S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Finning International Inc . (TSX:FTT), the world’s largest Caterpillar (NYSE:CAT) dealer, reported strong first-quarter results on May 13, 2025, with revenue growth across key business segments and regions. The company’s stock closed at $42.46 on May 12, up 3.61% ahead of the earnings release, reflecting positive market sentiment.

The equipment dealer demonstrated resilience amid varying regional market conditions, with particularly strong performance in its South American operations and robust growth in product support revenue across all territories. The company also announced a strategic divestiture of its 4Refuel business, signaling a focus on core operations.

Quarterly Performance Highlights

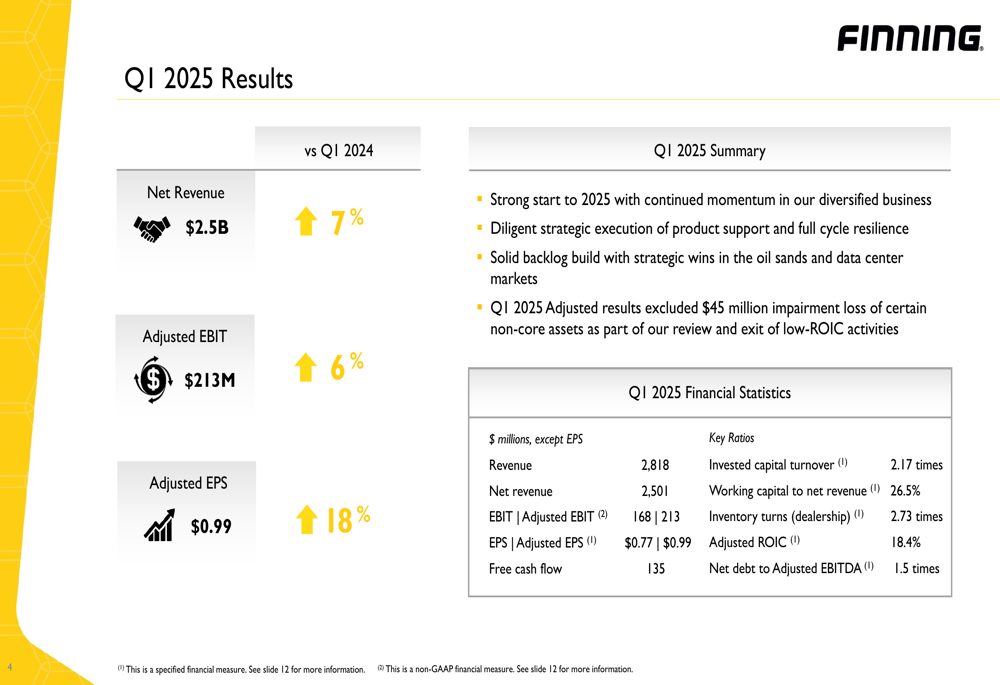

Finning reported Q1 2025 net revenue of $2.5 billion, representing a 7% increase compared to the same period last year. Adjusted EBIT reached $213 million, up 6% year-over-year, while adjusted earnings per share climbed 18% to $0.99. The company generated $135 million in free cash flow during the quarter.

As shown in the following comprehensive results summary:

Product support revenue, a key driver of Finning’s business model, increased 11% compared to Q1 2024, with growth across all regions. This performance underscores the company’s strategic focus on building resilient revenue streams less susceptible to economic cycles.

The equipment backlog grew to $2.8 billion, representing a 45% increase compared to March 31, 2024, and a 9% increase from December 31, 2024. This growth was primarily driven by strong order intake in mining and power systems segments.

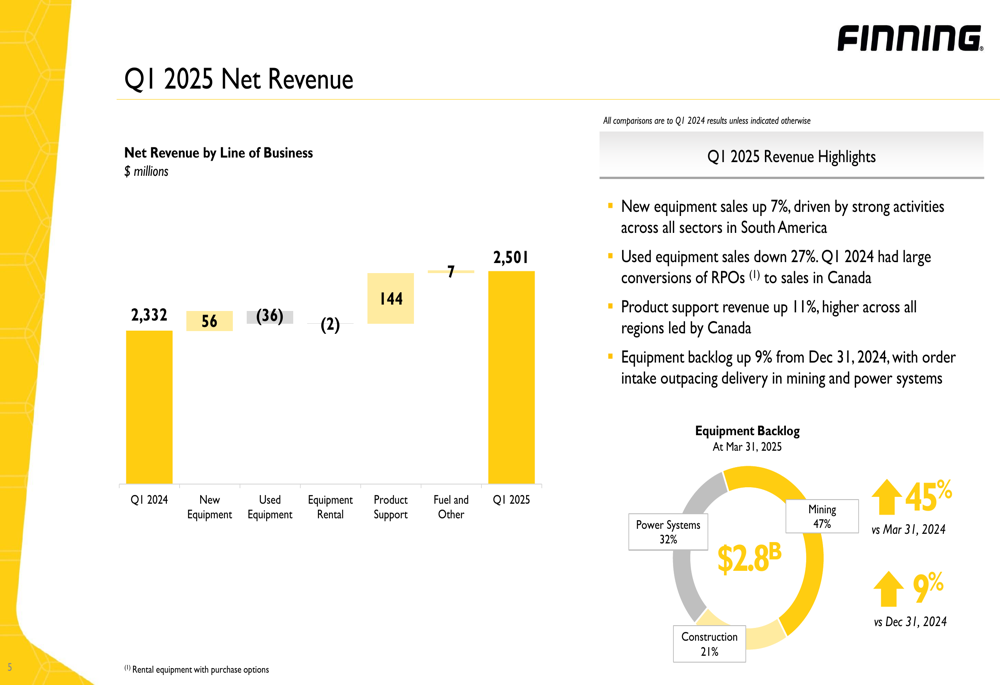

The following breakdown illustrates Finning’s revenue by line of business:

New equipment sales increased by 7%, primarily driven by strong activities across all sectors in South America. However, used equipment sales declined by 27%, as Q1 2024 had included large conversions of rental purchase options to sales in Canada. The equipment backlog composition as of March 31, 2025, was 47% mining, 32% power systems, and 21% construction.

Regional Performance Analysis

Finning’s performance varied significantly across its three main operating regions, with South America leading growth while Canada and UK & Ireland showed more mixed results.

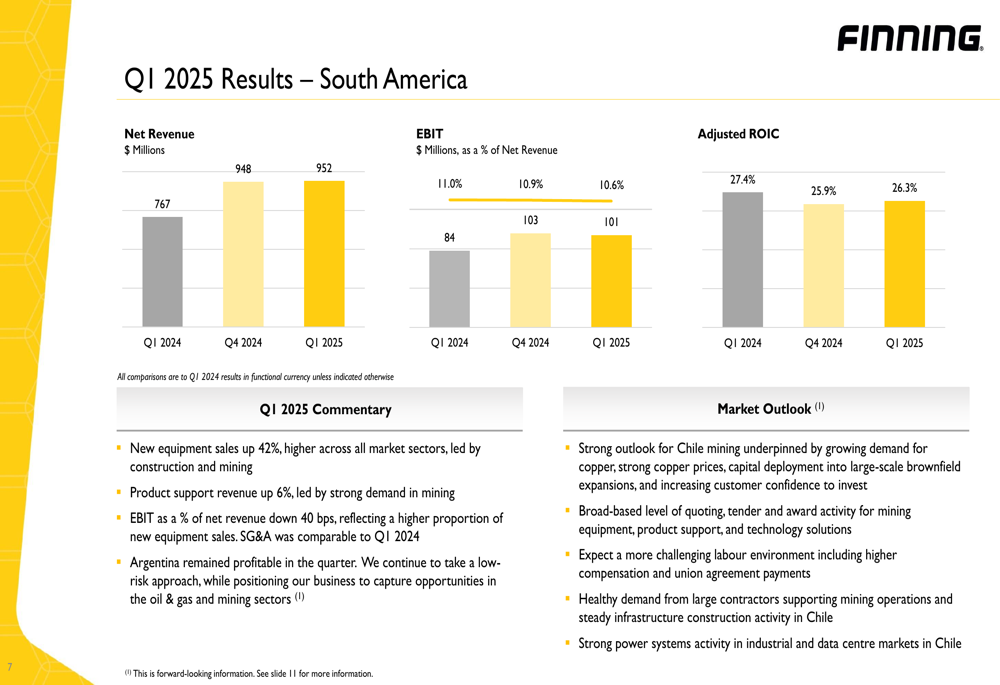

South American operations delivered exceptional performance with net revenue of $952 million, up significantly from $767 million in Q1 2024. New equipment sales surged 42% across all market sectors, led by construction and mining. Product support revenue increased by 6%, driven by strong demand in mining.

As illustrated in the South American results:

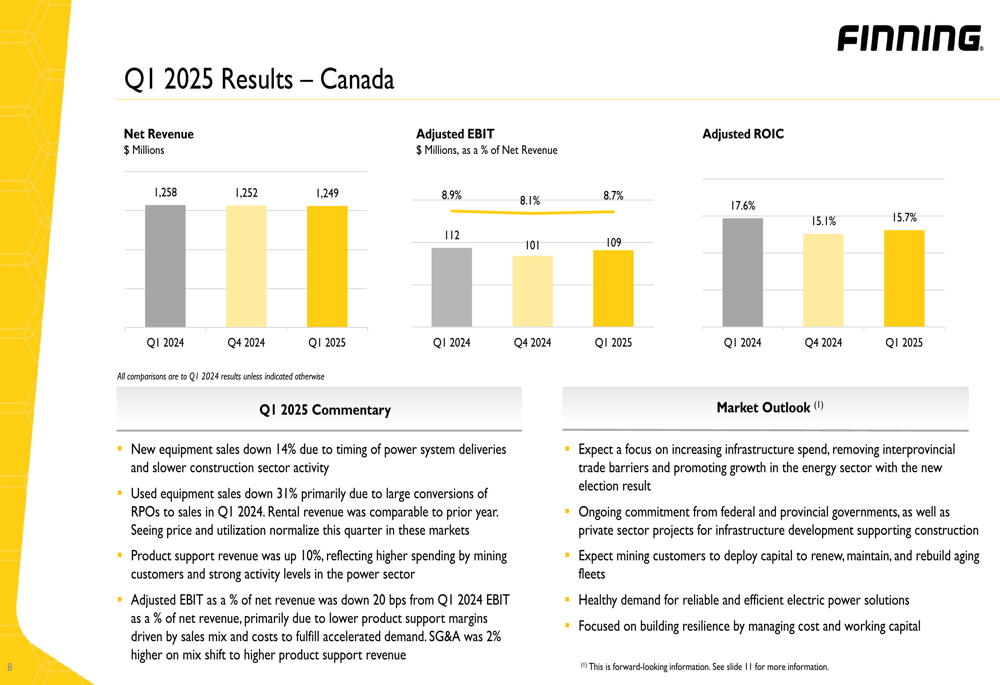

In Canada, net revenue remained relatively stable at $1,249 million compared to $1,258 million in Q1 2024. While new equipment sales declined by 14% due to timing of power system deliveries and slower construction sector activity, product support revenue increased by 10%, reflecting higher spending by mining customers and strong activity in the power sector.

The Canadian market outlook remains positive, with expectations of increased infrastructure spending and mining customers deploying capital to renew and maintain aging fleets:

The UK & Ireland region reported net revenue of $300 million, slightly down from $307 million in Q1 2024. New equipment sales decreased by 10% due to timing of power project deliveries, though this was partially offset by strong sales to construction customers. Product support revenue grew by 4%, driven by activity in the power system sector.

Strategic Initiatives

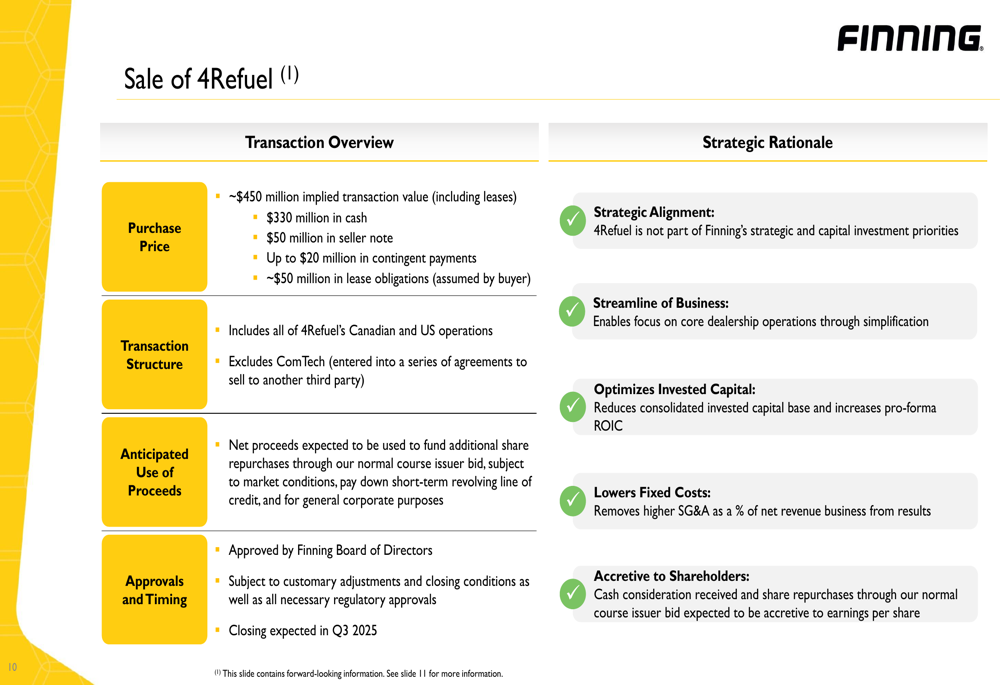

Finning announced the sale of its 4Refuel business for approximately $450 million, including a $330 million cash component and a $50 million seller note. The transaction, expected to close in Q3 2025, represents a strategic realignment to optimize invested capital and focus on core operations.

The following slide details the transaction structure and strategic rationale:

The company plans to use the net proceeds to fund additional share repurchases through its normal course issuer bid and for general corporate purposes. This divestiture aligns with Finning’s strategy to streamline operations, lower fixed costs, and create shareholder value.

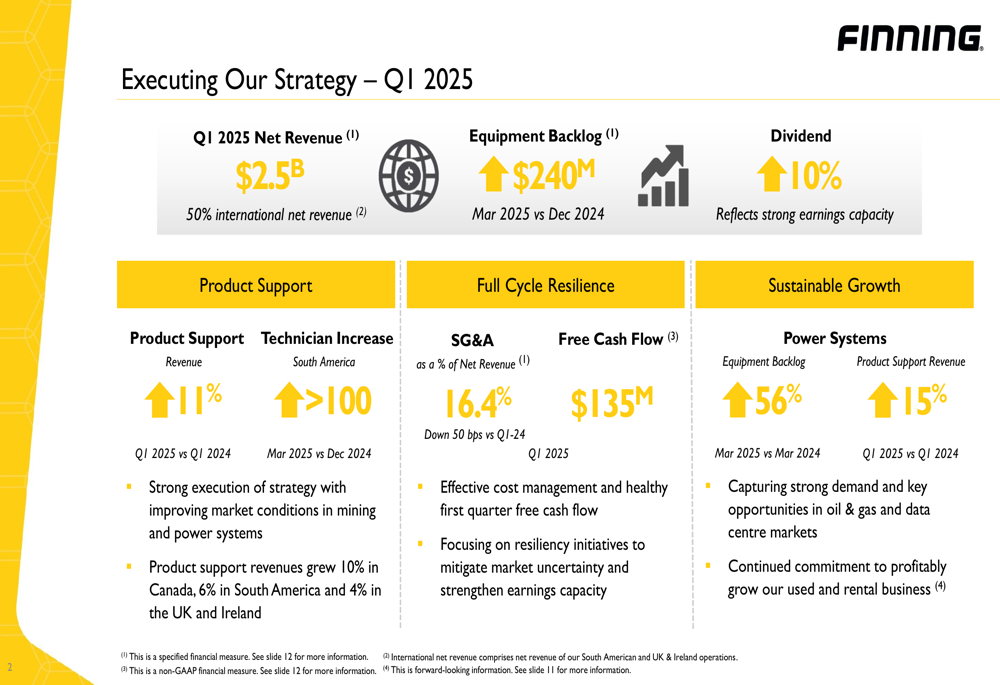

In addition to the 4Refuel sale, Finning continues to execute on its strategic priorities, including strengthening product support capabilities, enhancing operational efficiency, and pursuing sustainable growth opportunities. The company increased its dividend by 10%, reflecting confidence in its earnings capacity and marking 24 consecutive years of dividend growth.

As shown in the strategic execution overview:

The company has made significant progress in building full-cycle resilience, with SG&A as a percentage of net revenue decreasing by 50 basis points to 16.4% compared to Q1 2024. This improvement reflects strong cost control measures and operational efficiency initiatives.

Forward-Looking Statements

Finning’s outlook remains positive across its key markets, with particularly strong prospects in mining, power systems, and data center markets. In Chile, the company expects increasing customer confidence to invest in mining operations, supported by healthy demand from large contractors.

In Canada, the recent election results are expected to drive increased infrastructure spending and promote growth in the energy sector. Mining customers are anticipated to deploy capital to renew and maintain aging fleets.

The UK & Ireland market outlook suggests continued softness in the construction sector, in line with low projected GDP growth. However, the company expects growing contributions from used equipment and power systems as it executes on its strategy.

Finning’s strategic focus on product support, operational efficiency, and targeted growth opportunities positions the company well to navigate varying market conditions while delivering consistent financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.