Japan records surprise trade deficit in July as exports weaken further

Introduction & Market Context

EZCORP Inc (NASDAQ:EZPW), a leading provider of pawn transactions and seller of pre-owned merchandise in the United States and Latin America, has released its third-quarter fiscal 2025 earnings presentation, revealing strong growth across key metrics. The company, which operates 1,336 stores with 8,200 team members, continues to benefit from its strategic expansion and digital transformation initiatives.

The results build on the momentum seen in the previous quarter, where EZCORP reported an EPS beat but missed revenue expectations. The stock closed at $13.13 on July 30, 2025, up 1.45% for the day, and has shown resilience with a 52-week range of $10.26 to $16.60.

Quarterly Performance Highlights

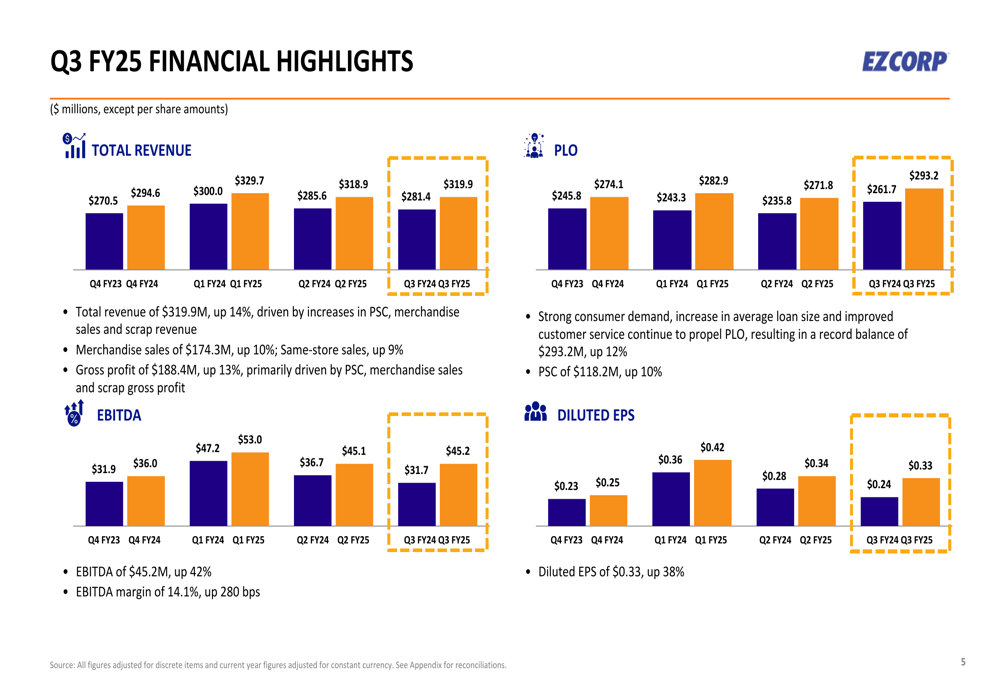

EZCORP delivered impressive financial results for Q3 FY25, with total revenue reaching $319.9 million, a 14% increase year-over-year. This growth was driven by strong performance across multiple revenue streams, including pawn service charges (PSC), merchandise sales, and scrap revenue.

As shown in the following chart of key financial metrics, the company achieved significant improvements across all major indicators:

Notably, EZCORP reported diluted earnings per share of $0.33, representing a 38% increase compared to the same period last year. This performance is particularly impressive considering the company’s Q2 FY25 EPS was $0.34, indicating relatively consistent profitability despite seasonal variations.

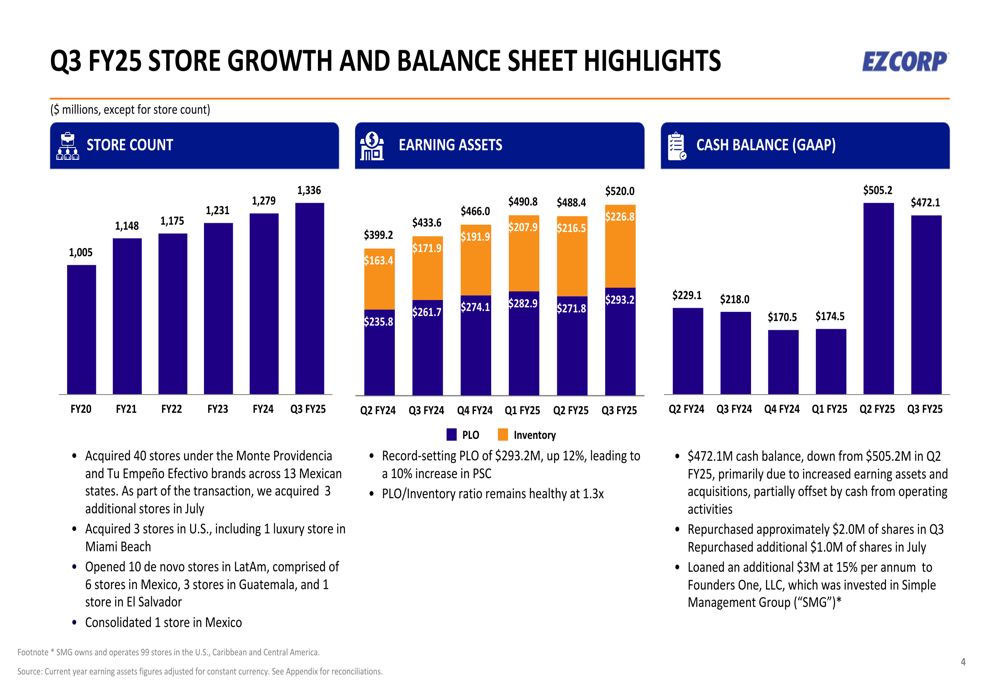

The company’s pawn loans outstanding (PLO) reached a record $293.2 million, up 12% year-over-year, demonstrating continued strong demand for EZCORP’s core lending services. This growth in PLO, combined with a 10% increase in pawn service charges, contributed significantly to the overall revenue increase.

Detailed Financial Analysis

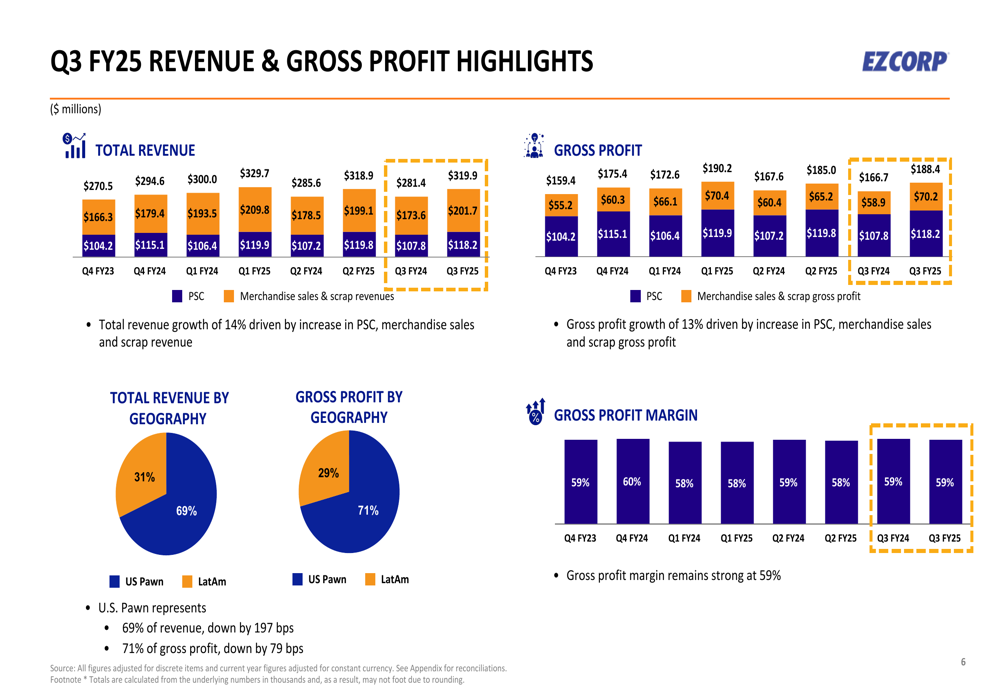

EZCORP’s financial performance showed strength across both geographic segments. The U.S. Pawn segment, which represents 69% of total revenue, saw an 11% increase in total revenue to $673.5 million. The Latin America Pawn segment demonstrated even stronger growth, with revenue increasing by 21% to $294.9 million.

The following chart illustrates the breakdown of revenue and gross profit by geography:

Gross profit reached $188.4 million, up 13% year-over-year, driven by increases in PSC, merchandise sales, and scrap gross profit. The company maintained a strong gross profit margin of 59%, reflecting effective inventory management and pricing strategies.

EBITDA showed remarkable improvement, increasing by 42% to $45.2 million, with the EBITDA margin expanding by 280 basis points to 14.1%. This significant margin expansion demonstrates the company’s ability to leverage its growing revenue base and improve operational efficiency.

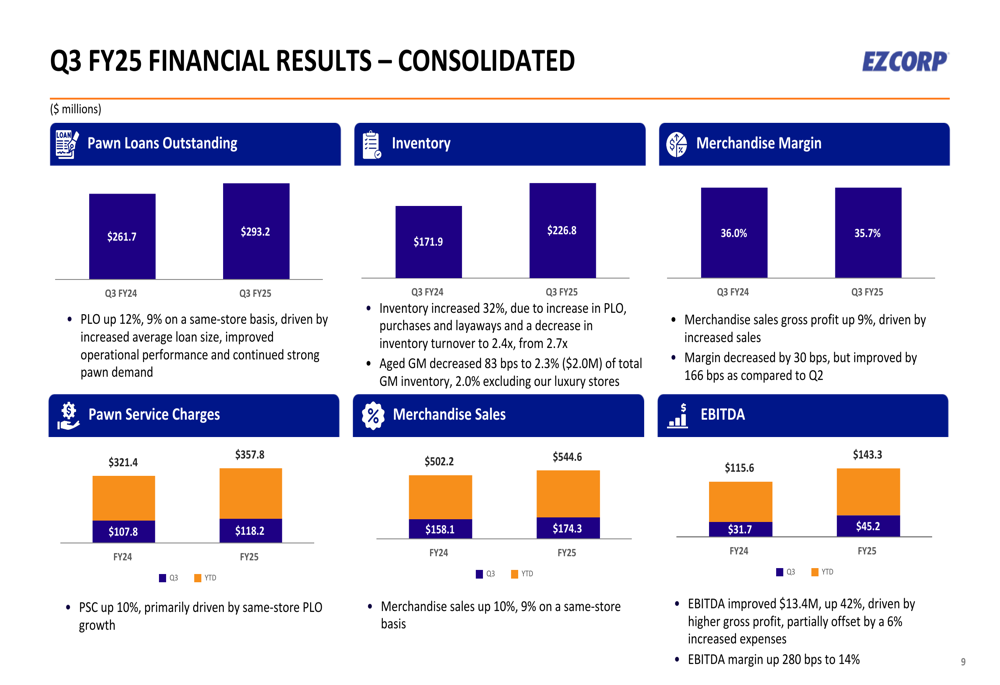

The consolidated financial results highlight the company’s strong performance across key metrics:

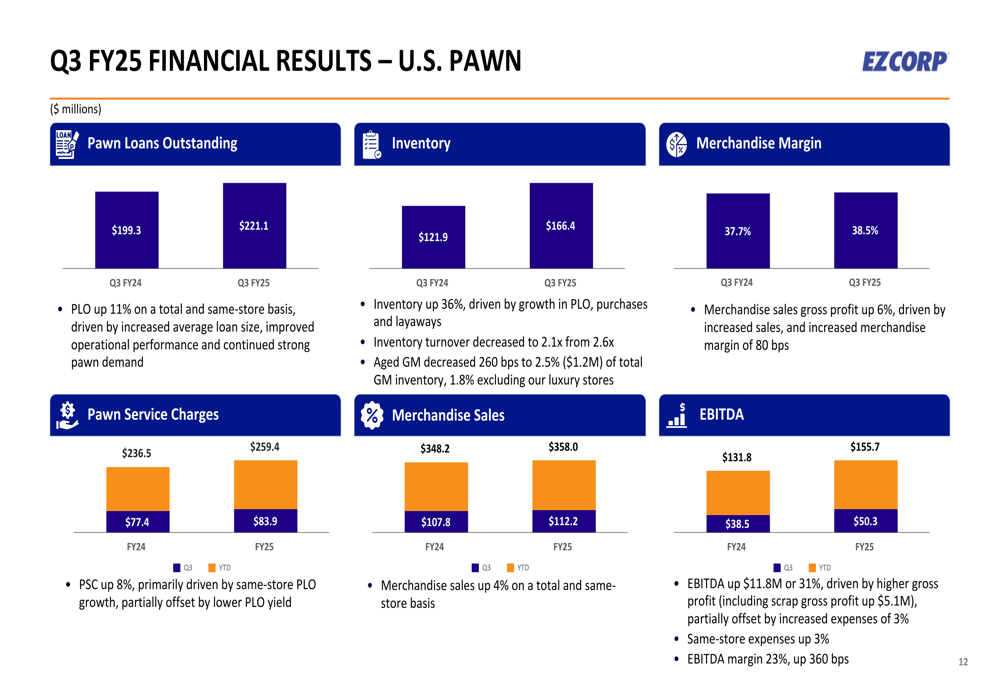

In the U.S. Pawn segment, EZCORP achieved notable improvements in several key areas. PLO increased by 11% to $221.1 million, while inventory grew to $166.4 million. The segment maintained a healthy merchandise margin of 38.5%, and EBITDA increased by 31% to $50.3 million.

The following chart details the financial performance of the U.S. Pawn segment:

The Latin America Pawn segment also delivered strong results, with PLO increasing by 16% to $72.1 million and inventory growing by 21% to $60.5 million. While the merchandise margin decreased slightly to 30.7% from 32.0% in the previous year, the segment’s overall performance remained robust with merchandise sales up 23%.

The financial results for the Latin America Pawn segment are illustrated in the following chart:

Strategic Initiatives

EZCORP continues to execute its growth strategy through both organic expansion and strategic acquisitions. The company’s store count has increased significantly from 1,005 in FY20 to 1,336 in Q3 FY25, as shown in the following chart:

During the quarter, EZCORP acquired 40 stores under the Monte Providencia brand, added 3 additional stores in the U.S. (including a luxury store in Miami Beach), and opened 10 de novo stores in Latin America. This expansion strengthens the company’s market presence and provides additional growth opportunities.

The company’s digital transformation initiatives are also gaining traction. EZ+ Rewards membership has grown to 6.5 million, and U.S. online payments reached $30 million. EZCORP has expanded its view-online, purchase-in-store experience to nearly 80% of U.S. stores and is testing an Instant Quote tool to further enhance the customer experience.

The company’s strategic focus on growing the jewelry category is evident in both segments. In the U.S., jewelry composition increased by 160 basis points, while in Latin America, it grew by 510 basis points, reflecting an operational focus on this higher-margin category.

Forward-Looking Statements

EZCORP’s strong Q3 performance positions the company well for continued growth in the coming quarters. The record PLO balance of $293.2 million provides a solid foundation for future pawn service charge revenue, while the company’s expanding store network offers multiple avenues for growth.

The company’s capital allocation strategy includes both investments in growth and returns to shareholders. During Q3, EZCORP repurchased approximately $2.0 million of shares, with an additional $1.0 million repurchased in July. The company also loaned $3 million at 15% per annum to Founders One, LLC, demonstrating its focus on generating returns from excess capital.

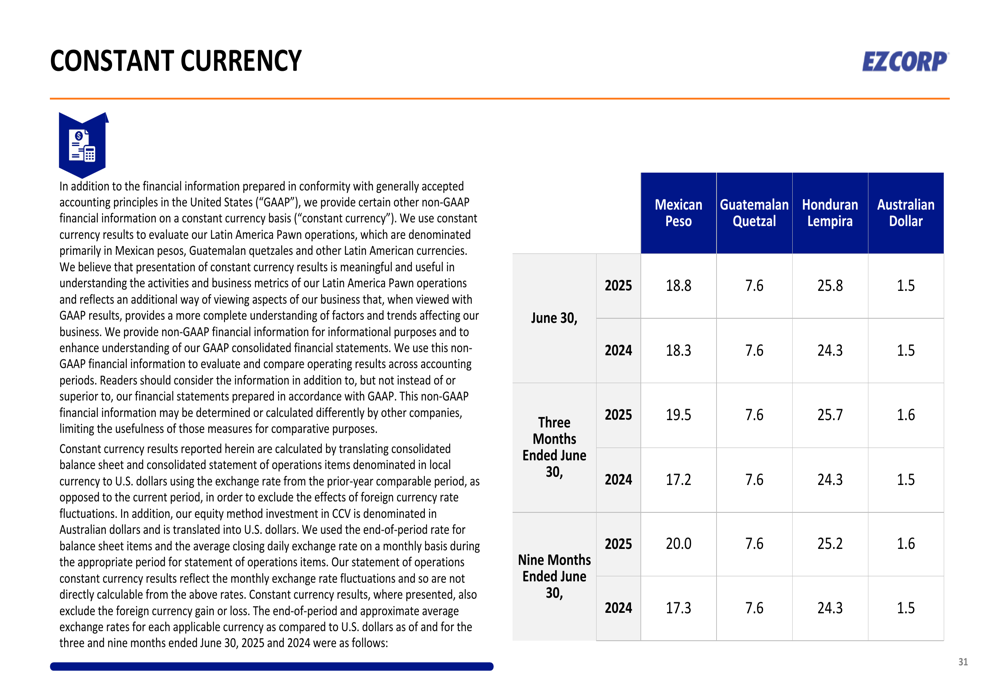

Currency fluctuations remain a factor in EZCORP’s international operations, particularly in Latin America. The company provides constant currency metrics to help investors understand the underlying business performance apart from exchange rate impacts:

As EZCORP continues to execute its growth strategy, investors will be watching for sustained momentum in key metrics such as PLO growth, store expansion, and digital adoption. The company’s ability to maintain strong margins while growing its store base will be crucial for long-term value creation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.