Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

Extreme Networks Inc (NASDAQ:EXTR) presented its third quarter fiscal year 2025 financial results on April 30, 2025, highlighting a return to a net cash positive position and significant improvement in free cash flow. The networking solutions provider reported total revenue of $284.5 million, continuing its recovery from the previous year’s challenges.

The company’s stock has shown volatility recently, with fundamentals indicating a premarket jump of 8.86% to $14.50 following the earnings release, after closing at $13.32 the previous day. This positive market reaction appears to reflect investor confidence in the company’s improving financial position and growth trajectory.

Quarterly Performance Highlights

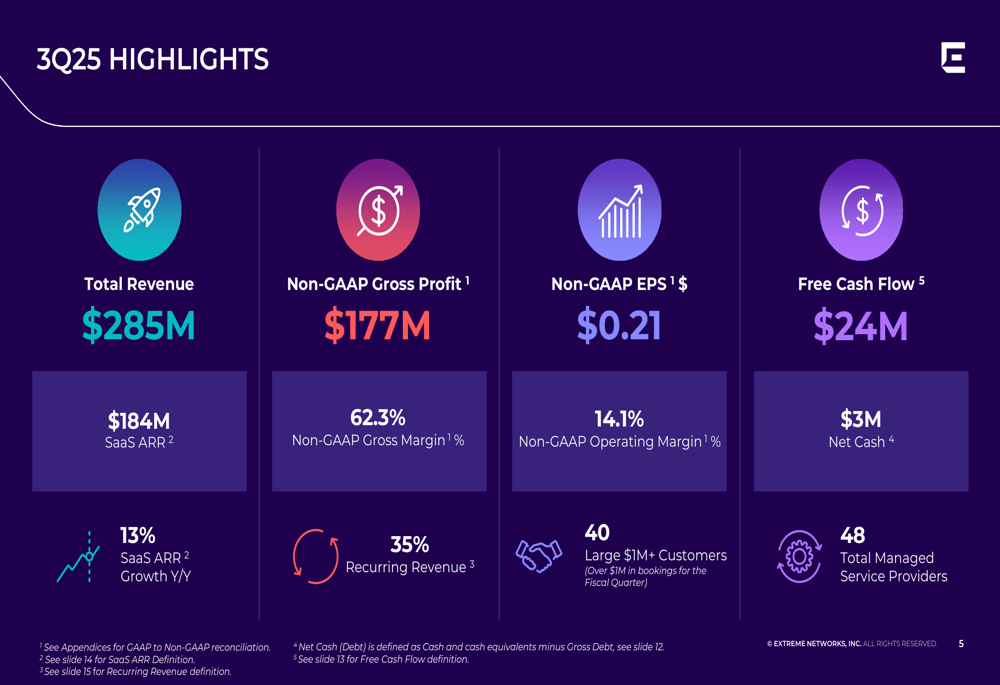

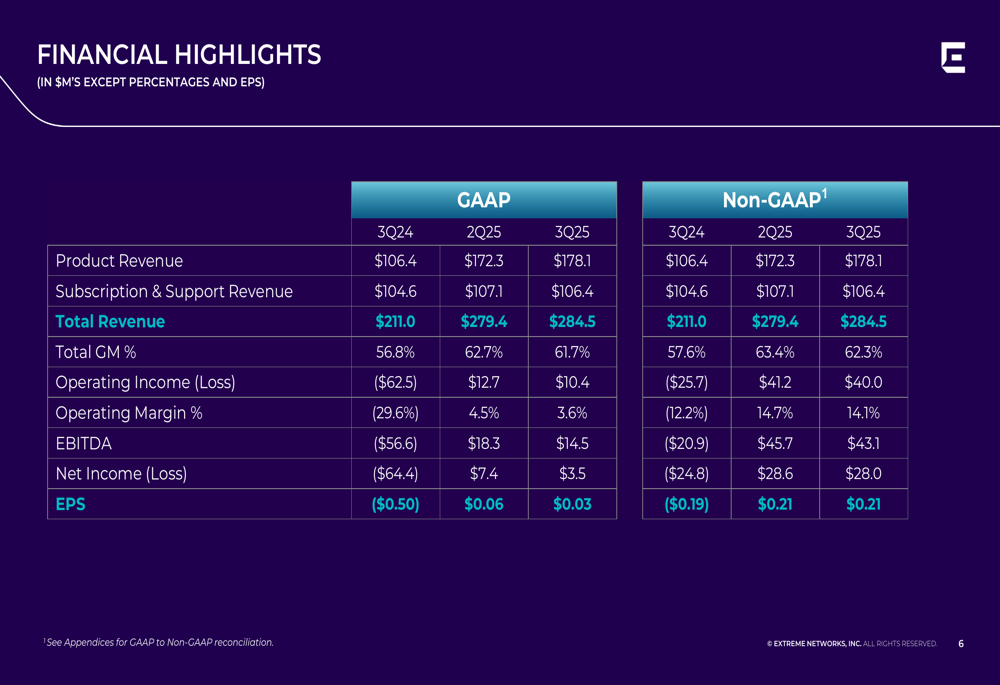

Extreme Networks reported Q3 2025 total revenue of $284.5 million, representing a substantial improvement from $211.0 million in the same quarter last year. The company achieved non-GAAP earnings per share of $0.21, maintaining the same level as the previous quarter and marking a significant turnaround from the ($0.19) loss per share in Q3 2024.

As shown in the following comprehensive overview of key metrics for the quarter:

The company highlighted several positive developments, including reaching a net cash positive position of $3 million, maintaining stable recurring revenue at $101 million (representing 35% of total revenue), and growing its SaaS Annual Recurring Revenue (ARR) to $184 million, up 13% year-over-year. Extreme Networks also reported having 40 large customers with over $1 million in business and partnerships with 48 managed service providers.

The financial comparison across recent quarters demonstrates the company’s continued recovery and stabilization:

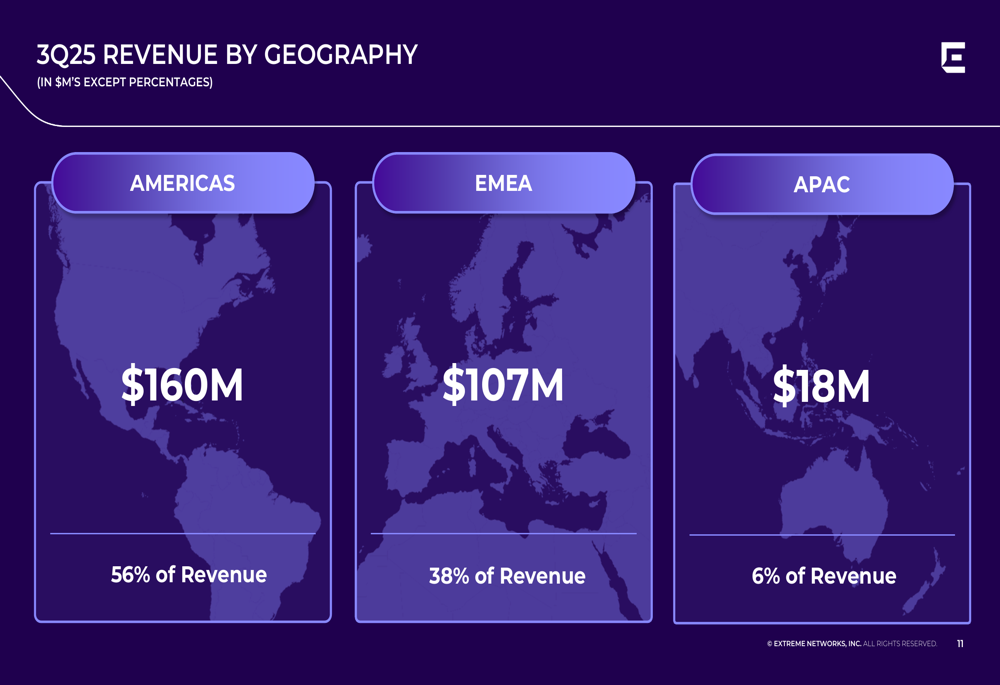

Revenue growth was led by the Americas region, which saw a 21% sequential increase. The geographic distribution of revenue shows that the Americas contributed 56% of total revenue, while EMEA and APAC accounted for 38% and 6%, respectively:

Detailed Financial Analysis

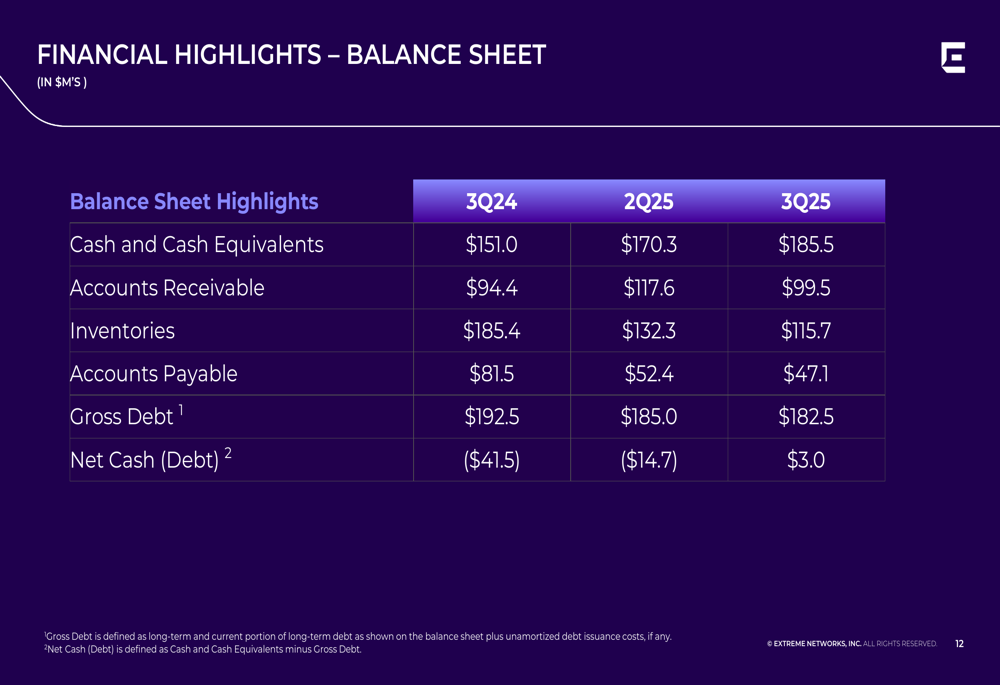

Extreme Networks’ balance sheet showed significant improvement, with cash and cash equivalents increasing to $185.5 million in Q3 2025 from $151.0 million in Q3 2024. The company also substantially reduced its inventory levels from $185.4 million to $115.7 million over the same period, indicating improved operational efficiency and supply chain management.

The following balance sheet highlights illustrate the company’s strengthening financial position:

One of the most notable improvements was in free cash flow, which reached $24.2 million in Q3 2025 compared to a negative $73.6 million in Q3 2024. This dramatic turnaround reflects enhanced operational efficiency and improved working capital management:

The company’s SaaS ARR continues to show consistent growth, increasing from $162 million in Q3 2024 to $184 million in Q3 2025, demonstrating the success of Extreme Networks’ subscription-based business model:

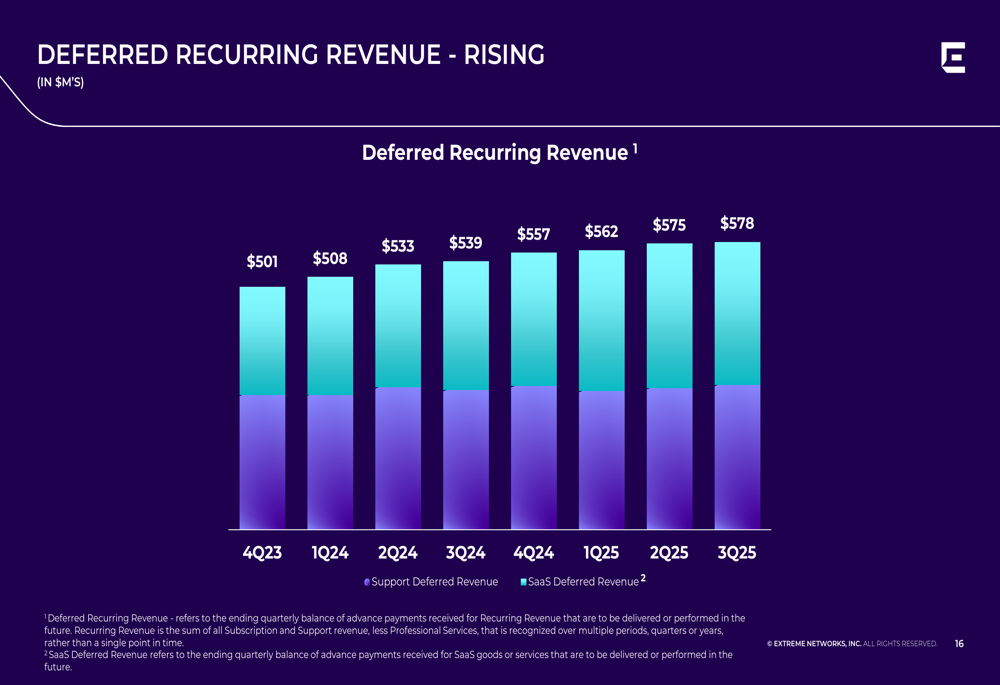

Another positive indicator for future revenue stability is the rising deferred recurring revenue, which reached $578 million in Q3 2025, up 7% year-over-year:

Forward-Looking Statements

For the fourth quarter of fiscal year 2025, Extreme Networks provided guidance for revenue between $295.0 million and $305.0 million, representing potential sequential growth. The company expects non-GAAP gross margin between 61.8% and 62.8%, operating margin between 13.3% and 15.3%, and earnings per share between $0.21 and $0.25.

The detailed Q4 2025 guidance shows the company’s expectations for continued improvement:

For the full fiscal year 2025, Extreme Networks projects revenue between $1,128 million and $1,138 million, reflecting the company’s confidence in its growth trajectory despite the challenges faced earlier in the fiscal year.

This guidance aligns with the company’s previous statements during its Q2 earnings call, where it anticipated sequential growth in the second half of the year driven by new product launches and improving market conditions. The Q3 results and Q4 guidance suggest that Extreme Networks is executing on this strategy, with particular strength in the Americas region.

The company’s return to a net cash positive position, combined with strong free cash flow and stable recurring revenue, positions Extreme Networks for potential continued improvement as it moves toward the close of fiscal year 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.