Tonix Pharmaceuticals stock halted ahead of FDA approval news

Expedia Group (NASDAQ:EXPE) shares surged 17.64% in premarket trading following the release of its Q2 2025 earnings presentation, which showcased stronger-than-expected results across key metrics. The travel technology company reported significant margin expansion and continued strength in its B2B and advertising segments, marking a substantial improvement from its Q1 performance.

Quarterly Performance Highlights

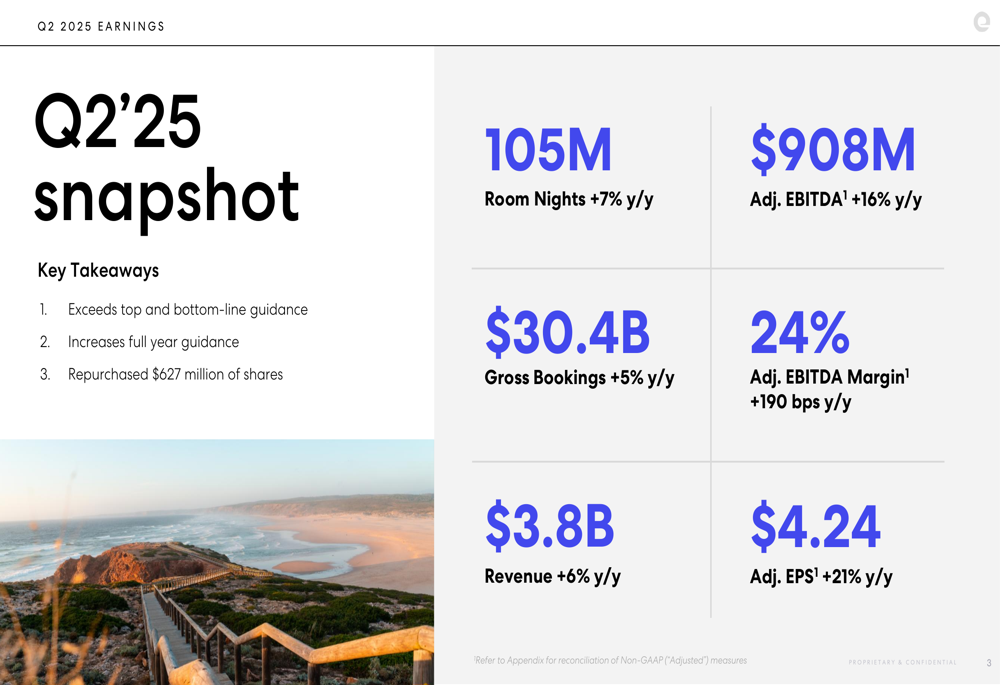

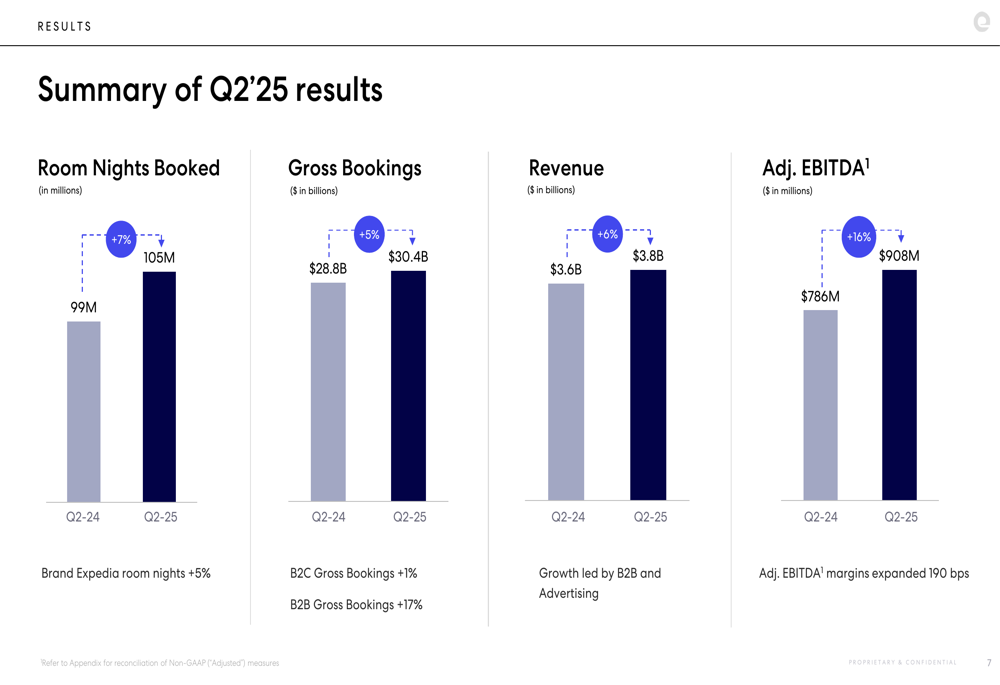

Expedia reported robust financial results for the second quarter, with revenue reaching $3.8 billion, up 6% year-over-year, accelerating from the 3% growth seen in Q1. Room nights booked increased 7% to 105 million, while gross bookings rose 5% to $30.4 billion. The company’s adjusted EBITDA grew 16% to $908 million, with margins expanding 190 basis points to 24%.

As shown in the following chart summarizing Q2 2025 results, the company demonstrated growth across all key metrics:

Adjusted earnings per share reached $4.24, representing a 21% increase compared to the same period last year. This performance significantly exceeded analyst expectations, driving the sharp rise in the company’s stock price, which had previously suffered a 7.68% decline following Q1 results.

The following chart provides a visual breakdown of Expedia’s key performance indicators over recent quarters:

Segment Performance Analysis

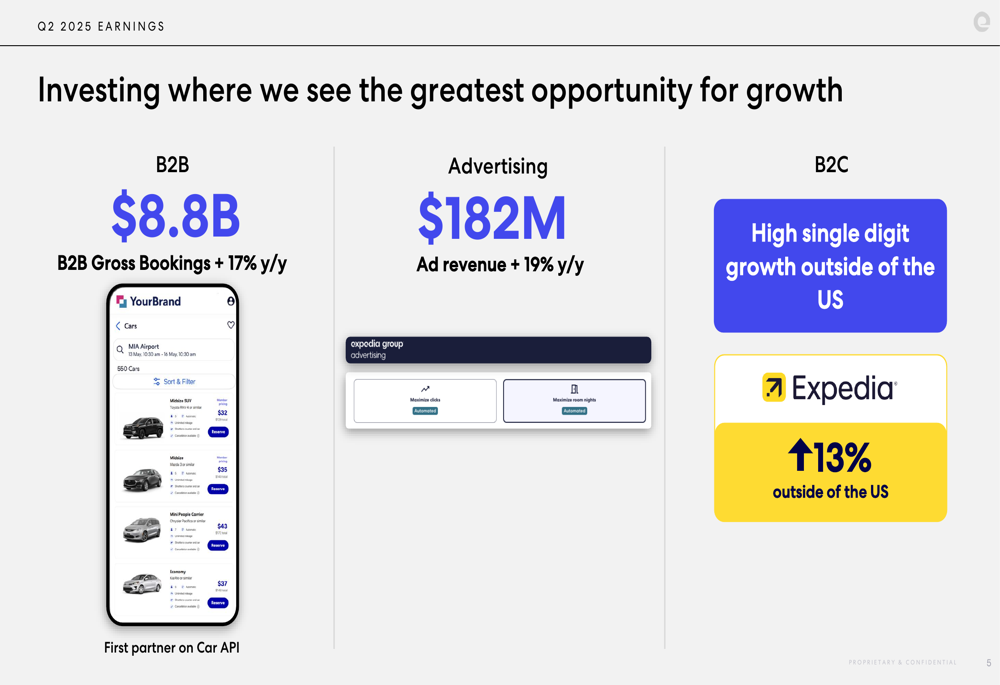

Expedia’s business segments showed divergent performance, with B2B and advertising emerging as the primary growth drivers. B2B gross bookings increased 17% year-over-year to $8.8 billion, while advertising revenue grew 19% to $182 million. In contrast, the B2C segment showed more modest growth, with gross bookings up just 1% to $21.6 billion.

The company highlighted that its B2C segment is experiencing high single-digit growth outside the United States, with particularly strong 13% growth in international markets. This international strength is helping to offset what the company had previously described as "softer U.S. travel demand" during its Q1 earnings call.

The following slide illustrates Expedia’s strategic growth investments across its business segments:

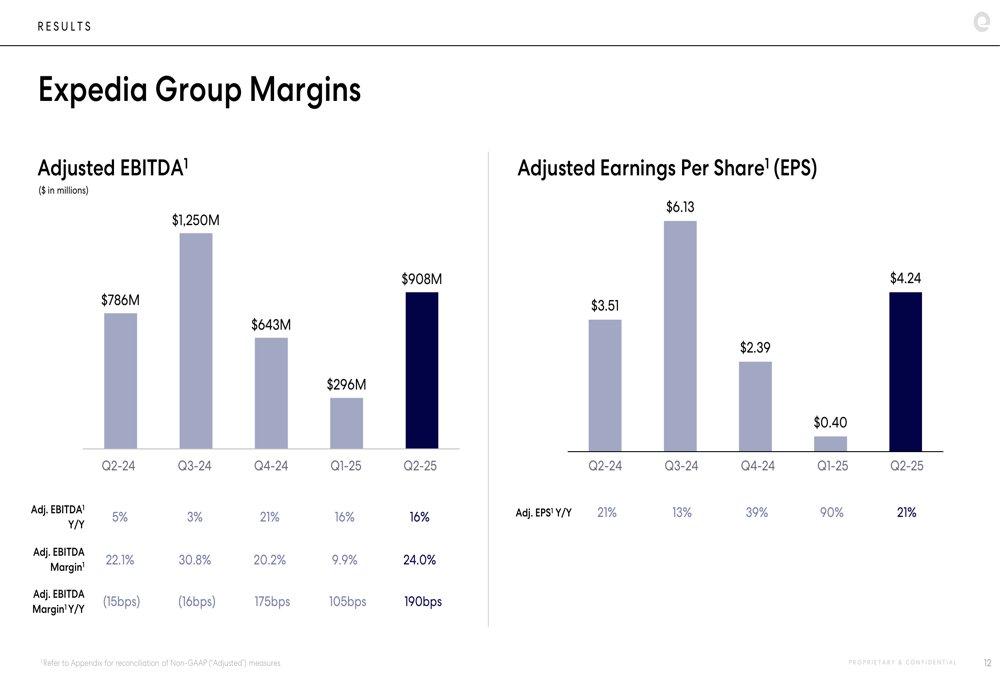

Expedia’s margin performance was particularly impressive, with adjusted EBITDA margins expanding by 190 basis points year-over-year. The B2C segment’s adjusted EBITDA margin reached 29.4%, while the B2B segment achieved a 27.3% margin.

As shown in the following chart, the company has maintained a trend of improving profitability:

Strategic Initiatives

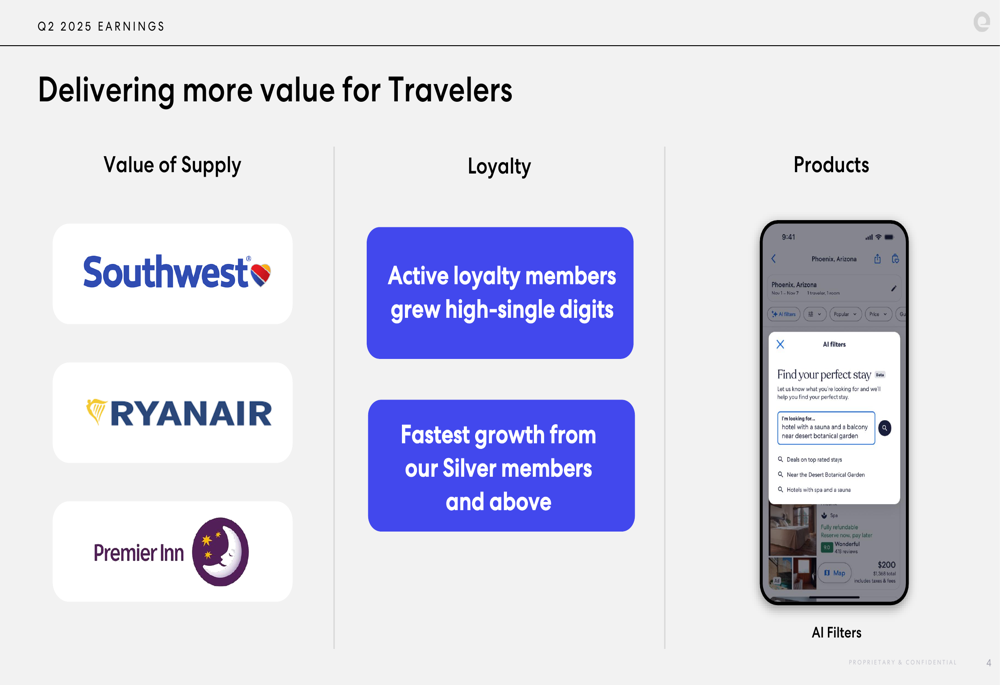

Expedia emphasized three key areas where it’s delivering more value for travelers: supply expansion, loyalty program enhancement, and product innovation. The company has added major airlines like Southwest and Ryanair to its platform, while loyalty membership has grown at high single-digit rates, with the fastest growth coming from Silver members and above.

The following slide details these strategic focus areas:

The company is leveraging artificial intelligence across its operations to drive efficiencies and enhance the customer experience. AI implementations are accelerating developer cycle times and improving operations across all functions, contributing to the significant margin expansion observed in Q2.

Expedia is also focusing on operational efficiency, with adjusted overhead expenses as a percentage of revenue decreasing by 20 basis points year-over-year to 16.8%. Direct marketing expenses increased slightly as a percentage of gross bookings, rising 10 basis points to 6.3%.

Financial Position and Capital Allocation

Expedia maintained a strong balance sheet with $6.7 billion in cash and short-term investments and total liquidity of $9.2 billion. The company’s leverage ratio improved to 2.0x, down from 2.3x in the same quarter last year.

The company continues to return capital to shareholders, with $1.6 billion returned over the trailing twelve months, including $1.5 billion in share repurchases and $0.1 billion in dividends. In Q2 alone, Expedia repurchased $627 million of its shares.

Free cash flow for the trailing twelve months was $2.0 billion, supporting the company’s capital return strategy while maintaining financial flexibility.

Forward-Looking Statements

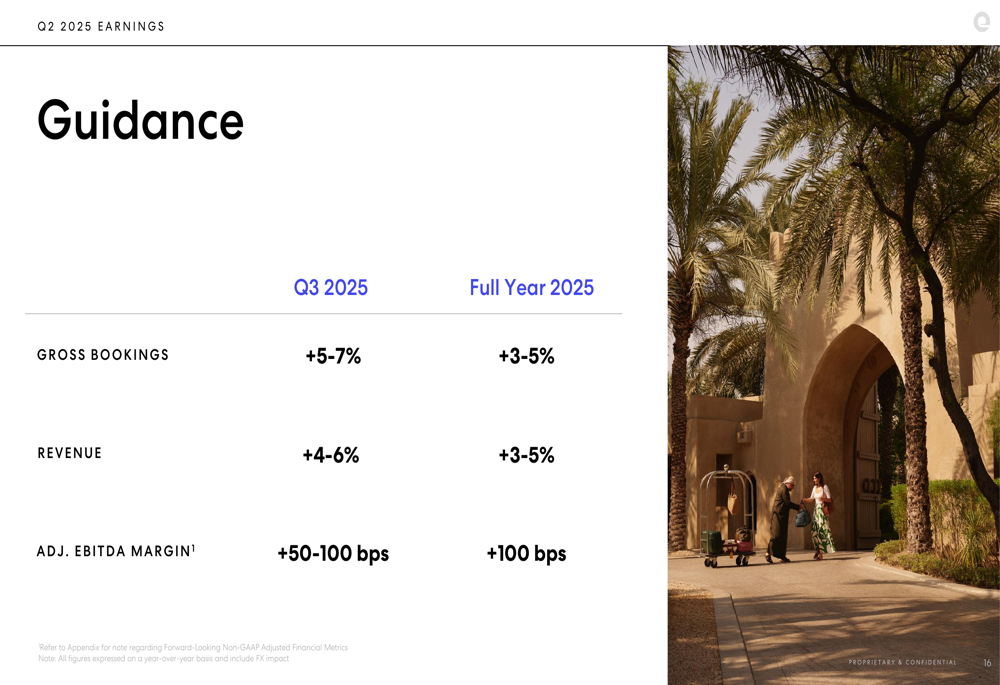

For Q3 2025, Expedia provided guidance for gross bookings growth of 5-7% and revenue growth of 4-6% year-over-year. The company expects adjusted EBITDA margin expansion of 50-100 basis points.

For the full year 2025, Expedia raised its guidance, now projecting gross bookings and revenue growth of 3-5% and adjusted EBITDA margin expansion of 100 basis points.

The following slide details the company’s guidance for the remainder of 2025:

Conclusion

Expedia’s Q2 2025 results demonstrate the company’s ability to navigate challenging market conditions through strategic diversification and operational efficiency. The strong performance in B2B and advertising segments, coupled with international growth in the B2C business, has positioned the company for continued success despite softer domestic travel demand.

The significant margin expansion and raised full-year guidance reflect management’s confidence in the company’s strategic direction. With a strong balance sheet and ongoing capital return program, Expedia appears well-positioned to capitalize on growth opportunities while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.