BofA warns Fed risks policy mistake with early rate cuts

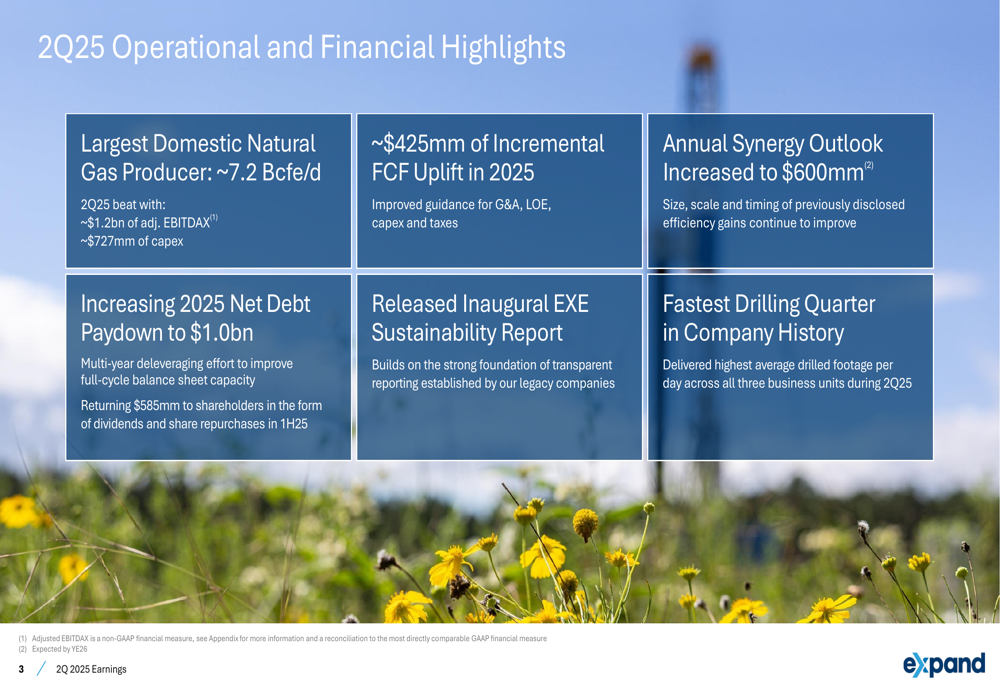

Expand Energy Corp (NYSE:EXE) presented its second-quarter 2025 earnings on July 29, showcasing record drilling performance and increased merger synergies while trading at $98.75 in after-hours, up 0.63% following the release. The natural gas producer reported adjusted EBITDAX of approximately $1.2 billion on capital expenditures of $727 million for the quarter.

Quarterly Performance Highlights

Expand Energy maintained its position as the largest domestic natural gas producer with approximately 7.2 Bcfe/d of production during the quarter. The company returned $585 million to shareholders through dividends and share repurchases in the first half of 2025, while simultaneously pursuing a deleveraging strategy.

"We’re increasing our 2025 net debt paydown to $1.0 billion as part of our multi-year deleveraging effort to improve full-cycle balance sheet capacity," the company stated in its presentation, highlighting its focus on financial strength alongside shareholder returns.

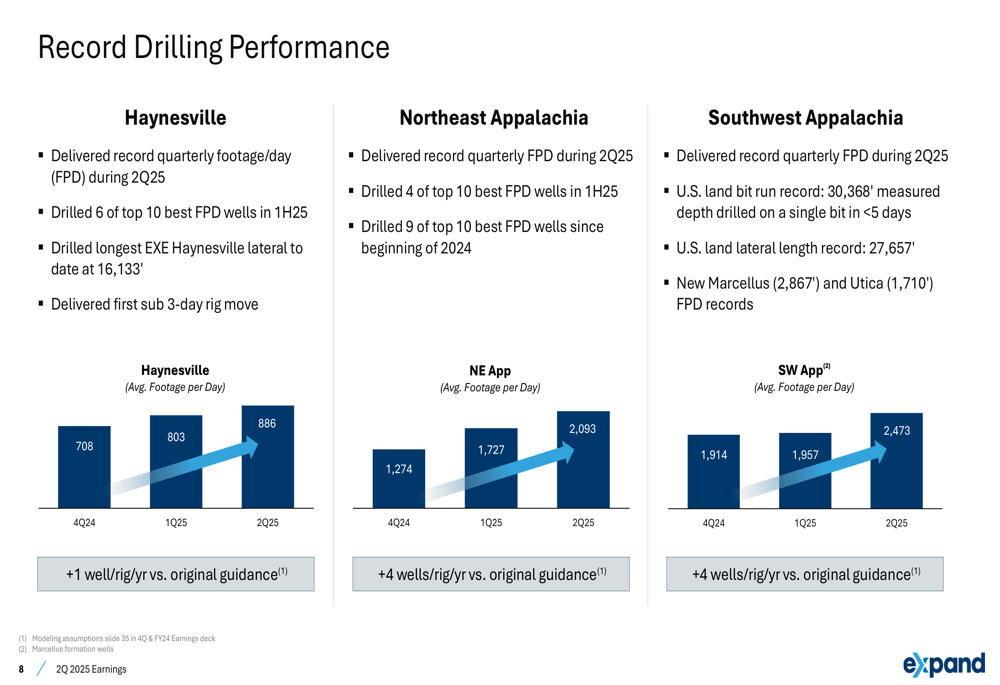

The quarter marked the fastest drilling period in company history, with record footage-per-day metrics across all three business units.

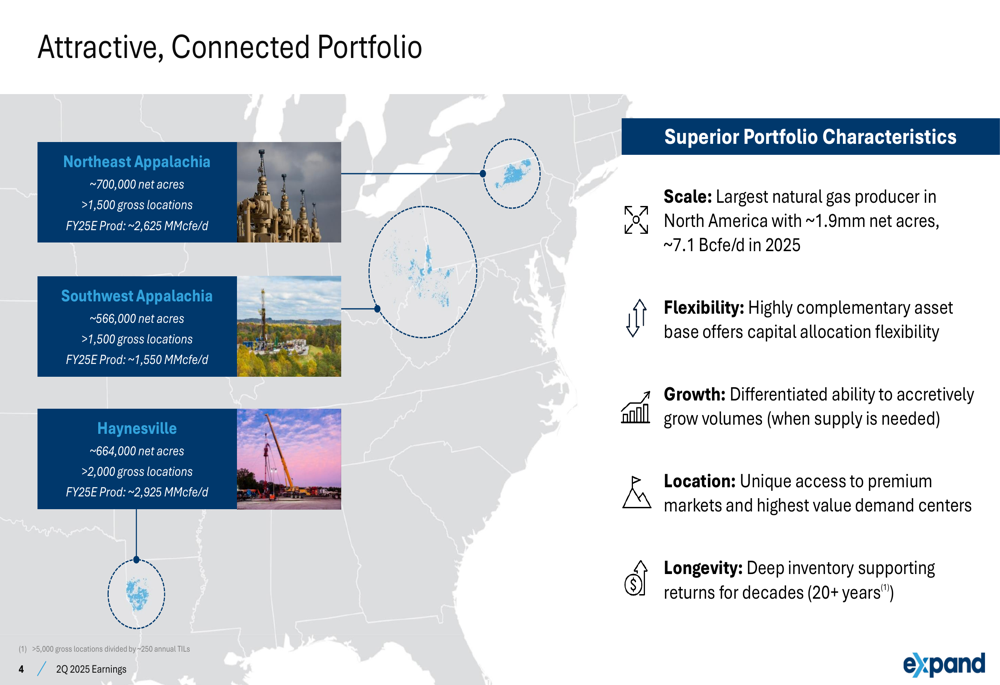

Expand Energy’s portfolio spans three major natural gas basins: Northeast Appalachia (~700,000 net acres), Southwest Appalachia (~566,000 net acres), and Haynesville (~664,000 net acres). This connected asset base provides the company with significant scale and flexibility in capital allocation.

As shown in the following portfolio overview, the company has over 5,000 gross drilling locations supporting more than 20 years of inventory at current development rates:

Financial Outlook and Synergies

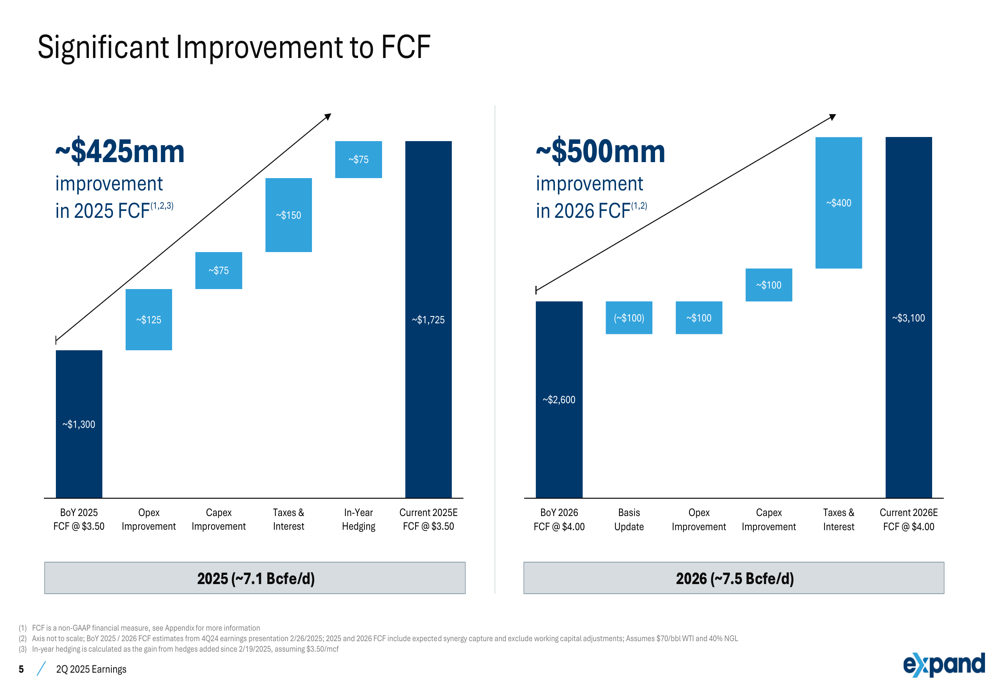

A key highlight from the presentation was the significant improvement in free cash flow projections. Expand Energy increased its 2025 FCF forecast by approximately $425 million, citing improvements in operating expenses, capital expenditures, taxes, interest, and in-year hedging. For 2026, the company projects an additional $500 million improvement in FCF.

The following chart illustrates these substantial improvements to the company’s cash flow outlook:

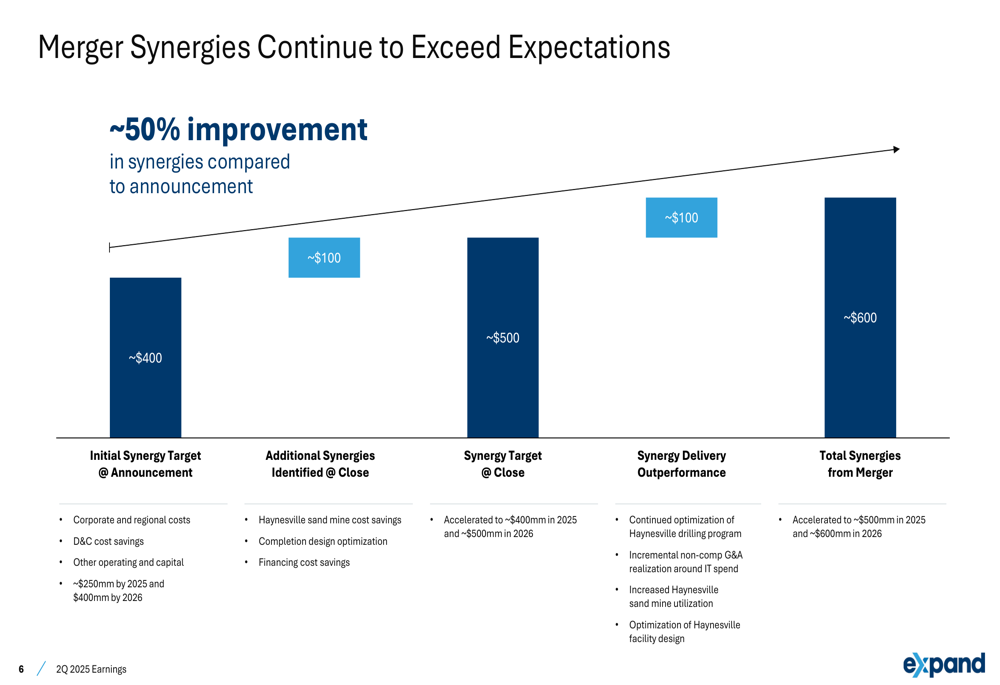

Merger synergies have significantly exceeded initial expectations, with the target now increased to $600 million annually—a 50% improvement compared to the $400 million initially announced. The company expects to realize approximately $500 million of these synergies in 2025 and the full $600 million in 2026.

As shown in the following synergy evolution chart, the improvements came from multiple sources including Haynesville sand mine optimization, completion design improvements, and reduced G&A expenses:

Operational Achievements

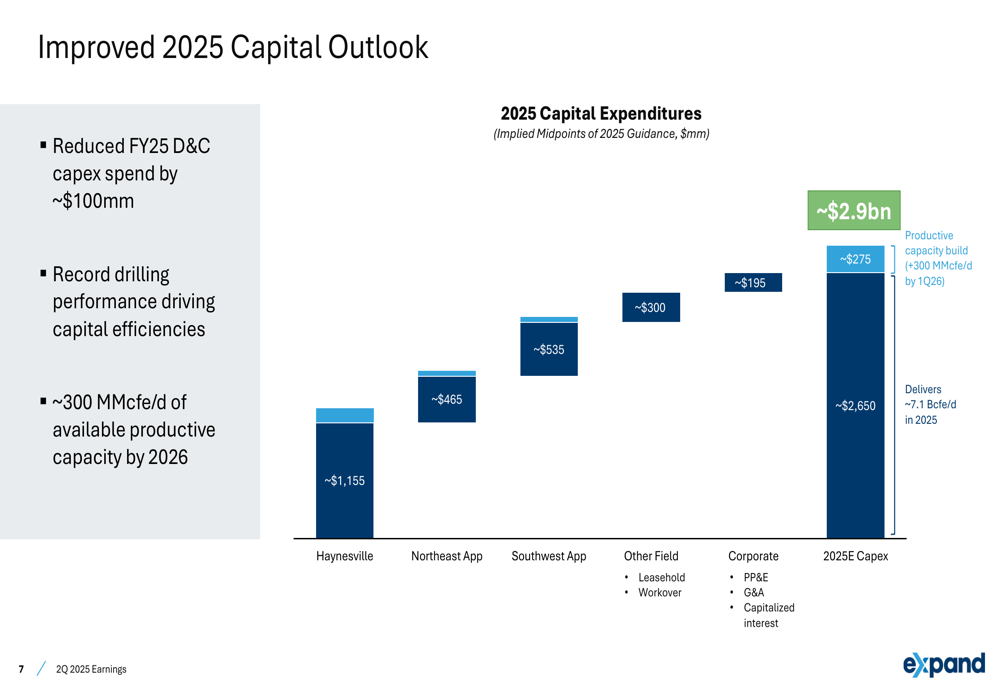

Expand Energy reduced its full-year 2025 drilling and completion capital expenditures by approximately $100 million while maintaining production guidance. The company’s total 2025 capital expenditure guidance now stands at approximately $2.65 billion, which is expected to deliver average production of 7.1 Bcfe/d for the year.

The following capital expenditure breakdown shows the allocation across the company’s operating regions:

Record drilling performance was achieved across all three operating regions during Q2 2025. In the Haynesville, the company drilled its longest lateral to date at 16,133 feet. In Southwest Appalachia, Expand Energy set a U.S. land bit run record by drilling 30,368 feet of measured depth on a single bit in less than five days, along with a U.S. land lateral length record of 27,657 feet.

The following chart demonstrates the consistent improvement in drilling efficiency across all regions:

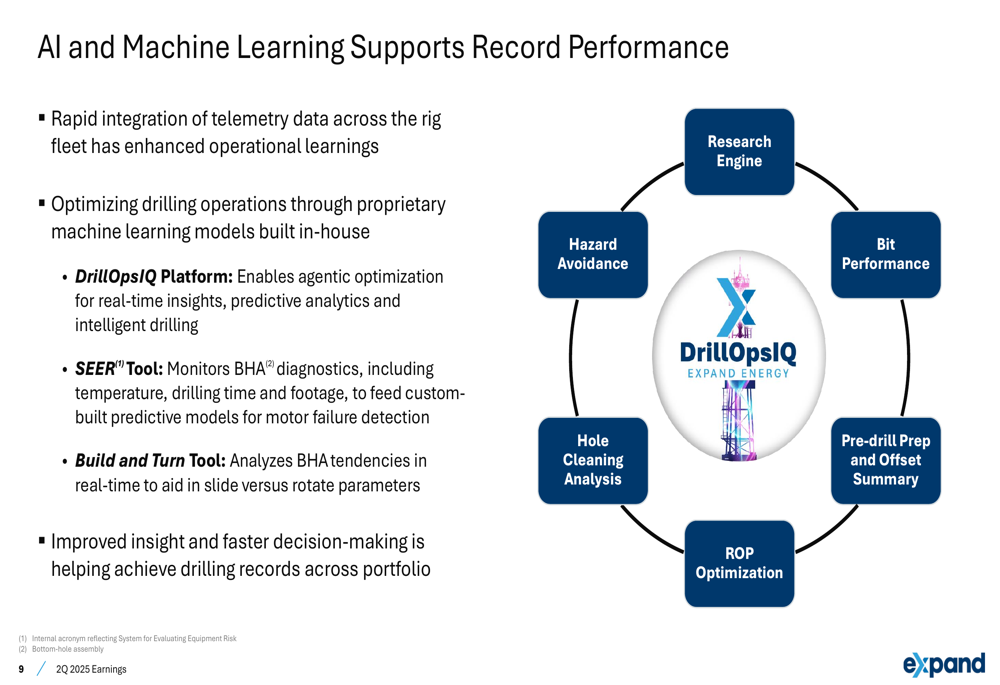

Expand Energy attributes much of its operational improvement to the implementation of artificial intelligence and machine learning technologies. The company has developed proprietary systems including the DrillOpsIQ Platform, which enables real-time insights and intelligent drilling optimization.

As illustrated in the following AI implementation overview, these technologies are driving significant operational efficiencies:

Forward-Looking Statements

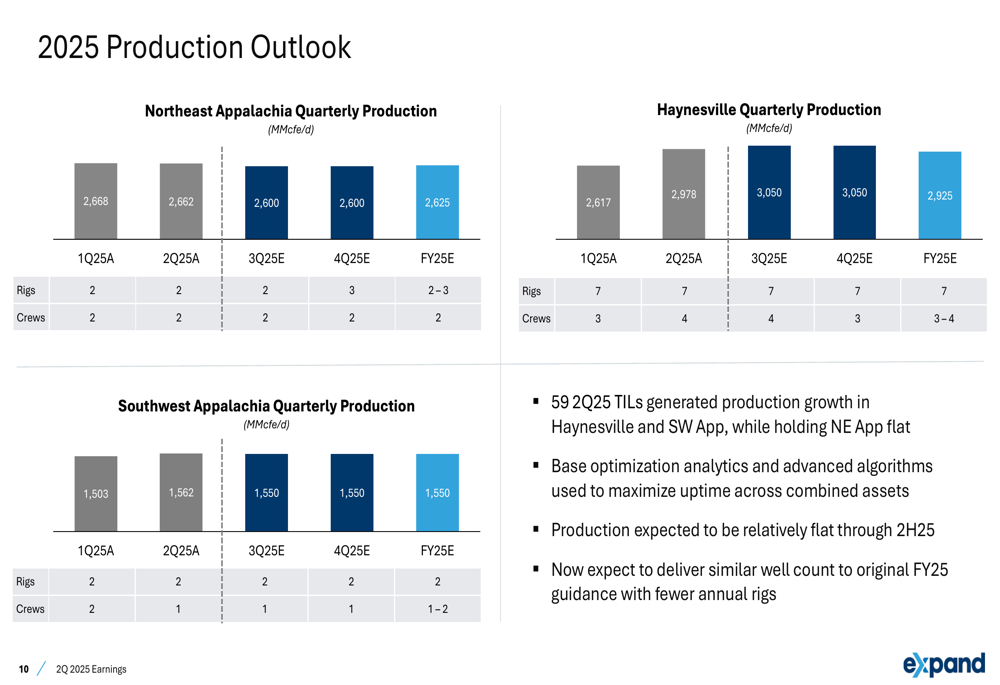

Looking ahead, Expand Energy expects production to remain relatively flat through the second half of 2025. The company anticipates delivering similar well count to its original 2025 guidance but with fewer rigs, demonstrating improved drilling efficiency.

For 2026, the company projects production growth to approximately 7.5 Bcfe/d, with about 300 MMcfe/d of available productive capacity expected to be built by the first quarter of 2026.

The following production outlook details quarterly expectations by region:

Despite these operational achievements, investors may remain cautious following the company’s Q1 2025 results, which showed an earnings beat but a revenue miss of $290 million. The stock is currently trading well below its 52-week high of $123.35, suggesting continued market skepticism about the company’s revenue growth prospects despite its operational efficiency gains.

Expand Energy’s focus on deleveraging, operational efficiency, and returning capital to shareholders indicates a strategic shift toward financial discipline in a volatile natural gas price environment. The company’s ability to translate these operational improvements into revenue growth will likely be a key focus for investors in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.