Gold prices briefly hit record high over $3,500/oz on fiscal, tariff concerns

Introduction & Market Context

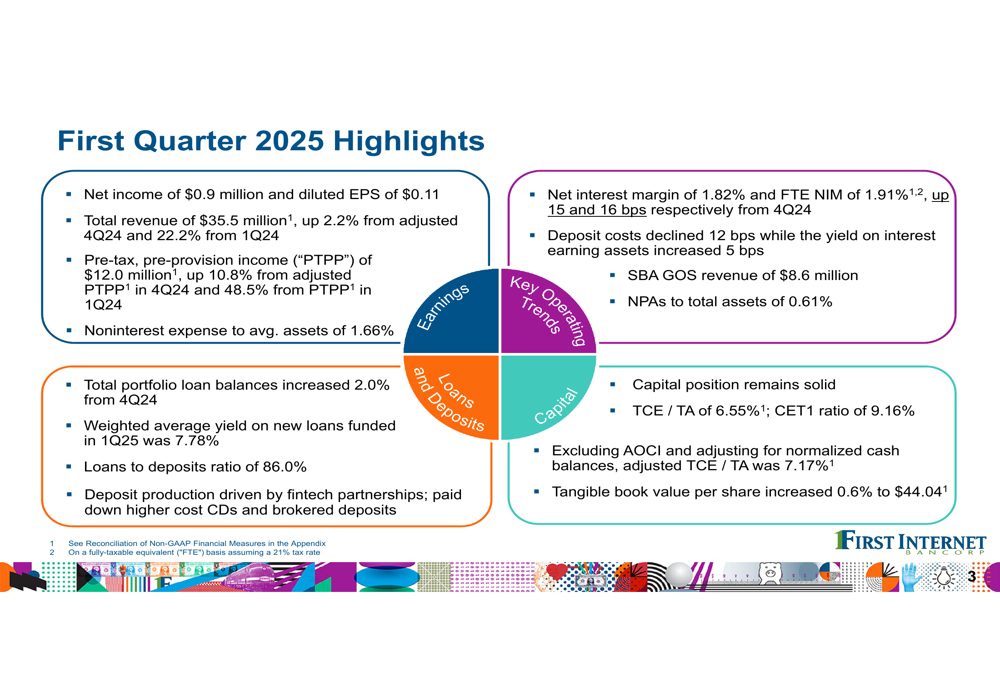

First Internet Bancorp (NASDAQ:INBK) released its first quarter 2025 financial results presentation on April 24, 2025, revealing a significant decline in profitability despite continued revenue growth. The company reported net income of $0.9 million and diluted earnings per share (EPS) of $0.11, a substantial decrease from the previous quarter’s EPS of $0.80. This earnings decline comes despite total revenue increasing to $35.5 million, up 2.2% from adjusted Q4 2024 and 22.2% from Q1 2024.

The company’s stock reacted negatively to the results, trading down 3.34% in premarket activity to $24.85, reflecting investor concerns about the sharp drop in profitability. This follows a pattern from the previous quarter, when shares also declined after the company missed EPS expectations despite revenue beats.

Quarterly Performance Highlights

First Internet Bancorp’s Q1 2025 results present a mixed picture, with strong revenue growth overshadowed by profitability challenges. The company’s pre-tax, pre-provision income (PTPP) reached $12.0 million, up 10.8% from adjusted PTPP in Q4 2024 and 48.5% from Q1 2024, demonstrating underlying operational strength.

As shown in the following quarterly highlights chart, the company maintained solid revenue growth while facing challenges in net income:

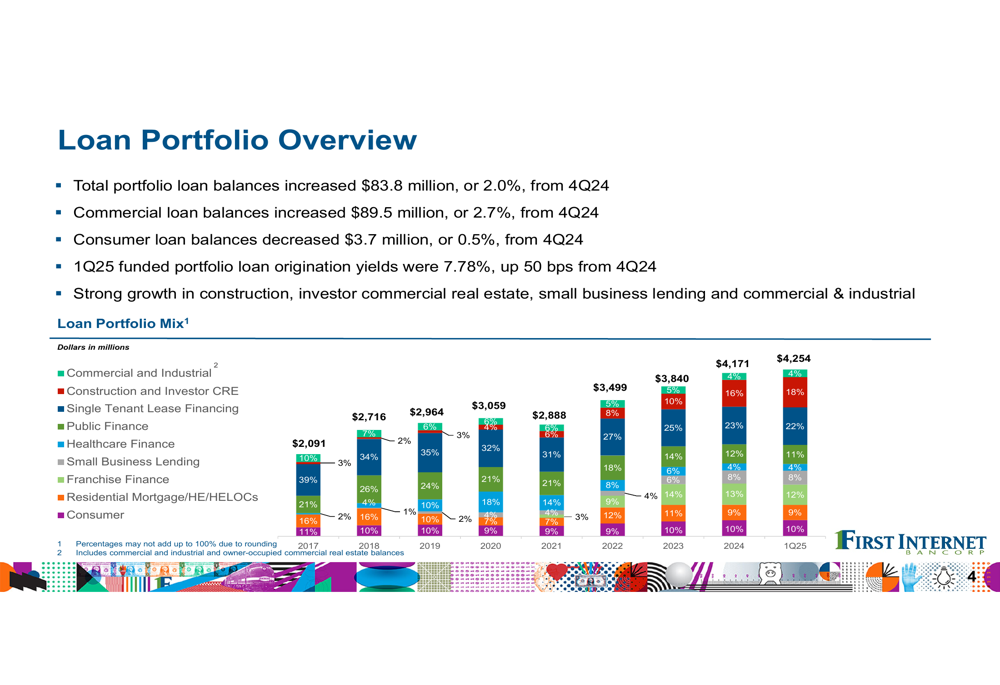

Total (EPA:TTEF) portfolio loan balances increased 2.0% from Q4 2024, with commercial loan balances growing 2.7% and consumer loan balances decreasing slightly by 0.5%. The weighted average yield on new loans funded in Q1 2025 was 7.78%, up 50 basis points from the previous quarter, indicating improved pricing on new originations.

The company’s loan portfolio continues to show diversification across multiple sectors, with construction and investor commercial real estate, single tenant lease financing, and small business lending representing significant portions of the portfolio:

Detailed Financial Analysis

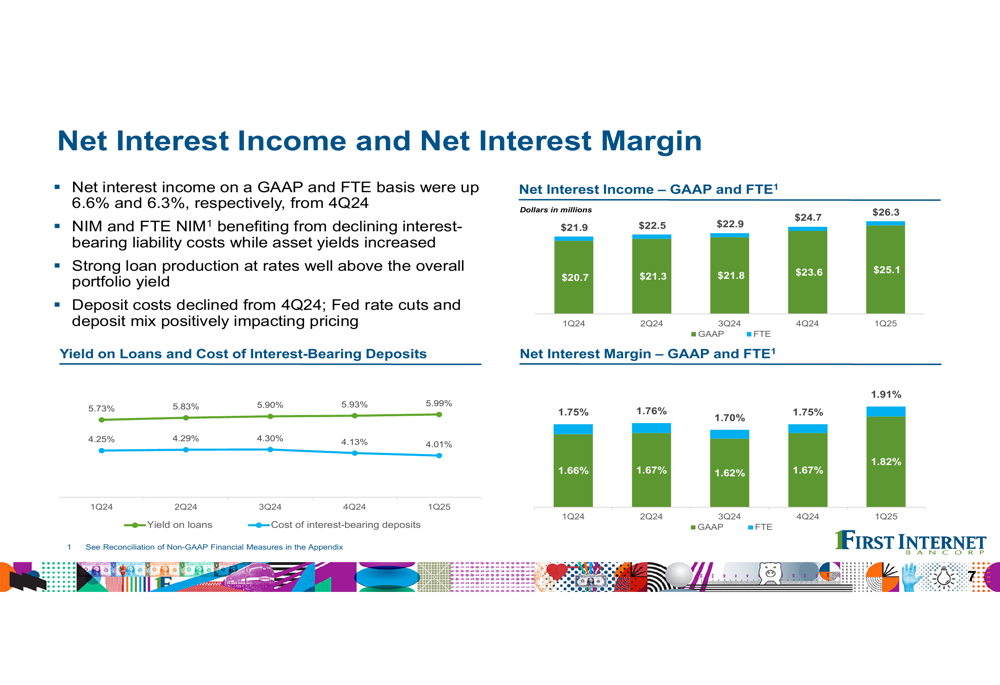

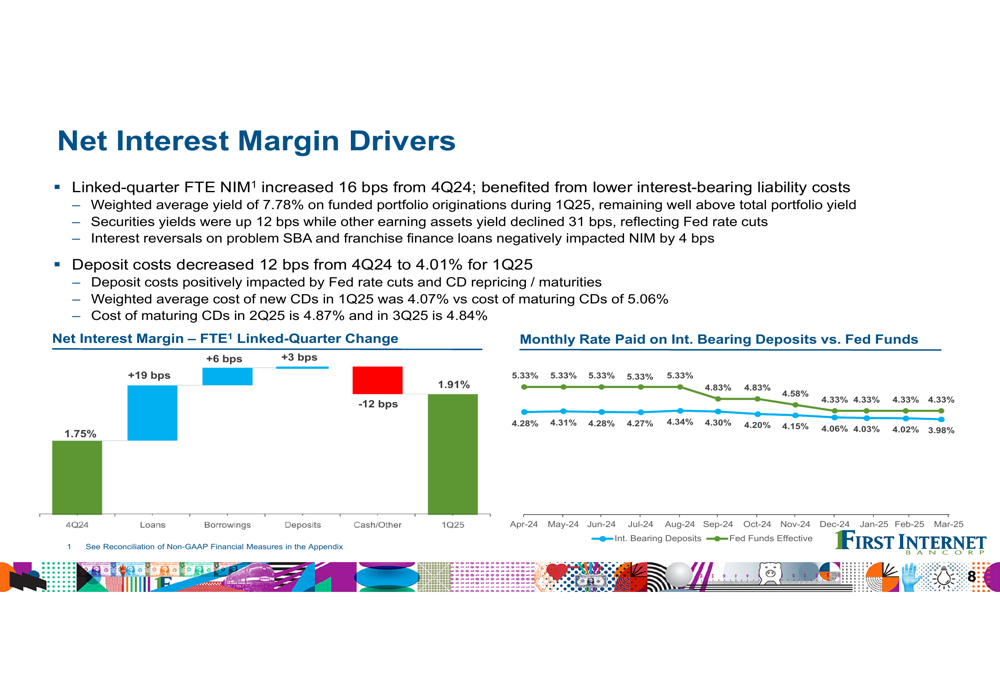

First Internet Bancorp’s net interest margin (NIM) showed improvement, reaching 1.82% on a GAAP basis and 1.91% on a fully taxable equivalent (FTE) basis, representing increases of 15 and 16 basis points respectively from Q4 2024. This improvement was driven by declining interest-bearing liability costs while asset yields increased.

The following chart illustrates the positive trend in net interest income and margin:

The margin improvement was primarily driven by lower deposit costs, which declined 12 basis points to 4.01% in Q1 2025. Meanwhile, the yield on interest-earning assets increased 5 basis points. The company benefited from Fed rate cuts and favorable CD repricing, with the weighted average cost of new CDs in Q1 2025 at 4.07% compared to the cost of maturing CDs at 5.06%.

This chart details the specific drivers of the net interest margin improvement:

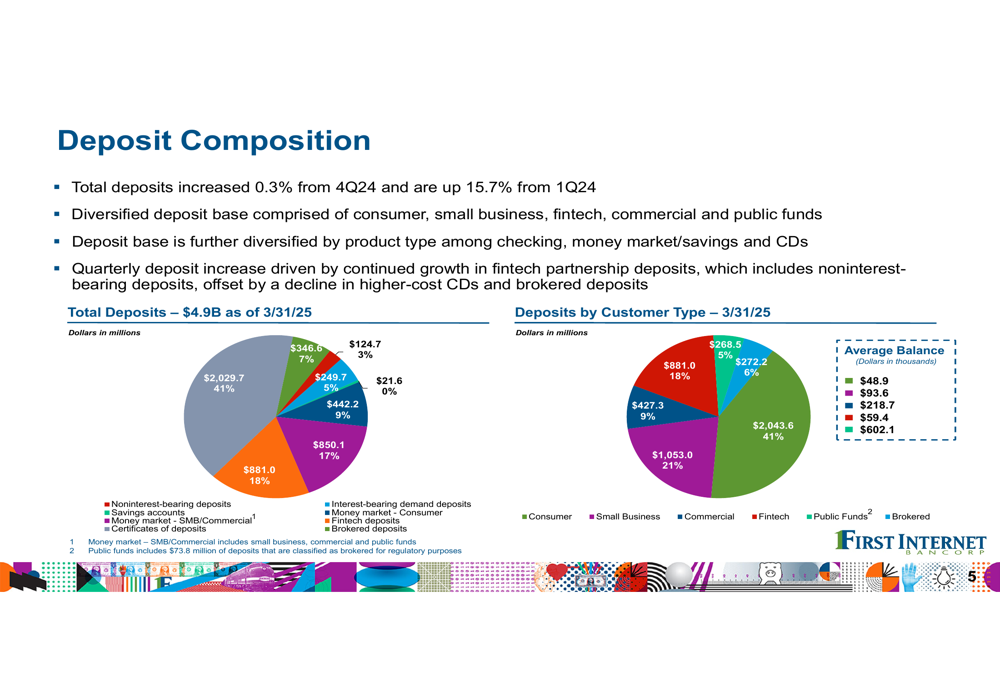

On the deposit front, First Internet Bancorp maintained a diversified base across consumer, small business, fintech, commercial, and public funds segments. Total deposits increased 0.3% from Q4 2024 and were up 15.7% from Q1 2024. The company’s deposit strategy focused on growing fintech partnership deposits while reducing higher-cost CDs and brokered deposits.

The following chart shows the company’s deposit composition:

Asset Quality Concerns

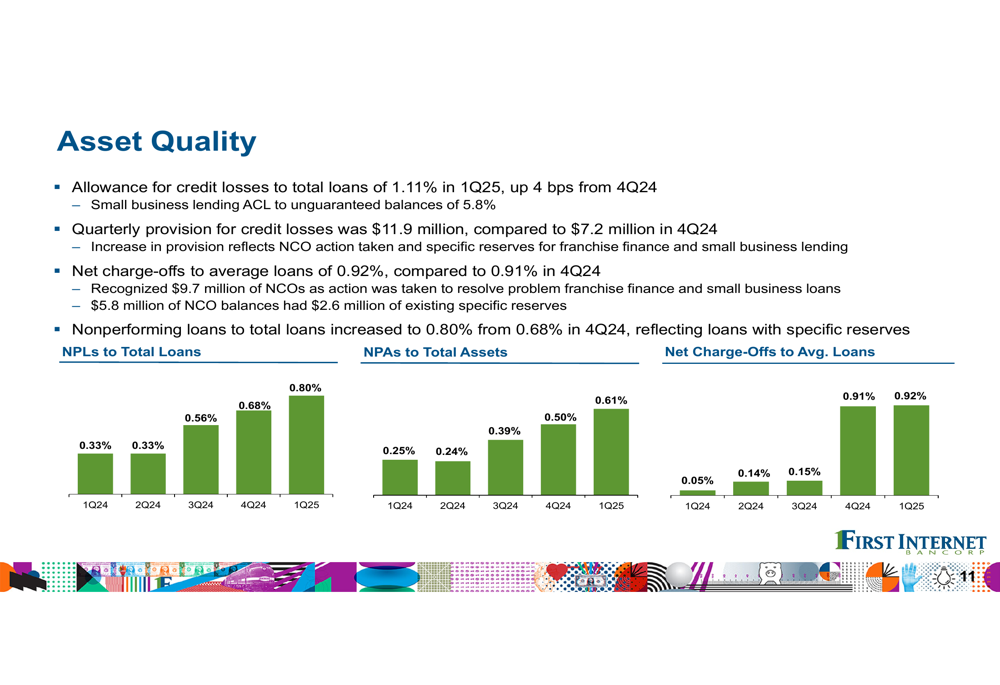

The most significant factor impacting First Internet Bancorp’s Q1 2025 profitability was a substantial increase in provision for credit losses, which rose to $11.9 million compared to $7.2 million in Q4 2024. This increase reflects deteriorating credit quality, particularly in the franchise finance and small business lending portfolios.

Net charge-offs to average loans increased slightly to 0.92% from 0.91% in Q4 2024, with the company recognizing $9.7 million of charge-offs as it took action to resolve problem loans. Nonperforming loans to total loans increased to 0.80% from 0.68% in the previous quarter.

The following chart illustrates the trends in asset quality metrics:

Despite these credit challenges, the company maintained a solid capital position. Tangible book value per share increased 0.6% to $44.04, while the tangible common equity to tangible assets ratio decreased slightly by 7 basis points to 6.55%. The company’s regulatory capital ratios remained well above minimum requirements.

Strategic Initiatives and Outlook

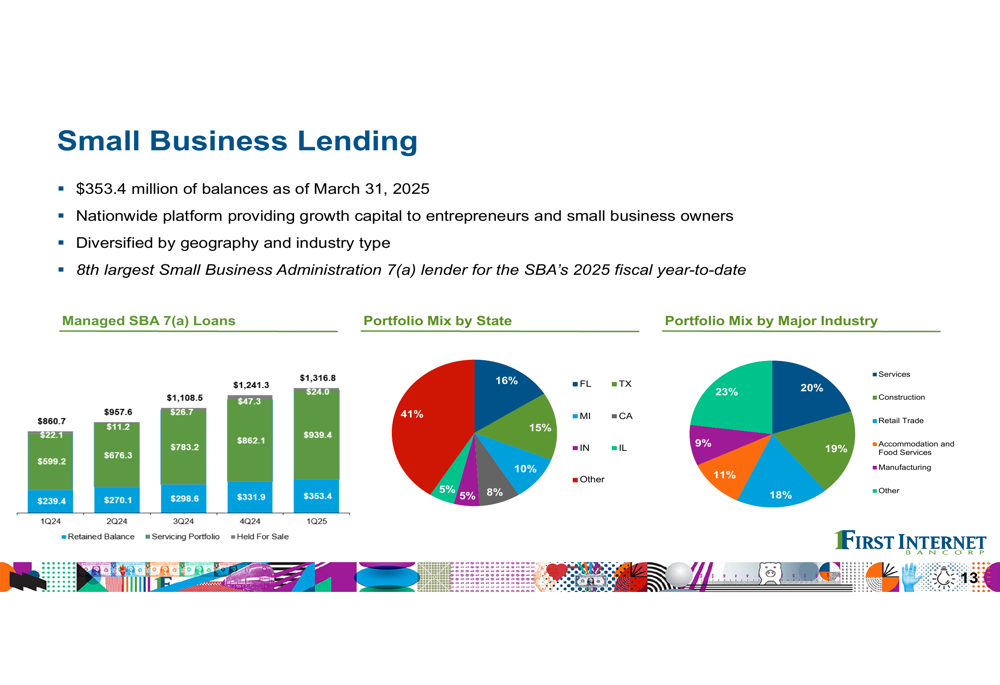

First Internet Bancorp continues to emphasize its Small Business Administration (SBA (LON:SBA)) lending program, which remains a key revenue driver. The company reported SBA gain-on-sale revenue of $8.6 million for Q1 2025 and maintains its position as the 8th largest SBA 7(a) lender for the SBA’s 2025 fiscal year-to-date.

The small business lending portfolio, which totaled $353.4 million as of March 31, 2025, is diversified by geography and industry:

The company’s liquidity position remains strong, with cash and unused borrowing capacity totaling $2.1 billion at the end of Q1 2025, representing 180% of total uninsured deposits. This provides flexibility to manage through credit challenges while continuing to fund loan growth.

Looking ahead, First Internet Bancorp faces the dual challenge of maintaining revenue growth while addressing credit quality concerns. The significant increase in loan loss provisions suggests potential continued pressure on earnings in the near term, though improved net interest margin and strong SBA lending activity provide positive counterbalances.

In the previous quarter’s earnings call, management had projected expense growth of 7-8% for 2025 and anticipated loan growth of 7-9%. While loan growth in Q1 2025 was below this annual target at 2.0%, the company’s focus on higher-yielding originations aligns with its strategy to improve profitability through margin expansion rather than volume alone.

The sharp decline in Q1 2025 earnings compared to the previous quarter’s results and management’s optimistic outlook suggests that credit quality challenges may have emerged more rapidly than anticipated, requiring investors to closely monitor asset quality metrics in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.