Nvidia shares pop as analysts dismiss AI bubble concerns

Introduction & Market Context

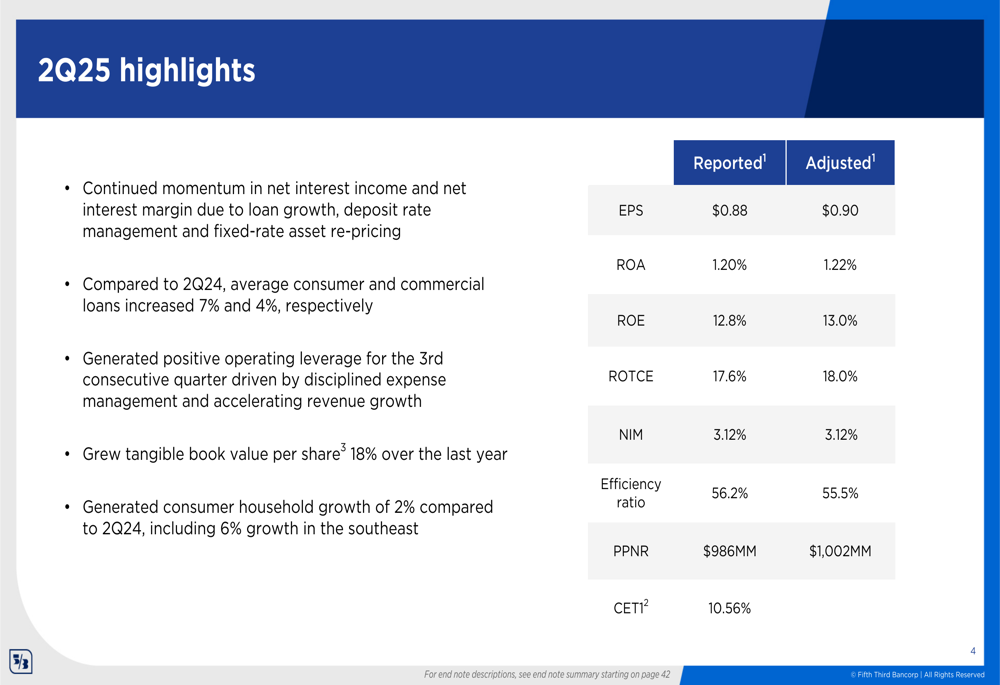

Fifth Third Bancorp (NASDAQ:FITB) delivered a strong performance in the second quarter of 2025, with accelerating net interest income growth and significant efficiency improvements. The bank's July 17, 2025 earnings presentation highlighted positive momentum across key business segments, setting the stage for continued growth in the second half of the year.

The Cincinnati-based regional bank reported adjusted earnings per share of $0.90, outperforming the reported EPS of $0.88, while achieving an adjusted return on tangible common equity (ROTCE) of 18.0%. These results come amid a moderating interest rate environment, with the Federal Reserve maintaining the federal funds rate at 4.50% throughout the quarter.

As shown in the following comprehensive overview of Q2 2025 performance metrics, Fifth Third demonstrated strength across multiple financial indicators:

Quarterly Performance Highlights

Fifth Third's net interest income reached $1.50 billion in Q2 2025, up from $1.44 billion in the previous quarter, representing a significant improvement in the bank's core earnings power. This growth was accompanied by a net interest margin expansion to 3.12%, up 9 basis points from 3.03% in Q1 2025.

The bank's presentation highlighted several key drivers behind the NII improvement, including loan growth, deposit rate management, and the favorable repricing of fixed-rate assets. The following chart illustrates this positive trajectory in both NII and NIM:

On the expense front, Fifth Third demonstrated strong discipline with adjusted noninterest expenses of $1.249 billion, down 4% from the previous quarter. This decline was primarily driven by a seasonal decrease in compensation and benefits expenses. The efficiency ratio improved to 55.5%, representing a 130 basis point enhancement compared to the same period last year.

The detailed breakdown of noninterest expenses shows the bank's focus on strategic investments while maintaining overall cost control:

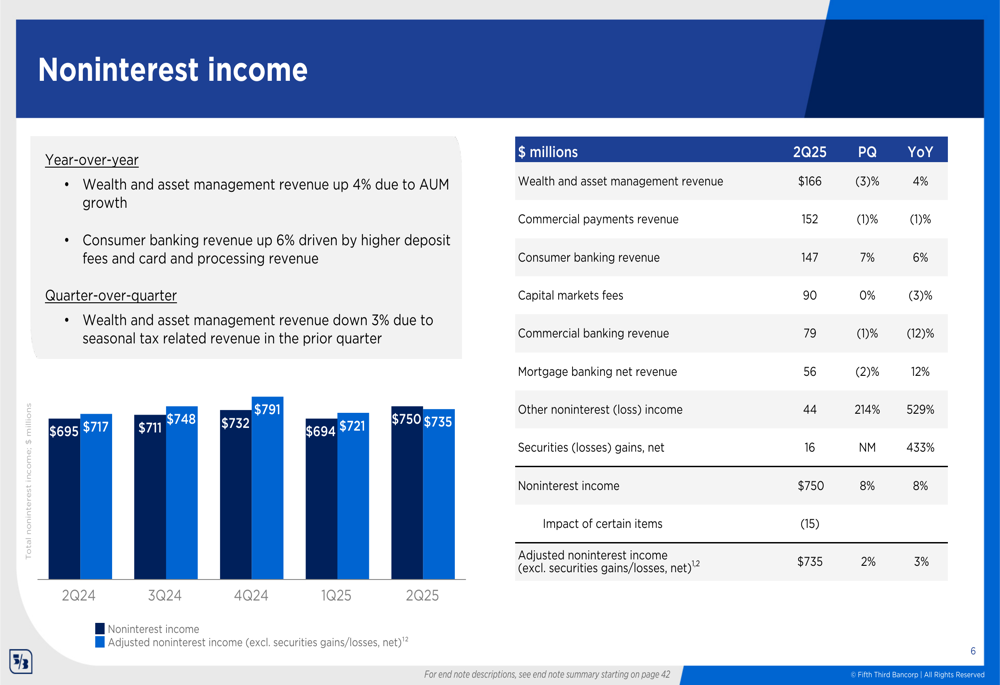

Fee income diversification remained a key strength for Fifth Third, with adjusted noninterest income of $735 million in Q2 2025, up 2% from the previous quarter and 3% year-over-year. Wealth and asset management revenue grew 4% compared to Q2 2024, while consumer banking revenue increased 6% over the same period.

Credit Quality and Capital Position

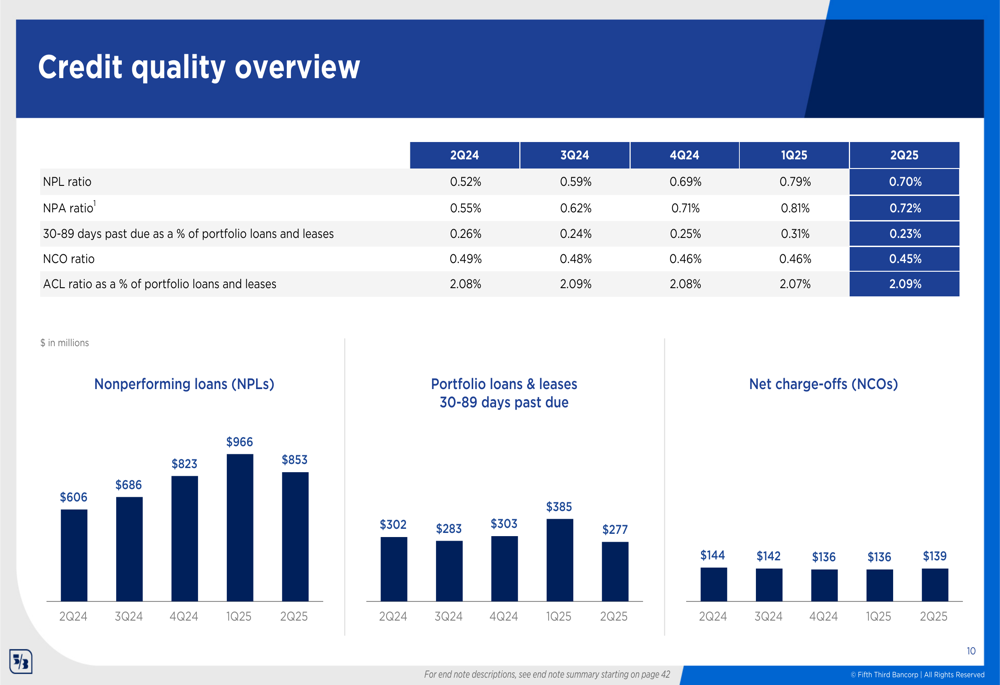

Fifth Third reported significant improvements in credit quality during Q2 2025, with non-performing assets (NPAs) declining 11% sequentially, led by an 18% reduction in commercial NPAs. The non-performing loan ratio improved to 0.70% from 0.79% in the previous quarter, while the net charge-off ratio remained stable at 0.45%.

The following credit quality overview demonstrates the bank's strengthening credit metrics:

The bank maintained a strong capital position with a Common Equity Tier 1 (CET1) ratio of 10.56%, up from 10.43% in the previous quarter. This capital strength provides Fifth Third with flexibility for strategic investments and shareholder returns.

Strategic Initiatives

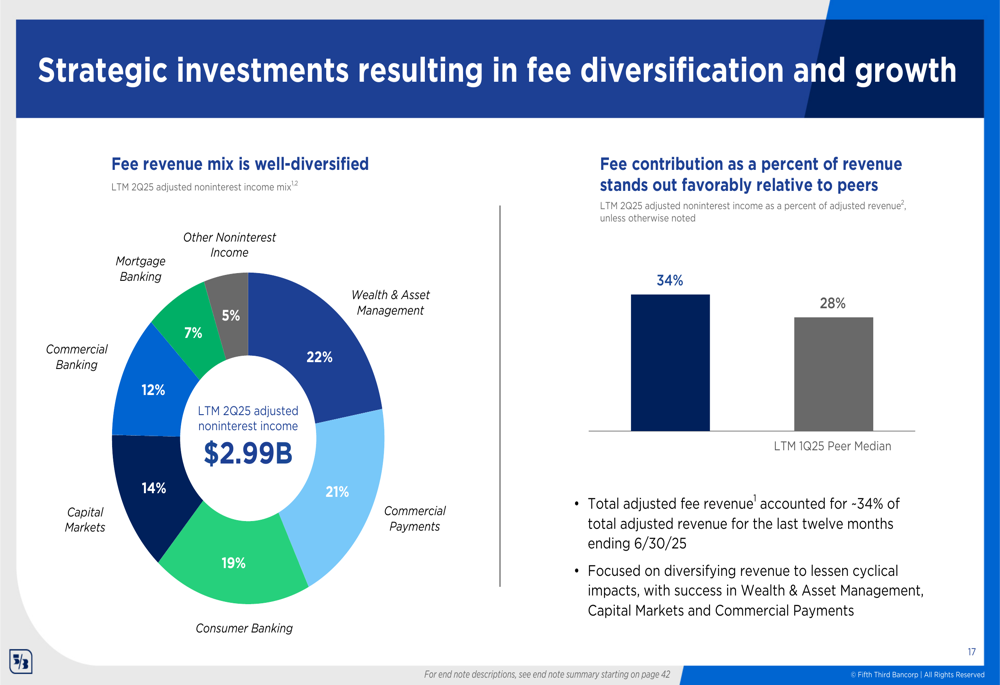

Fifth Third's strategic investments have resulted in significant fee income diversification, positioning the bank favorably compared to peers. The presentation highlighted that fee income contributed 34% of total revenue on a last twelve months basis, compared to a peer median of 28%.

The following chart illustrates the bank's well-diversified fee revenue streams:

Digital engagement continued to show positive momentum, with average active digital users increasing to 3.17 million in Q2 2025, up from 3.14 million in the previous quarter and 3.07 million a year earlier. Mobile users similarly grew to 2.44 million, reflecting the bank's successful digital transformation efforts.

Forward-Looking Statements

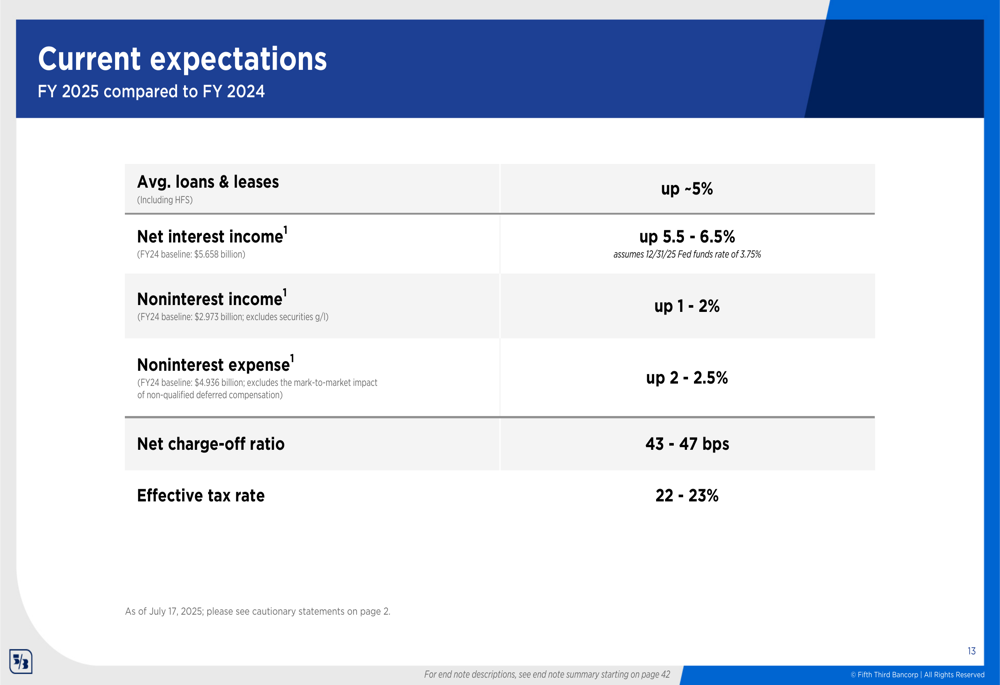

Looking ahead, Fifth Third provided an optimistic outlook for the remainder of 2025. For the full year, the bank expects average loans and leases to increase approximately 5% compared to 2024, with net interest income projected to grow 5.5-6.5%. This guidance assumes a Federal funds rate of 3.75% by year-end, reflecting expectations for continued monetary policy easing.

The bank's detailed expectations for fiscal year 2025 include:

For the third quarter of 2025, Fifth Third projects continued momentum with net interest income expected to increase approximately 1% compared to Q2, assuming a Federal funds rate of 4.25% by September 30, 2025. Noninterest income is forecast to grow 1-4%, while expenses are expected to increase by about 1%.

Notably, Fifth Third subsequently exceeded these Q3 projections according to recent earnings reports, posting an EPS of $0.91 against forecasts of $0.86, with revenue reaching $2.31 billion. The bank also announced a merger with Comerica, expanding its market presence beyond what was indicated in the Q2 presentation.

Competitive Industry Position

Fifth Third's loan portfolio remained well-diversified, with commercial loans accounting for 61% and consumer loans making up 39% of the total. Average loan balances increased to $123.1 billion in Q2 2025, with commercial loans growing 4% year-over-year and consumer loans up 7%.

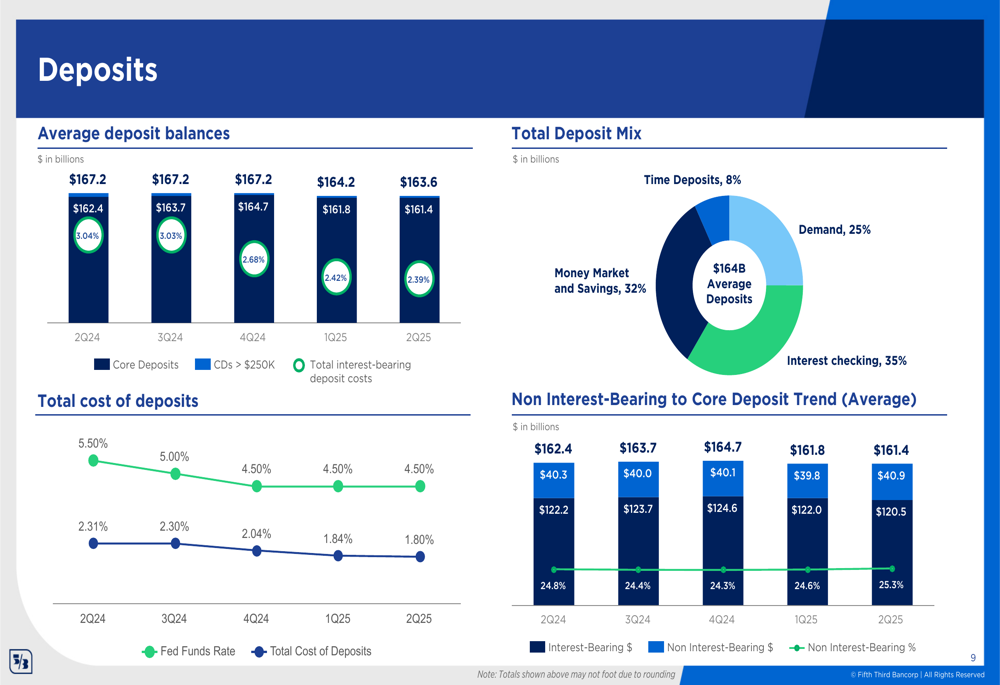

The bank's deposit base remained stable at $161.4 billion, with a favorable mix of 25% demand deposits and 35% interest checking accounts. The cost of deposits declined to 1.80% from 1.84% in the previous quarter, despite the stable rate environment.

Fifth Third's consumer household growth of 2% year-over-year, including 6% growth in the Southeast region, demonstrates the bank's successful geographic expansion strategy. This growth, combined with the bank's digital transformation efforts and fee income diversification, positions Fifth Third competitively within the regional banking landscape.

As Fifth Third moves forward with its recently announced Comerica merger, the bank appears well-positioned to capitalize on its strong Q2 2025 performance and execute on its strategic growth initiatives for the remainder of the year and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.