Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

Fast Retailing Co Ltd (TYO:9983), the parent company of UNIQLO, presented its fiscal year 2025 results and FY2026 estimates on October 9, 2025. The company reported its fourth consecutive record annual performance, with significant revenue and profit growth across most regions. Chief Financial Officer Takeshi Okazaki delivered the presentation, highlighting the company’s successful global expansion strategy and improved operational efficiency.

Financial Performance Highlights

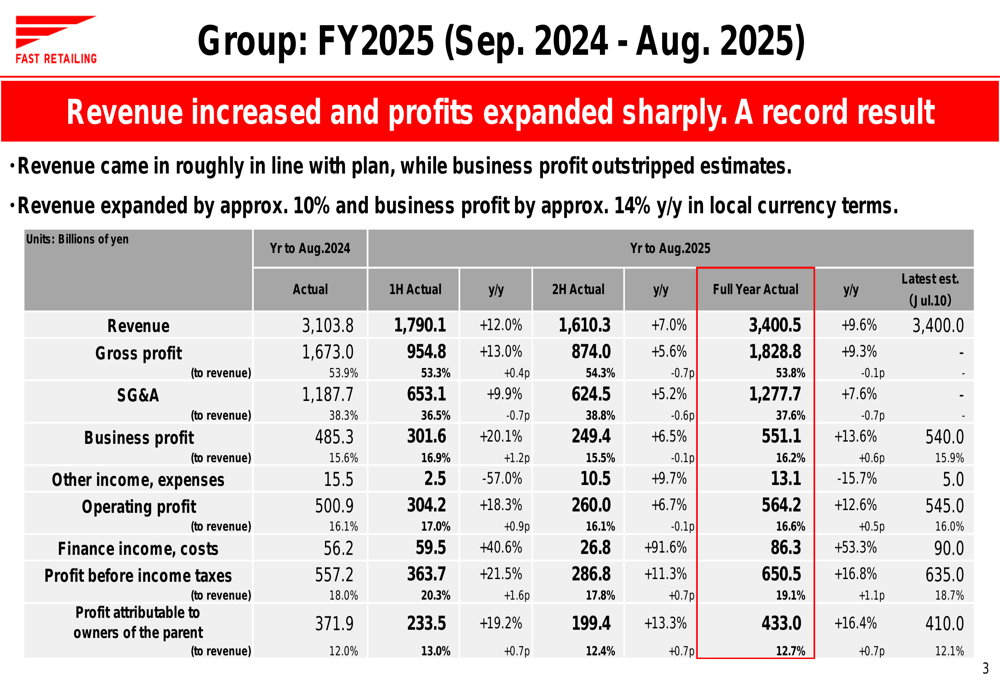

Fast Retailing achieved substantial growth in FY2025 (September 2024 - August 2025), with revenue increasing 9.6% to ¥3,400.5 billion and business profit rising 13.6% to ¥551.1 billion. Operating profit grew 12.6% to ¥564.2 billion, while profit attributable to owners of the parent jumped 16.4% to ¥433.0 billion.

The company’s business profit margin improved to 16.2%, up 0.6 percentage points from the previous year, reflecting enhanced operational efficiency and better inventory management, particularly in the fourth quarter.

As shown in the following comprehensive financial overview:

The results were roughly in line with revenue plans but exceeded business profit estimates. The company noted that both revenue and business profit grew significantly in local currency terms, demonstrating strong underlying performance despite currency fluctuations.

Segment Analysis

Fast Retailing’s performance varied across its business segments, with UNIQLO operations showing particularly strong results.

UNIQLO Japan

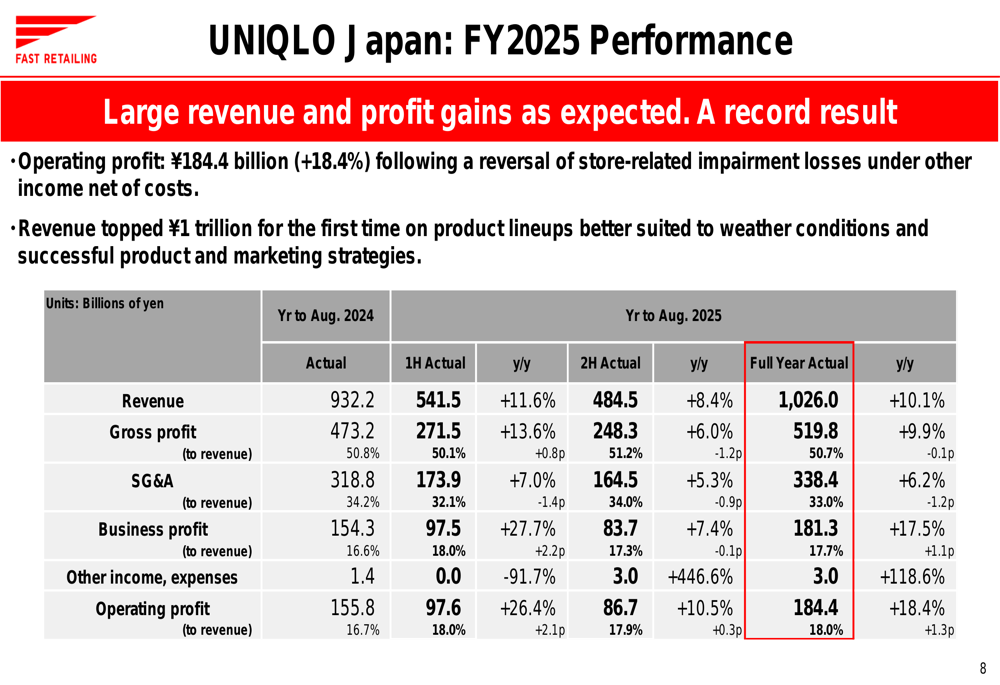

UNIQLO Japan achieved a significant milestone by exceeding ¥1 trillion in revenue for the first time. Revenue increased 10.1% to ¥1,026.0 billion, while business profit rose 17.5% to ¥181.3 billion. Same-store sales grew 8.1% year-over-year, with first-half sales up 9.8% and second-half sales up 6.2%.

The segment’s success was attributed to better product offerings aligned with weather conditions, improved marketing coordination, and the incorporation of trending designs into core items. Tourism also played a significant role, with sales to visitors to Japan expanding to approximately 9% of total sales.

The following table details UNIQLO Japan’s financial performance:

E-commerce continued to grow, with online sales increasing 11.2% to ¥152.3 billion, representing 14.8% of total UNIQLO Japan sales.

UNIQLO International

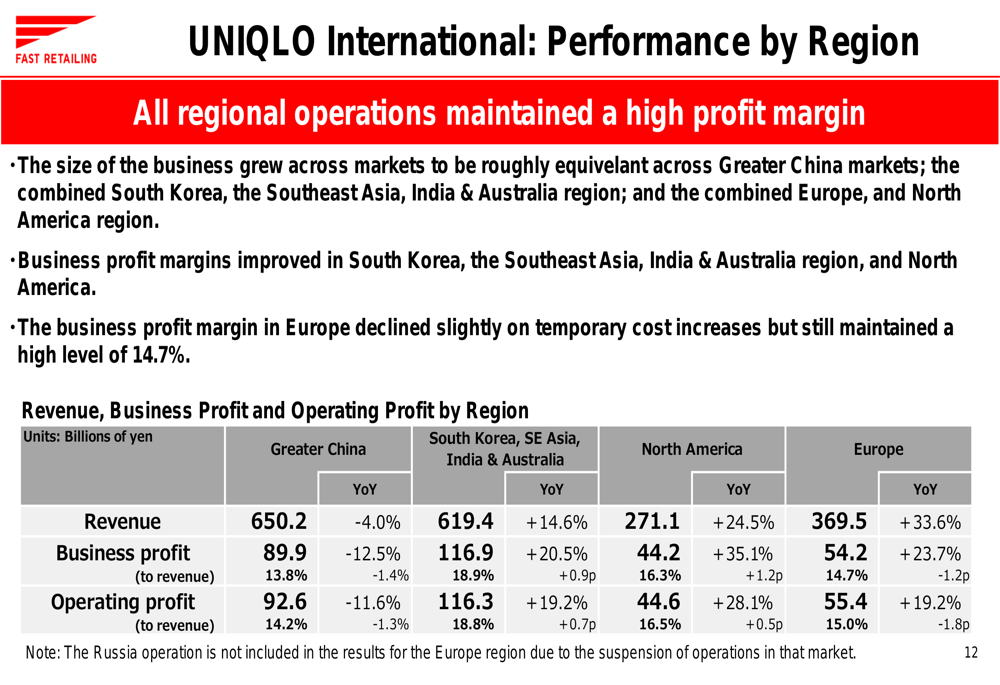

UNIQLO International delivered strong performance with revenue up 11.6% to ¥1,910.3 billion and business profit increasing 10.6% to ¥305.3 billion. In local currency terms, revenue expanded by approximately 13% and business profit by about 12%.

The regional breakdown shows varied performance across markets:

North America, Europe, South Korea, and Southeast Asia/India/Australia regions showed robust growth, while Greater China experienced challenges. The company noted that structural reforms in the Greater China market are progressing as planned, with benefits expected in the medium term.

GU

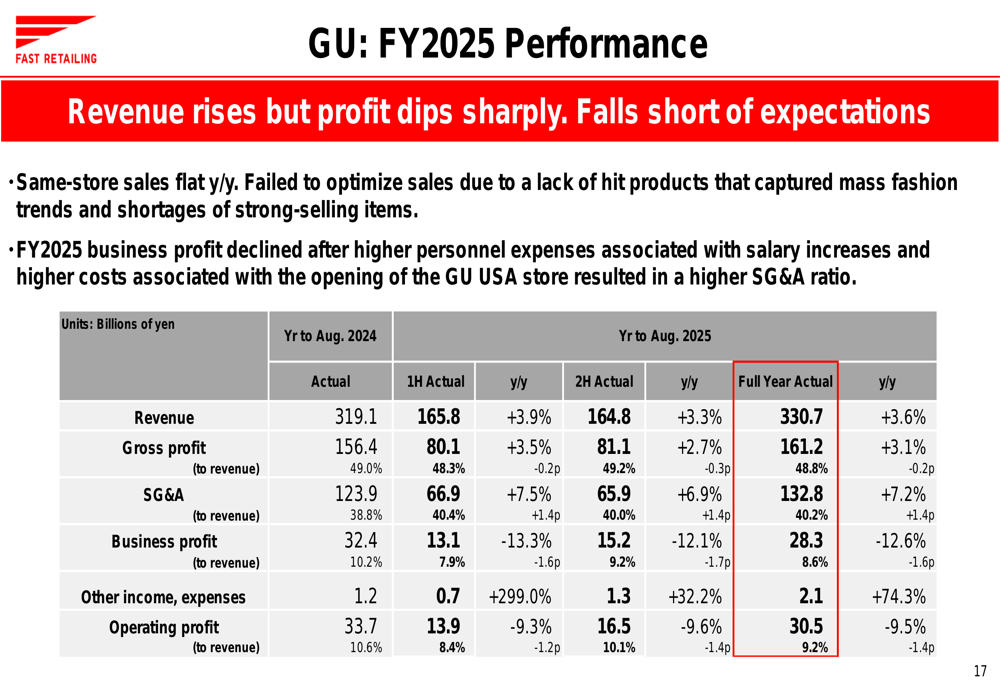

The GU segment reported mixed results, with revenue increasing 3.6% to ¥330.7 billion but business profit declining 12.6% to ¥28.3 billion. This profit decline was attributed to increased SG&A expenses, which rose 7.2% year-over-year.

The following chart illustrates GU’s financial performance:

Global Brands

The Global Brands segment saw revenue decline 5.3% to ¥131.5 billion, primarily due to sluggish Theory sales. However, business profit increased as Comptoir des Cotonniers losses were halved. Despite the profit improvement, the segment fell short of the company’s plan.

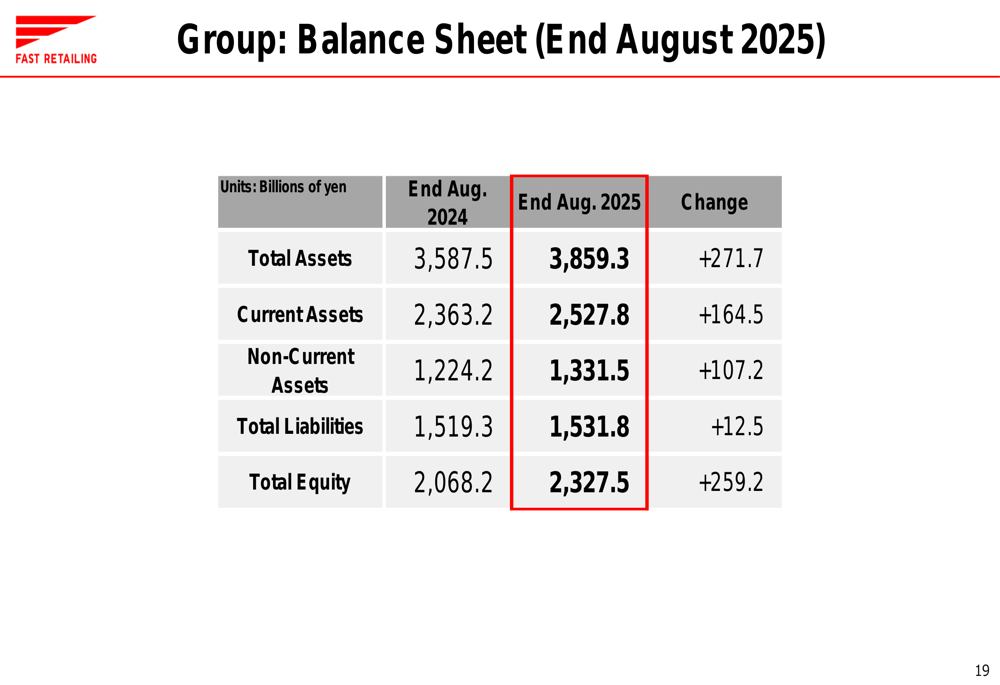

Balance Sheet and Cash Flow

Fast Retailing maintained a strong financial position, with total assets increasing to ¥3,859.3 billion as of August 31, 2025, up from ¥3,587.5 billion a year earlier. Total equity rose to ¥2,327.5 billion, reflecting the company’s strong profitability.

The following balance sheet summary provides more details:

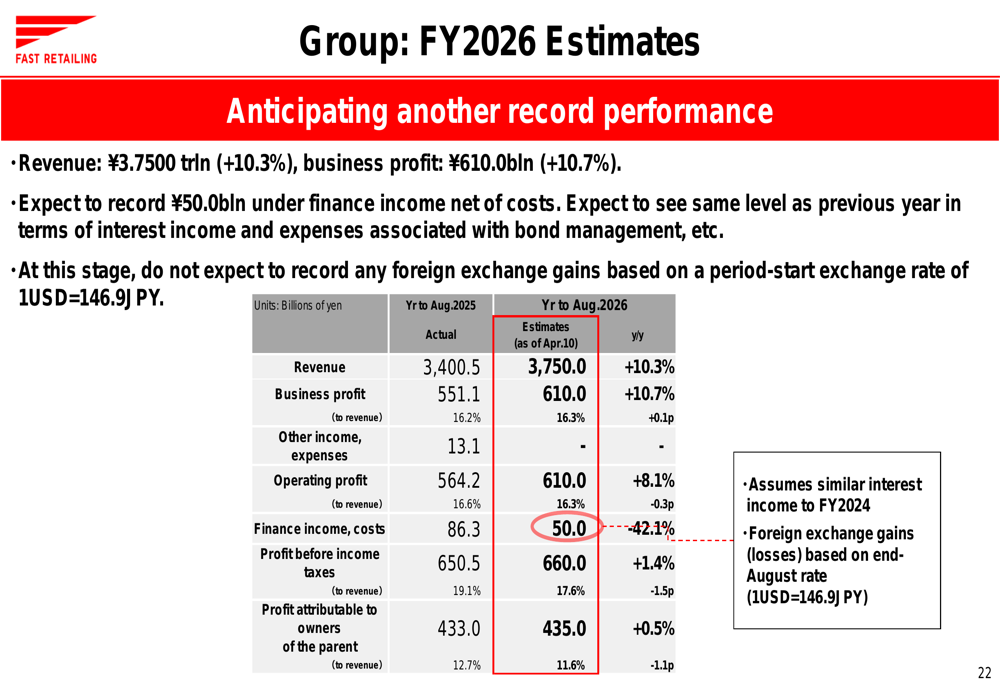

FY2026 Outlook

Fast Retailing provided an optimistic outlook for FY2026, projecting revenue to increase 10.3% to ¥3.75 trillion and business profit to rise 10.7% to ¥610.0 billion.

The company’s forward-looking estimates are summarized in the following chart:

By segment, UNIQLO International is expected to lead growth with significant revenue and profit gains across all regions. UNIQLO Japan is projected to achieve steady growth, while GU is anticipated to recover with revenue and profit increases. Global Brands is forecast to see revenue gains and a large rise in profits.

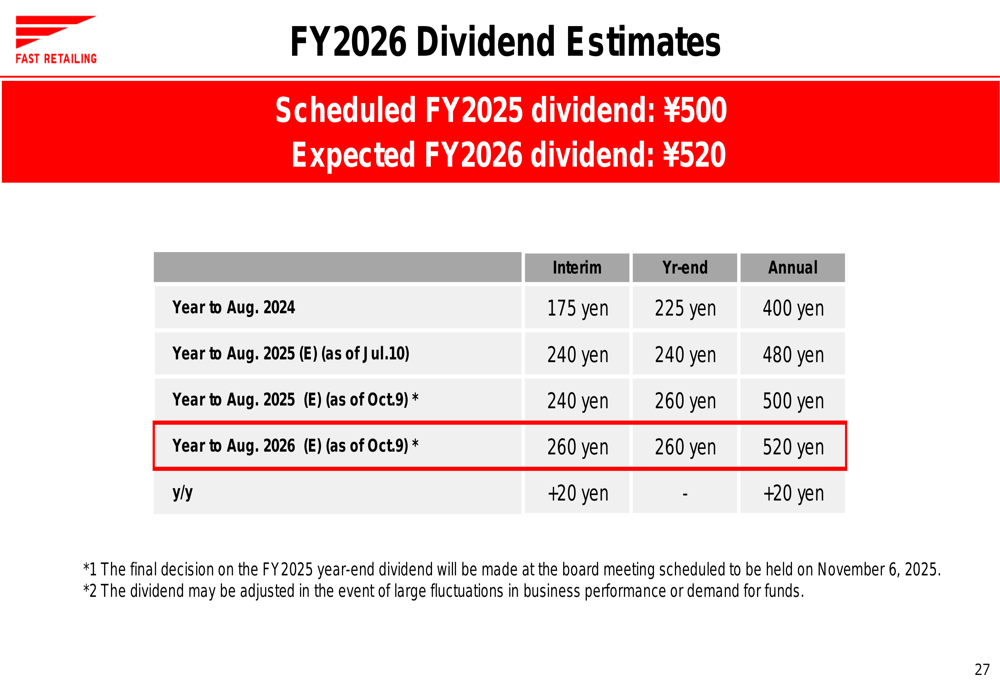

For shareholders, Fast Retailing announced a scheduled FY2025 dividend of ¥500 per share and expects to increase the dividend to ¥520 per share in FY2026, demonstrating confidence in continued strong performance.

Strategic Initiatives

Fast Retailing highlighted its continued focus on opening quality stores globally, with successful new locations contributing to performance. The company emphasized its increased presence in North America and Europe, while also noting the progress of structural reforms in UNIQLO Mainland China and GU operations.

The company’s operational improvements were evident in the enhanced business profit margin and improved inventory management. Fast Retailing also continued to expand its e-commerce capabilities, with online sales growing as a percentage of total revenue.

Forward-Looking Statements

Looking ahead, Fast Retailing expects to maintain its growth trajectory through continued global expansion, operational improvements, and strategic investments. The company anticipates benefits from its structural reforms in China and GU to materialize in the medium term, contributing to future performance.

The projected 10.3% revenue growth and 10.7% business profit growth for FY2026 reflect management’s confidence in the company’s business model and market positioning, despite ongoing global economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.