Tonix Pharmaceuticals stock halted ahead of FDA approval news

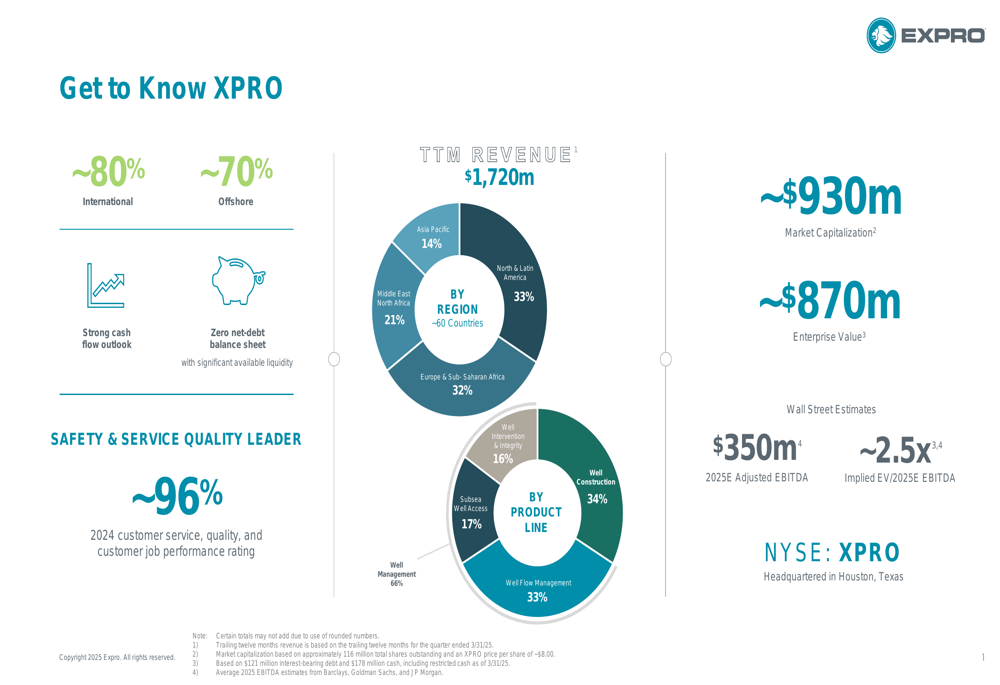

Introduction & Market Context

Expro Group Holdings N.V. (NYSE:XPRO) reported record first-quarter results for 2025, with revenue reaching $391 million and Adjusted EBITDA of $76 million. The company highlighted its strong performance despite varying regional results, with its Middle East & North Africa segment showing particularly robust growth while Asia Pacific experienced declines.

The oilfield services provider maintains a strong financial position with zero net debt and a robust backlog of $2.2 billion. According to the presentation, Expro’s business is approximately 80% international and 70% offshore, positioning it well in higher-margin markets.

As shown in the following overview of the company’s positioning and financial strength:

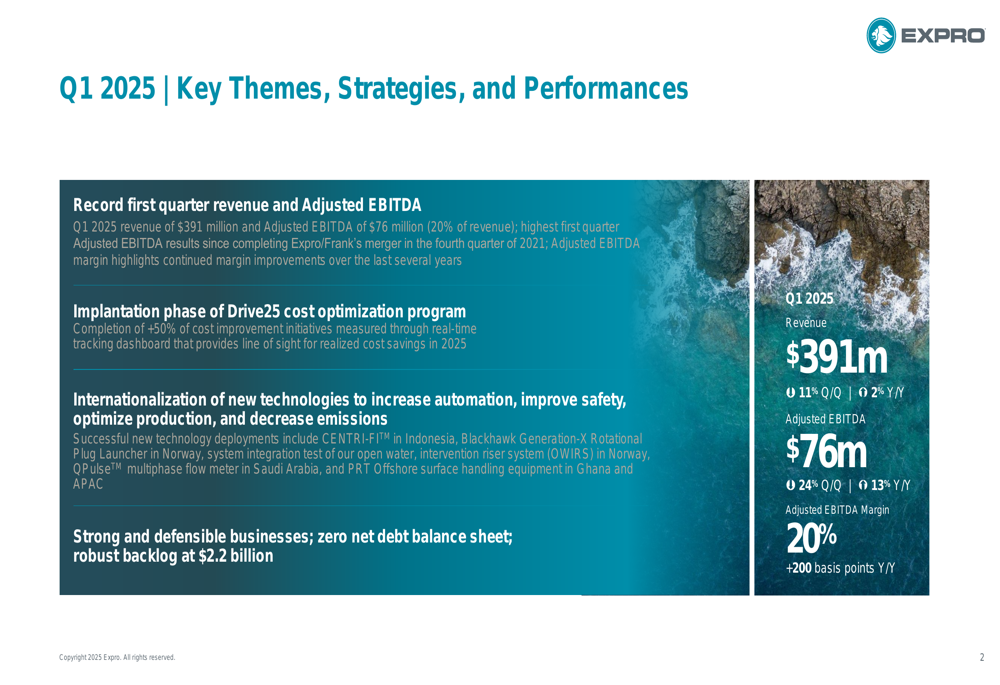

Quarterly Performance Highlights

Expro reported Q1 2025 revenue of $391 million, representing an 11% increase quarter-over-quarter and a 2% increase year-over-year. Adjusted EBITDA reached $76 million, up 24% quarter-over-quarter and 13% year-over-year, with Adjusted EBITDA margin improving to 20%, a 200 basis point increase compared to the same period last year.

The following slide highlights these key performance metrics and strategic themes:

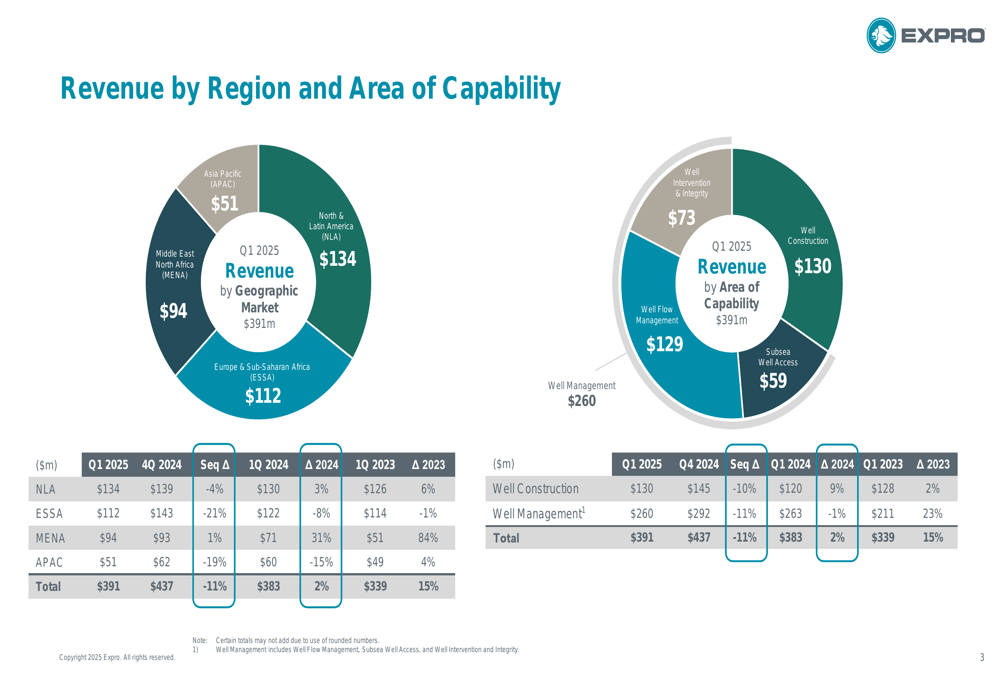

Revenue performance varied significantly across regions. North & Latin America (NLA) generated $134 million in revenue (up 4% Q/Q, 3% Y/Y), Europe & Sub-Saharan Africa (ESSA) contributed $112 million (down 21% Q/Q, up 8% Y/Y), Middle East & North Africa (MENA) delivered $94 million (up 1% Q/Q, up 31% Y/Y), and Asia Pacific (APAC) reported $51 million (down 19% Q/Q, down 15% Y/Y).

The breakdown of revenue by region and capability is illustrated in the following chart:

MENA emerged as the standout performer with a segment EBITDA margin of 37%, the highest among all regions. This strong performance was driven by higher well intervention and integrity revenue in Qatar and increased production solutions revenue in Algeria. The company also successfully executed its first ReLine expandables deployment in Saudi Arabia since acquiring Coretrax in May 2024.

Conversely, APAC experienced the most significant decline, with revenue dropping 19% sequentially and 15% year-over-year. This decrease was primarily attributed to lower subsea well access, well flow management, and well construction activity offshore Australia. Despite these challenges, the region secured new contracts in Indonesia and Brunei worth approximately $23 million combined.

Strategic Initiatives

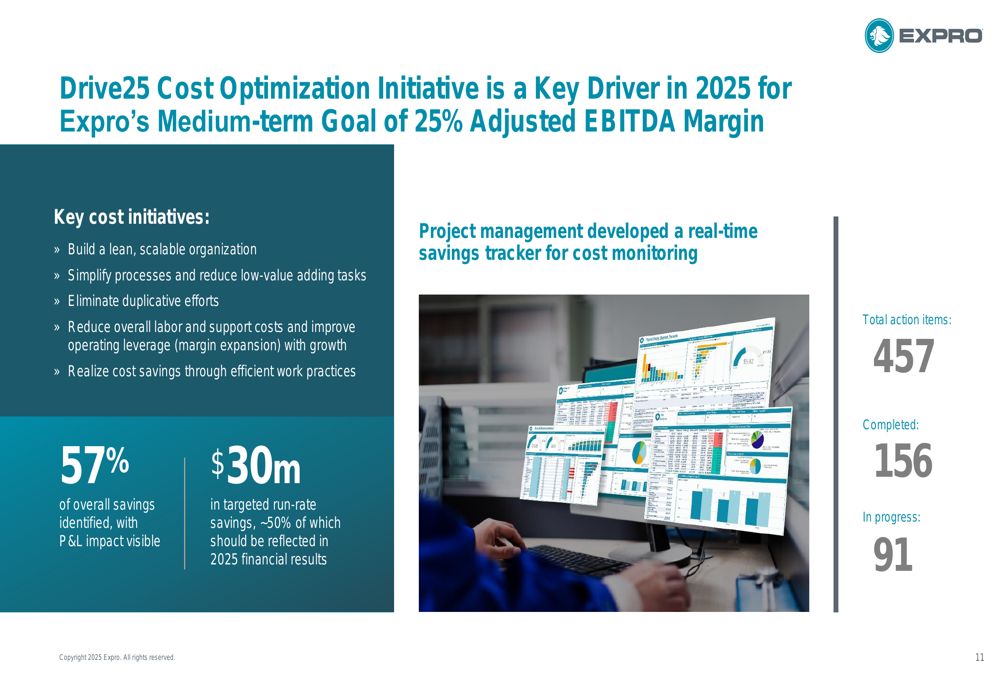

Expro is actively implementing its Drive25 cost optimization program, which aims to build a leaner, more scalable organization while reducing support costs. The initiative targets $30 million in run-rate savings, with approximately 50% expected to be reflected in 2025 financial results. As of Q1 2025, the company has identified 57% of overall savings, with the P&L impact already visible.

The following slide details the progress of the Drive25 initiative:

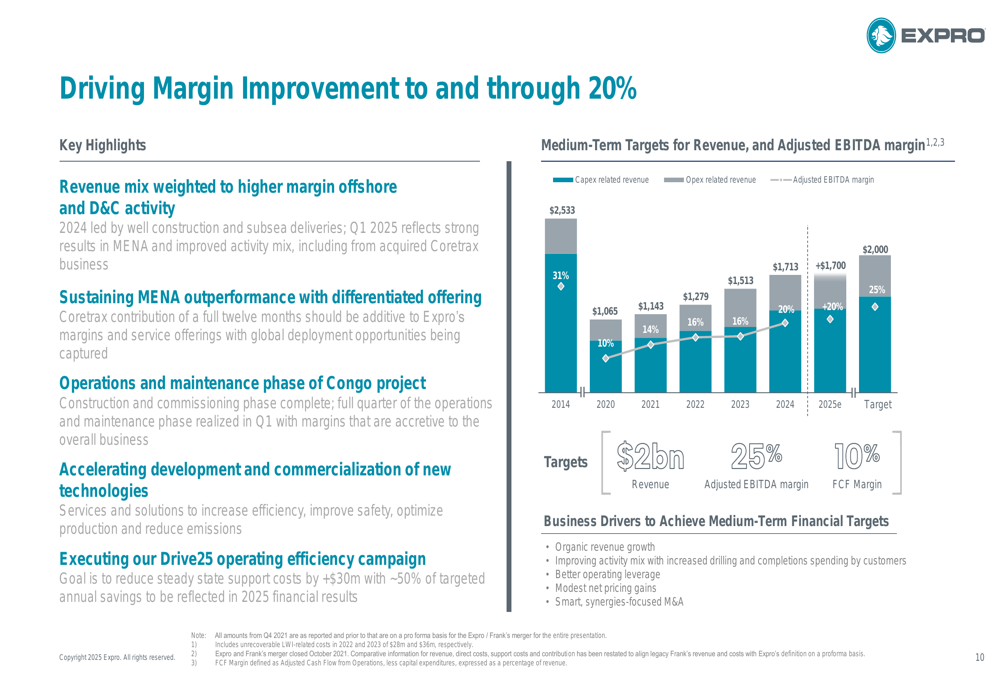

The company is also focused on driving margin improvement through several strategic initiatives, including weighting its revenue mix toward higher-margin offshore and drilling and completions activity, sustaining MENA outperformance, and accelerating the development and commercialization of new technologies.

Expro’s medium-term targets include growing revenue to $2,533 million, increasing Adjusted EBITDA margin to 25%, and improving free cash flow margin to 10%, as illustrated in this strategic overview:

Historical Performance & Trends

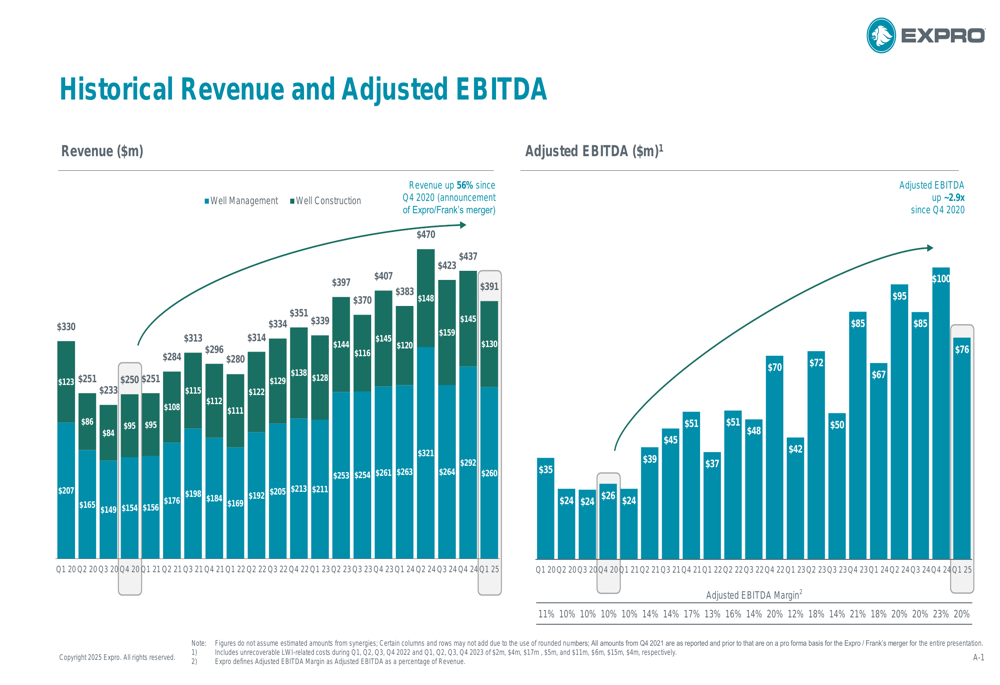

Expro has demonstrated consistent financial improvement since the merger of Expro and Frank’s in Q4 2020. Revenue has increased by 56% during this period, while Adjusted EBITDA has grown approximately 2.9x, with Adjusted EBITDA margin expanding from 11% to 20%.

The following chart illustrates this historical performance:

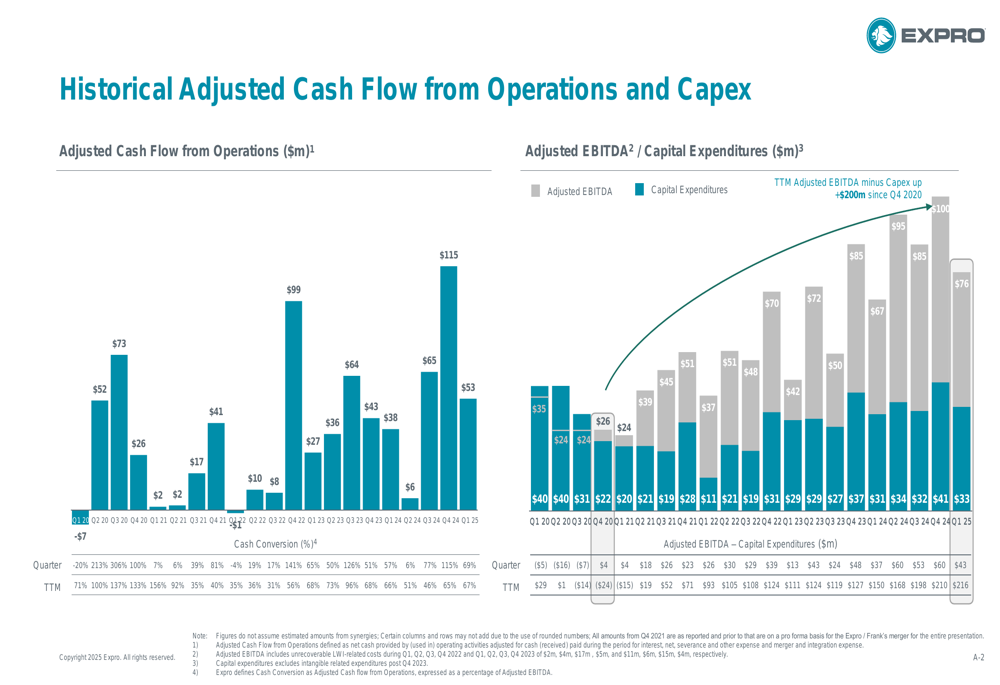

The company has also shown improvement in cash flow generation. Adjusted EBITDA minus capital expenditures has increased by more than $200 million since Q4 2020, reflecting enhanced operational efficiency and disciplined capital allocation.

This trend is demonstrated in the following cash flow chart:

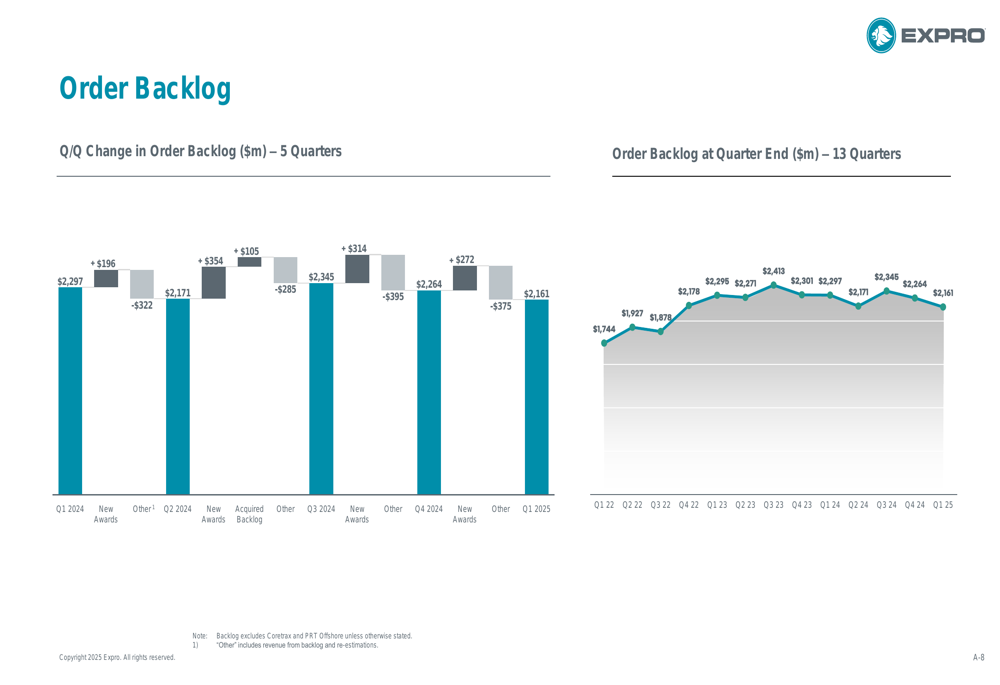

Order backlog has remained strong, providing visibility into future revenue. As of Q1 2025, Expro’s backlog stood at $2.2 billion, supporting the company’s revenue outlook for the remainder of the year.

The evolution of the company’s order backlog is illustrated here:

Forward-Looking Statements

For Q2 2025, Expro expects revenue between $400 million and $410 million, representing a sequential increase of approximately 4% but a year-over-year decrease of around 14%. Adjusted EBITDA for Q2 is projected to be between $80 million and $90 million, with Adjusted EBITDA margin expected to improve sequentially by 100 basis points and year-over-year by approximately 50 basis points.

For the full year 2025, the company anticipates revenue exceeding $1,700 million and Adjusted EBITDA of more than $350 million. Key financial targets include an Adjusted EBITDA margin of approximately 21%, capital expenditures of around 7% of revenue, and a free cash flow margin of approximately 7%.

It’s worth noting that Expro’s stock has experienced significant volatility since its Q4 2024 earnings report. According to the provided fundamentals data, the stock closed at $8.04 on April 29, 2025, with premarket trading showing an increase of 3.23% to $8.30. This represents a substantial decline from the $13.02 price mentioned in the Q4 2024 earnings article, suggesting investors may be concerned about the company’s outlook despite the record Q1 results.

The company’s ability to execute its Drive25 cost optimization program and navigate regional performance variations will be crucial for achieving its 2025 financial targets and medium-term strategic objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.