Street Calls of the Week

Introduction & Market Context

First Interstate BancSystem, Inc. (NASDAQ:FIBK) presented its second quarter 2025 results on July 29, showing significant improvement over its disappointing first quarter. The Billings, Montana-based regional bank reported net income of $71.7 million, or $0.69 per share, representing a substantial increase from the $0.49 per share reported in Q1 2025, which had missed analyst expectations.

The bank’s stock closed at $29.38 on July 29, down 0.91% for the day, but has recovered from its post-Q1 earnings dip when it fell to $26.14 following the earnings miss. With a market capitalization of $3.0 billion and an annualized dividend yield of 7.0%, First Interstate continues to position itself as a stable income investment while executing on its strategic repositioning.

Quarterly Performance Highlights

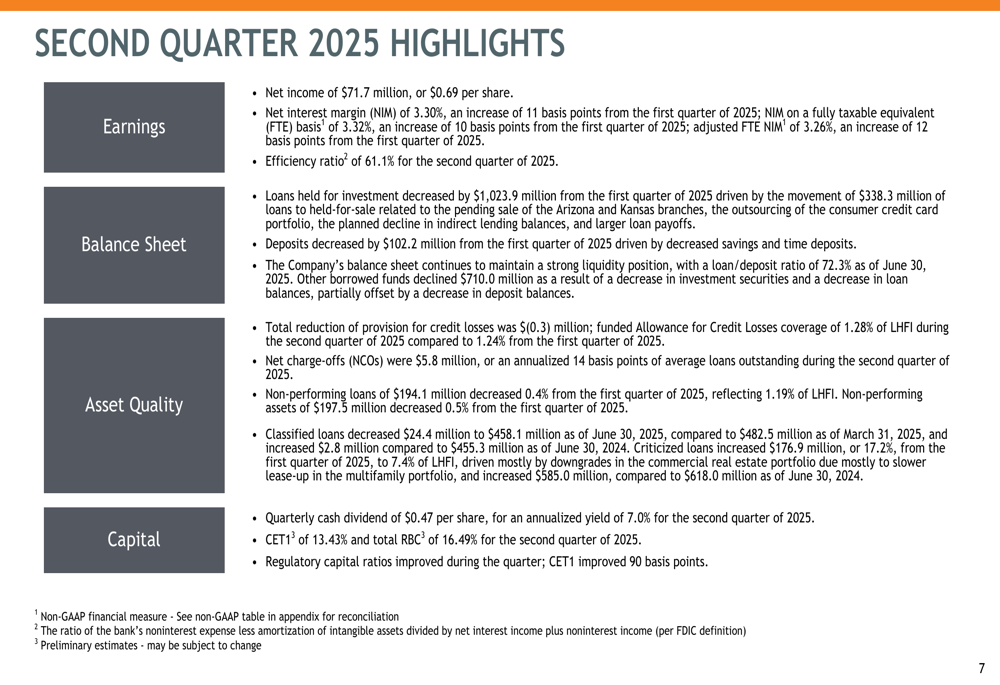

First Interstate’s second quarter results showed marked improvement across several key metrics. The company reported net income of $71.7 million ($0.69 per share), with a net interest margin (NIM) of 3.30%, up from 3.22% in the previous quarter. The efficiency ratio improved to 61.1%, reflecting better operational performance.

As shown in the following quarterly highlights summary:

The bank’s provision for credit losses was $(0.3) million, indicating confidence in the quality of its loan portfolio. Asset quality remained stable with the allowance for credit losses (ACL) coverage at 1.28% of loans held for investment. Net charge-offs totaled $5.8 million, representing just 14 basis points of average loans.

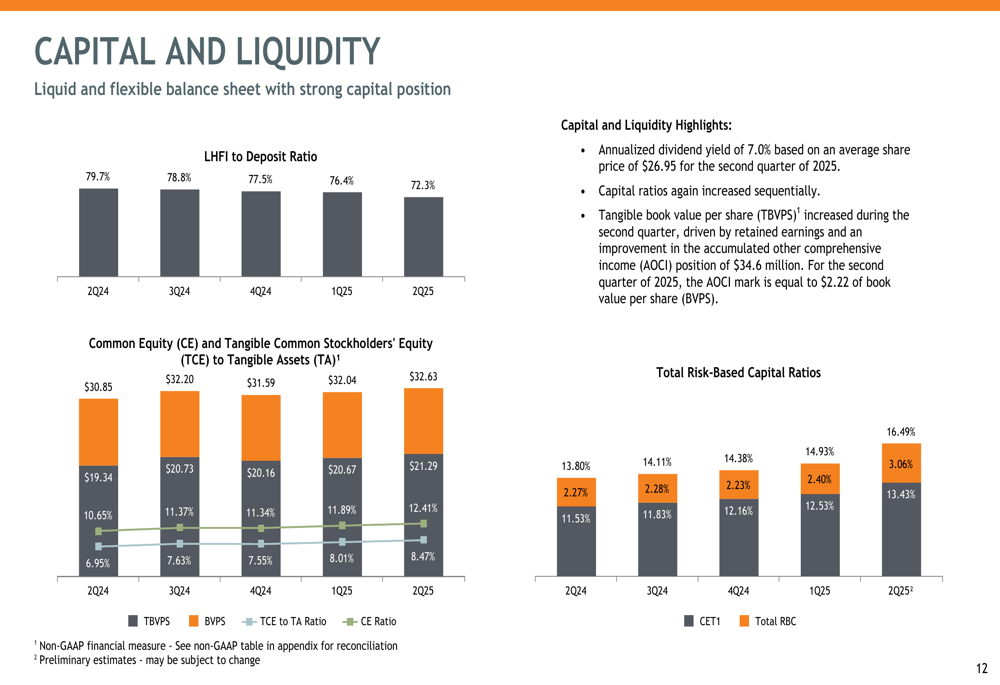

Capital ratios continued to strengthen, with Common Equity Tier 1 (CET1) at 13.43% and Total (EPA:TTEF) Risk-Based Capital at 16.49%. The company maintained its quarterly dividend at $0.47 per share, supporting the attractive 7.0% yield.

Strategic Initiatives

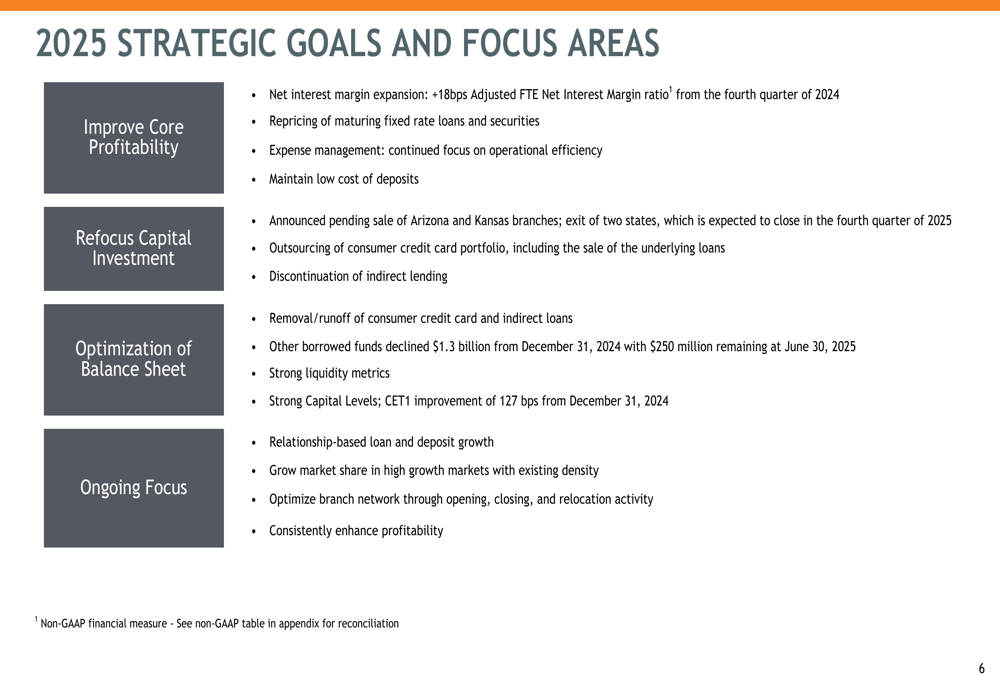

First Interstate’s presentation highlighted its ongoing strategic repositioning, which aligns with CEO Jim Reuter’s Q1 statement about "deemphasizing large scale M&A and refocusing on full relationship banking." The bank is executing several strategic initiatives aimed at improving profitability and optimizing its footprint.

The company’s strategic goals for 2025 focus on four key areas:

Notably, the bank is selling its Arizona and Kansas branches and outsourcing its consumer credit card portfolio. These moves are part of a broader strategy to focus on markets where First Interstate has stronger market positions. The Q2 results included a $7.3 million valuation allowance for loans transferred to held for sale related to the pending branch sales, as well as a $4.3 million gain associated with the outsourcing of the consumer credit card portfolio.

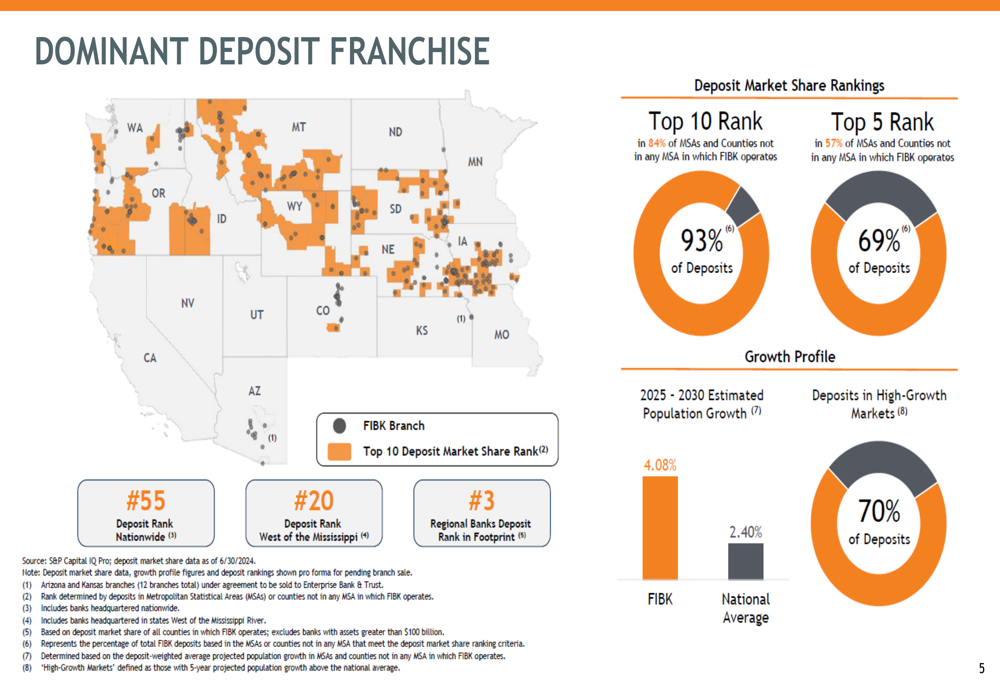

First Interstate is leveraging its dominant position in its core markets, where it ranks in the top 10 in 84% of its MSAs and counties, and in the top 5 in 57% of these markets. The bank is focusing on high-growth regions, with projected population growth in its footprint (4.08%) significantly exceeding the national average (2.40%).

As illustrated in the following deposit franchise overview:

Balance Sheet and Portfolio Management

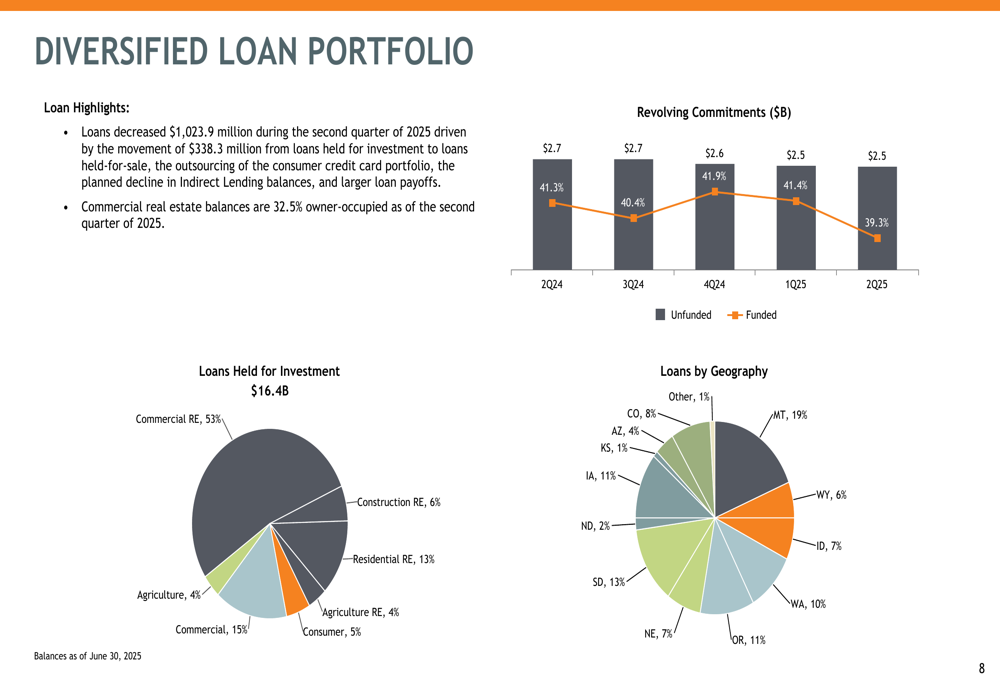

The bank’s balance sheet continues to evolve as part of its strategic repositioning. Loans decreased by $1,023.9 million during the quarter, while deposits decreased by $102.2 million. The loan-to-deposit ratio stood at 72.3%, indicating strong liquidity.

First Interstate maintains a diversified loan portfolio, with commercial real estate representing the largest segment at 53% of total loans. The portfolio is geographically diverse across 12 states, with Montana (19%), South Dakota (13%), and Oregon/Iowa (11% each) representing the largest concentrations.

The following chart illustrates the loan portfolio composition:

The bank’s deposit base remains stable, with a good mix between consumer (47%) and business (53%) deposits. Total deposit costs declined by 1 basis point from the prior quarter to 1.33%, helping support the improved net interest margin.

First Interstate’s investment portfolio is positioned to benefit from asset repricing opportunities. Through 2026, $2.0 billion of fixed and adjustable rate loans at a weighted average rate of 4.3% are expected to mature or reprice, and $1.4 billion of securities cashflows are expected at a weighted average rate of 2.6%. These repricing opportunities should support continued NIM expansion.

Capital and liquidity remain strong points for the bank. Tangible book value per share increased during the second quarter to $21.29, while the tangible common equity to tangible assets ratio improved to 8.47%.

Forward-Looking Statements

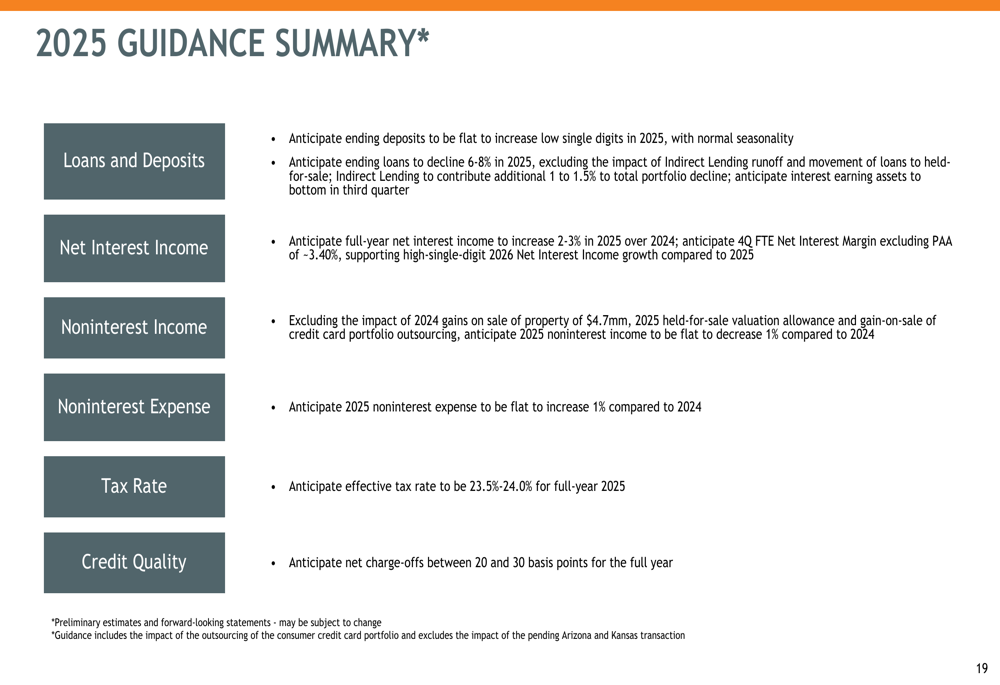

First Interstate provided specific guidance for the remainder of 2025, projecting continued improvement in key metrics despite the strategic reduction in loan balances.

The company’s 2025 guidance includes:

The bank anticipates ending loans to decline 6-8% in 2025, reflecting the strategic repositioning of its portfolio. Despite this reduction, net interest income is expected to increase 2-3% over 2024, with the fourth quarter FTE net interest margin (excluding purchase accounting accretion) projected to reach approximately 3.40%.

This guidance represents an improvement from the outlook provided after Q1 2025, when the bank projected net interest income growth of 3.5-5.5% for 2025. The adjustment likely reflects the accelerated timeline for portfolio repositioning, with short-term loan reductions impacting total interest income while improving margins.

Noninterest income is expected to be flat to down 1% compared to 2024, while noninterest expenses are projected to be flat to up 1%, indicating continued focus on operational efficiency. The bank anticipates net charge-offs between 20 and 30 basis points for the full year, reflecting a conservative credit outlook.

First Interstate’s improved Q2 performance and strategic execution suggest the bank is making progress on its repositioning efforts after the Q1 disappointment. With its strong capital position, attractive dividend yield, and clear strategic direction, the bank appears well-positioned to navigate the current banking environment while building long-term value for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.