Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Fiserv Inc (NYSE:FI) released its first quarter 2025 financial results on April 24, revealing solid performance with 7% organic revenue growth and 14% adjusted earnings per share growth. Despite these positive results, the company’s shares dropped 7.93% in premarket trading to $199.89, suggesting investors may have expected stronger performance or raised guidance.

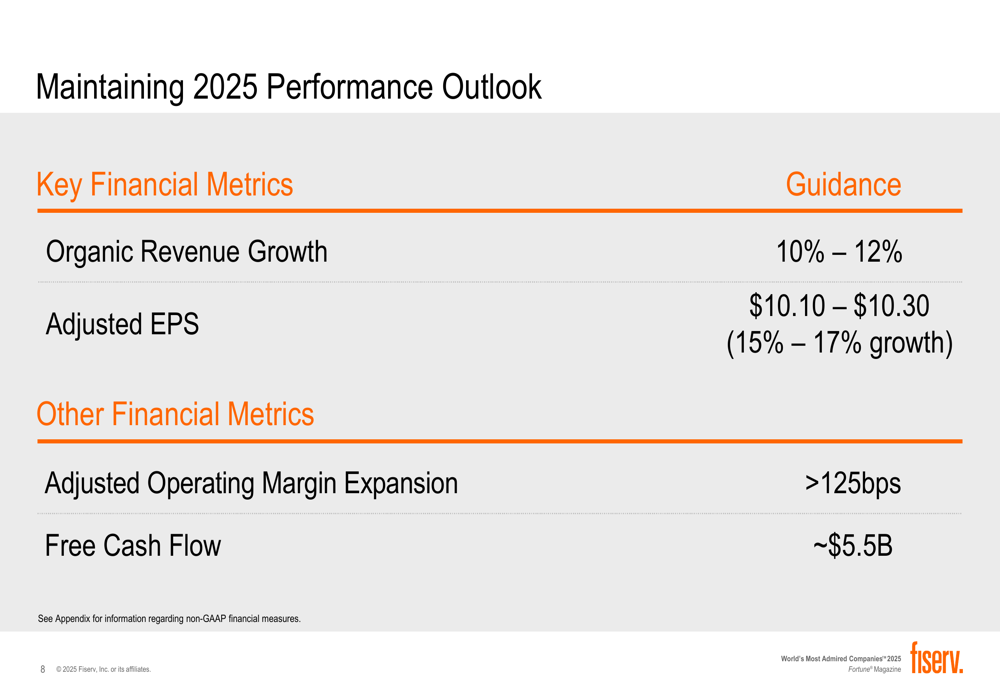

The global payments and financial services technology provider maintained its full-year 2025 guidance, projecting organic revenue growth of 10-12% and adjusted EPS of $10.10-$10.30, representing 15-17% growth over 2024.

Quarterly Performance Highlights

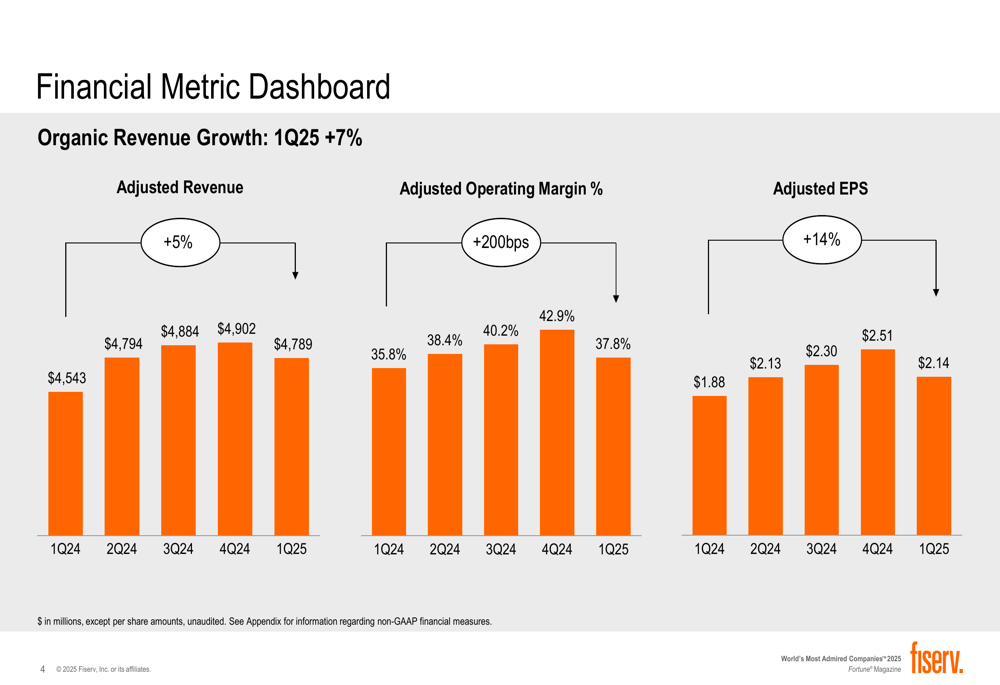

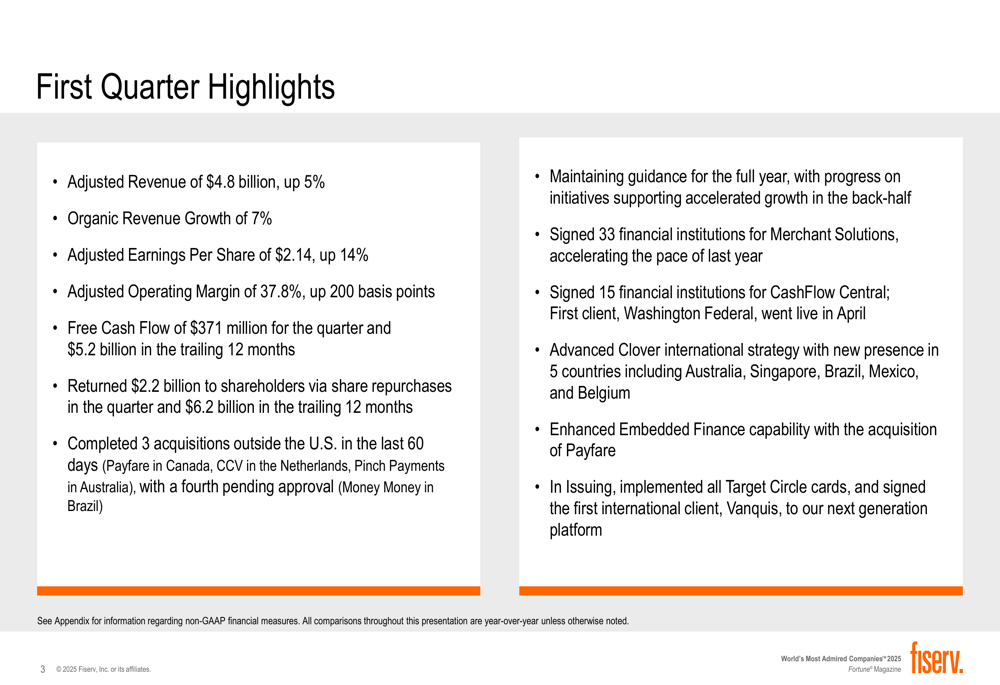

Fiserv reported adjusted revenue of $4.8 billion for the first quarter, representing a 5% increase compared to the same period last year. Organic revenue growth, which excludes the impact of acquisitions, divestitures, and foreign currency fluctuations, reached 7%.

As shown in the following financial metrics dashboard, the company has maintained consistent growth across key performance indicators over the past five quarters:

Adjusted earnings per share reached $2.14, up 14% year-over-year, while adjusted operating margin expanded by 200 basis points to 37.8%. Free cash flow for the quarter totaled $371 million, with trailing 12-month free cash flow reaching $5.2 billion.

The company’s first quarter highlights included several strategic initiatives alongside its financial performance:

Segment Analysis

Fiserv’s business is divided into two main segments: Merchant Solutions and Financial Solutions. Both segments showed positive growth in the quarter, though with varying performance across business lines.

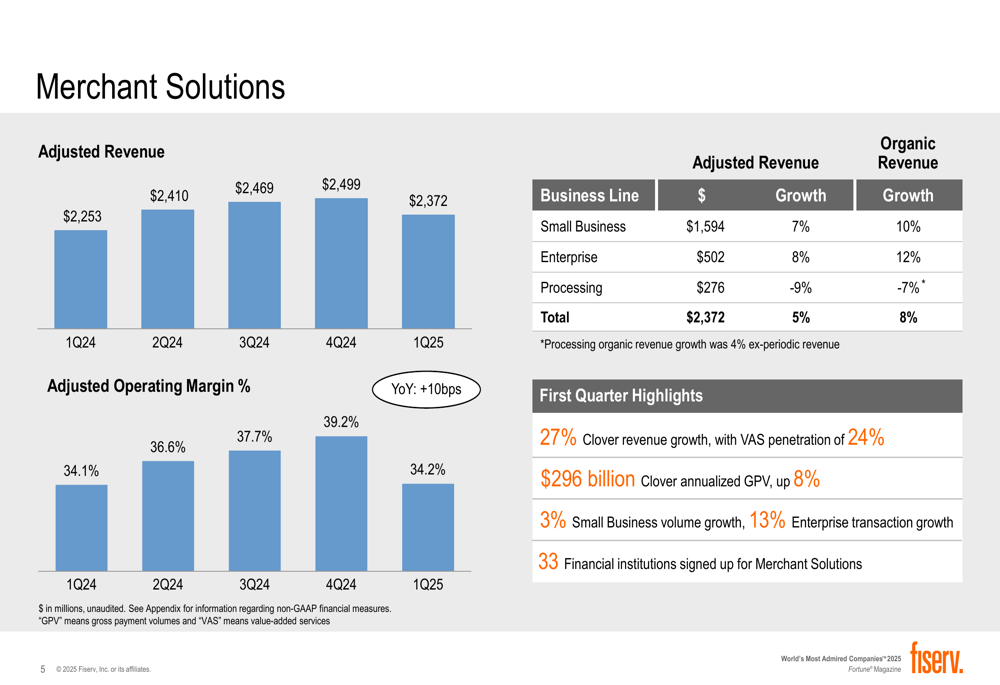

The Merchant Solutions segment, which includes the company’s payment processing services for merchants, generated $2.37 billion in revenue, up 5% year-over-year, with organic growth of 8%. Within this segment, Small Business and Enterprise business lines showed strong performance with organic growth of 10% and 12% respectively, while the Processing business line declined by 7% organically.

The following breakdown illustrates the performance of the Merchant Solutions segment:

Clover, Fiserv’s small business commerce platform, continued its strong performance with 27% revenue growth. The platform achieved 24% value-added services penetration and processed an annualized gross payment volume of $296 billion, up 8% year-over-year.

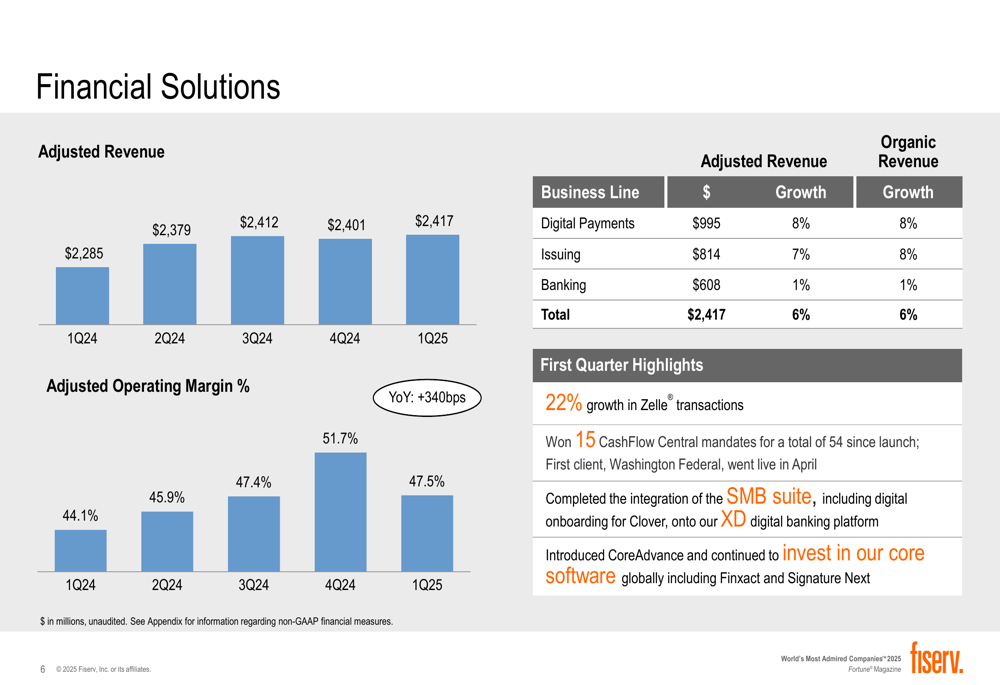

The Financial Solutions segment, which includes digital payments, issuing, and banking services, delivered $2.42 billion in revenue, representing 6% growth both on a reported and organic basis. Digital Payments was the strongest performer with 8% growth, followed by Issuing at 8% organic growth, while Banking showed more modest 1% growth.

The segment breakdown shows consistent performance across Financial Solutions business lines:

Capital Allocation & Cash Flow

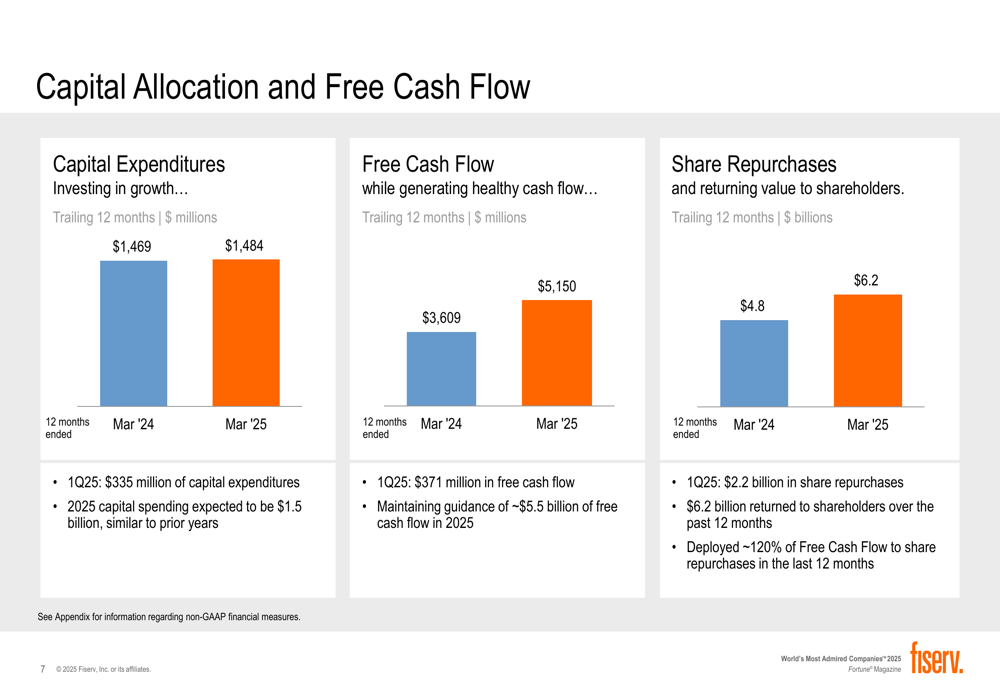

Fiserv continued its aggressive share repurchase program in the first quarter, returning $2.2 billion to shareholders. Over the trailing 12 months, the company has repurchased $6.2 billion worth of shares, representing approximately 120% of its free cash flow during that period.

Free cash flow for the quarter was $371 million, while trailing 12-month free cash flow reached $5.15 billion, a significant increase from $3.61 billion in the comparable prior-year period. Capital expenditures for the quarter totaled $335 million, with the company expecting full-year 2025 capital spending to be approximately $1.5 billion, similar to prior years.

The following chart illustrates Fiserv’s capital allocation and free cash flow performance:

Forward Outlook

Fiserv maintained its full-year 2025 guidance across all key metrics, projecting:

The maintained guidance suggests management’s confidence in accelerating growth throughout the remainder of the year to achieve the full-year targets, despite the first quarter’s 7% organic growth being below the annual target range of 10-12%.

During the quarter, Fiserv completed three acquisitions outside the U.S. and enhanced its embedded finance capabilities with the acquisition of Payfare. The company also signed 33 financial institutions for its Merchant Solutions and 15 financial institutions for CashFlow Central, demonstrating continued client acquisition momentum.

Market Reaction & Analysis

The negative premarket reaction to Fiserv’s results suggests investors may have been expecting the company to raise its full-year guidance, as it did following its strong Q3 2024 performance. The 7% organic revenue growth in Q1 2025 represents a deceleration from the 15% reported in Q3 2024, which may have contributed to investor concerns.

The decline in the Processing business line within Merchant Solutions (-7% organic growth) could also be raising questions about competitive pressures in that segment. Additionally, investors may have been looking for stronger performance in the Banking business line, which showed only 1% growth.

Despite these concerns, Fiserv’s overall performance remains solid with double-digit earnings growth, margin expansion, and strong free cash flow generation. The company’s continued investment in strategic initiatives and international expansion, coupled with its aggressive share repurchase program, suggests management remains confident in its long-term growth strategy.

As Fiserv moves through 2025, investors will be watching closely to see if the company can accelerate organic revenue growth to meet its full-year guidance of 10-12%, particularly in the face of potentially challenging macroeconomic conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.