Robinhood reports August 2025 customer and trading metrics

Introduction & Market Context

FibroGen Inc . (NASDAQ:FGEN) presented its second quarter 2025 financial results on August 11, revealing a strategic transformation centered around the sale of its China operations while advancing key clinical programs. The presentation came as the company reported disappointing financial results, with an EPS of -$1.88 versus expectations of -$0.09 and revenue of $1.3 million against a forecast of $2.88 million.

The biotech firm, currently valued at approximately $34 million, saw its stock drop 3.9% following the earnings announcement, closing at $8.71. Despite these financial challenges, FibroGen’s presentation highlighted significant progress in its clinical pipeline and strategic initiatives designed to extend its cash runway.

Strategic Initiatives

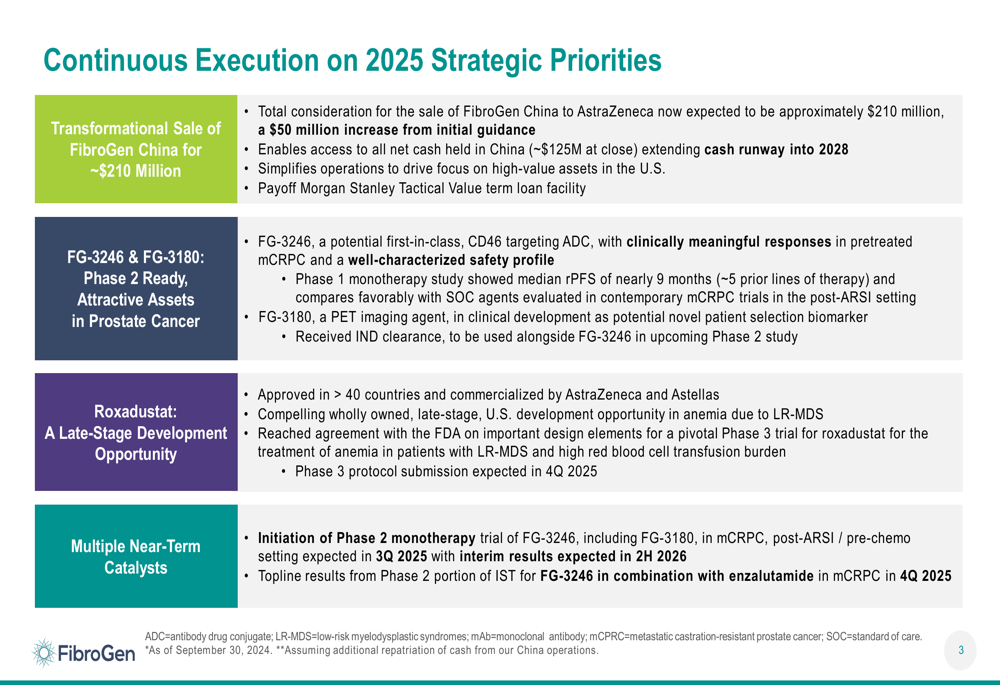

The cornerstone of FibroGen’s strategic transformation is the sale of its China operations, which the company described as "transformational" in its presentation. The deal, valued at approximately $210 million, includes an enterprise value of $85 million plus access to approximately $125 million of FibroGen net cash held in China.

This transaction, expected to close in Q3 2025, represents a significant balance sheet transformation for the company. The proceeds will be used in part to pay off FibroGen’s MSTV term loan facility at closing, with the remaining funds extending the company’s cash runway into 2028.

The extended runway provides FibroGen with substantial operational flexibility as it advances its clinical programs. This financial cushion is particularly important given the company’s current financial performance, with operating costs decreasing by 72% year-over-year to $13.4 million and R&D expenses down 82% to $5.9 million in Q2 2025.

Clinical Pipeline Highlights

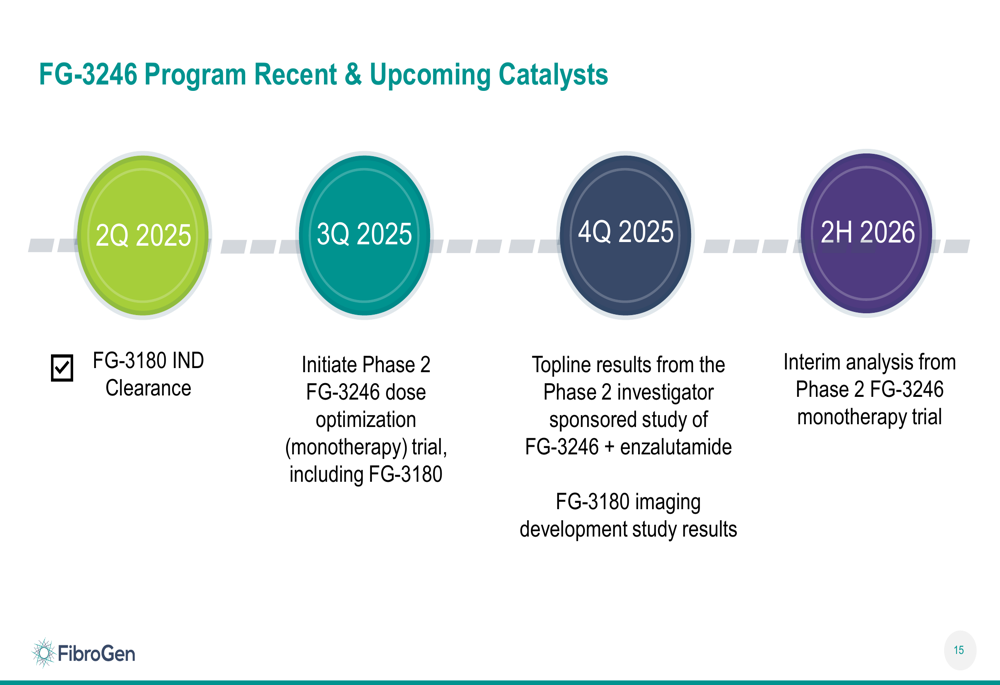

FibroGen’s presentation emphasized the potential of its oncology assets, particularly FG-3246 and FG-3180, which are being developed for metastatic castration-resistant prostate cancer (mCRPC). The company positioned these as Phase 2-ready assets with compelling clinical data.

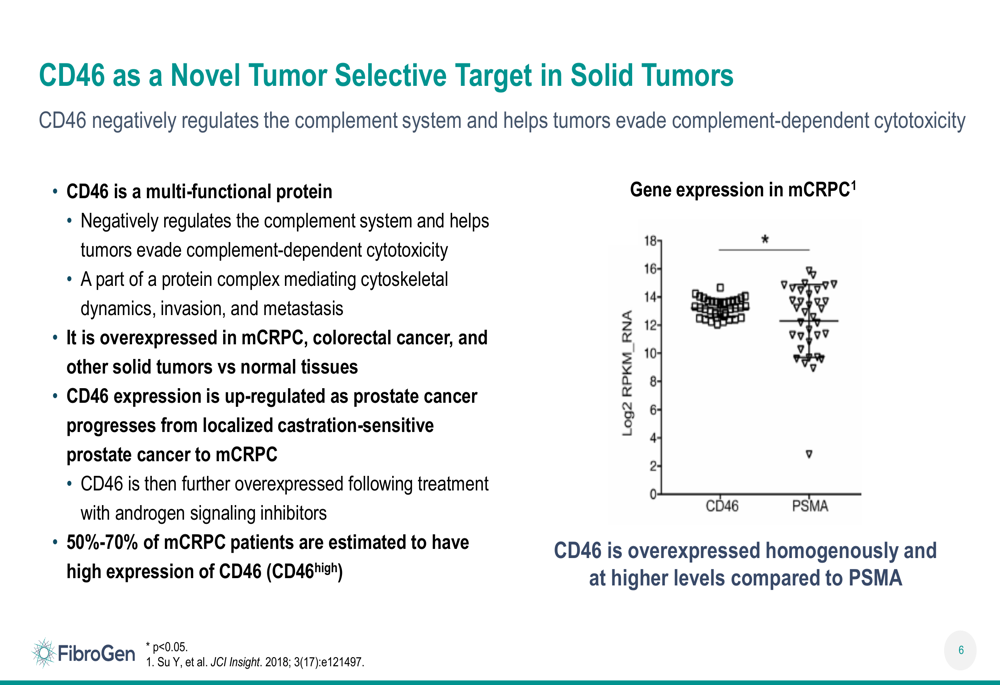

FG-3246 is an antibody-drug conjugate (ADC) targeting CD46, a protein that is overexpressed in prostate cancer and helps tumors evade the immune system. The presentation highlighted that 50-70% of mCRPC patients have high expression of CD46, making it a promising target. The company noted that prostate cancer represents a significant unmet need, with approximately 65,000 drug-treatable mCRPC cases annually in the U.S. and a 5-year survival rate of only about 30%.

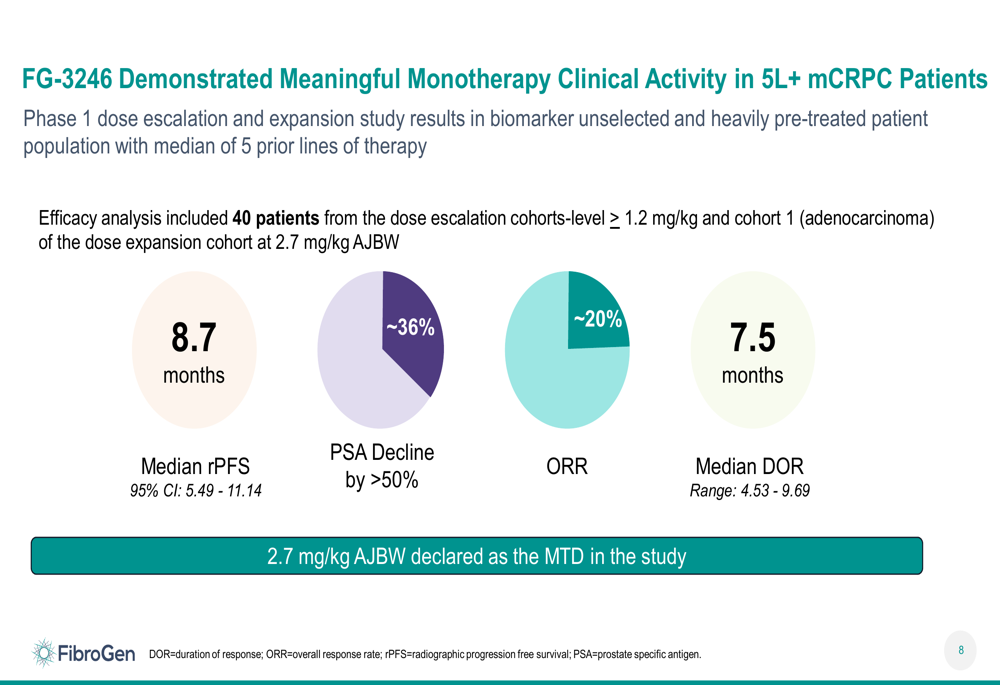

In Phase 1 trials, FG-3246 demonstrated meaningful clinical activity as a monotherapy in heavily pretreated patients (5+ prior lines of therapy), with a median radiographic progression-free survival (rPFS) of 8.7 months, PSA decline >50% in approximately 36% of patients, and an objective response rate of approximately 20%.

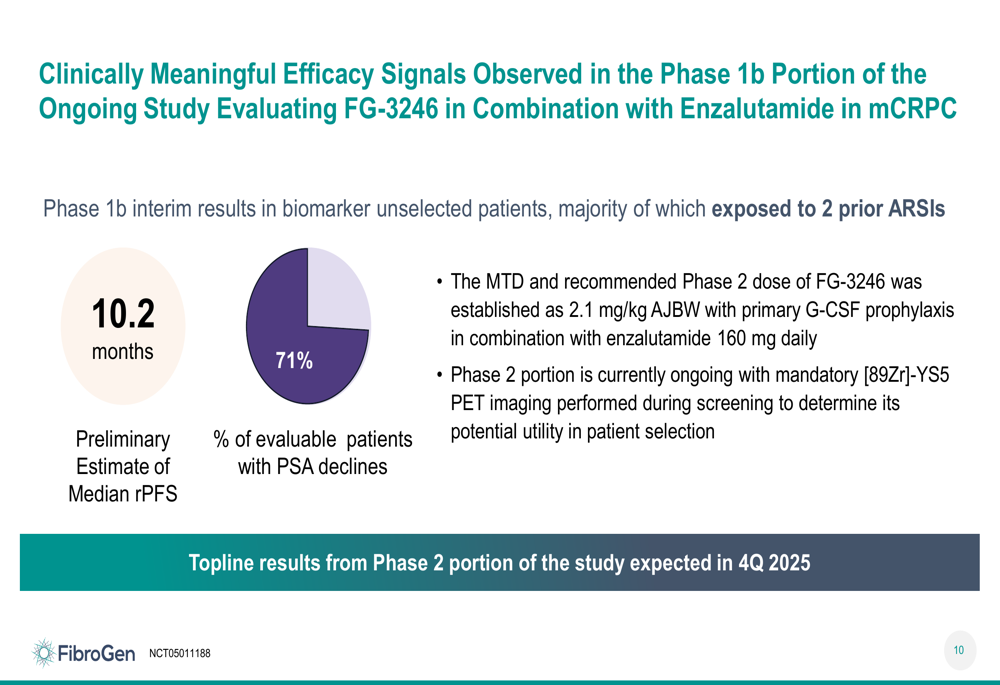

The company also presented promising data from a Phase 1b study of FG-3246 in combination with enzalutamide, showing a preliminary median rPFS of 10.2 months and PSA declines in 71% of evaluable patients.

FG-3180, a companion PET imaging agent utilizing the same targeting antibody as FG-3246, is being developed to potentially identify patients who would benefit most from treatment. This dual approach of therapeutic and diagnostic could provide FibroGen with a competitive advantage in the crowded oncology space.

Roxadustat Development

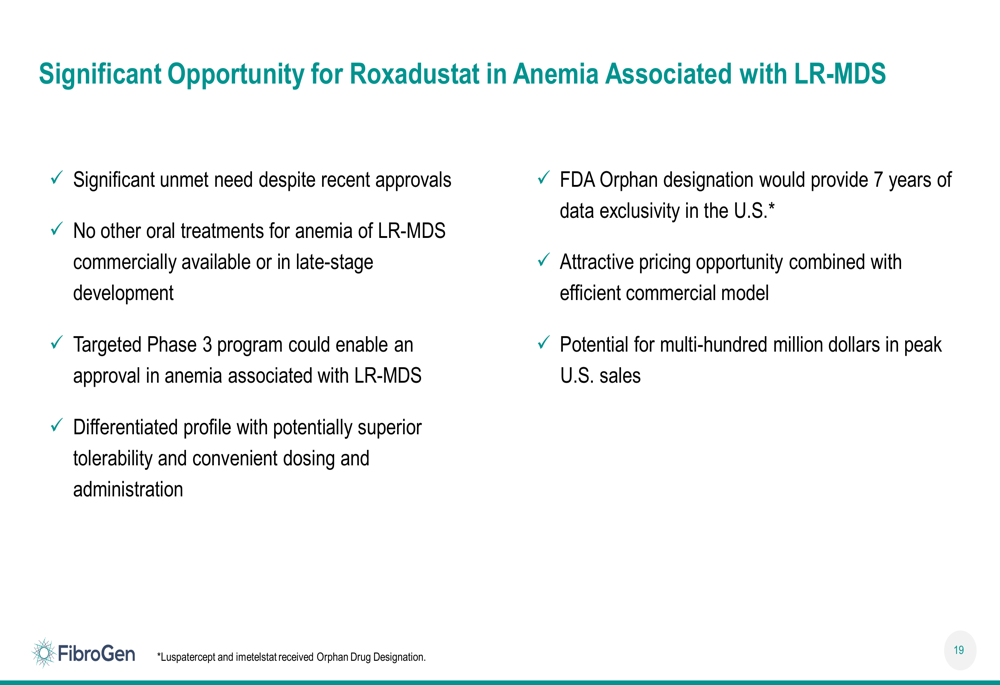

Beyond oncology, FibroGen continues to develop roxadustat for anemia associated with lower-risk myelodysplastic syndromes (LR-MDS). The company has reached an agreement with the FDA for a pivotal Phase 3 trial design, positioning roxadustat as potentially the only oral treatment for this condition.

The presentation emphasized the significant unmet need in this area, with approximately 70,000 patients living with MDS in the U.S., about 90% of whom suffer from anemia. Current first-line agents are effective in less than 50% of patients, and existing treatments require intravenous or subcutaneous administration.

Post-hoc analysis of the MATTERHORN Phase 3 trial showed that roxadustat demonstrated transfusion independence benefits compared to placebo in patients with high transfusion burden. Within 28 weeks, 36% of roxadustat-treated patients achieved 8-week red blood cell transfusion independence versus only 7% in the placebo group.

Financial Performance

While the presentation focused primarily on clinical progress and strategic initiatives, FibroGen’s actual financial results for Q2 2025 revealed significant challenges. The company reported revenue of $1.3 million, up slightly from $1 million in Q2 2024 but well below the forecast of $2.88 million.

The earnings miss was substantial, with an EPS of -$1.88 compared to the expected -$0.09, representing a negative surprise of nearly 1989%. The company reported a net loss from continuing operations of $13.7 million, or $3.38 per share.

Despite these disappointing results, FibroGen did generate $13.7 million in positive cash flow during the quarter and has provided full-year 2025 revenue guidance of $6-8 million. The significant reduction in operating costs and R&D expenses demonstrates the company’s focus on extending its cash runway while advancing key programs.

Forward-Looking Statements & Upcoming Catalysts

FibroGen outlined several near-term catalysts that could drive value for investors, including the initiation of a Phase 2 monotherapy trial of FG-3246 expected in Q3 2025 and topline results from the Phase 2 portion of the investigator-sponsored trial of FG-3246 in combination with enzalutamide expected in Q4 2025.

The Phase 2 monotherapy trial will evaluate three dose levels (1.8 mg/kg, 2.4 mg/kg, and 2.7 mg/kg) in post-ARSI, pre-chemotherapy mCRPC patients, with an interim analysis expected in the second half of 2026. The company believes this trial design, which includes primary prophylaxis with G-CSF to mitigate adverse events and focuses on healthier patients in earlier lines of therapy, could potentially improve upon the 8.7-month rPFS seen in the Phase 1 trial.

CEO Thane Wedi expressed optimism about the company’s clinical programs, stating, "We are extremely excited about our clinical development programs," while CFO David Biluchia highlighted the financial impact of the China sale, noting, "These increases in expected net cash represent a meaningful outcome for shareholders."

With multiple catalysts on the horizon and a significantly extended cash runway following the China sale, FibroGen is positioning itself to advance its clinical programs despite current financial challenges. However, investors will likely remain cautious given the significant earnings miss and the inherent risks associated with clinical development in the competitive oncology and anemia treatment landscapes.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.