Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Ferrari (BIT:RACE) N.V. (NYSE:RACE) reported robust first-quarter 2025 results on May 6, showcasing strong financial performance despite minimal growth in vehicle shipments. The Italian luxury sports car manufacturer continues to leverage its premium positioning and product mix strategy to drive revenue and profitability growth in an evolving automotive landscape.

The company’s stock closed at $466.46 on May 5, 2025, up 0.78% ahead of the earnings release, though it was trading down 1.33% in premarket activity following the announcement. Ferrari’s shares have performed well over the past year, trading near the upper end of their 52-week range ($391.54-$509.13).

Quarterly Performance Highlights

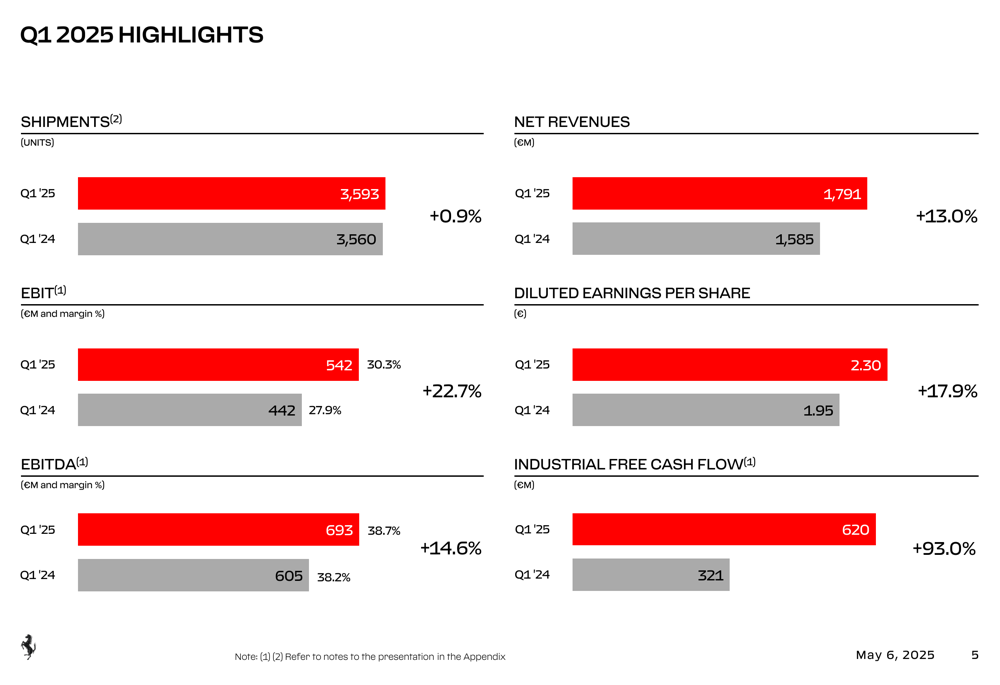

Ferrari delivered impressive financial results for Q1 2025, with revenue reaching €1.8 billion, a 13.0% increase compared to the same period in 2024. This substantial growth came despite only a modest 0.9% increase in vehicle shipments (3,593 units vs. 3,560 units in Q1 2024), highlighting the company’s successful strategy of enhancing revenue per vehicle through premium pricing and personalization.

Net profit rose to €412 million, up 17.0% from €352 million in Q1 2024, while diluted earnings per share increased by 17.9% to €2.30. The company’s operating profit (EBIT) showed even stronger growth, jumping 22.7% to €542 million, with the EBIT margin expanding to 30.3% from 27.9% in the prior-year period.

As shown in the following chart of key financial highlights, Ferrari demonstrated growth across all major financial metrics:

Industrial free cash flow was particularly impressive, nearly doubling year-over-year to €620 million, a 93.0% increase from €321 million in Q1 2024. This substantial improvement in cash generation underscores the company’s operational efficiency and strong financial health.

Product Mix and Regional Analysis

Ferrari’s product strategy continues to evolve, with hybrid vehicles now accounting for 49% of total shipments, up significantly from previous periods. This shift reflects the company’s gradual transition toward electrification while maintaining its focus on performance and exclusivity. The quarter also saw the unveiling of two new models: the Ferrari 296 Speciale and 296 Speciale A.

The following image showcases these new additions to Ferrari’s lineup:

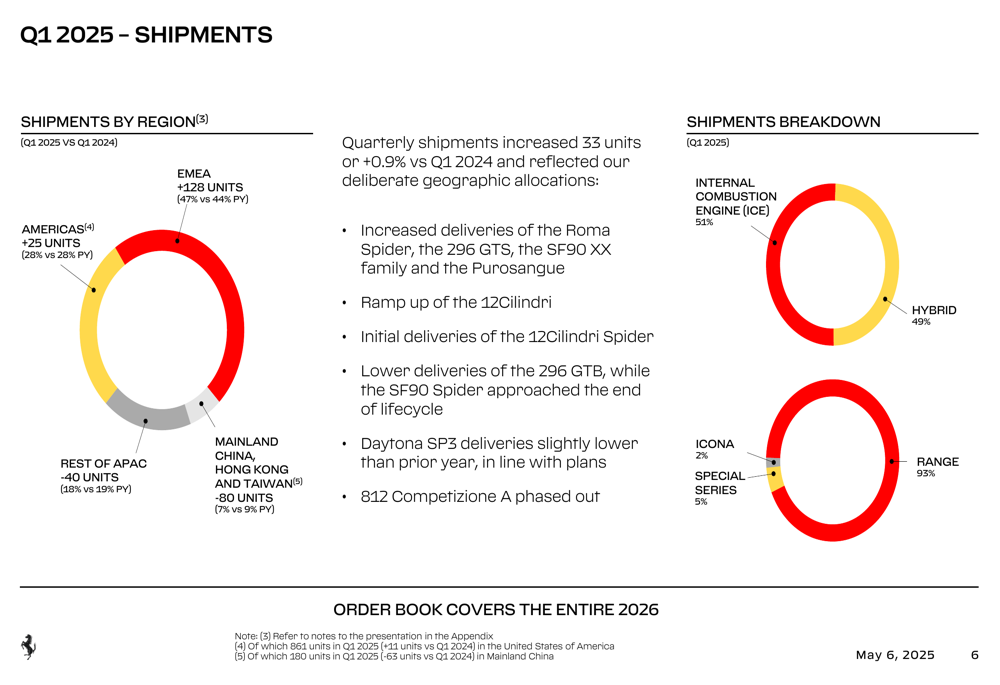

From a regional perspective, Ferrari implemented deliberate geographic allocations to maintain exclusivity and balance market exposure. EMEA (Europe, Middle East, and Africa) saw an increase in shipment share from 44% to 47%, while Mainland China, Hong Kong, and Taiwan decreased from 9% to 7% of total shipments. The Americas region maintained its 28% share of deliveries.

The regional breakdown of shipments is illustrated in the following chart:

Financial Analysis

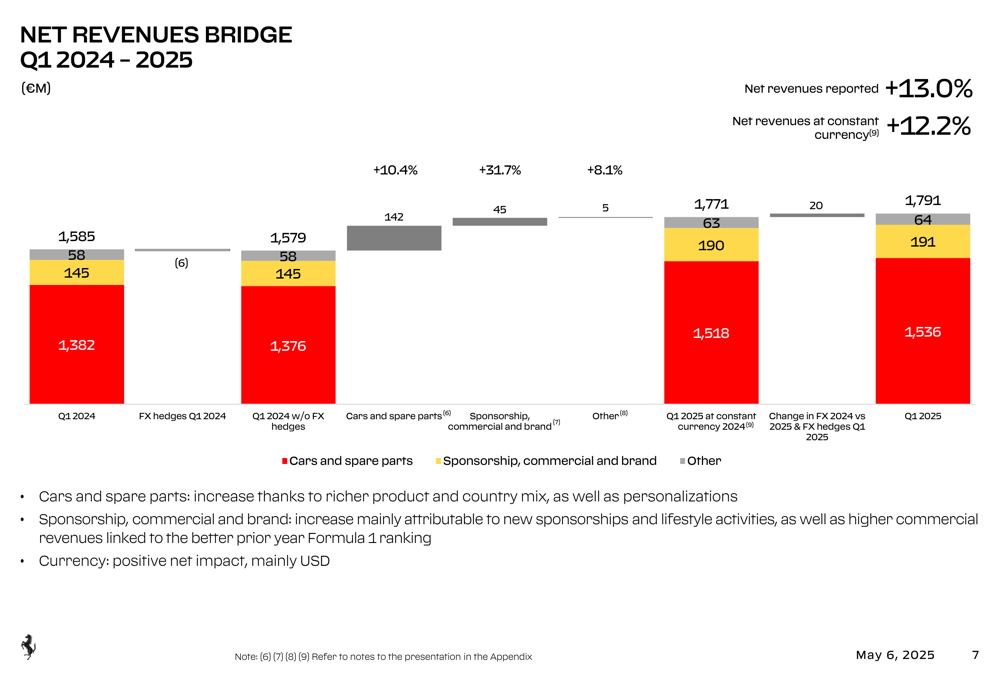

Ferrari’s revenue growth of 13.0% (12.2% at constant currency) was primarily driven by an enriched product mix, increased personalization, and stronger contributions from sponsorship and brand activities. The company’s cars and spare parts segment, which accounts for the bulk of revenue, benefited from a richer product mix including models like the SF90 XX, 12Cilindri, and 499P Modificata.

The following bridge chart illustrates the factors contributing to revenue growth between Q1 2024 and Q1 2025:

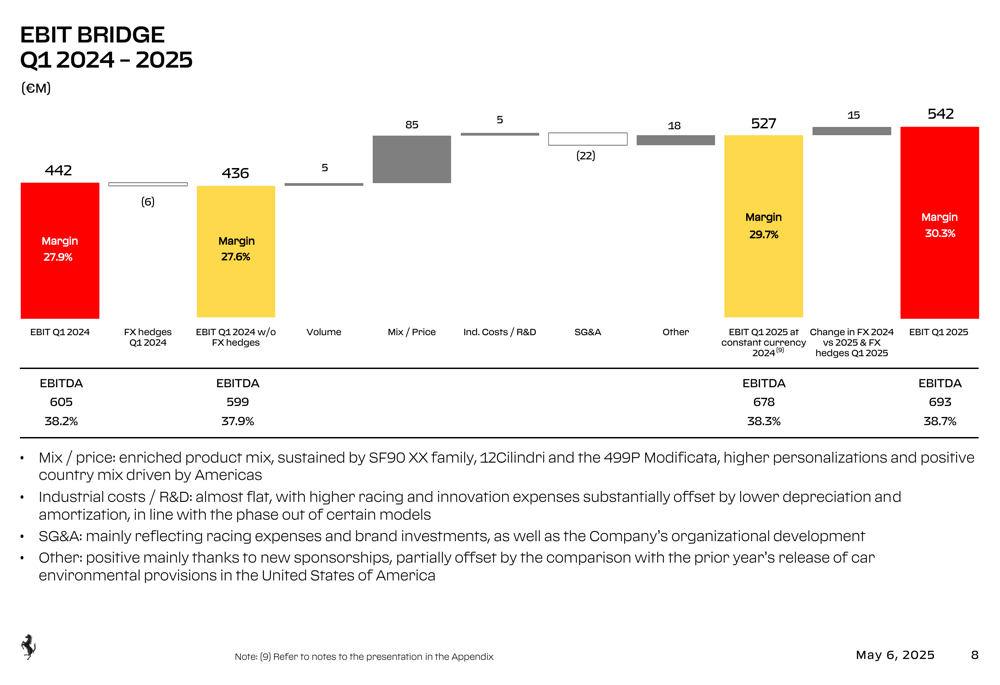

On the profitability front, Ferrari’s EBIT increased by 22.7% to €542 million, with margin expansion from 27.9% to 30.3%. This improvement was primarily driven by the favorable product mix and pricing, which more than offset increases in industrial costs, R&D, and SG&A expenses. The company’s EBITDA also grew by 14.6% to €693 million, with the margin improving to 38.7%.

The factors influencing EBIT growth are detailed in the following bridge chart:

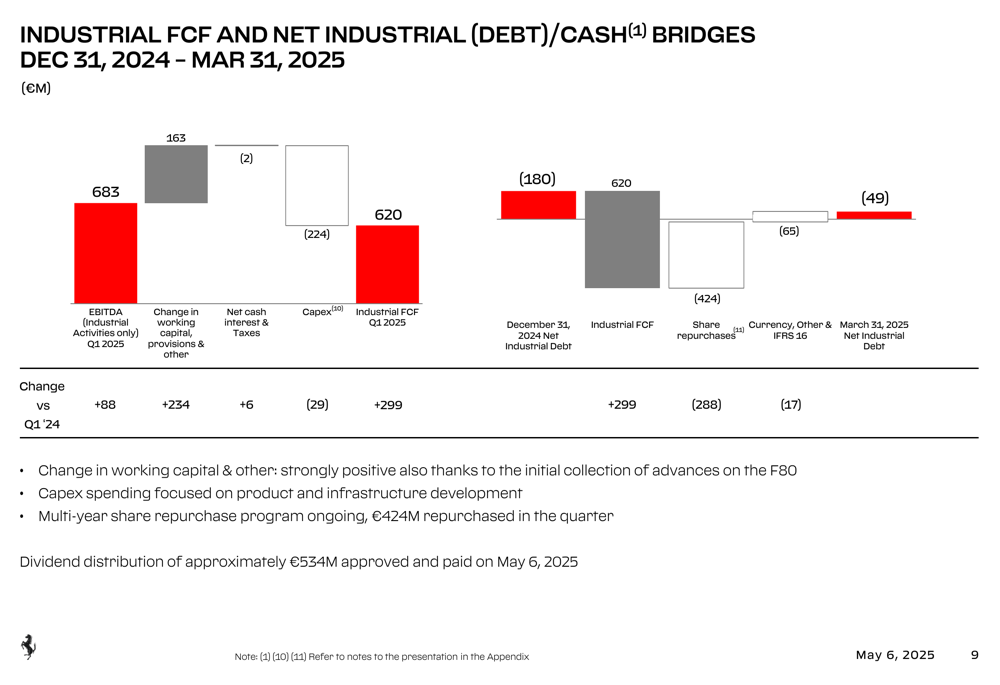

Ferrari’s strong cash flow performance resulted in a significant improvement in its financial position. The company generated €620 million in Industrial Free Cash Flow during Q1 2025, despite ongoing investments in product development and infrastructure. Capital expenditures for the quarter totaled €224 million, including €110 million in capitalized development costs.

The following chart illustrates the bridge from EBITDA to Industrial Free Cash Flow and the evolution of the company’s net industrial debt position:

Forward Guidance and Outlook

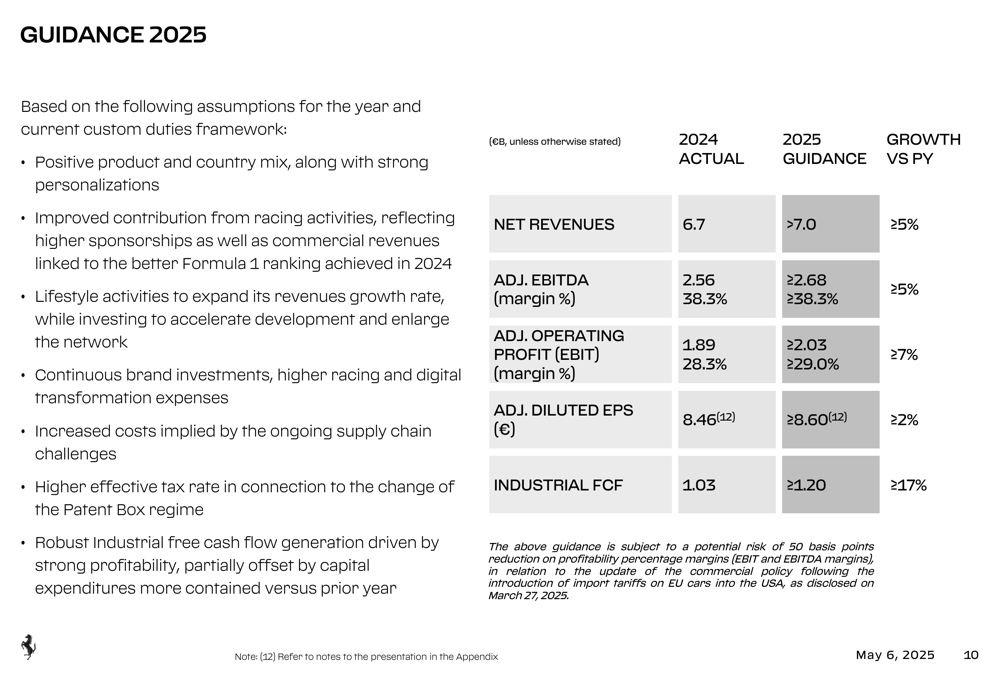

Ferrari maintained a confident outlook for 2025, projecting net revenues to exceed €7.0 billion, representing growth of at least 5% compared to 2024. The company expects to maintain strong profitability, with an adjusted EBITDA margin of approximately 38.3% or higher and adjusted operating profit exceeding €2.03 billion.

The guidance is based on assumptions including positive product and country mix, improved contributions from racing activities, continued lifestyle activities, and ongoing brand investments. However, Ferrari did note a potential risk of a 50 basis point reduction in profitability margins related to the update of its commercial policy following the introduction of import tariffs on EU cars into the United States.

The company’s full-year guidance is summarized in the following table:

Ferrari’s order book remains robust, covering the entire 2026 production, which provides significant visibility and stability for the company’s future performance. This strong demand backdrop, combined with Ferrari’s continued focus on exclusive, high-performance vehicles and gradual shift toward electrification, positions the company well for sustained growth despite potential macroeconomic challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.