AZTR receives NYSE delisting warning over equity requirement

Introduction & Market Context

Fannie Mae (OTC:FNMA) released its second-quarter 2025 earnings presentation on July 30, revealing a decline in quarterly profit despite achieving a significant milestone in its capital position. The mortgage finance giant reported net income of $3.3 billion on revenues of $7.2 billion, marking a decrease from both the previous quarter and the same period last year.

The company’s stock has shown remarkable volatility over the past year, with FNMA (ST:FNMA) shares trading at $8.56 as of July 29, representing a 12.89% daily gain. The stock has traded between $1.02 and $11.91 over the past 52 weeks, reflecting investor uncertainty about the company’s long-term status.

Quarterly Performance Highlights

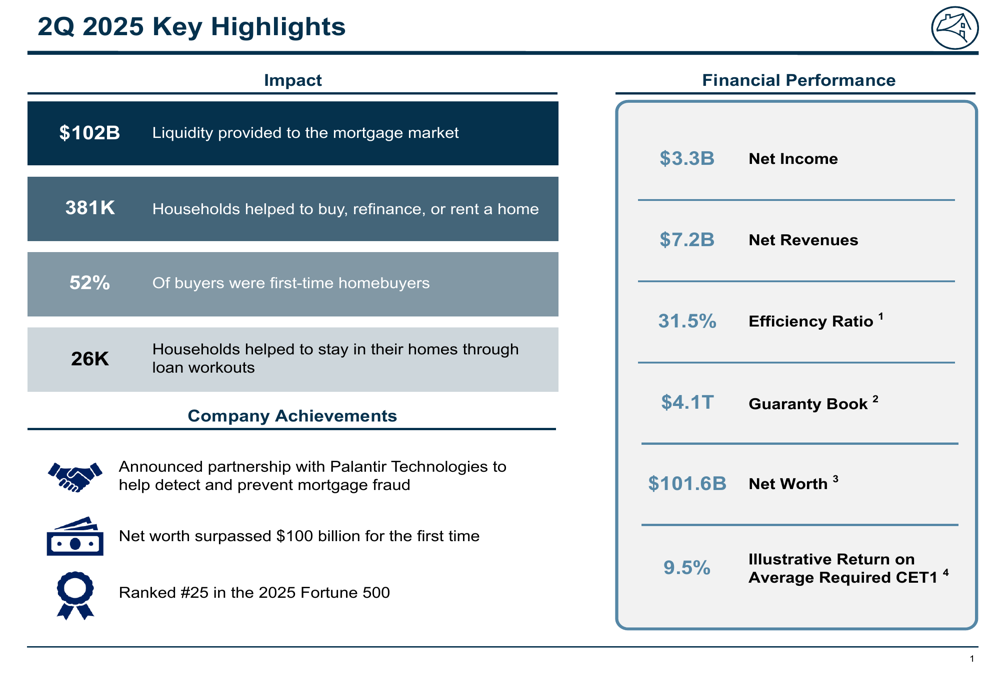

Fannie Mae provided $102 billion in liquidity to the mortgage market during Q2 2025, helping 381,000 households buy, refinance, or rent homes. Notably, 52% of homebuyers served were first-time buyers, underscoring the company’s role in supporting housing affordability.

As shown in the following comprehensive overview of key metrics, the company achieved several notable milestones while maintaining stable operational performance:

The company’s net income of $3.3 billion represents a 26% decrease from the $4.5 billion reported in Q2 2024 and a 9.4% decline from $3.7 billion in Q1 2025. This downward trend was primarily driven by increased provisions for credit losses, which jumped to $946 million in Q2 2025 compared to just $24 million in the previous quarter.

Detailed Financial Analysis

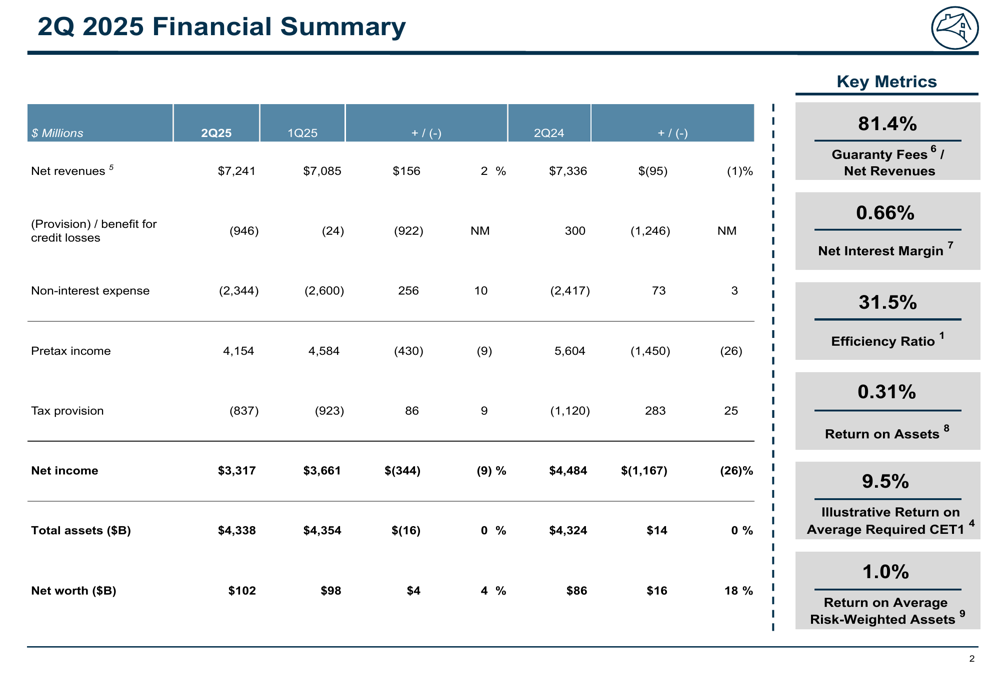

Fannie Mae’s financial summary reveals mixed results across key metrics. While net revenues slightly increased quarter-over-quarter to $7.2 billion, the substantial rise in credit loss provisions significantly impacted bottom-line performance.

The following financial summary illustrates the quarter’s performance compared to previous periods:

The company’s efficiency ratio improved to 31.5% in Q2 2025 from 36.1% in Q1 2025, reflecting better cost management. Non-interest expenses decreased by 9.8% quarter-over-quarter to $2.3 billion, helping to partially offset the impact of higher credit loss provisions.

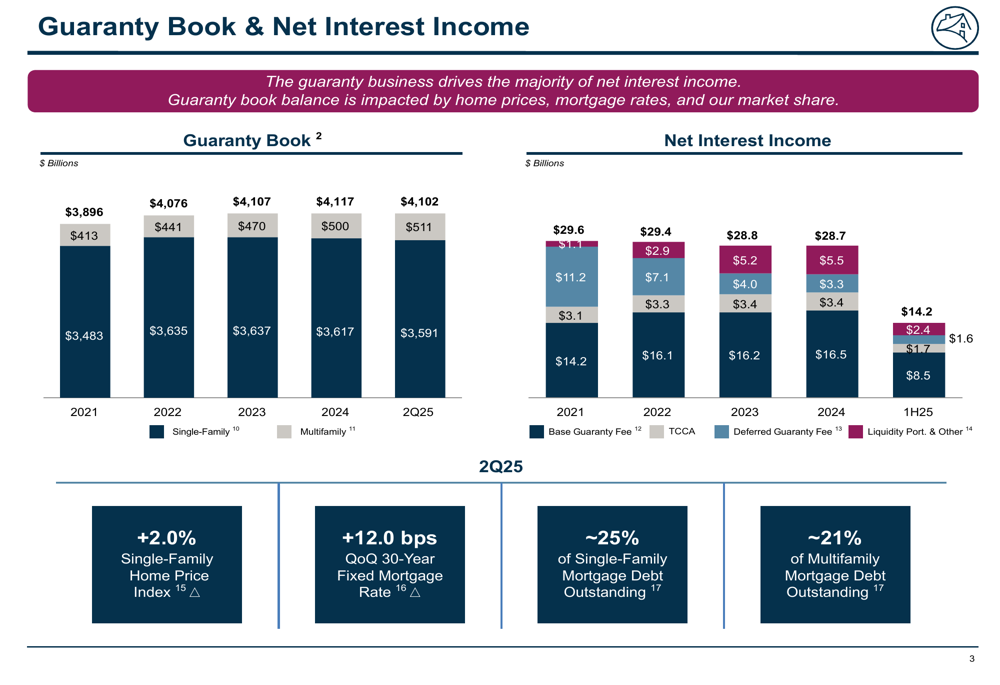

Fannie Mae’s guaranty book of business remained relatively stable at $4.1 trillion, with the multifamily portfolio continuing to grow while the single-family portfolio slightly contracted. Net interest income trends demonstrate the shifting composition of the company’s revenue streams:

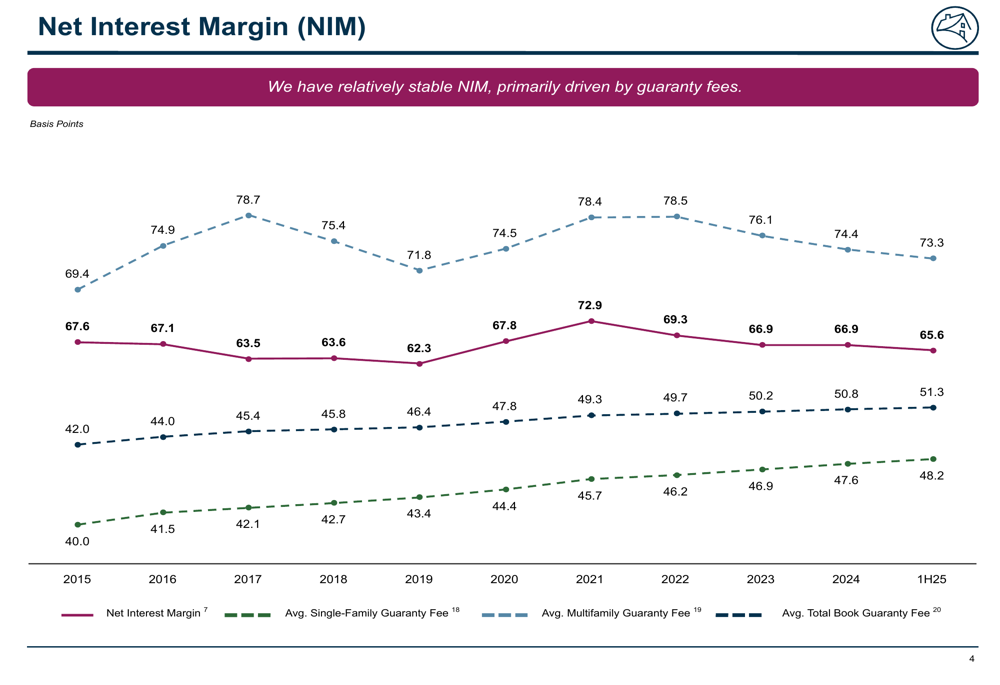

The net interest margin (NIM) has shown a gradual decline over recent years, settling at 65.6 basis points for the first half of 2025. This trend reflects the competitive pressure on guaranty fees and the evolving interest rate environment:

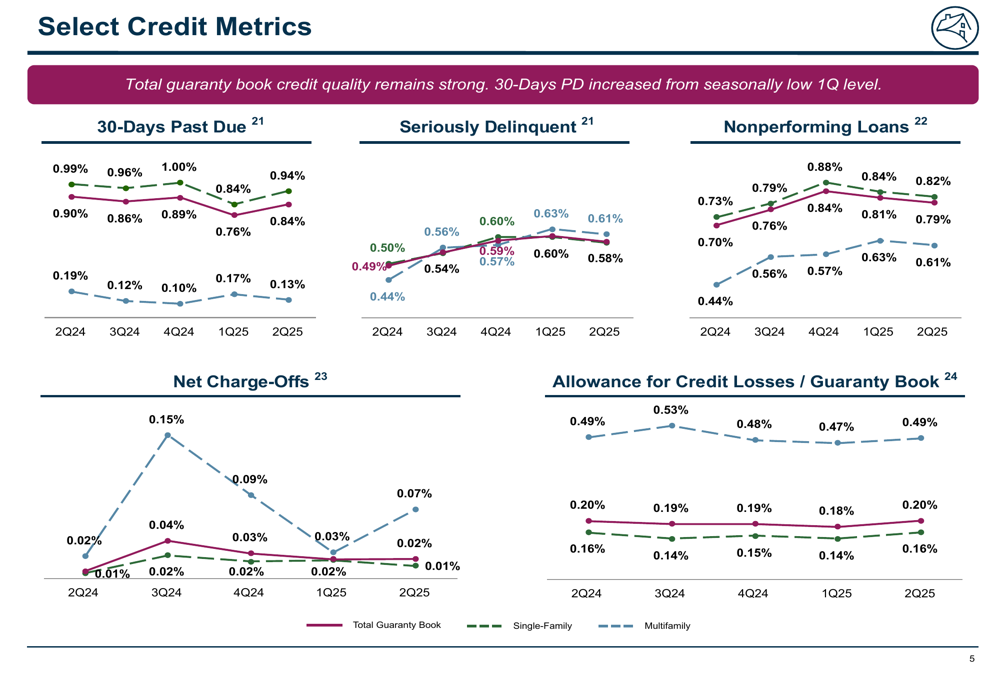

Credit Quality and Risk Management

Fannie Mae’s credit metrics remained relatively stable despite economic uncertainties. The serious delinquency rate held steady at 0.61% in Q2 2025, unchanged from the previous quarter but higher than the 0.50% reported in Q2 2024. Nonperforming loans showed modest improvement, decreasing to 0.79% from 0.82% in Q1 2025.

The following chart illustrates key credit metrics trends across Fannie Mae’s portfolio:

The significant increase in provisions for credit losses suggests management is taking a more cautious approach to potential future credit deterioration, despite relatively stable current delinquency metrics.

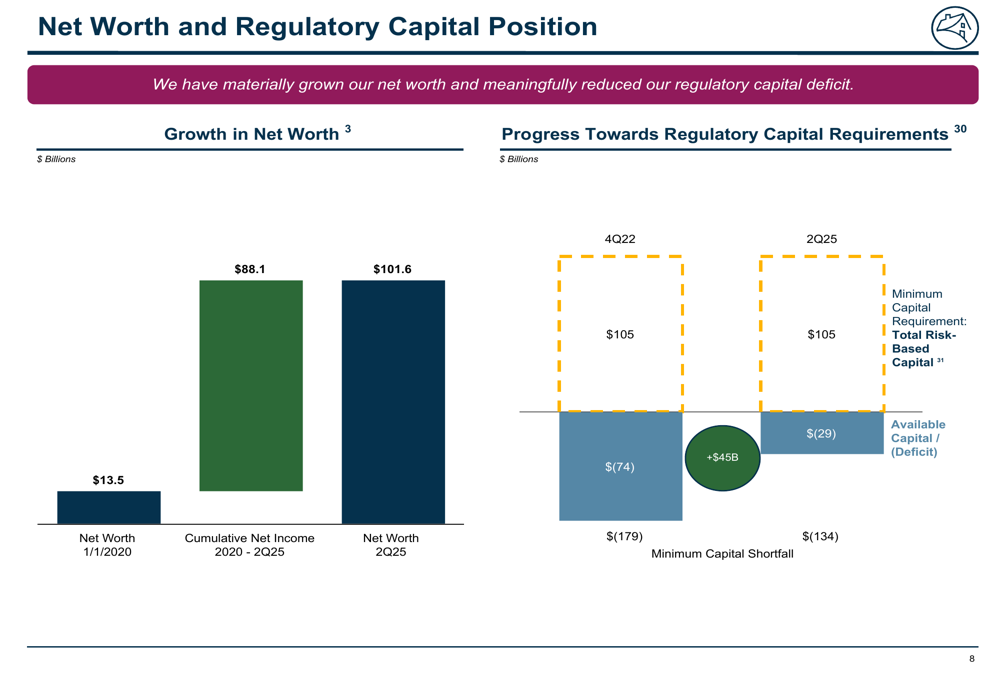

Capital Position and Regulatory Requirements

A major milestone for Fannie Mae was surpassing $100 billion in net worth for the first time, reaching $101.6 billion in Q2 2025. This represents an 18.6% increase from $86 billion in Q2 2024 and continues the strong capital accumulation trend.

Despite this progress, the company still faces a significant capital deficit under regulatory requirements. The following chart illustrates Fannie Mae’s capital position and progress toward meeting regulatory mandates:

While Fannie Mae has reduced its capital deficit by $45 billion since Q4 2022, it still faces a $29 billion shortfall against minimum capital requirements and a larger $134 billion shortfall against prescribed capital buffers. This capital position remains a key focus for investors considering the company’s long-term outlook.

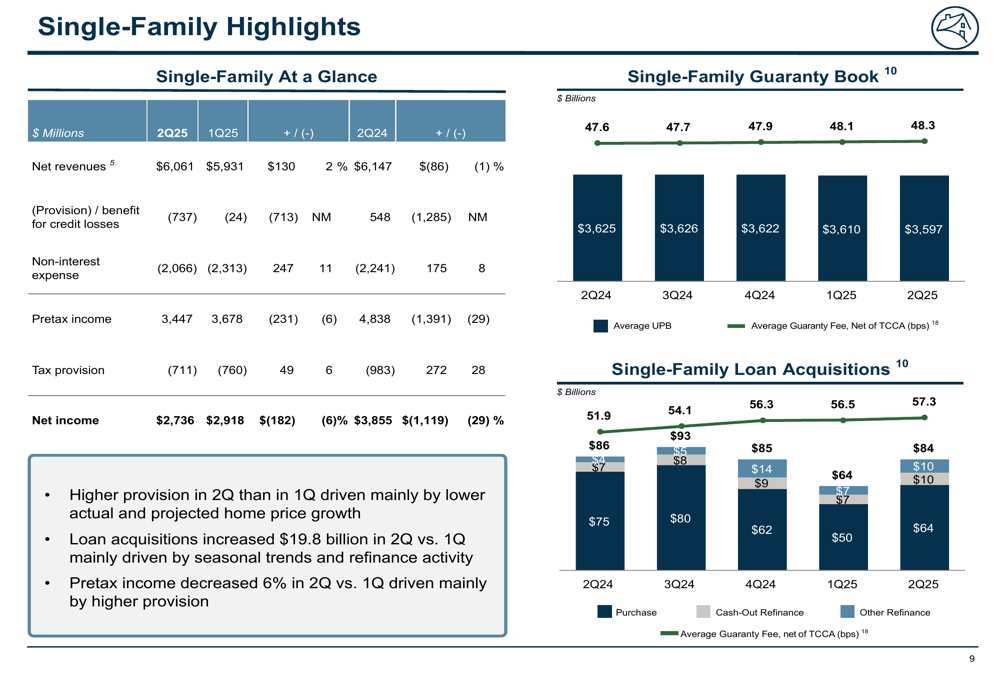

Business Segment Performance

Fannie Mae’s single-family business, which represents the bulk of its operations, generated $2.7 billion in net income during Q2 2025, down from $2.9 billion in Q1 2025 and $3.9 billion in Q2 2024. Single-family loan acquisitions declined significantly to $50 billion, down 21.9% from $64 billion in the previous quarter.

The following chart details the single-family segment’s performance:

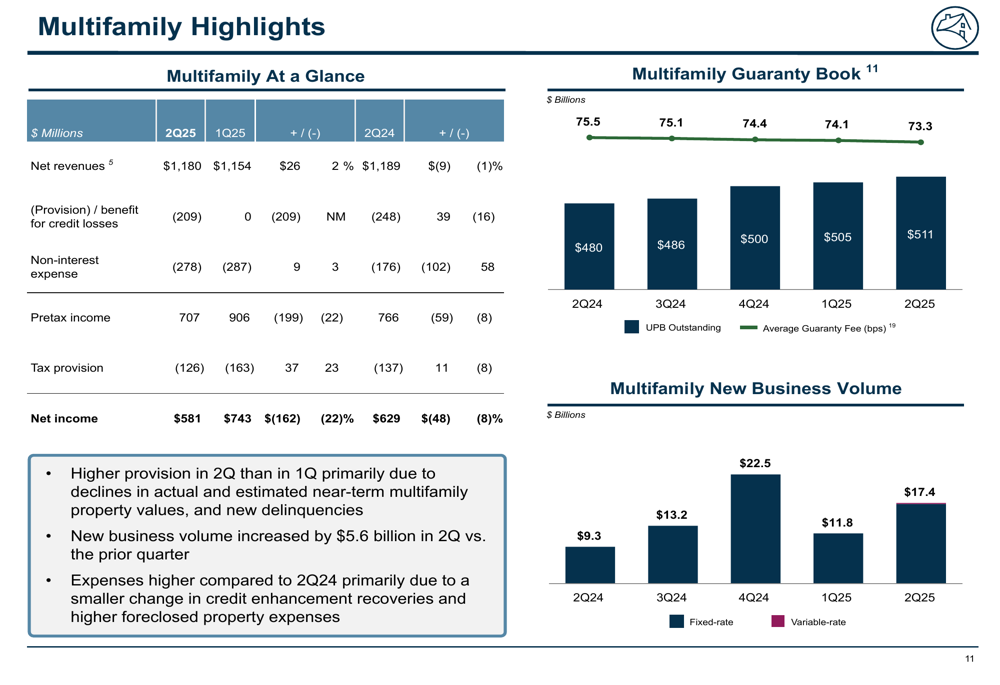

Meanwhile, the multifamily business showed more resilience, with net income of $581 million in Q2 2025, though this was down from $743 million in Q1 2025. New business volume in this segment increased substantially to $17.4 billion, up 47.5% from $11.8 billion in the previous quarter.

The multifamily segment’s performance is illustrated in the following chart:

Forward-Looking Statements

Fannie Mae continues to make progress on its strategic initiatives, including a newly announced partnership with Palantir Technologies (NASDAQ:PLTR) to enhance mortgage fraud detection and prevention capabilities. The company also highlighted its improved Fortune 500 ranking, now standing at #25.

Looking ahead, Fannie Mae faces several challenges, including continued pressure on its single-family acquisition volumes amid higher mortgage rates and housing affordability concerns. The increased provisions for credit losses suggest management anticipates potential deterioration in credit performance, despite currently stable delinquency metrics.

The company’s progress toward meeting regulatory capital requirements remains a critical focus, with the $101.6 billion net worth milestone representing significant progress but still falling short of the required thresholds. This capital position will continue to influence the company’s strategic decisions and potential path toward exiting conservatorship.

For investors, Fannie Mae’s declining quarterly profits amid stable revenue highlight the challenges of managing credit risk in the current economic environment, while the improving capital position provides a more solid foundation for future operations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.