Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

FAT Brands Inc. (NASDAQ:FAT) released its Q2 2025 earnings presentation on July 30, 2025, revealing continued revenue challenges amid an ambitious expansion strategy. The multi-brand restaurant company, which operates chains including Fatburger, Twin Peaks, and Johnny Rockets, reported system-wide sales declines while maintaining its adjusted EBITDA levels. The stock closed at $2.40, down 0.83% for the day, and fell an additional 1.67% in after-hours trading to $2.36.

As shown in the company’s presentation cover, FAT Brands continues to operate a diverse portfolio of restaurant concepts across various segments:

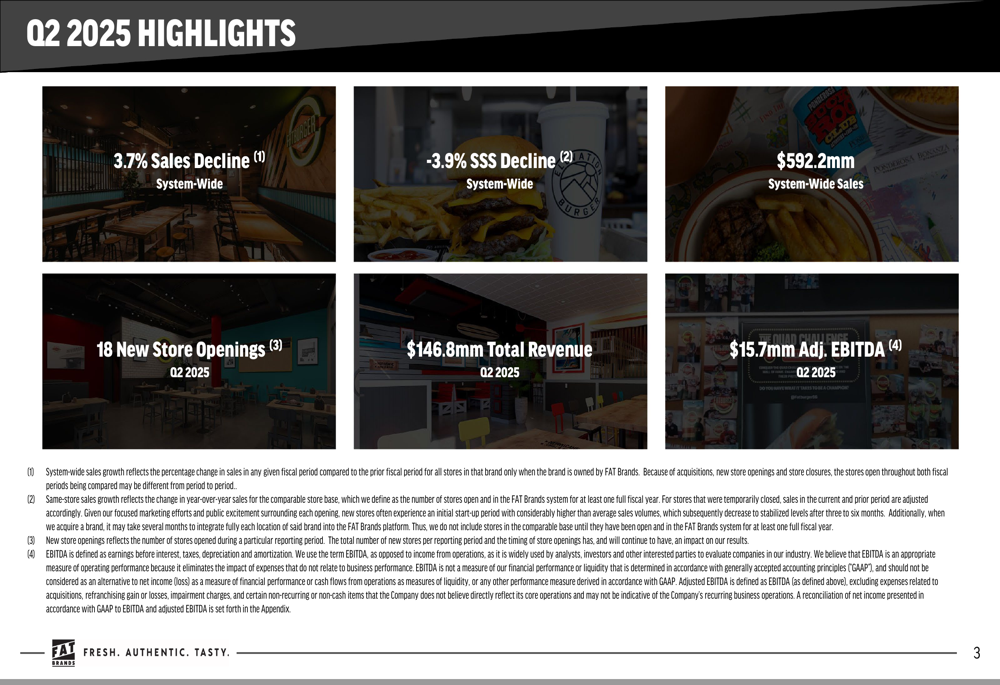

Quarterly Performance Highlights

FAT Brands reported a 3.7% system-wide sales decline and a 3.9% same-store sales decrease in Q2 2025. Despite these challenges, the company opened 18 new locations during the quarter and maintained its adjusted EBITDA at $15.7 million, unchanged from the same period last year. Total (EPA:TTEF) revenue reached $146.8 million, with system-wide sales of $592.2 million.

The following slide illustrates these key performance metrics for the quarter:

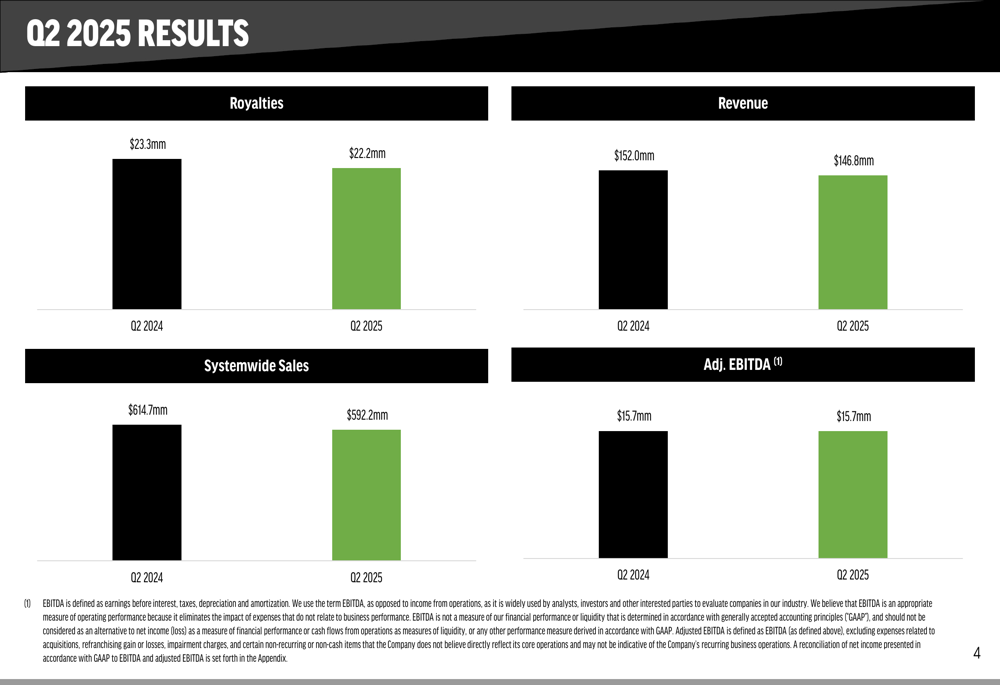

Comparing Q2 2025 results to the same period in 2024 shows the extent of the revenue challenges. Total revenue decreased from $152.0 million to $146.8 million, while system-wide sales fell from $614.7 million to $592.2 million. Royalties also declined from $23.3 million to $22.2 million. However, the company managed to maintain its adjusted EBITDA at $15.7 million despite these headwinds.

This comparative performance is illustrated in the following chart:

Detailed Financial Analysis

The company’s consolidated statement of operations reveals a net loss of $55.369 million for the thirteen weeks ended June 29, 2025. The net loss attributable to FAT Brands Inc. was $54.188 million, representing a significant increase from the $46 million net loss reported in Q1 2025. This suggests that despite maintaining adjusted EBITDA levels, the company’s bottom line continues to deteriorate.

The reconciliation of net loss to adjusted EBITDA shows that the $15.695 million adjusted EBITDA for Q2 2025 includes significant adjustments to the reported EBITDA of $(5.980) million. These adjustments include items such as share-based compensation expenses, litigation costs, and pre-opening expenses, highlighting the gap between the company’s adjusted metrics and its GAAP financial performance.

After adjustments, the company’s adjusted net loss was $48.956 million for the quarter, still representing a substantial negative figure despite the positive adjusted EBITDA. This continues a trend seen in Q1 2025, where the company reported an adjusted net loss of $38.7 million.

Strategic Initiatives

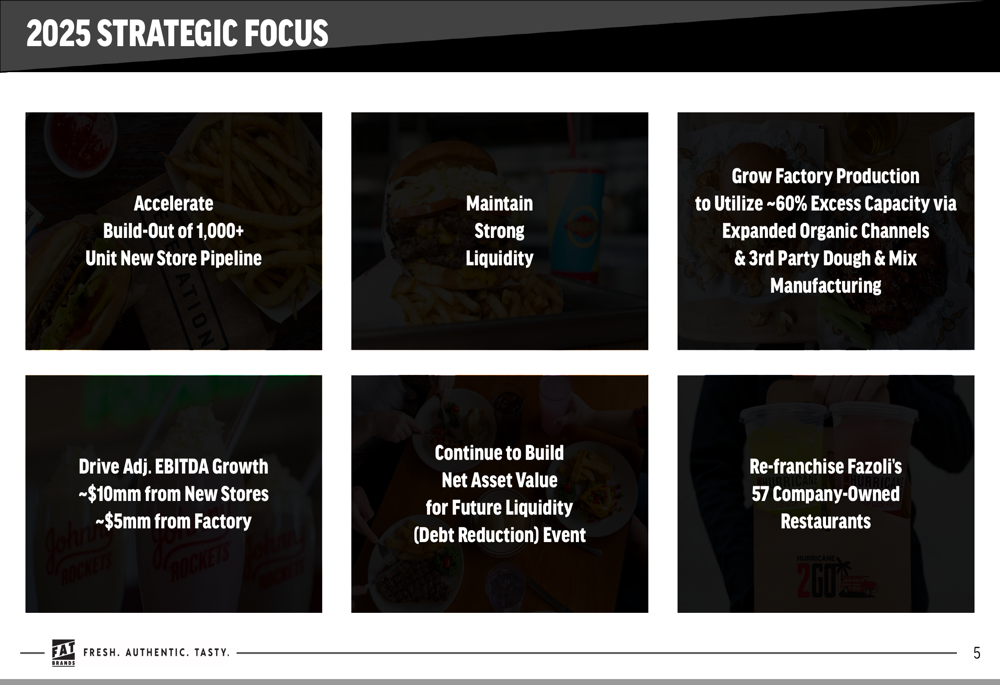

Despite ongoing financial challenges, FAT Brands outlined an ambitious strategic plan for 2025, focusing on expansion and operational improvements. The company aims to accelerate the build-out of its 1,000+ unit new store pipeline while maintaining strong liquidity. Additionally, it plans to grow factory production to utilize approximately 60% of excess capacity through expanded organic channels and third-party dough and mix manufacturing.

The strategic roadmap also includes driving adjusted EBITDA growth of approximately $10 million from new stores and $5 million from factory operations. The company continues to build net asset value for a future liquidity event focused on debt reduction, and plans to re-franchise Fazoli’s 57 company-owned restaurants.

These strategic initiatives are outlined in the following slide:

Forward-Looking Statements

FAT Brands’ forward-looking strategy suggests confidence in its expansion plans despite current financial challenges. The company’s focus on new store openings indicates a belief that growth will eventually overcome the current same-store sales declines. The emphasis on debt reduction acknowledges the company’s substantial debt burden, which stood at $1.57 billion as of Q1 2025 reporting.

The re-franchising of Fazoli’s restaurants appears to be part of a broader strategy to shift toward an asset-light business model, potentially improving cash flow and reducing operational costs. Meanwhile, the focus on factory production suggests an attempt to diversify revenue streams beyond traditional restaurant operations.

However, investors should note the significant gap between the company’s adjusted EBITDA figures and its substantial net losses, which may indicate ongoing structural challenges in the business model. The continued decline in system-wide sales and same-store sales also raises questions about the long-term viability of the expansion strategy if consumer demand continues to weaken.

As FAT Brands navigates these challenges, the market will be watching closely to see if its strategic initiatives can reverse the negative trends in revenue and profitability while managing its substantial debt load.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.