These are top 10 stocks traded on the Robinhood UK platform in July

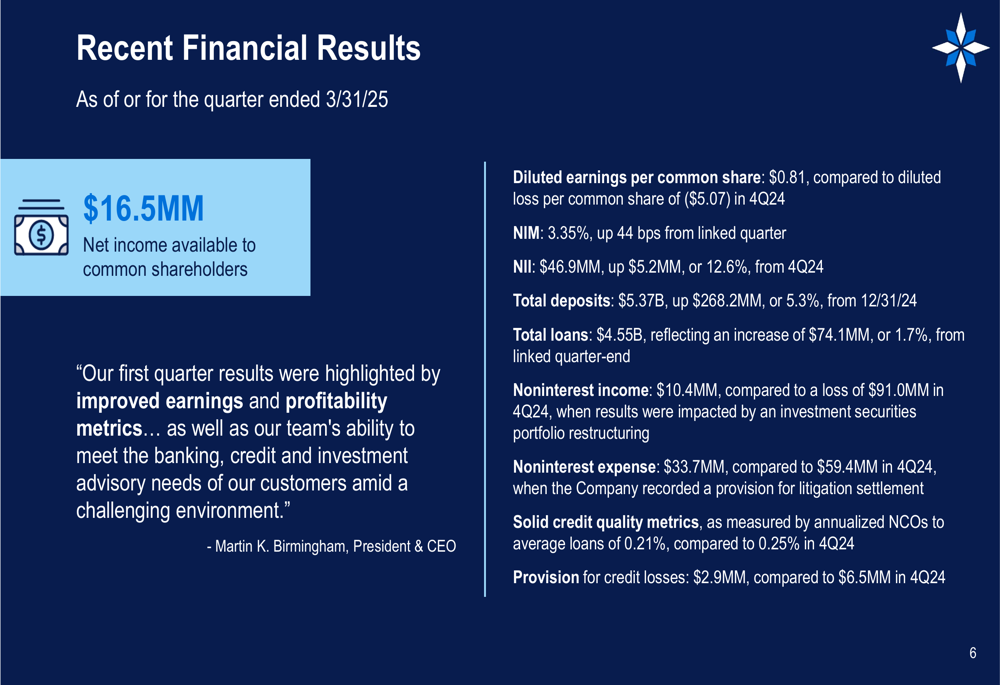

Financial Institutions , Inc. (NASDAQ:FISI) presented its first quarter 2025 results on April 28, showing a significant recovery from the previous quarter’s losses. The company reported net income available to common shareholders of $16.5 million with diluted earnings per share of $0.81, marking a substantial turnaround from the $66.1 million loss in Q4 2024.

Executive Summary

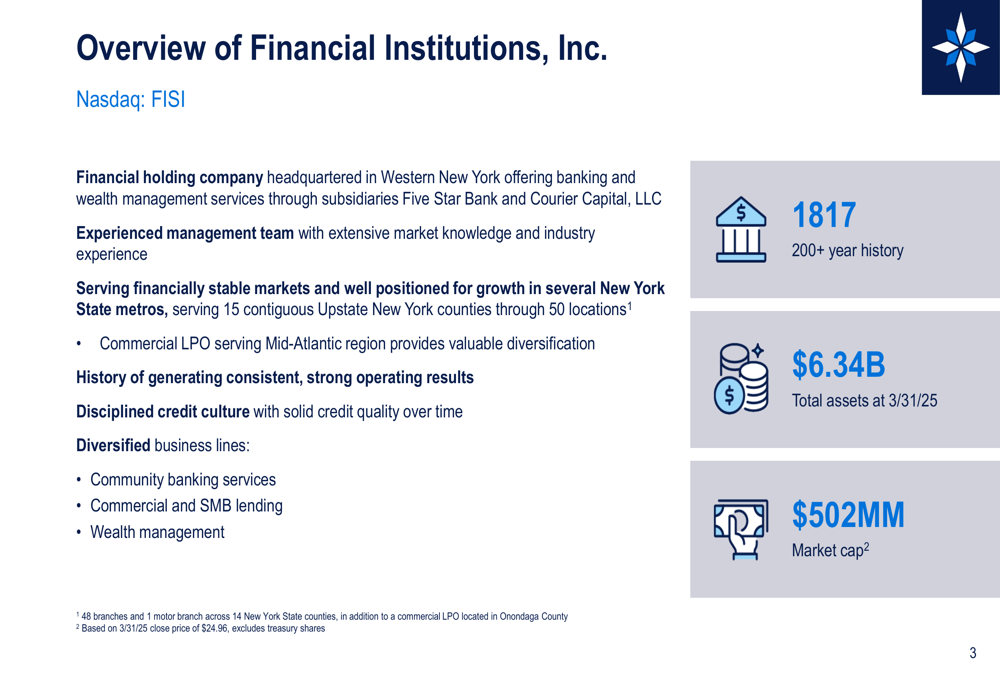

FISI, a financial holding company headquartered in Western New York with $6.34 billion in total assets, demonstrated strong performance across key metrics in Q1 2025. The company’s net interest margin (NIM) expanded to 3.35%, up 44 basis points from the linked quarter, while total deposits increased by $268.2 million (5.3%) to $5.37 billion.

As shown in the following overview of the company’s structure and market position:

"We are pleased with our first quarter performance, which demonstrates the resilience of our business model and the effectiveness of our strategic initiatives," said the company’s CEO in the presentation. This positive sentiment represents a stark contrast to the challenging fourth quarter of 2024, when the company reported a significant loss.

Quarterly Performance Highlights

The bank’s Q1 2025 results showed notable improvement across multiple financial metrics. Net interest income reached $46.9 million, up $5.2 million (12.6%) from Q4 2024 and $6.8 million (16.9%) from the year-ago quarter. Total (EPA:TTEF) loans grew to $4.55 billion, reflecting an increase of $74.1 million (1.7%) from the previous quarter.

The following slide details the company’s recent financial results:

Credit quality remained solid, with annualized net charge-offs to average loans of 0.21%, while the provision for credit losses was $2.9 million. Noninterest income totaled $10.4 million, and noninterest expense was $33.7 million for the quarter.

This performance represents a significant improvement from Q4 2024, when the company reported a net loss of $66.1 million and a diluted loss per share of $4.02, as noted in recent earnings reports.

Detailed Financial Analysis

Net Interest Margin and Income

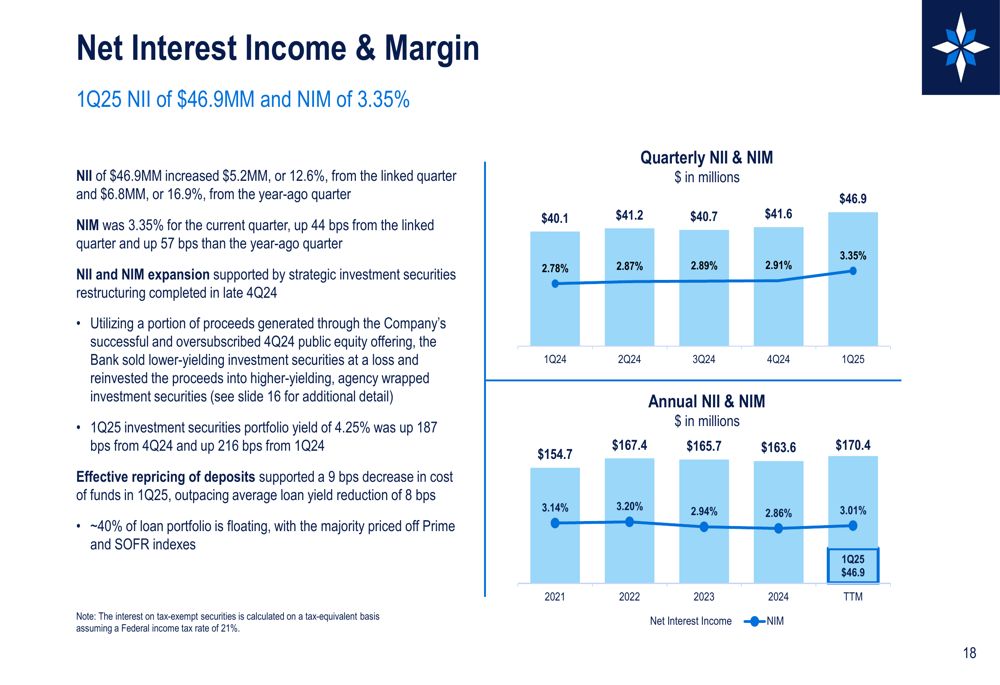

FISI’s net interest margin expansion to 3.35% was a key driver of improved performance in Q1 2025. This 44 basis point increase from the linked quarter and 57 basis point improvement from the year-ago quarter contributed significantly to the bank’s profitability.

The following chart illustrates the trend in net interest income and margin:

The company’s balance sheet is structured to provide ample cash flow, with approximately $1.2 billion in anticipated cash flow from investment securities and loan portfolios over the next twelve months. This positions FISI well for continued margin improvement as interest rates evolve.

Deposit Base and Liquidity

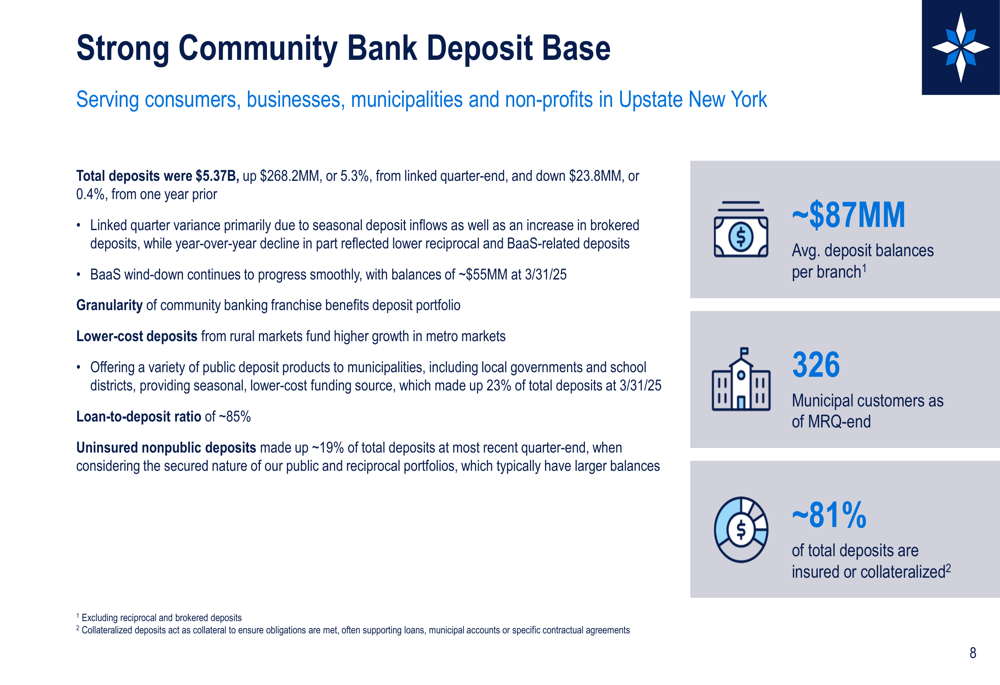

FISI maintained a strong community bank deposit base, with total deposits of $5.37 billion as of March 31, 2025. The 5.3% increase from the previous quarter was primarily attributed to seasonal deposit inflows and the wind-down of Banking-as-a-Service (BaaS) operations.

The company’s deposit structure and trends are illustrated in the following slide:

Importantly, approximately 81% of total deposits are insured or collateralized, with uninsured nonpublic deposits making up only about 19% of total deposits. The bank maintains a loan-to-deposit ratio of approximately 85%, reflecting a balanced approach to funding its lending activities.

FISI’s liquidity position remains robust, with $1.29 billion in available committed liquidity as of March 31, 2025, providing a strong buffer against potential market volatility.

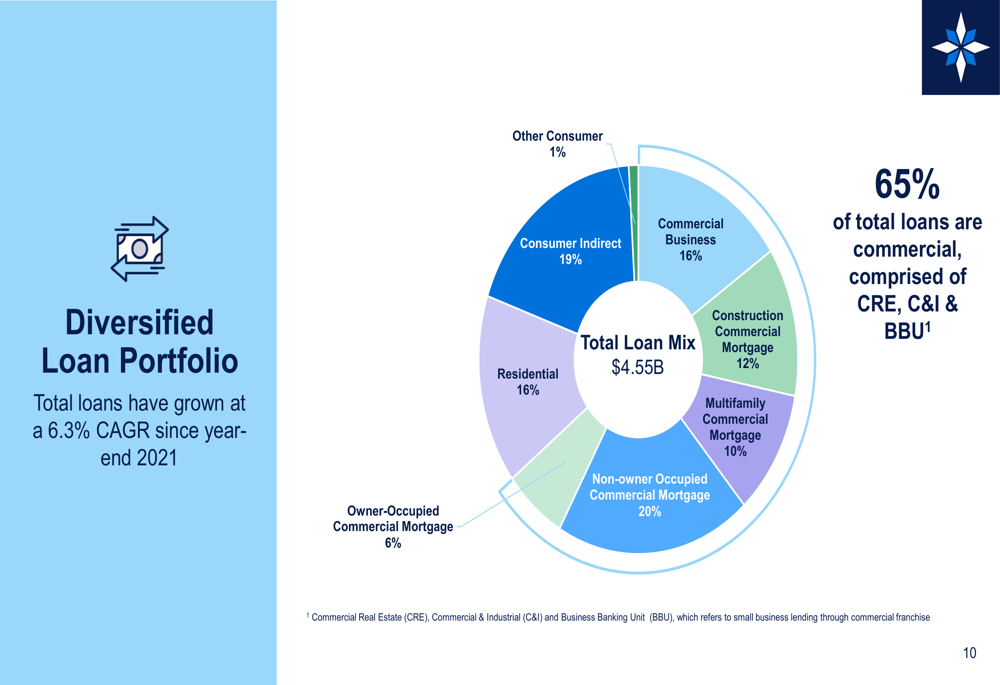

Diversified Loan Portfolio

The bank’s $4.55 billion loan portfolio is well-diversified across various sectors, with commercial loans comprising 65% of the total. The portfolio has grown at a 6.3% compound annual growth rate (CAGR) since year-end 2021.

The composition of the loan portfolio is illustrated in the following chart:

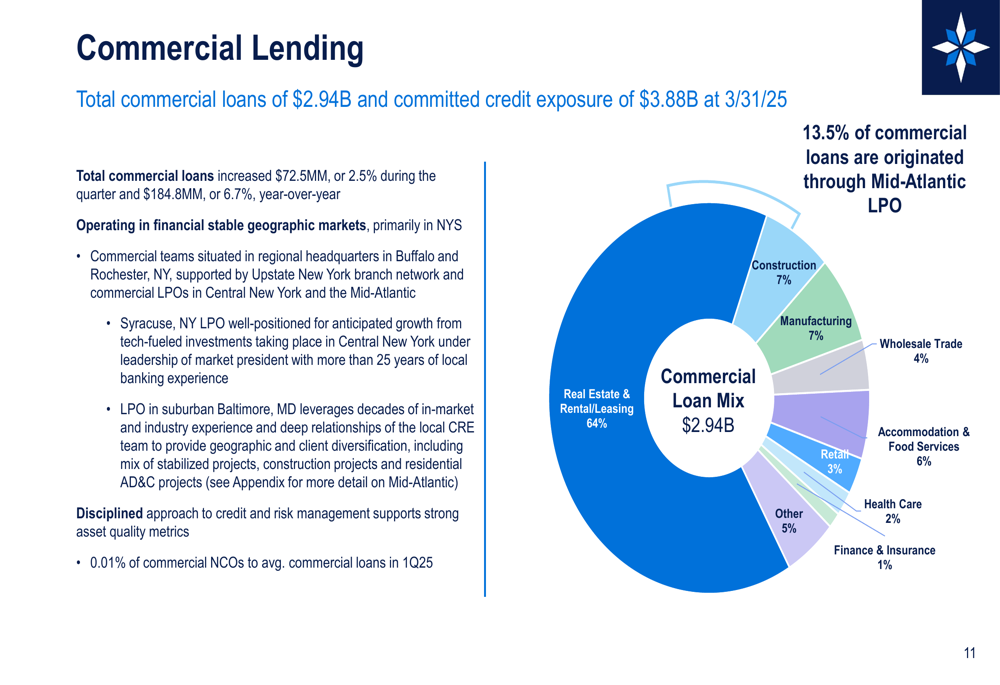

Commercial lending, totaling $2.94 billion with committed credit exposure of $3.88 billion, increased by $72.5 million (2.5%) during the quarter and $184.8 million (6.7%) year-over-year. The commercial loan portfolio is diversified across multiple industries, with real estate and rental/leasing representing the largest segment at 64%.

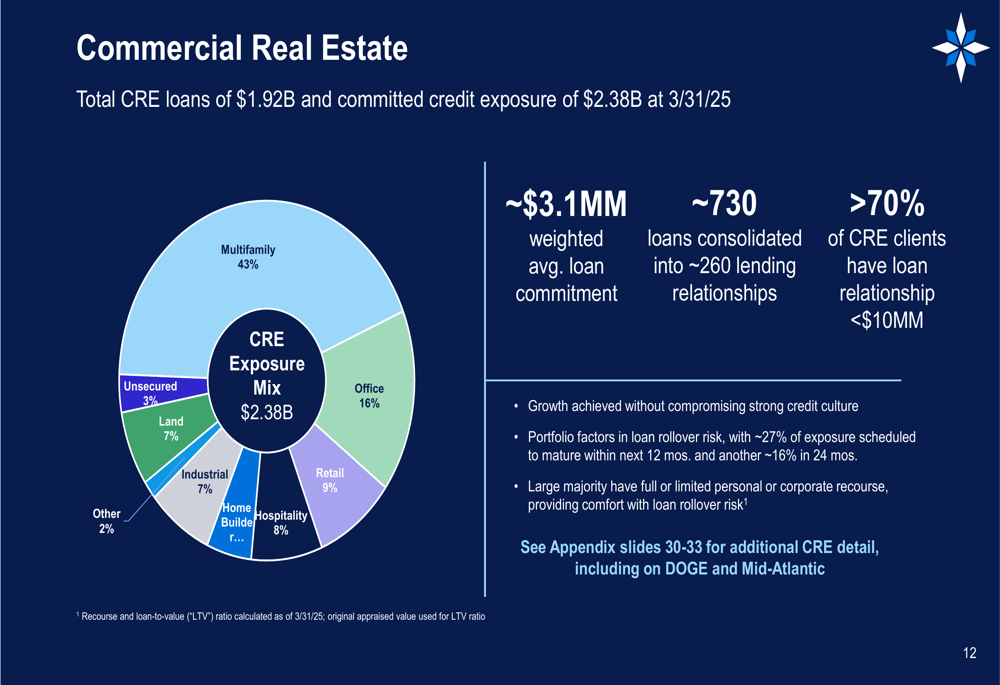

Commercial real estate (CRE) loans totaled $1.92 billion with committed credit exposure of $2.38 billion. The CRE portfolio is characterized by a weighted average loan commitment of approximately $3.1 million spread across about 730 loans consolidated into roughly 260 lending relationships. More than 70% of CRE clients have loan relationships under $10 million, reflecting the bank’s focus on smaller, manageable exposures.

Strategic Initiatives and Outlook

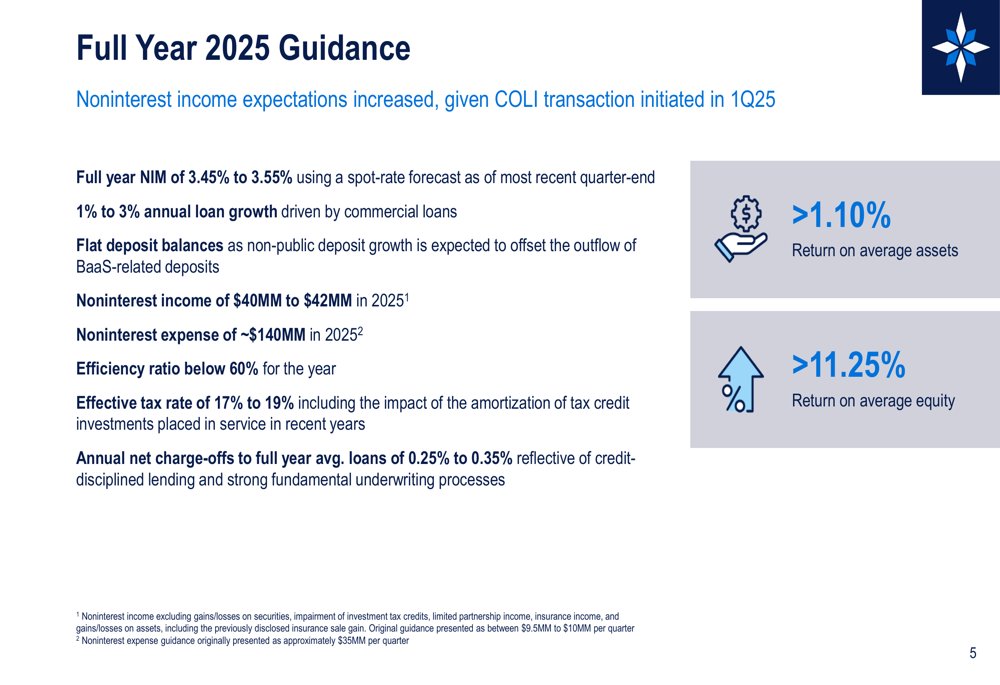

FISI provided full-year 2025 guidance that reflects its focus on profitable growth and operational efficiency. The company expects a net interest margin of 3.45% to 3.55%, annual loan growth of 1% to 3% driven by commercial loans, and flat deposit balances.

The following slide outlines the company’s full-year 2025 guidance:

Noninterest income is projected to be $40 million to $42 million in 2025, with noninterest expense of approximately $140 million. The bank is targeting an efficiency ratio below 60% for the year, along with an effective tax rate of 17% to 19% and annual net charge-offs to full-year average loans of 0.25% to 0.35%.

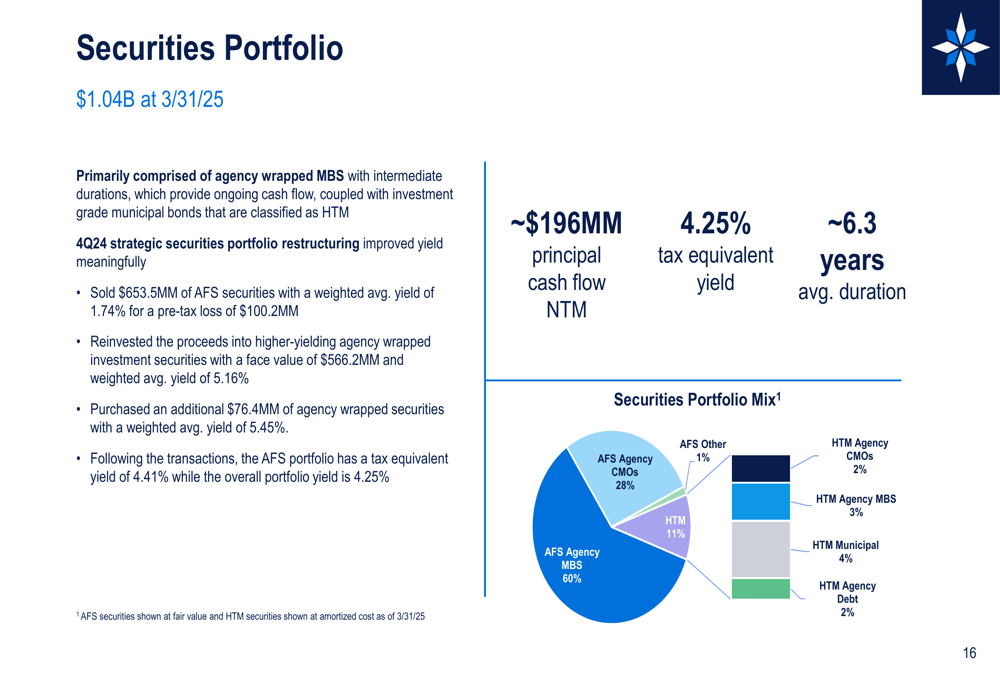

The company’s investment securities portfolio, valued at $1.04 billion, is primarily comprised of agency-wrapped mortgage-backed securities (MBS). This portfolio, with a tax-equivalent yield of 4.25% and average duration of approximately 6.3 years, provides a stable source of income while maintaining liquidity.

Forward-Looking Statements

FISI’s management has set performance targets that include a return on average assets exceeding 1.10% and a return on average equity above 11.25% for 2025. These goals align with the company’s focus on profitable growth rather than growth for its own sake.

"We are not focused simply on growth. We are focused on profitable growth," emphasized the company’s CFO in recent statements, underscoring FISI’s strategic direction.

The bank’s conservative loan growth estimate of 1-3% reflects a cautious approach in the current economic environment, though management has indicated potential for mid-single-digit growth under favorable conditions. This measured strategy, combined with the bank’s strong capital position and improved financial performance, positions Financial Institutions, Inc. to continue its recovery and pursue sustainable growth throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.