AirNet Technology raises $180 million in digital assets offering

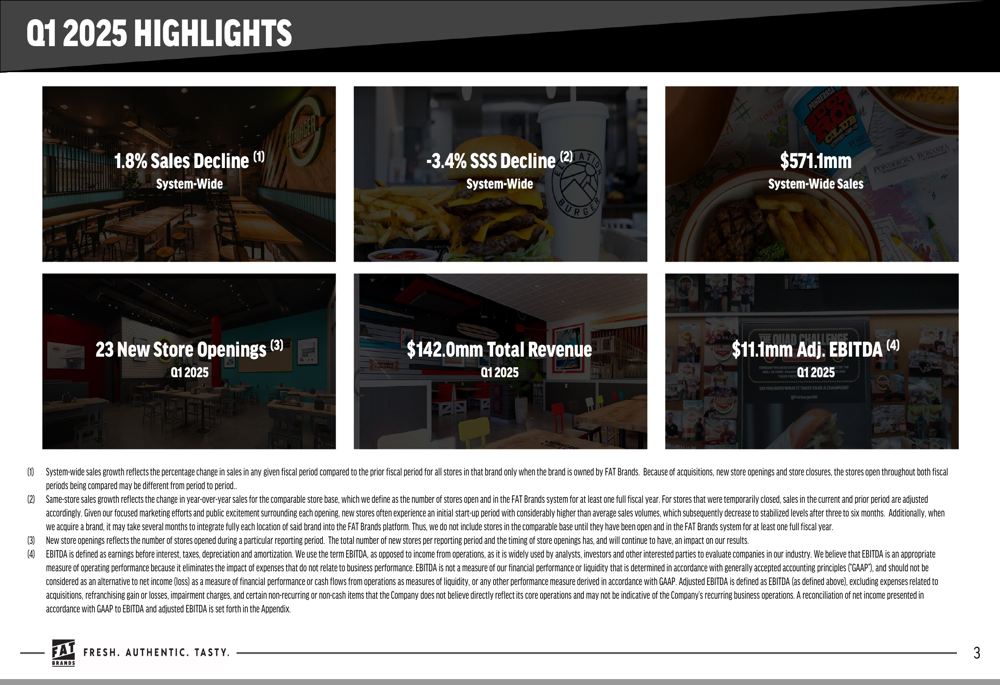

FAT Brands Inc (NASDAQ:FAT) reported continued revenue declines in its Q1 2025 earnings presentation released on May 8, 2025, with total revenue falling to $142.0 million, down 6.6% from $152.0 million in the same period last year. Despite these challenges, the multi-brand restaurant franchisor is maintaining an aggressive growth strategy focused on new store openings and operational improvements.

Quarterly Performance Highlights

FAT Brands, which owns popular restaurant chains including Fatburger, Twin Peaks, Round Table Pizza, and Johnny Rockets, reported system-wide sales of $571.1 million for Q1 2025, representing a 1.8% decline from the $581.8 million reported in Q1 2024. Same-store sales decreased by 3.4% across the company’s portfolio of brands.

As shown in the following summary of Q1 2025 highlights:

The company opened 23 new stores during the quarter, continuing its expansion efforts despite the challenging sales environment. Royalty revenue remained relatively stable at $21.8 million compared to $21.9 million in the prior year period, suggesting that the company’s franchise model continues to generate consistent recurring revenue despite broader sales challenges.

Detailed Financial Analysis

The financial comparison between Q1 2025 and Q1 2024 reveals concerning trends across key metrics, with revenue, system-wide sales, and adjusted EBITDA all showing year-over-year declines:

Particularly concerning is the significant drop in adjusted EBITDA, which fell to $11.1 million in Q1 2025, down approximately 39% from $18.2 million in Q1 2024. This substantial decline suggests the company is facing increased pressure on profitability despite relatively modest decreases in top-line metrics.

The consolidated statement of operations reveals that FAT Brands’ net loss attributable to shareholders widened to $46.0 million in Q1 2025, compared to $38.3 million in the same period last year. This deterioration was driven by both operational challenges and high interest expenses of $31.4 million, highlighting the company’s significant debt burden.

Strategic Initiatives

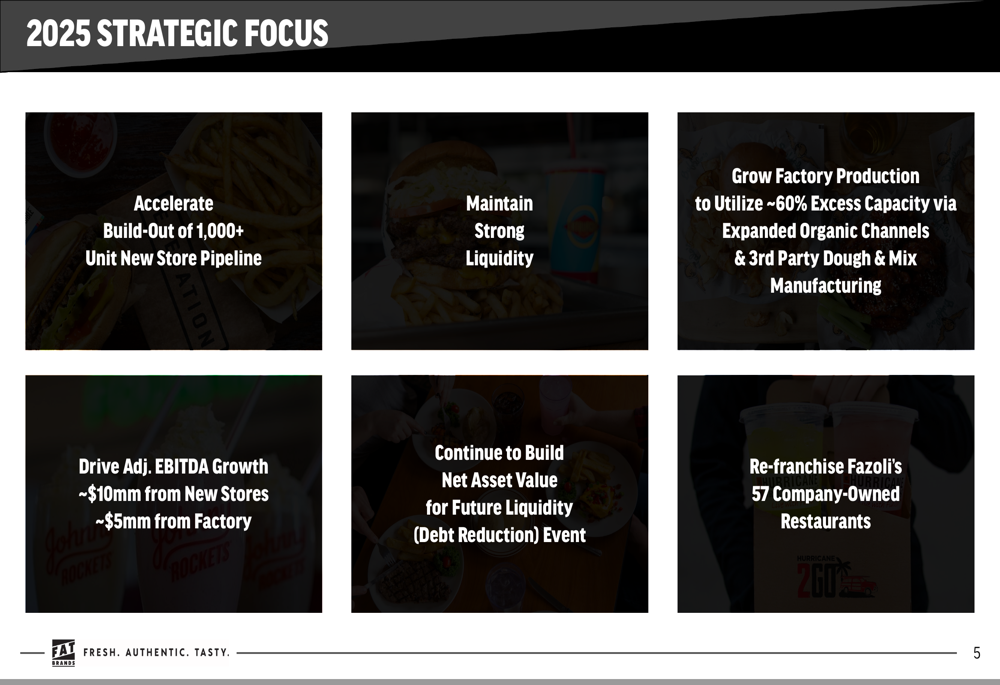

Despite the financial headwinds, FAT Brands outlined an ambitious strategic plan for 2025, focusing on expansion, operational improvements, and debt reduction:

A key element of the strategy involves accelerating the build-out of the company’s 1,000+ unit new store pipeline, which management believes will drive significant future growth. The company also plans to re-franchise Fazoli’s 57 company-owned restaurants, a move that aligns with its predominantly franchise-based business model and could improve capital efficiency.

Additionally, FAT Brands aims to grow factory production to utilize approximately 60% of excess capacity through expanded organic channels and third-party dough and mix manufacturing. Management expects this initiative to contribute approximately $5 million in adjusted EBITDA growth, while new store openings are projected to add approximately $10 million.

Market Context and Stock Performance

FAT Brands’ stock has shown modest improvement recently, with shares trading at $2.88 during regular market hours on May 8, 2025, representing a 2.86% increase. In after-hours trading, the stock gained an additional 4.17% to reach $3.00 per share, suggesting investors may see potential in the company’s growth strategy despite current financial challenges.

This modest stock performance comes against the backdrop of continued operational difficulties. The company’s previous earnings report for Q4 2024 had also shown revenue declines, with total revenue decreasing by 8.4% to $145.3 million and a net loss of $67.4 million reported for that quarter.

Forward-Looking Statements

FAT Brands’ focus on building net asset value for a future liquidity event suggests management is prioritizing debt reduction, which would address one of the company’s most significant challenges. With total debt reported at $1.54 billion as of Q3 2024 (according to previous earnings reports), and high quarterly interest expenses continuing to impact profitability, improving the balance sheet remains critical.

The company’s strategic focus on expanding its store network while simultaneously working to improve factory utilization represents a balanced approach to growth and operational efficiency. If successful, these initiatives could help offset the current negative trends in same-store sales and overall revenue.

However, investors should note that the continued decline in same-store sales (-3.4%) represents a fundamental challenge that could undermine expansion efforts if not reversed. The company will need to address these underlying performance issues while executing on its growth strategy to achieve sustainable long-term improvement in financial results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.