JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

First Business Financial Services (NASDAQ:FBIZ) presented its first quarter 2025 earnings results on April 25, 2025, highlighting strong loan and deposit growth alongside improved asset quality metrics. The bank’s stock closed at $49.93 on April 24, up 2.61% ahead of the presentation, though premarket trading on the 25th showed a 1.66% decline to $49.10. The company continues to operate within its 52-week range of $33.00 to $56.46.

The presentation revealed First Business Bank’s continued focus on relationship banking and disciplined interest rate risk management, which has helped the institution maintain balanced growth in a challenging economic environment.

Quarterly Performance Highlights

First Business Bank reported robust performance across key metrics in Q1 2025, with notable growth in loans, deposits, and revenue compared to both the linked quarter and the prior year period.

As shown in the following comprehensive overview of the bank’s Q1 2025 performance:

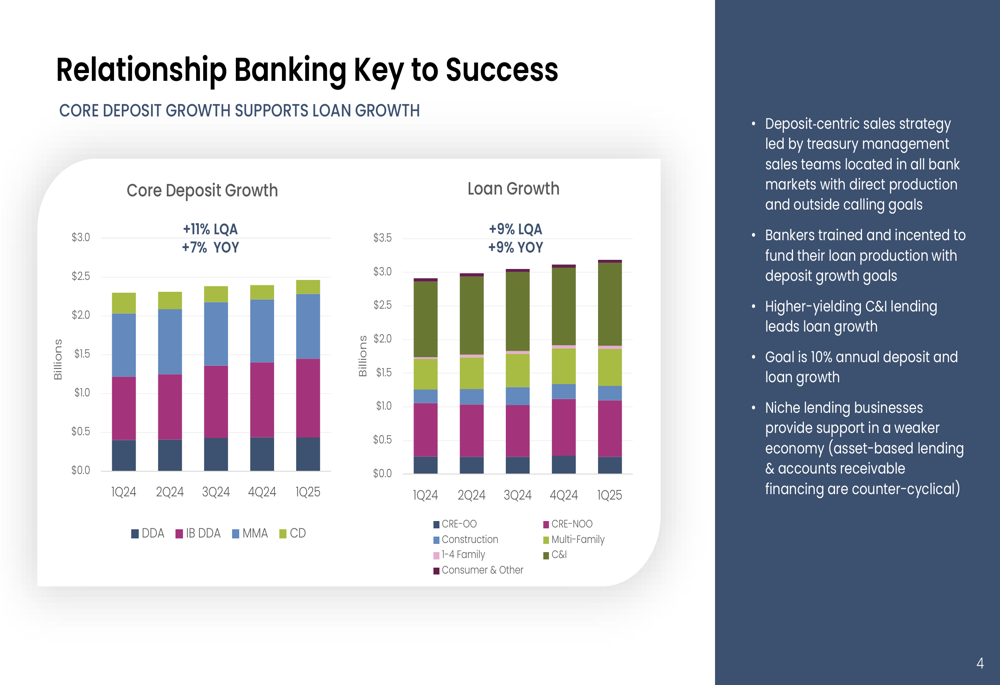

Loan growth reached 9% year-over-year, with a 9.2% annualized increase from the linked quarter. Core deposits grew even faster at 11% annualized from the linked quarter and 7.2% year-over-year. The bank’s Private Wealth division reported assets under management and administration (AUM&A) of $3.4 billion, generating fee income of $3.5 million, a 12.2% increase over Q1 2024.

Asset quality showed marked improvement, with non-performing assets (NPAs) decreasing by 15% and the NPA to total assets ratio falling to 0.76% from 0.91% in Q4 2024. The allowance coverage ratio improved to 151.8%.

Detailed Financial Analysis

First Business Bank’s relationship banking strategy has been instrumental in driving balanced growth in both loans and deposits, as illustrated in the following chart:

The bank’s deposit-centric sales strategy, led by treasury management teams, has helped fund loan production with deposit growth. Higher-yielding commercial and industrial (C&I) lending is leading loan growth, with the bank targeting 10% annual growth in both deposits and loans.

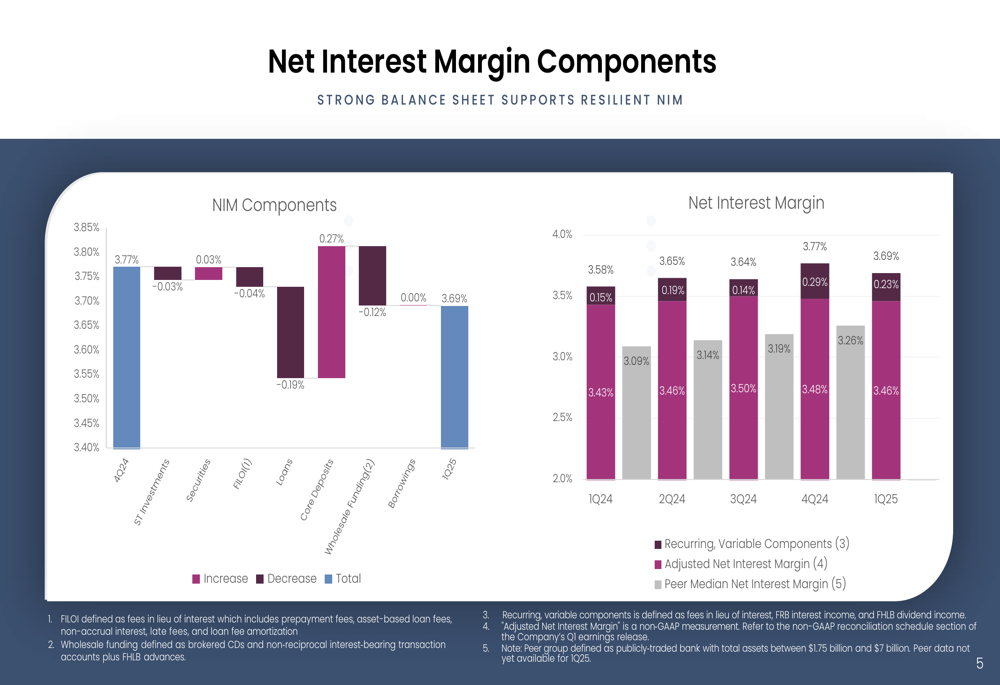

Net interest margin (NIM) remained strong at 3.69%, compared to 3.77% in the linked quarter and 3.58% in the prior year quarter. The following breakdown illustrates the components affecting the bank’s NIM:

The bank’s adjusted net interest margin of 3.46% in Q1 2025 continues to outperform the peer median, reflecting effective management of interest rate risk and a disciplined approach to balance sheet management.

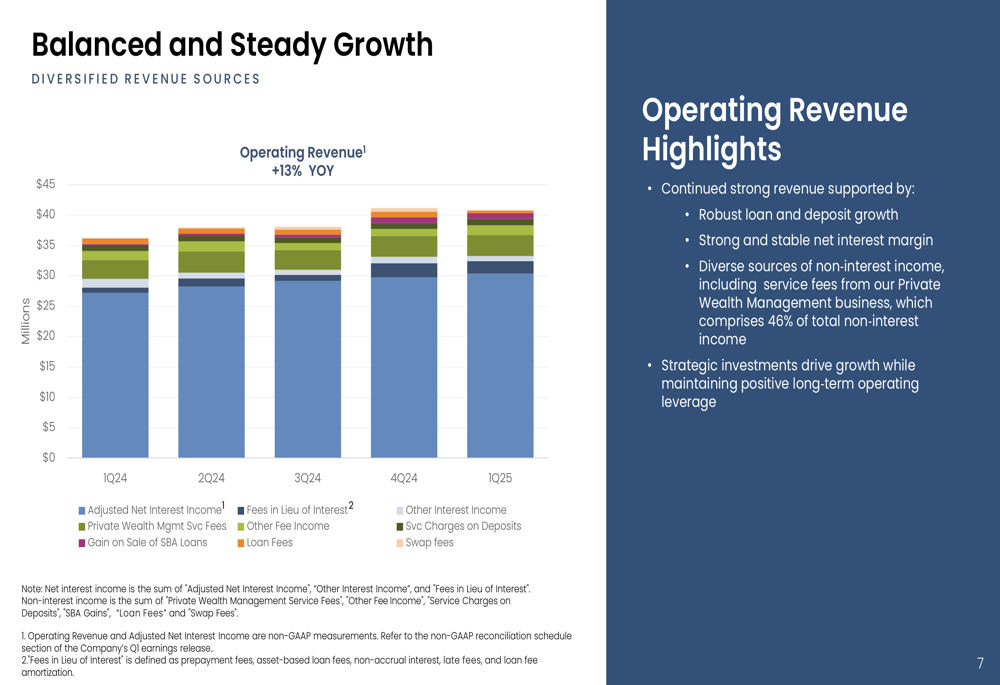

Revenue diversification remains a key strength for First Business Bank, with a 13% year-over-year increase in operating revenue driven by loan growth, NIM, and fee income:

Private Wealth Management service fees comprise 46% of total non-interest income, providing a stable revenue stream alongside the bank’s traditional lending operations. This diversification helps buffer against interest rate volatility and economic fluctuations.

Asset Quality and Capital Position

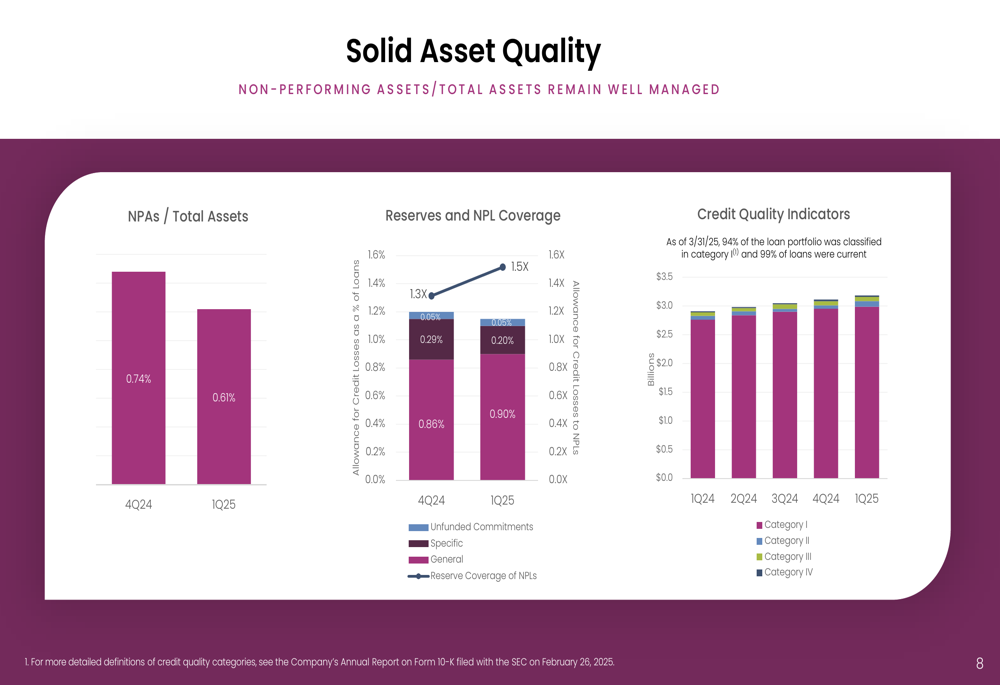

First Business Bank reported significant improvements in asset quality metrics during Q1 2025, with non-performing assets to total assets decreasing to 0.61% from 0.74% in the previous quarter:

The bank maintains a strong allowance for credit losses, with 94% of the loan portfolio classified in the highest credit quality category as of March 31, 2025, and 99% of loans current on payments.

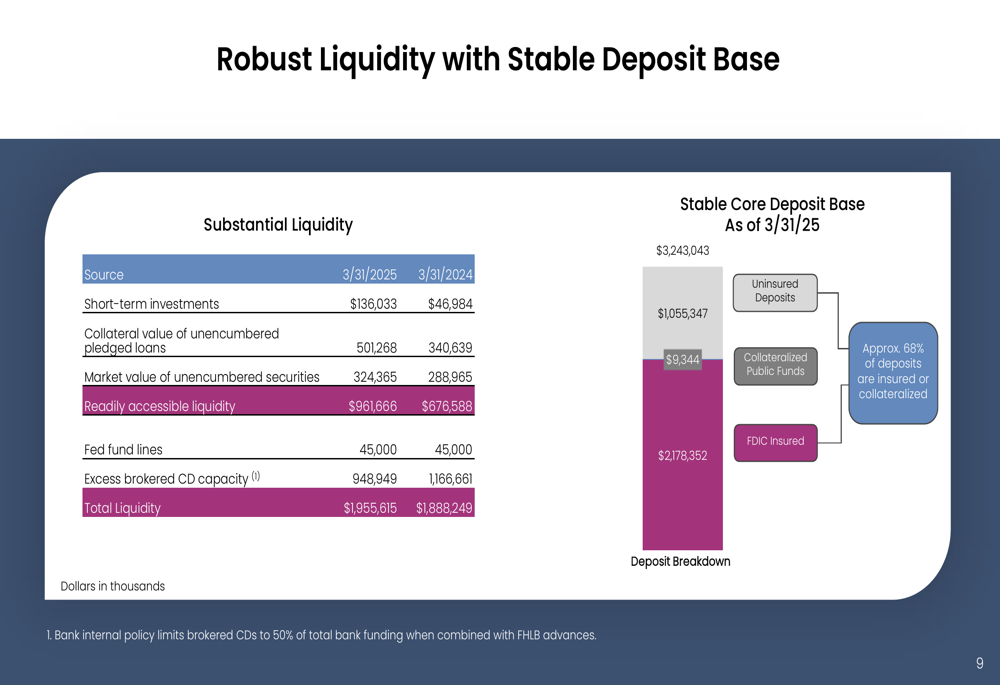

Liquidity remains robust with $1.96 billion in total liquidity as of March 31, 2025, compared to $1.89 billion a year earlier. The deposit base shows stability with 67% of deposits FDIC insured:

The bank’s capital position remains strong, with all regulatory capital ratios well above required levels. Tangible book value per share increased to $37.58 in Q1 2025, representing 9% growth from the linked quarter and 14% year-over-year growth.

Strategic Initiatives & Progress

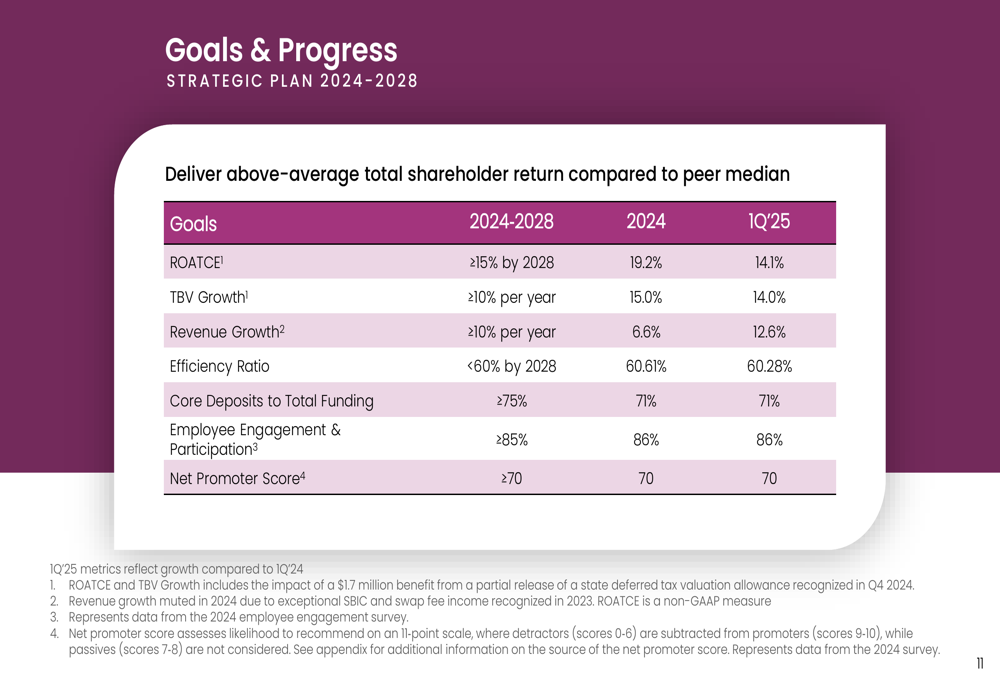

First Business Bank continues to make progress toward its strategic goals for 2024-2028, as shown in the following performance summary:

The bank achieved a return on average tangible common equity (ROATCE) of 14.1% in Q1 2025, approaching its goal of ≥15% by 2028. Tangible book value growth of 14.0% in Q1 2025 exceeded the target of ≥10% per year, while revenue growth of 12.6% also surpassed the ≥10% annual target.

The efficiency ratio improved slightly to 60.28% in Q1 2025 from 60.61% in 2024, moving closer to the goal of <60% by 2028. Core deposits to total funding remained stable at 71%, with a target of ≥75%.

Forward-Looking Statements

First Business Bank’s presentation indicates continued focus on its relationship banking model and disciplined interest rate risk management approach. The bank’s match-funding strategy for fixed-rate loans aims to lock in interest rate spreads and maintain stability in net interest margin.

The bank’s niche lending businesses are positioned to provide support in a potentially weaker economic environment, while the deposit-centric sales strategy continues to drive balanced growth. With strong capital ratios and improving asset quality, First Business Bank appears well-positioned to navigate the current economic landscape while pursuing its strategic growth objectives.

Investors should note that while the bank has made significant progress toward its strategic goals, challenges remain in achieving the targeted efficiency ratio and core deposits to total funding ratio. The slight decline in net interest margin from the linked quarter also bears watching as the bank navigates the evolving interest rate environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.