JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

First Watch Restaurant Group (LON:RTN) Inc (NASDAQ:FWRG), a leader in the Daytime Dining category operating from 7 am to 2:30 pm, presented its Q1 2025 earnings results on May 6, 2025. The company, which focuses on made-to-order breakfast, brunch, and lunch using fresh ingredients, continues to expand its footprint while navigating profitability challenges in the current economic environment.

First Watch’s stock closed at $18.61 on May 5, 2025, but was down 2.74% in premarket trading to $18.10 ahead of the earnings presentation, suggesting investor concerns about the company’s performance despite its continued revenue growth.

The company positions itself to capitalize on long-term consumer trends including the growing breakfast daypart, increasing demand for fresh food, and on-demand dining preferences.

Quarterly Performance Highlights

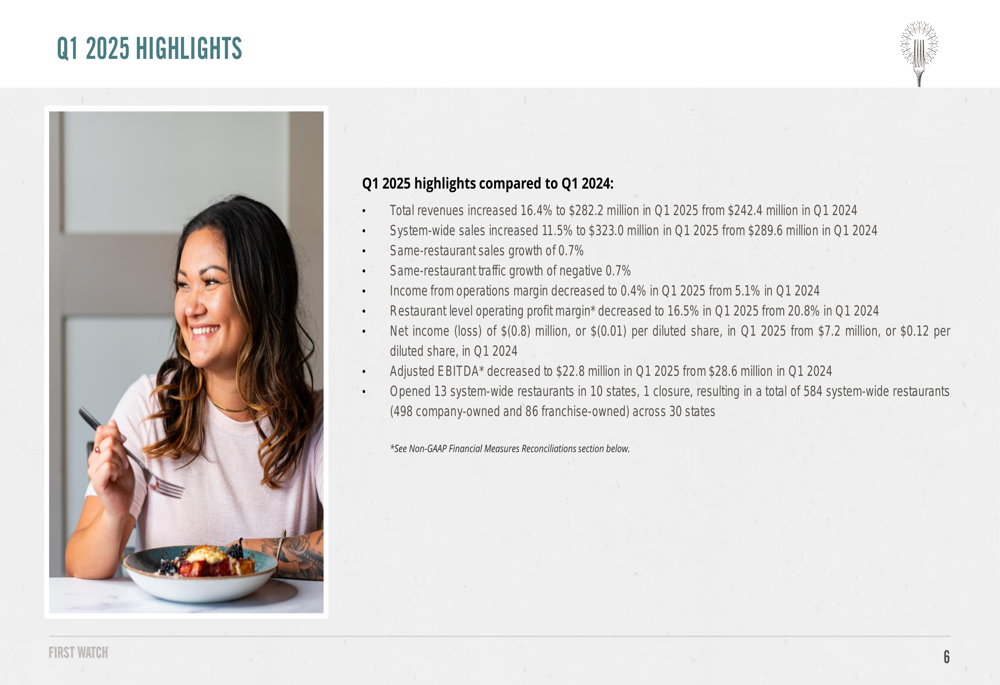

First Watch reported total revenues of $282.2 million in Q1 2025, a 16.4% increase from $242.4 million in Q1 2024. System-wide sales grew 11.5% to $323.0 million compared to $289.6 million in the prior year period. Same-restaurant sales showed modest growth of 0.7%, while same-restaurant traffic declined by 0.7%, indicating that price increases rather than customer volume drove the sales growth.

Despite the revenue growth, profitability metrics declined significantly. Income from operations margin decreased to 0.4% in Q1 2025 from 5.1% in Q1 2024, while restaurant level operating profit margin fell to 16.5% from 20.8% in the same period. The company reported a net loss of $0.8 million, or $(0.01) per diluted share, compared to net income of $7.2 million, or $0.12 per diluted share, in Q1 2024.

The following slide summarizes the key financial highlights from the quarter:

CEO Chris Tomasso provided an optimistic view of the results, focusing on the encouraging same-restaurant traffic trends that continue patterns seen at the end of 2024. He emphasized the strength and resilience of the First Watch brand, along with the success of new restaurant openings and the robust development pipeline despite the challenging macroeconomic environment.

Detailed Financial Analysis

The decline in profitability metrics can be attributed to several factors, including higher food and beverage costs, which increased to $66.6 million in Q1 2025 from $52.2 million in Q1 2024, and higher labor and other related expenses, which rose to $96.8 million from $79.7 million. These increases outpaced revenue growth, putting pressure on margins.

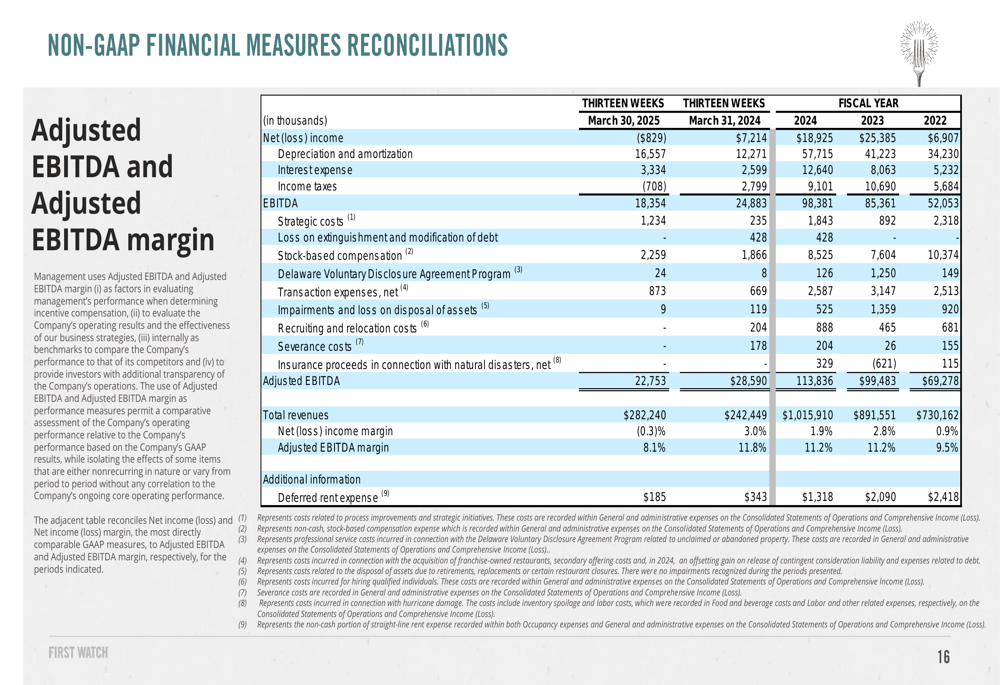

Adjusted EBITDA decreased to $22.8 million in Q1 2025 from $28.6 million in Q1 2024, reflecting the operational challenges the company faced during the quarter. The reconciliation of net income to Adjusted EBITDA shows the various adjustments made to arrive at this non-GAAP measure:

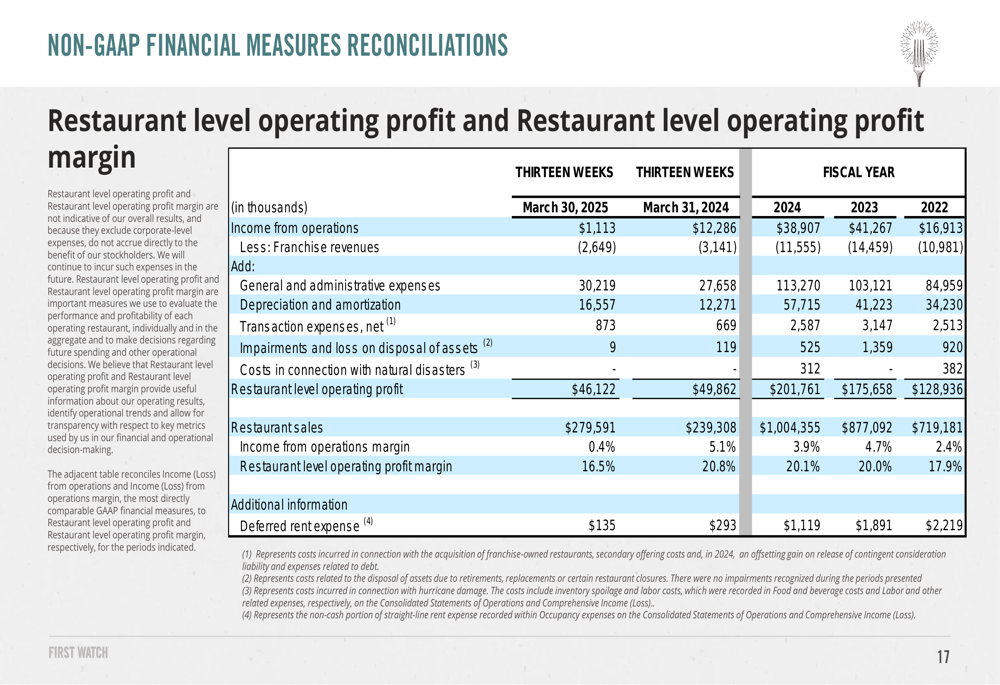

Similarly, the reconciliation of income from operations to restaurant-level operating profit provides insight into the company’s core restaurant operations performance:

Strategic Initiatives & Expansion

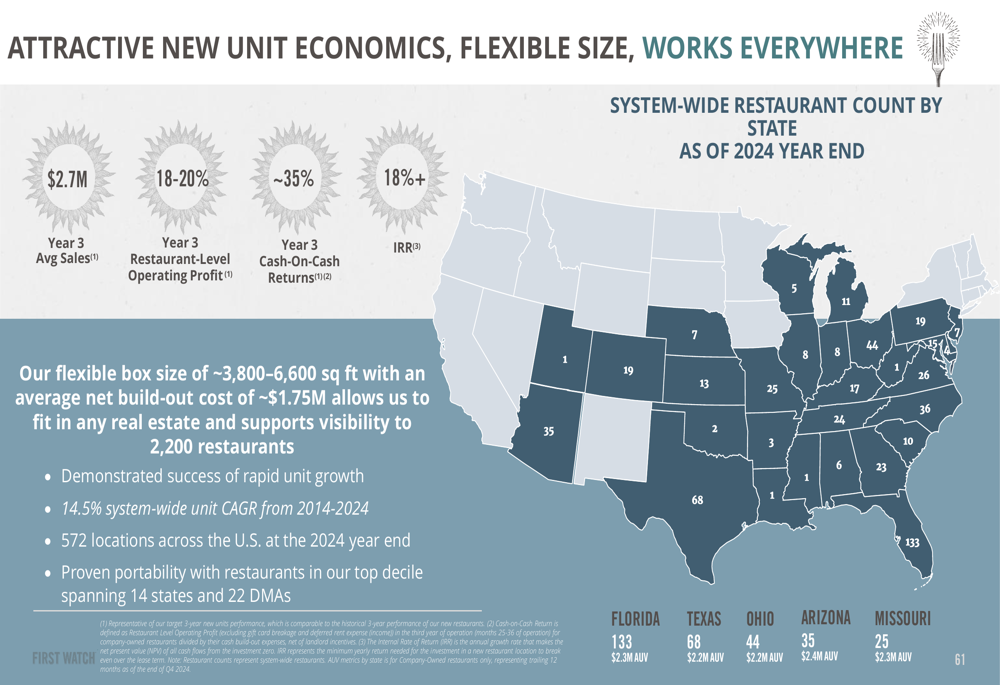

Despite profitability challenges, First Watch continues to execute its expansion strategy. The company opened 13 system-wide restaurants in 10 states during Q1 2025, with one closure, bringing the total to 584 system-wide restaurants (498 company-owned and 86 franchise-owned) across 30 states.

The company’s new unit economics remain attractive, with average Year 3 sales of $2.7 million, Year 3 restaurant-level operating profit of 18-20%, and Year 3 cash-on-cash returns of approximately 35%. First Watch maintains that its flexible box size (3,800-6,600 sq ft) and average net build-out cost of approximately $1.75 million provide visibility and growth potential to 2,200 restaurants, a significant increase from the current count.

First Watch continues to innovate with its menu offerings, introducing new items as part of seasonal promotions. During Q1, the company featured a "Jump Start" promotion from January 7 to March 17, 2025, which included items such as Parmesan Prosciutto Toast (NYSE:TOST), Carne Asada Hash, Raspberry Ricotta French Toast, and the Blue Booster juice.

For Q2, the company has launched a "Spring" promotion running from March 18 to June 2, 2025, featuring items like Bacon Cheddar Cornbread, Wild Berry Lavender French Toast, The B.E.C. breakfast sandwich, and the Pineapple Express juice.

Forward-Looking Statements

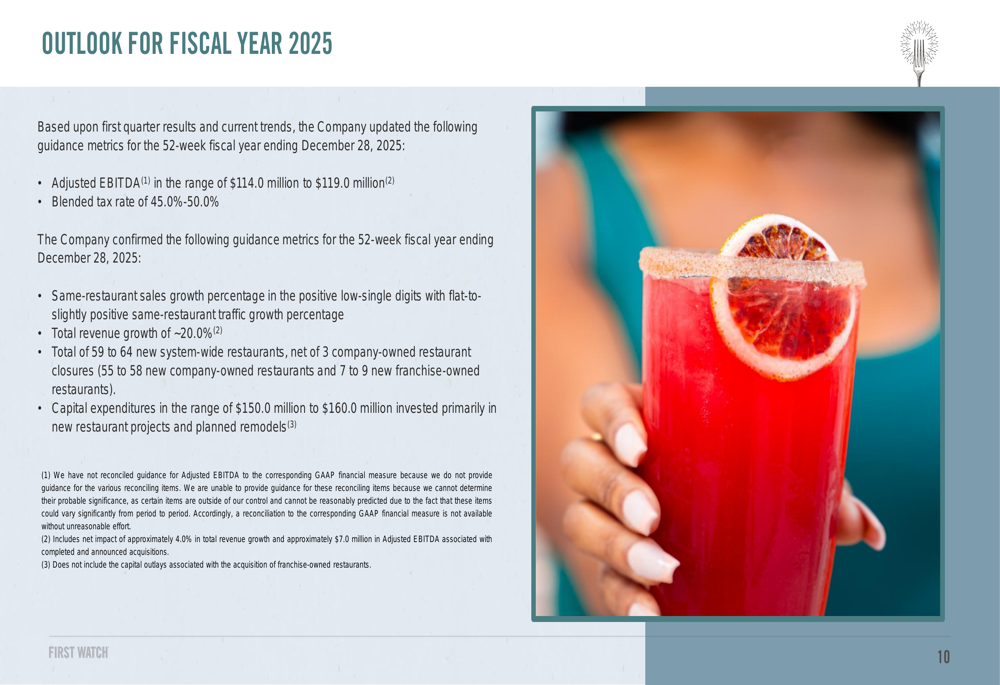

First Watch updated its guidance for the 52-week fiscal year ending December 28, 2025, projecting Adjusted EBITDA in the range of $114.0 million to $119.0 million. This represents a downward revision from the $124-130 million range mentioned in the previous quarter’s earnings call, suggesting some caution regarding profitability for the remainder of the year.

The company expects same-restaurant sales growth in the positive low-single digits with flat-to-slightly positive same-restaurant traffic growth. Total (EPA:TTEF) revenue growth is projected at approximately 20.0%, driven by both same-restaurant sales growth and new restaurant openings.

First Watch plans to open 59 to 64 new system-wide restaurants in 2025, net of 3 company-owned restaurant closures. This includes 55 to 58 new company-owned restaurants and 7 to 9 new franchise-owned restaurants. Capital expenditures are expected to be in the range of $150.0 million to $160.0 million, primarily for new restaurant projects and planned remodels.

While First Watch continues to demonstrate strong revenue growth and expansion capabilities, the decline in profitability metrics will likely be a key focus for investors in the coming quarters. The company’s ability to manage rising costs while maintaining its growth trajectory will be crucial for its long-term success in the competitive restaurant industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.