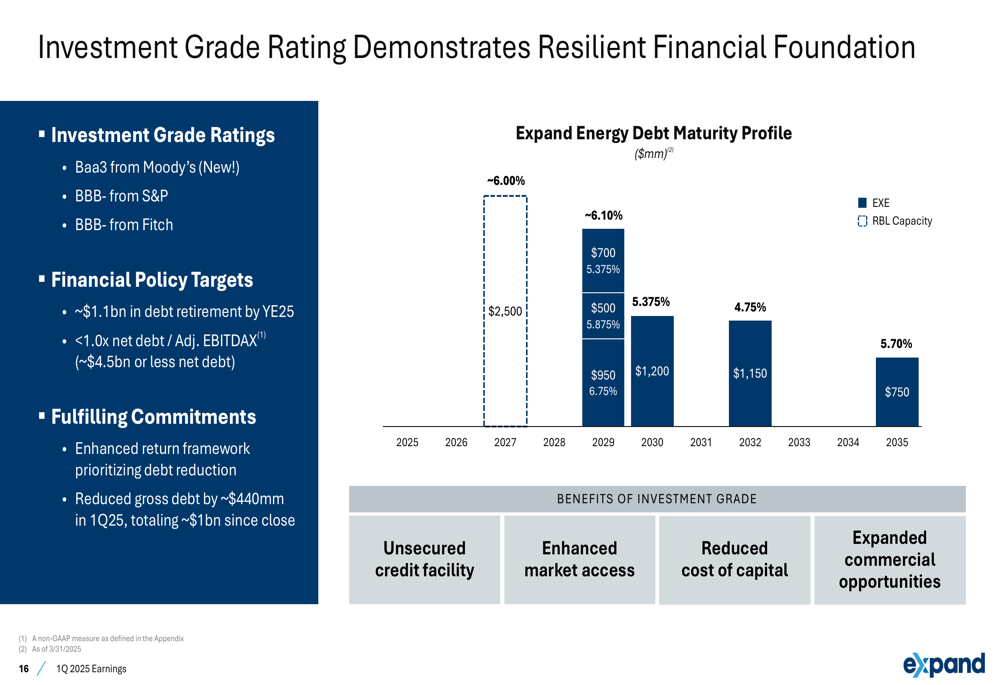

The investment grade ratings from all three major agencies (Moody’s, S&P, and Fitch) provide Expand Energy with financial flexibility and lower borrowing costs. The company aims to reduce its net debt to below $4.5 billion by year-end 2025, targeting a net debt to Adjusted EBITDAX ratio of less than 1.0x.

As shown in the following debt maturity profile and financial foundation overview:

Production Outlook & Market Positioning

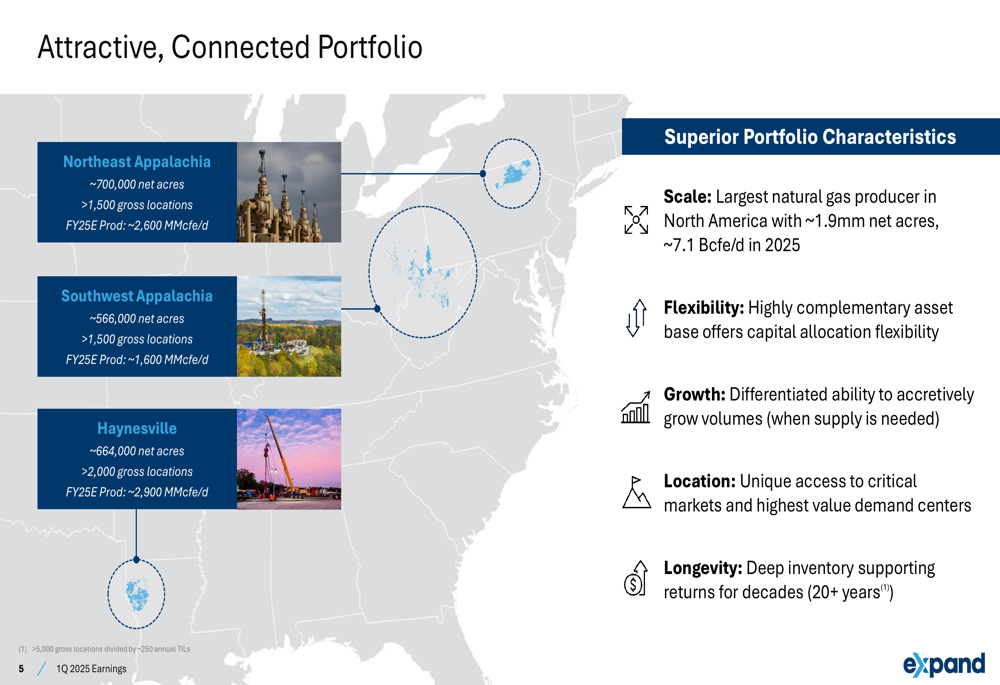

Expand Energy’s operations span three key natural gas basins: Northeast Appalachia, Southwest Appalachia, and Haynesville. This geographic diversity provides the company with strategic flexibility and access to premium markets.

The company’s asset portfolio and production outlook are detailed in the following slide:

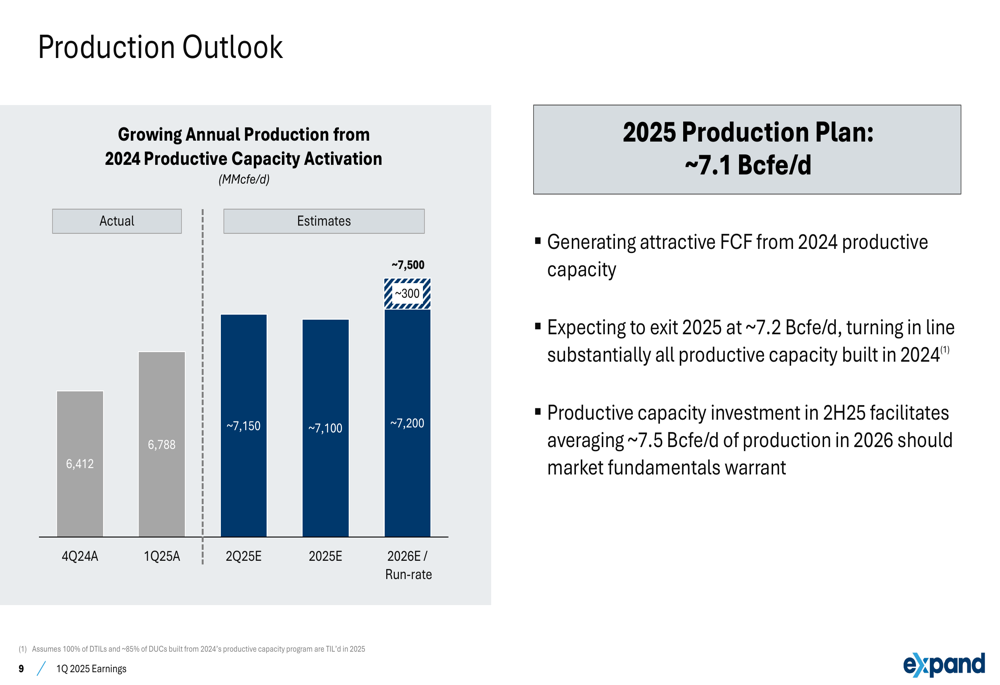

For 2025, Expand Energy is targeting production of approximately 7.1 Bcfe/d, with capital expenditures of approximately $3.0 billion. This includes approximately $2.7 billion in base capital and $300 million in productive capacity capital that will create approximately 300 MMcfe/d of additional production capacity available by Q1 2026.

The production trajectory is illustrated in the following chart:

Expand Energy is strategically positioned to benefit from growing demand for liquefied natural gas (LNG) exports. The company is currently selling approximately 2 Bcf/d to LNG export facilities and has approximately 2.5 Bcf/d of deliverability to the LNG corridor. With U.S. LNG capacity expected to grow from the current 14.9 Bcf/d to approximately 29 Bcf/d, Expand Energy sees significant opportunities in this market.

Forward-Looking Statements

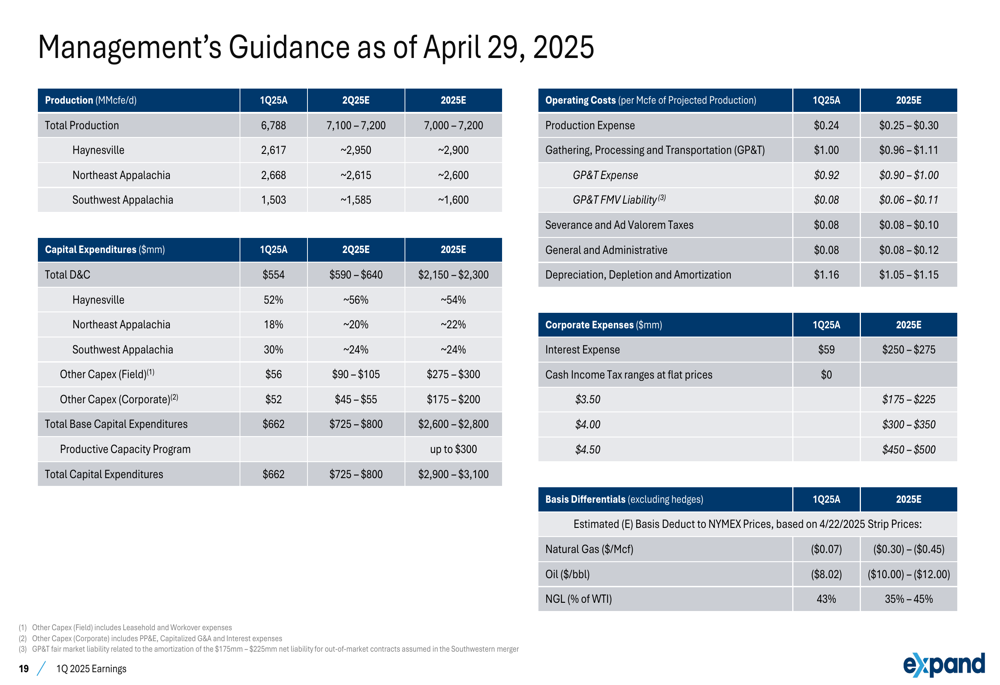

Management’s guidance for Q2 2025 and full-year 2025 indicates continued strong performance, with Q2 production expected to reach 7,100-7,200 MMcfe/d. The company anticipates relatively flat production through the second half of 2025, with an exit rate of approximately 7.2 Bcfe/d.

As detailed in the management guidance slide:

Expand Energy maintains that the fundamentals-driven mid-cycle price of $3.50-$4.00 for natural gas remains intact despite recent market volatility. The company’s hedging strategy is designed to preserve upside potential as prices strengthen while providing downside protection.

The company’s optimized maintenance production strategy aims to maximize free cash flow at these mid-cycle prices, with a production target of approximately 7.5 Bcfe/d through the cycle. This approach allows Expand Energy to adjust its capital allocation based on market conditions, increasing production when prices are above the mid-cycle range and reducing activity when prices fall below target levels.

With its strategic asset portfolio, financial strength, and operational efficiency, Expand Energy appears well-positioned to deliver on its 2025 objectives while creating long-term value for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.