One & One Green Technologies stock soars 100% after IPO debut

Introduction & Market Context

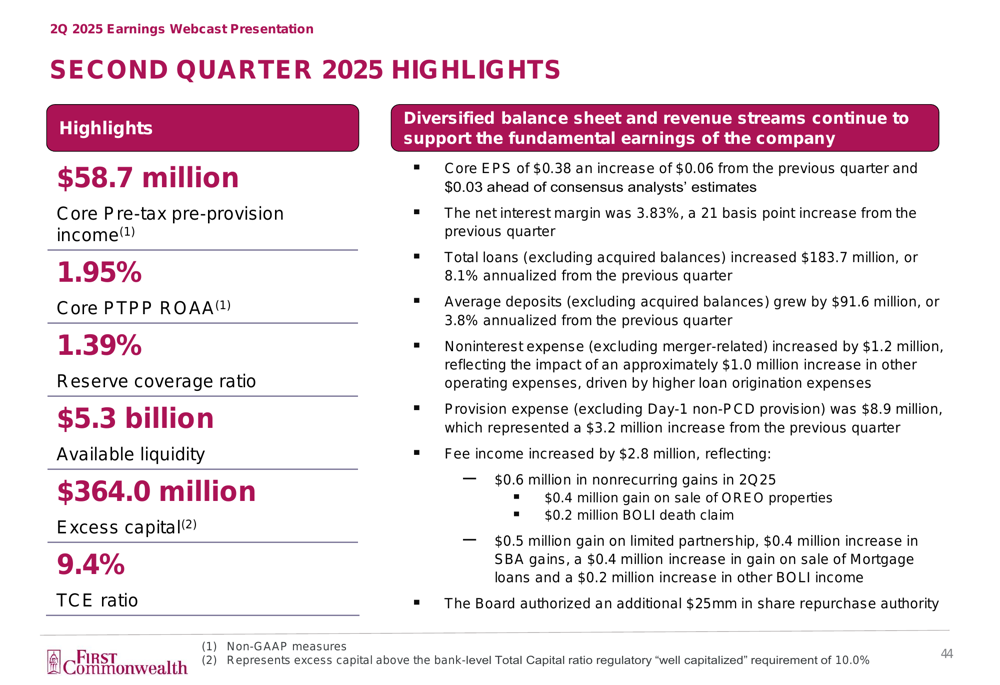

First Commonwealth Financial Corporation (NYSE:FCF) reported strong second-quarter results that exceeded analyst expectations, according to the company’s Q2 2025 earnings presentation released on July 30, 2025. The regional bank posted core earnings per share of $0.38, up $0.06 from the previous quarter and $0.03 ahead of consensus estimates.

The stock responded positively to the earnings beat, with shares trading up 3.64% at market close on the day of the announcement. This performance continues the company’s upward trajectory following its Q1 results, when it met earnings expectations with EPS of $0.32.

Quarterly Performance Highlights

First Commonwealth delivered substantial improvement across key financial metrics in the second quarter, with notable expansion in net interest margin and accelerated loan growth.

As shown in the following comprehensive overview of the quarter’s performance:

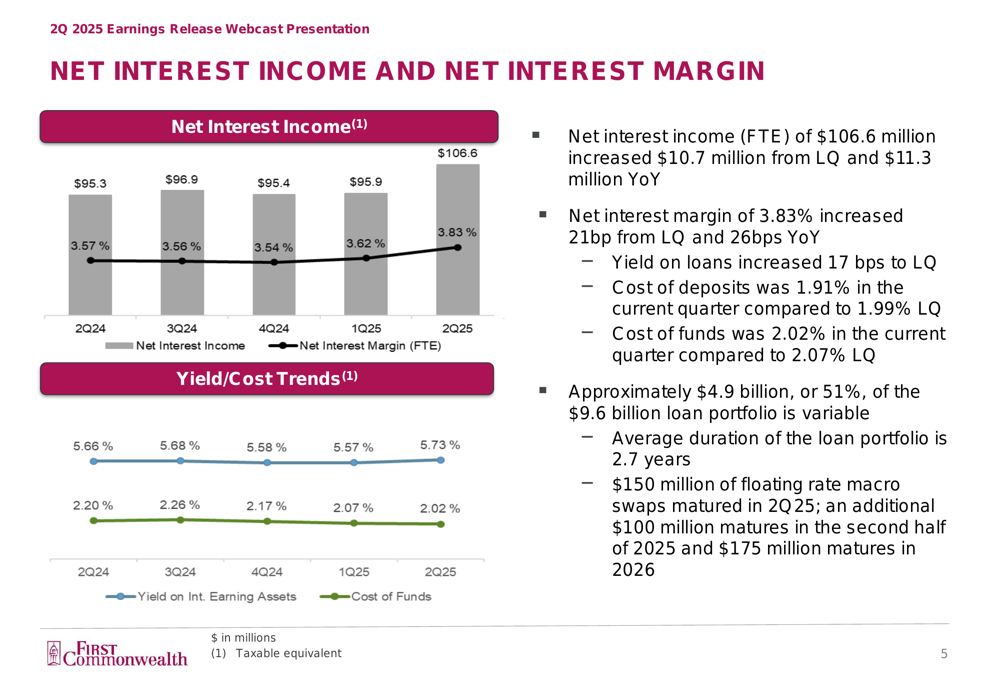

The bank reported core pre-tax pre-provision income of $58.7 million and a core PTPP return on average assets of 1.95%. Net interest margin expanded significantly to 3.83%, representing a 21 basis point increase from the previous quarter and a 26 basis point improvement year-over-year.

This margin expansion aligns with the company’s Q1 guidance, which projected NIM would reach "the high 370s by year-end." The current trajectory suggests First Commonwealth is on track to meet or potentially exceed this target.

Detailed Financial Analysis

The bank’s net interest income showed remarkable growth, increasing by $10.7 million from the previous quarter to $106.6 million. This improvement was driven by both higher loan volumes and improved spreads.

The following chart illustrates the positive trend in net interest income and margin:

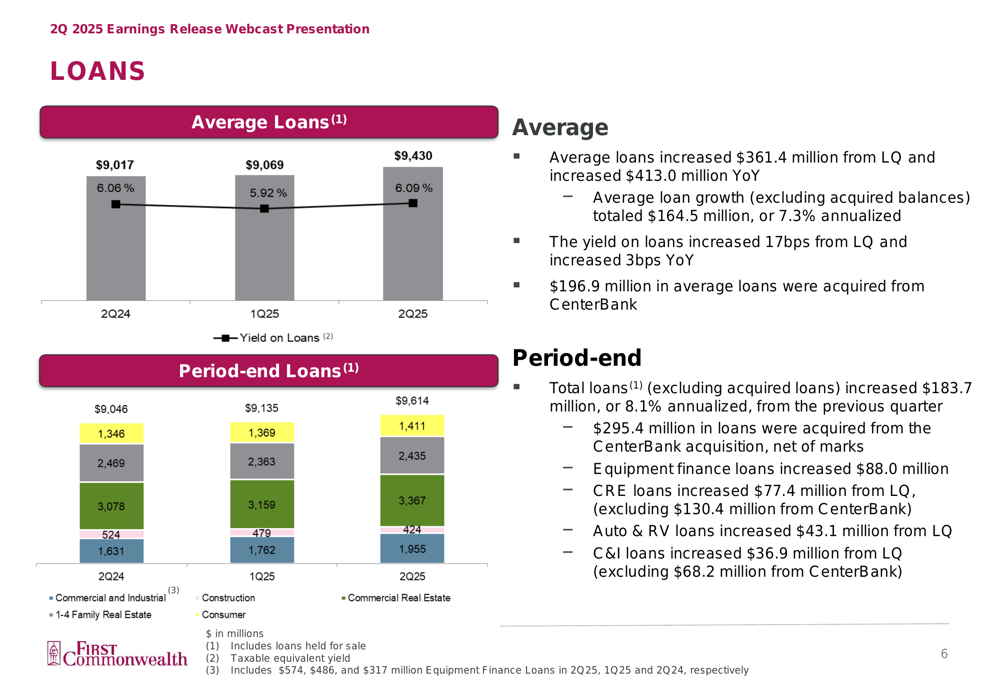

Loan growth was particularly strong in Q2, with total loans increasing by $183.7 million or 8.1% annualized, excluding acquired balances. This represents a significant acceleration from the 4.4% annualized growth reported in Q1 2025. The acquisition of CenterBank contributed an additional $295.4 million in loans, further bolstering the bank’s lending portfolio.

The composition and growth of the loan portfolio can be seen in the following chart:

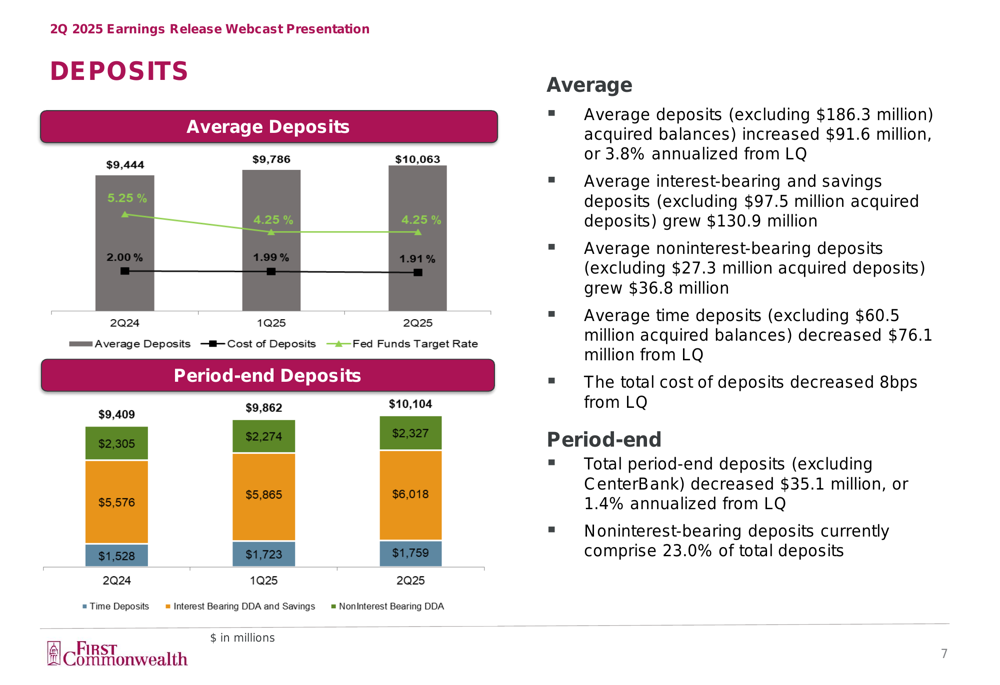

On the funding side, average deposits grew by $91.6 million or 3.8% annualized, excluding acquired balances. The bank also benefited from a reduction in funding costs, with the cost of deposits decreasing to 1.91% from 1.99% in the previous quarter.

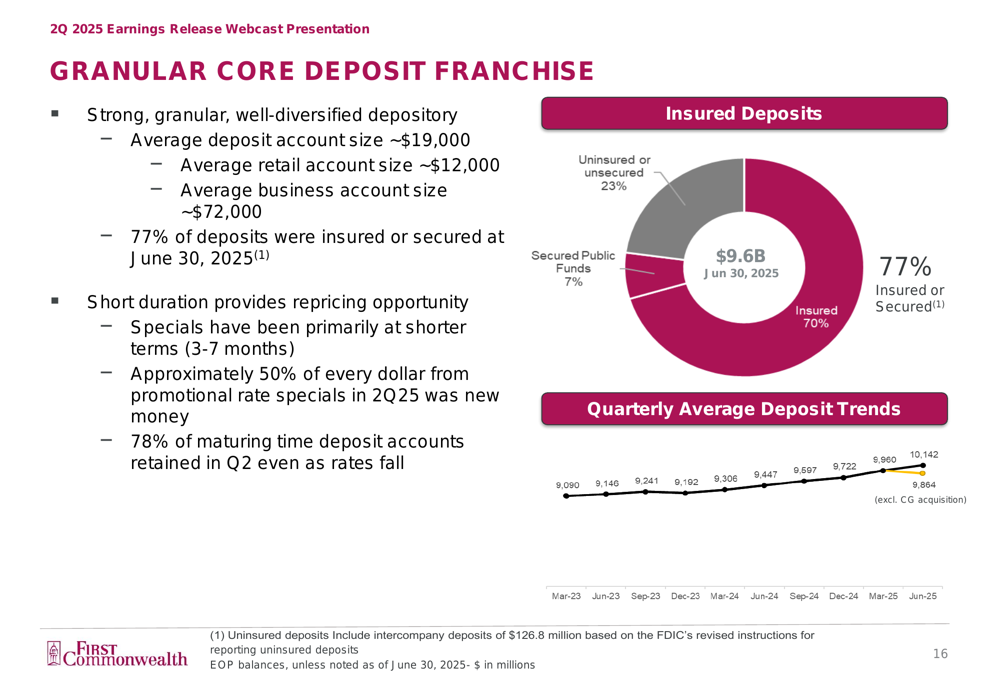

The following chart details the deposit composition and trends:

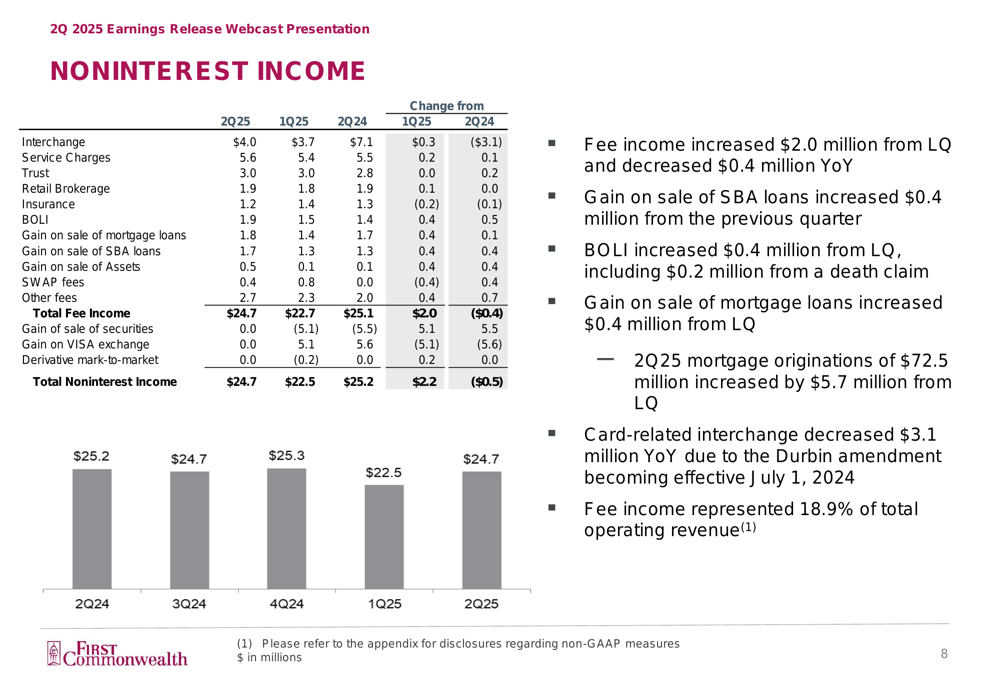

Fee income showed significant improvement, increasing by $2.8 million from the previous quarter. This growth was driven by gains across multiple categories, including SBA (LON:SBA) loans, mortgage sales, and BOLI income.

The following breakdown illustrates the sources of noninterest income:

Strategic Initiatives

First Commonwealth completed the acquisition of CenterBank during the quarter, which contributed significantly to the bank’s growth metrics. The acquisition added approximately $196.9 million in average loans and $186.3 million in average deposits.

The bank’s capital position remains strong, with a tangible common equity ratio of 9.4% and excess capital of $364.0 million. This robust capital base has enabled First Commonwealth to continue returning value to shareholders through dividends and share repurchases.

On July 29, 2025, the Board of Directors authorized an additional $25 million share repurchase program, following the near completion of the previous authorization. The bank had $6.2 million remaining under its current program as of June 30, 2025, after repurchasing 32,844 shares in Q2.

Credit Quality & Risk Management

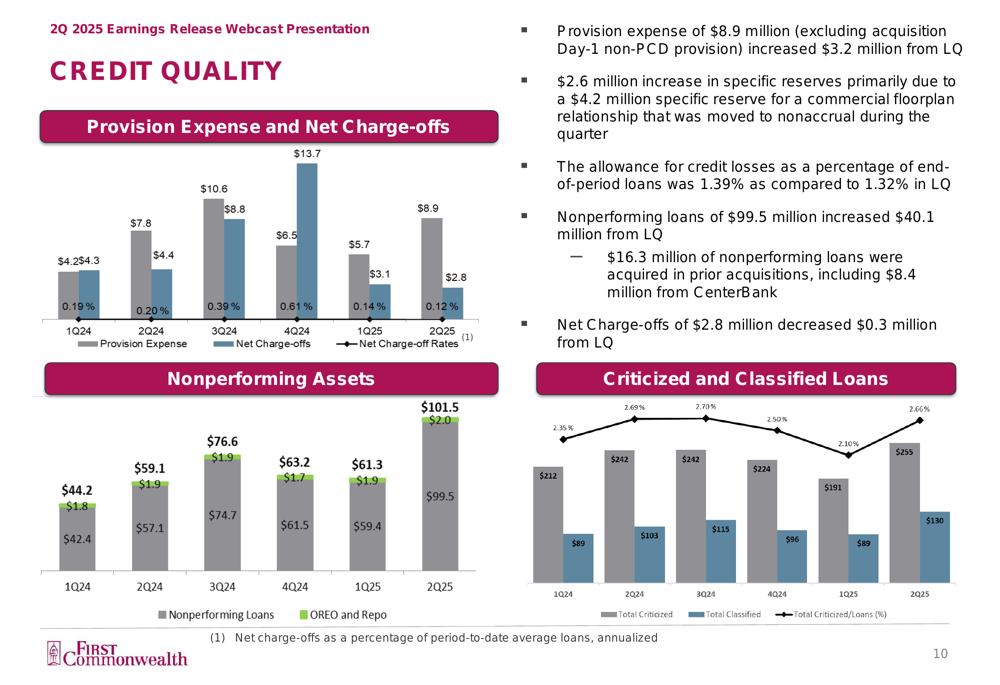

Despite the overall positive performance, First Commonwealth reported an increase in credit concerns during the quarter. Nonperforming loans rose to $99.5 million, up $40.1 million from the previous quarter. This increase was partially attributable to a commercial floorplan relationship that was moved to nonaccrual status, requiring a $4.2 million specific reserve.

The following chart illustrates the trends in credit quality:

The bank’s provision expense increased to $8.9 million, up $3.2 million from the previous quarter. The allowance for credit losses as a percentage of end-of-period loans rose to 1.39% compared to 1.32% in the previous quarter, reflecting the bank’s prudent approach to managing emerging credit risks.

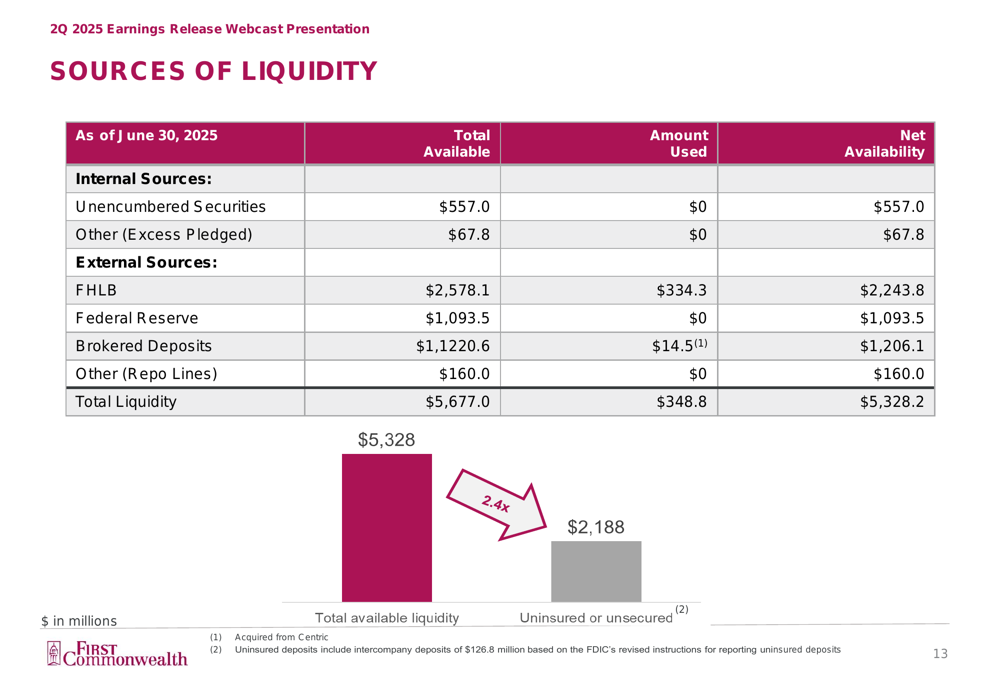

Despite these credit concerns, First Commonwealth maintains a strong liquidity position, with available liquidity of $5.3 billion, representing 2.4 times uninsured or unsecured deposits.

The following chart details the bank’s liquidity sources:

Forward-Looking Statements

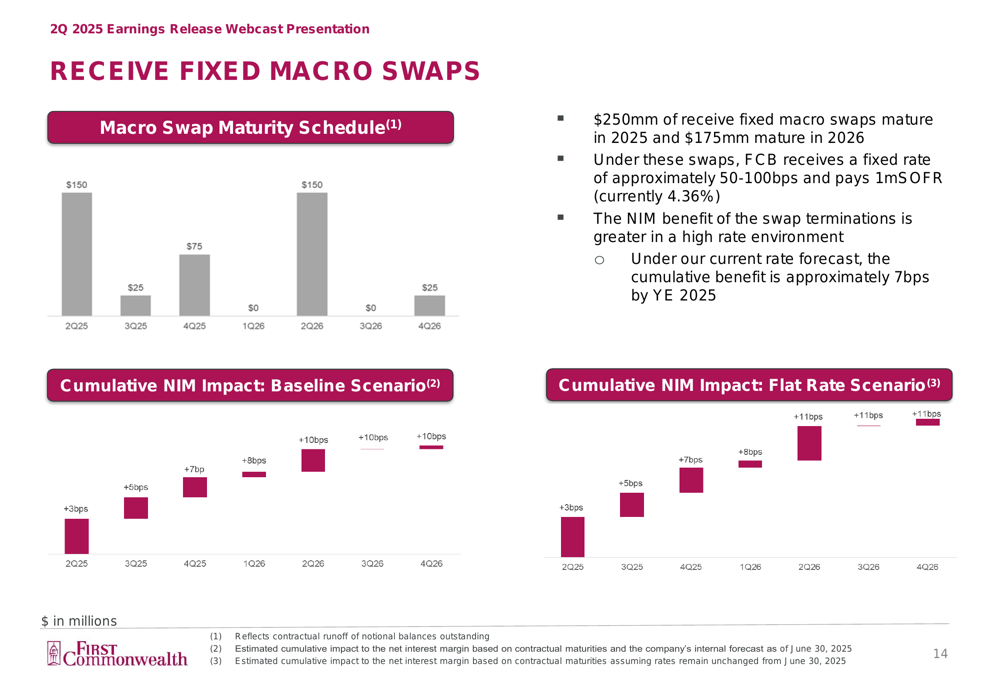

First Commonwealth is well-positioned to benefit from the current interest rate environment, particularly as its receive-fixed macro swaps mature. The bank has $250 million of receive-fixed macro swaps maturing in 2025 and $175 million maturing in 2026.

The following chart illustrates the expected impact on net interest margin:

Under the bank’s current rate forecast, these swap terminations are expected to provide a cumulative benefit of approximately 7 basis points to NIM by year-end 2025, further supporting the bank’s projection of continued margin expansion.

First Commonwealth’s investment securities portfolio remains conservative, with 94% consisting of Agency, CMO, and MBS securities. This approach is intended to maintain a pool of liquidity while managing interest rate risk.

The bank’s deposit base continues to be a source of strength, with 77% of deposits insured or secured as of June 30, 2025. The average deposit account size is approximately $19,000, reflecting a granular and stable funding base.

As shown in the following chart of the bank’s deposit characteristics:

With its strong capital position, improving net interest margin, and accelerated loan growth, First Commonwealth appears well-positioned for continued performance improvement in the second half of 2025, despite the noted increase in credit concerns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.