Palantir a high-risk investment with ’a one-of-a-kind growth and margin model’

Introduction & Market Context

Fiserv Inc (NASDAQ:NYSE:FI) released its second quarter 2025 financial results on July 23, revealing solid performance across key metrics but trimming its full-year organic revenue growth guidance. Despite reporting 8% organic revenue growth and a 16% increase in adjusted earnings per share, the stock plummeted 13.21% in pre-market trading to $144.06, reflecting investor disappointment with the revised outlook.

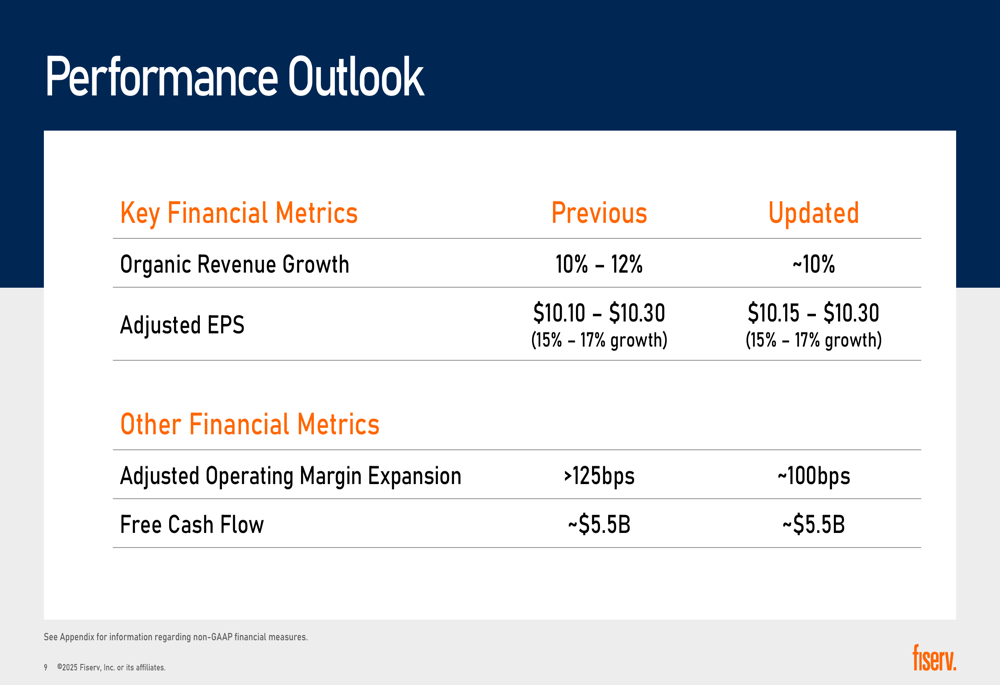

The financial technology giant, which provides payment processing and financial services technology, maintained its adjusted EPS guidance range but narrowed its organic revenue growth expectations from 10-12% to approximately 10%, signaling potential headwinds in the second half of the year.

Quarterly Performance Highlights

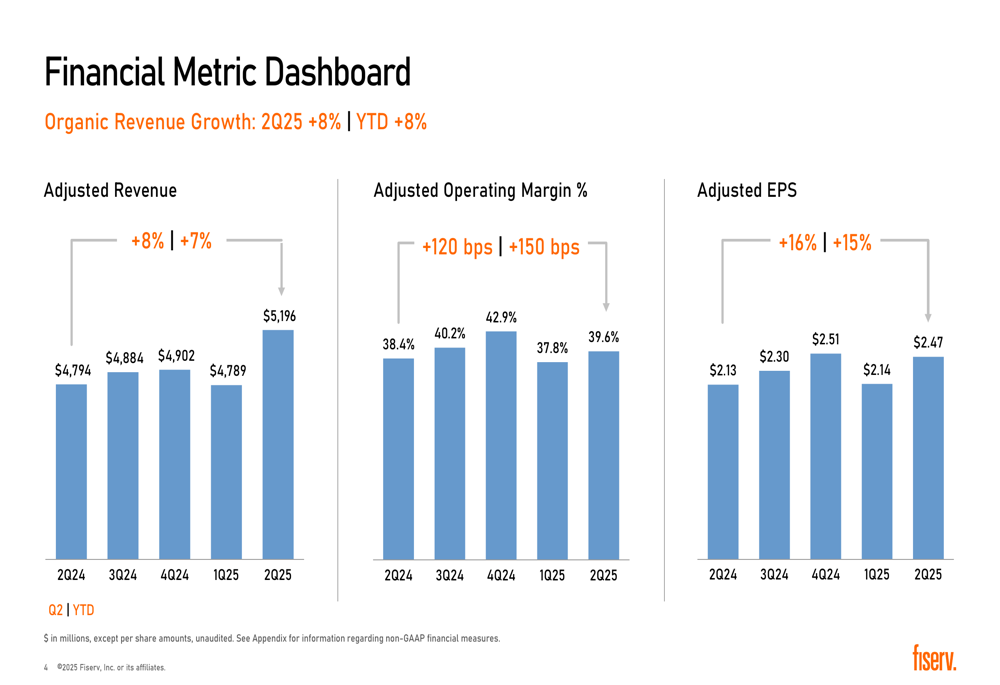

Fiserv reported adjusted revenue of $5.2 billion for Q2 2025, representing an 8% increase compared to the same period last year. Adjusted earnings per share reached $2.47, up 16% year-over-year, while adjusted operating margin expanded by 120 basis points to 39.6%.

As shown in the following financial metrics dashboard, the company has maintained consistent growth across key performance indicators throughout recent quarters:

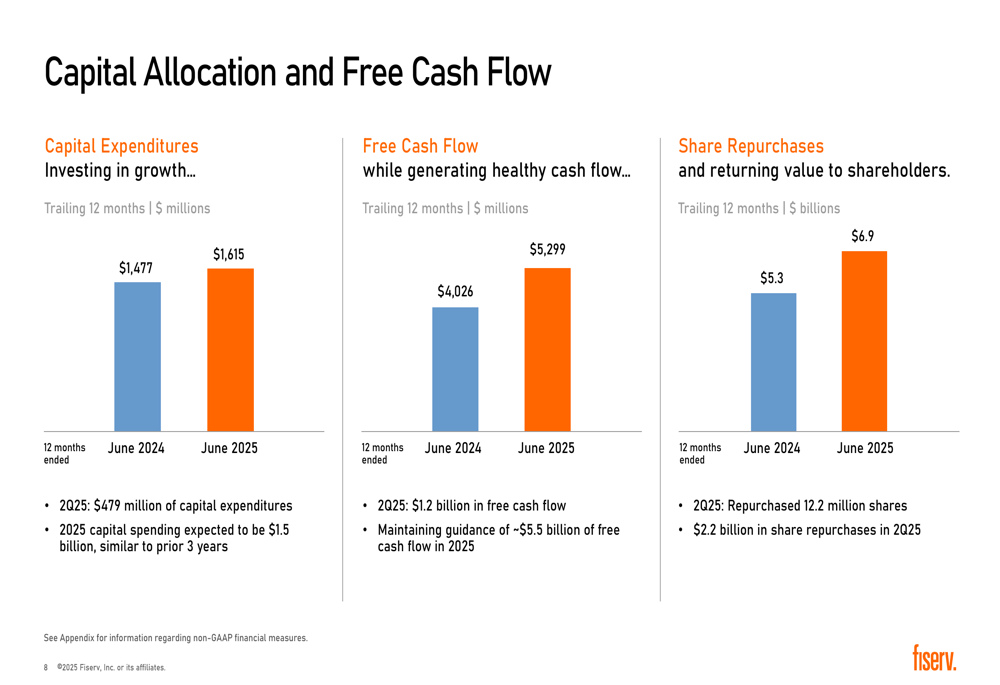

Free cash flow generation remained strong at $1.2 billion for the quarter and $5.3 billion for the trailing twelve months. The company continued its substantial share repurchase program, buying back 12.2 million shares for $2.2 billion in the second quarter alone, bringing the trailing twelve-month total to $6.9 billion.

Segment Performance Analysis

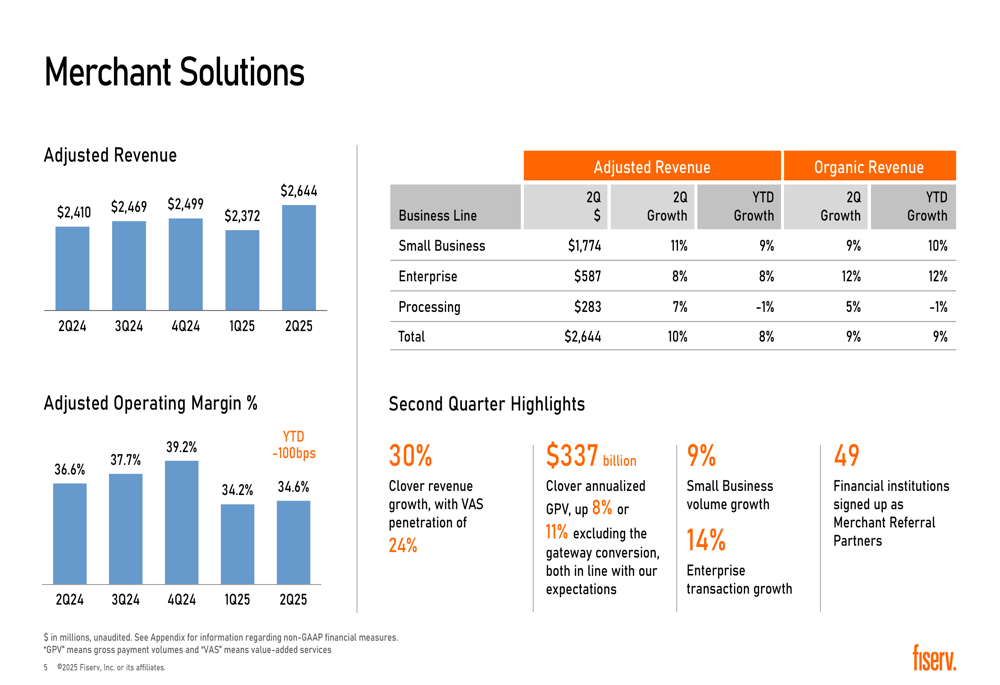

The Merchant Solutions segment, which includes Fiserv’s payment processing services for merchants, posted adjusted revenue of $2.64 billion, up 10% compared to Q2 2024. However, the segment’s adjusted operating margin decreased slightly to 34.6% from 36.6% in the prior year, representing a year-to-date decline of 100 basis points.

The following breakdown shows performance across the Merchant Solutions business lines:

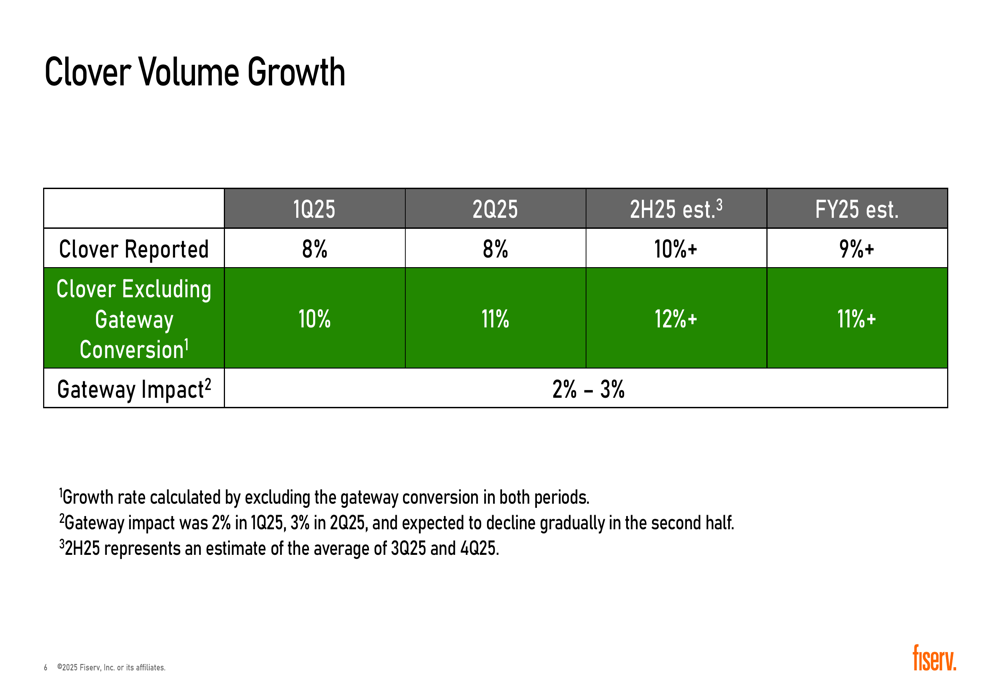

Clover, Fiserv’s small business payment platform, continued to show strong momentum with 30% revenue growth. However, Clover’s volume growth has been impacted by gateway conversions, as illustrated in the following chart:

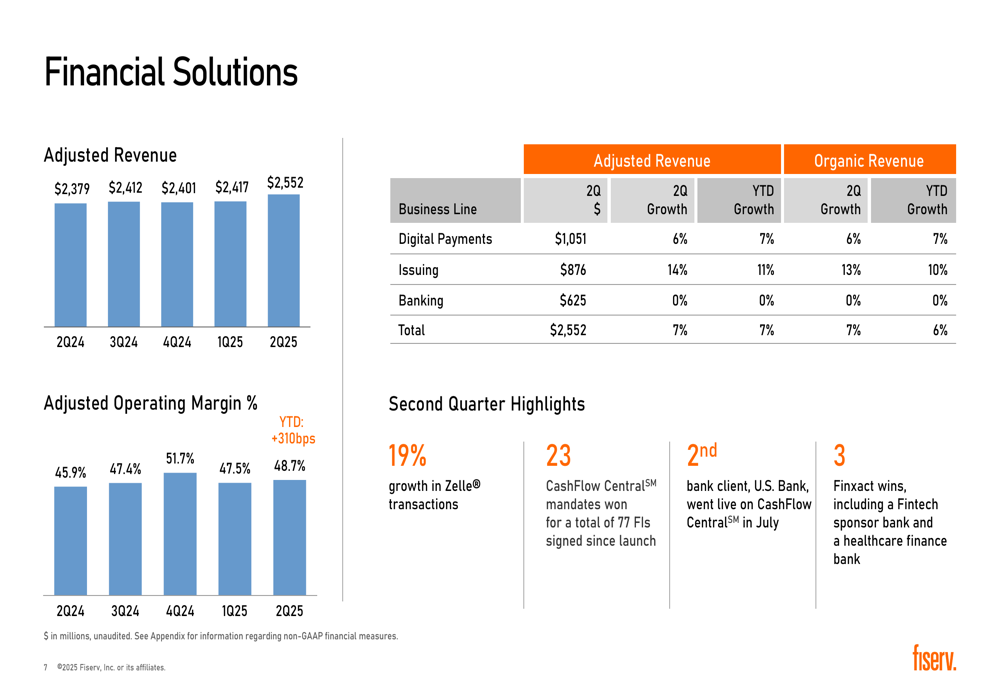

Meanwhile, the Financial Solutions segment delivered adjusted revenue of $2.55 billion, a 7% increase year-over-year. This segment demonstrated significant margin expansion, with adjusted operating margin reaching 48.7%, up from 45.9% in Q2 2024, representing a 310 basis point improvement year-to-date.

Strategic Initiatives

During the quarter, Fiserv announced several strategic moves to expand its global footprint and enhance its product offerings. The company reached an agreement to become the merchant processing provider for TD in Canada and to acquire a portion of TD’s existing merchant processing portfolio. Additionally, Fiserv agreed to acquire the remaining 49.9% of the AIB Merchant Services joint venture, strengthening its position in Ireland and Europe.

On the innovation front, Fiserv launched FIUSD stablecoin for financial institutions and merchants in partnership with Mastercard (NYSE:MA), PayPal (NASDAQ:PYPL), Circle, and Paxos. The company also highlighted 23 new mandates for its CashFlow Central platform, with U.S. Bank becoming the second bank client to go live on the platform in July.

These strategic initiatives align with Fiserv’s long-term growth strategy, despite the near-term adjustment to revenue guidance. The company’s recognition as one of TIME100 Most Influential Companies and inclusion in CNBC’s World’s Top Fintech Companies for 2025 underscores its industry leadership position.

Forward-Looking Statements

In a significant update that likely contributed to the negative market reaction, Fiserv refined its 2025 outlook, lowering organic revenue growth guidance and adjusted operating margin expansion targets:

While the company maintained its adjusted EPS guidance range of $10.15-$10.30, the upper end of which represents a 17% increase from 2024, the reduction in organic revenue growth expectations from 10-12% to approximately 10% suggests potential challenges in the second half of the year. Similarly, the adjusted operating margin expansion target was reduced from more than 125 basis points to approximately 100 basis points.

This guidance adjustment comes after the company’s Q1 2025 earnings release in April, which also saw a negative market reaction despite beating analyst expectations. At that time, Fiserv had maintained its full-year guidance, making the current revision particularly impactful for investor sentiment.

Detailed Financial Analysis

Fiserv’s second quarter results demonstrate the company’s ability to generate strong cash flow and maintain disciplined capital allocation. The company completed a public offering of €2.2 billion of senior notes with a weighted average coupon of 3.43%, indicating continued access to favorable financing terms despite the rising interest rate environment.

The company’s Small Business segment, which includes Clover, showed the strongest growth at 11% for the quarter and 9% year-to-date. Enterprise and Issuing segments also performed well, with growth rates of 8% and 14% respectively. However, the Processing segment showed signs of slowing, with 7% growth for the quarter but -1% year-to-date.

In the Financial Solutions segment, Digital Payments grew by 6%, while Issuing showed robust 14% growth. The Banking segment remained flat, potentially reflecting cautious technology spending by financial institutions in the current economic environment.

The company’s free cash flow conversion remains strong, enabling continued investment in growth initiatives while returning substantial capital to shareholders through share repurchases. Capital expenditures for Q2 2025 were $479 million, with full-year capital spending expected to be approximately $1.5 billion.

Despite the solid financial performance in Q2, the market’s negative reaction highlights investor concerns about growth sustainability and margin pressure, particularly in the Merchant Solutions segment. The revised guidance suggests that Fiserv may be facing increased competitive pressures or macroeconomic headwinds that could impact its performance in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.