Vivek Ramaswamy buys Strive Inc (ASST) stock worth $1.25 million

Introduction & Market Context

First Interstate BancSystem, Inc. (NASDAQ:FIBK) presented its third quarter 2025 results on October 30, revealing a strategic repositioning effort that has contributed to an earnings beat despite modest revenue challenges. The Billings, Montana-based regional bank reported earnings per share of $0.69, surpassing analyst expectations of $0.62 by 11.29%, while revenue came in slightly below forecasts at $250.5 million.

Following the earnings release, FIBK shares closed at $32.25, up 1.09% from the previous close, reflecting positive investor sentiment toward the company’s strategic direction and capital management.

Quarterly Performance Highlights

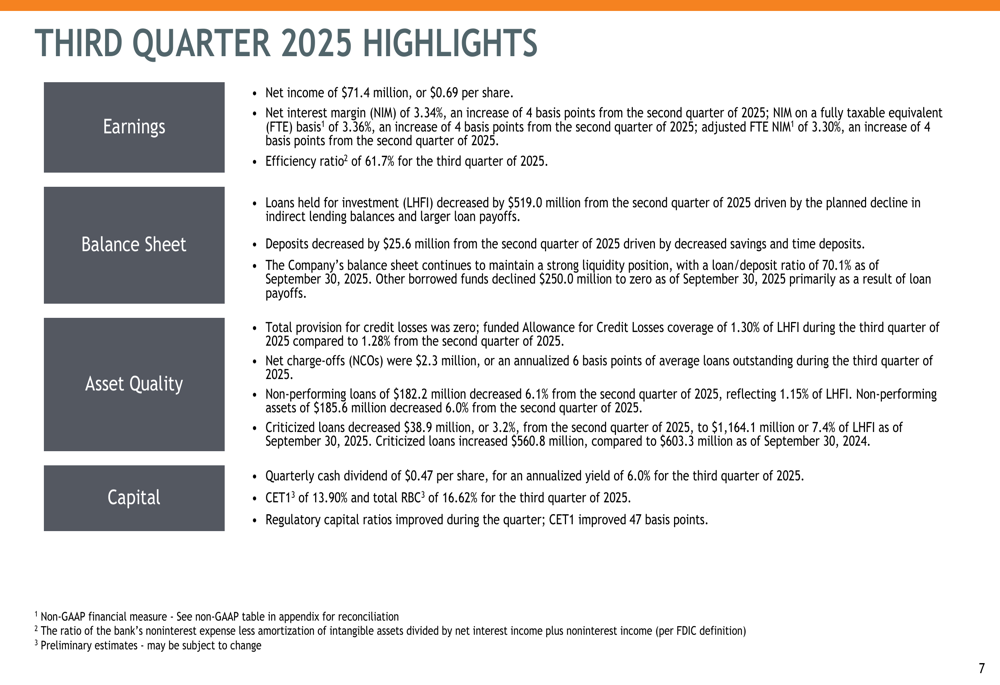

First Interstate reported net income of $71.4 million for Q3 2025, maintaining stable profitability despite ongoing strategic branch divestitures. The bank’s net interest margin stood at 3.34%, showing improvement as part of a broader trend of margin expansion that has seen a 22 basis point increase in adjusted FTE NIM since Q4 2024.

The company’s efficiency ratio was reported at 61.7%, reflecting ongoing efforts to streamline operations and reduce expenses. Total assets reached $27.3 billion, with loans held for investment at $15.8 billion and deposits at $22.6 billion.

As shown in the following quarterly highlights:

Strategic Initiatives

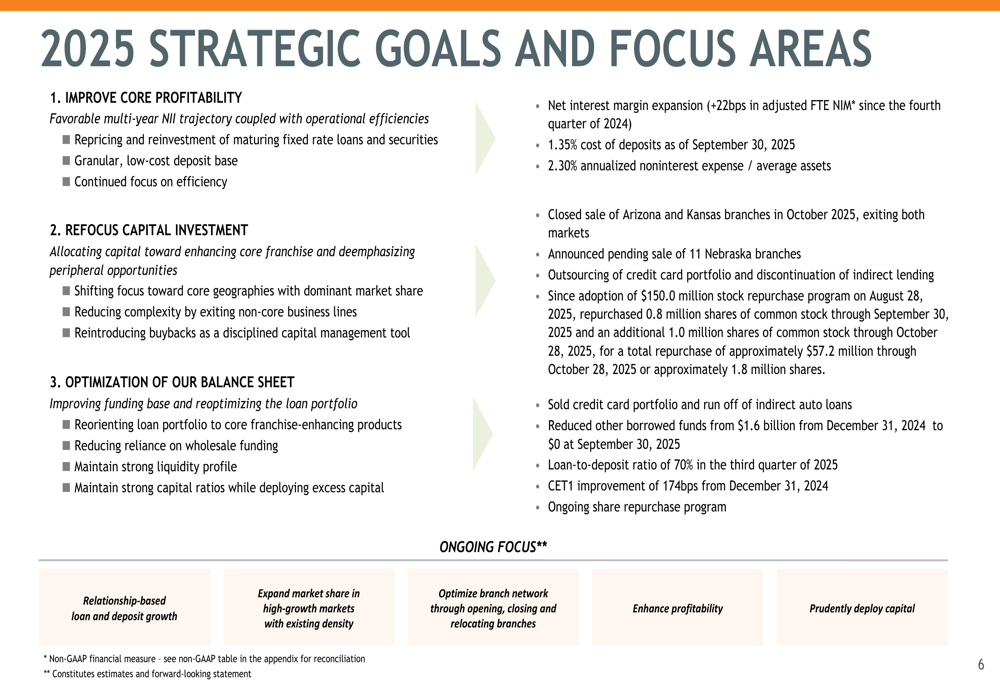

First Interstate has embarked on a strategic repositioning effort focused on three key areas: improving core profitability, refocusing capital investment, and optimizing the balance sheet. The company has already completed the sale of its Arizona and Kansas branches and has an agreement to sell 11 Nebraska branches to Security First Bank.

These strategic divestitures align with management’s focus on the Rocky Mountain Northwest region, where the bank holds stronger market positions and sees better growth opportunities. The company is also actively repurchasing shares, having bought back approximately 0.8 million shares at a weighted average price of $32.58 during Q3.

The company’s strategic focus areas are outlined below:

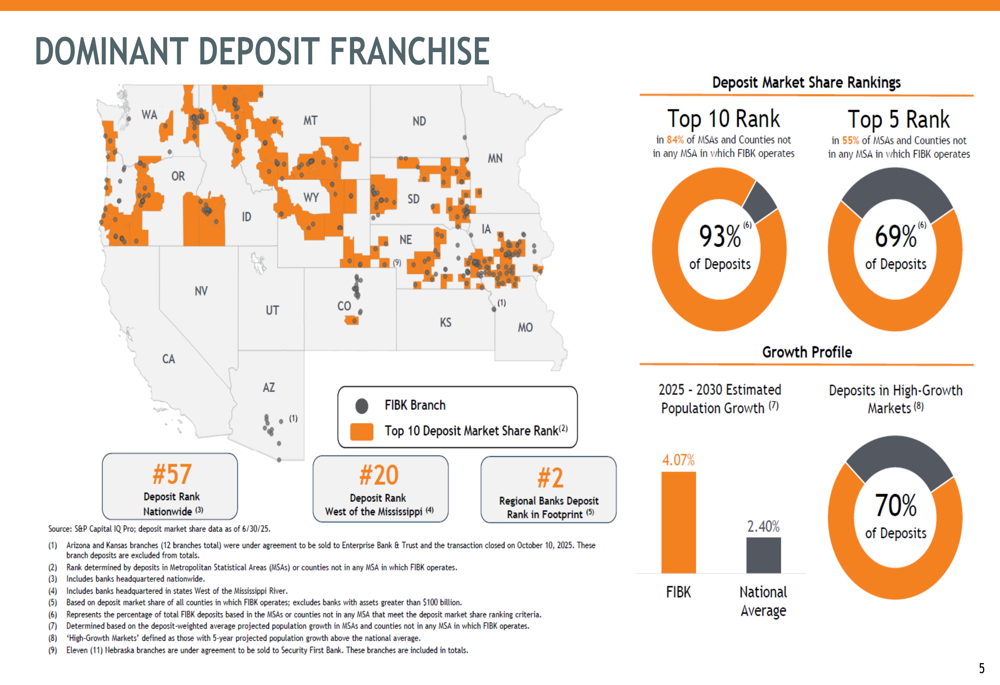

First Interstate maintains a dominant deposit franchise across its footprint, ranking in the top 10 in 84% of the MSAs and counties where it operates, and in the top 5 in 55% of these markets. The bank ranks 57th nationwide in deposits and 20th among banks west of the Mississippi River.

A key competitive advantage is the bank’s presence in high-growth markets, with 70% of deposits in areas expected to outpace the national average for population growth. FIBK’s markets are projected to grow 4.07% between 2025-2030, compared to the national average of 2.40%.

The following slide illustrates the bank’s market positioning:

Detailed Financial Analysis

First Interstate’s loan portfolio decreased by $519.0 million during Q3 2025, reflecting the bank’s strategic focus on quality over growth. The portfolio remains well-diversified, with commercial real estate representing 54% of loans (32.9% of which is owner-occupied), commercial loans at 15%, residential real estate at 13%, and the remainder distributed across construction, agriculture, and consumer segments.

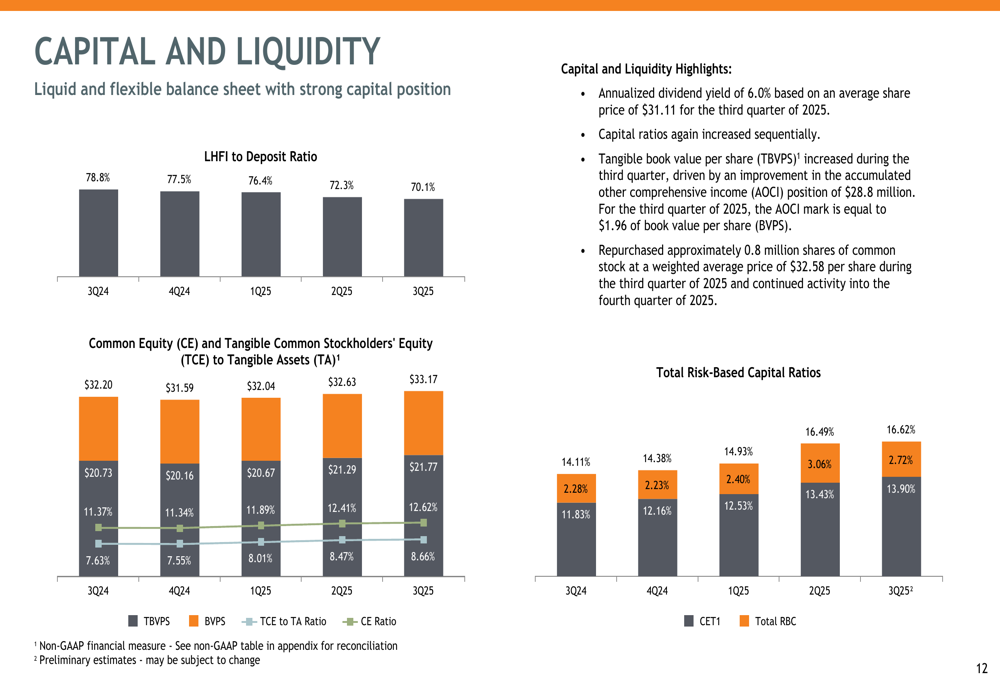

The bank’s capital position continues to strengthen, with Common Equity Tier 1 (CET1) ratio at 13.90% and total risk-based capital at 16.62%. The tangible common equity to tangible assets ratio stood at 8.66%, providing substantial loss-absorbing capacity. The loan-to-deposit ratio decreased to 70.1% in Q3 2025 from 78.8% a year earlier, highlighting improved liquidity.

The following capital and liquidity metrics demonstrate the bank’s strong financial foundation:

First Interstate maintains a conservative approach to credit risk, with its allowance for credit losses increasing to 1.30% of loans from 1.28% in the prior quarter. Net charge-offs remained low at just 6 basis points of average loans during Q3 2025, reflecting the bank’s disciplined underwriting standards.

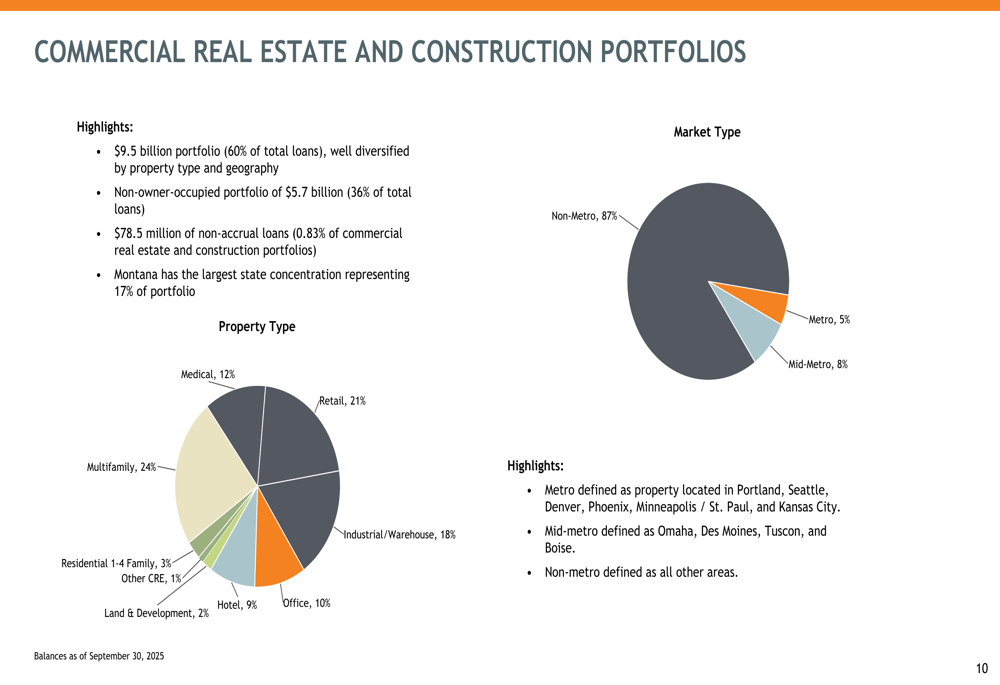

The commercial real estate portfolio, which represents 60% of total loans, is well-diversified by property type and geography. Montana represents the largest state concentration at 17% of the portfolio, with multifamily (24%), retail (21%), and industrial/warehouse (18%) comprising the largest property type segments.

The following breakdown illustrates the composition of the bank’s commercial real estate portfolio:

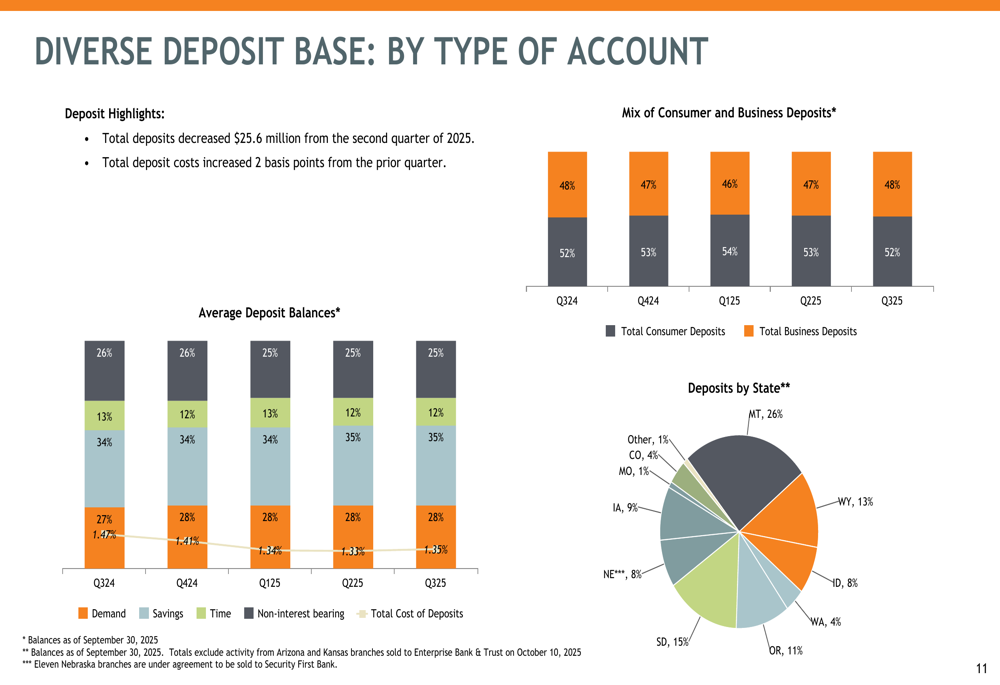

First Interstate’s deposit base remains diverse both geographically and by account type. Total deposits decreased by $25.6 million from Q2 2025, while deposit costs increased by just 2 basis points quarter-over-quarter. The deposit mix includes a healthy proportion of non-interest bearing accounts, helping to moderate overall funding costs.

The geographic distribution of deposits spans multiple states, with Montana representing the largest concentration at 26%, followed by South Dakota at 15% and Wyoming at 13%.

Forward-Looking Statements

Looking ahead, First Interstate is positioned for potential earnings growth as its fixed and adjustable rate loan portfolio reprices. Through 2027, approximately $3.5 billion of loans with a weighted average rate of 4.5% are expected to mature or reprice, potentially providing yield enhancement in a stable or declining rate environment.

Similarly, $2.1 billion of fixed and adjustable rate securities with a weighted average rate of 2.4% are expected to generate cashflows through 2027, providing reinvestment opportunities at potentially higher yields.

During the earnings call, CEO Jim Reuter emphasized the company’s disciplined approach to growth, stating, "We’re not going to chase growth for growth’s sake, but we want to grow, and we’re going to be smart about it." He also highlighted the bank’s "strong balance sheet" with "liquidity" and "strong capital" as "a position of strength to operate from."

Management anticipates mid-single-digit growth in net interest income for 2026, with flat total loans and modest deposit growth. The company is targeting low single-digit expense growth and continues its share repurchase program with a $150 million authorization.

While First Interstate faces challenges including muted real estate lending demand and increased competition in metropolitan markets, its strategic repositioning, strong capital position, and presence in high-growth markets provide a solid foundation for navigating the evolving banking landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.